Hydrogen Truck Market Report Scope & Overview:

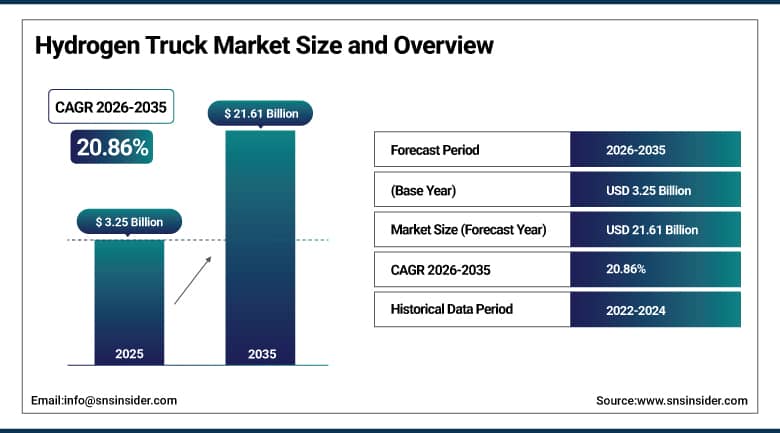

The Hydrogen Truck Market was valued at USD 3.25 Billion in 2025 and is expected to reach USD 21.61 Billion by 2035, growing at a CAGR of 20.86% from 2026–2035.

The global hydrogen truck market is at the frontier of the commercial vehicle industry’s decarbonisation transition, positioned as the zero-emission alternative that can address the range, refuelling speed, and payload performance requirements of heavy-duty long-haul freight that battery electric trucks currently struggle to serve economically. Hydrogen fuel cell electric trucks emit only water vapour at the tailpipe, can be refuelled in under 15 minutes, and can travel 500 to 1,000 kilometres on a full tank in configurations comparable to long-range diesel trucks, making them the most commercially viable zero-emission option for applications where mission profiles extend beyond the practical range of battery electric alternatives. The market’s commercial momentum is being accelerated by tightening zero-emission commercial vehicle mandates across the EU, California, and other major jurisdictions, the substantial government incentive programmes that are reducing the total cost of ownership premium of hydrogen trucks relative to diesel equivalents, and the growing commercial commitment of both established OEMs including Daimler Truck, Volvo Group, and Hyundai and new entrants including Nikola and Hyzon whose combined product pipelines are progressively expanding the range of available hydrogen truck configurations.

In 2024, global hydrogen truck deployments surged by 60%, with over 8,000 units ordered, primarily by logistics and freight operators, supported by a 40% expansion in refuelling infrastructure and USD 4.5 billion in government clean-transport incentives worldwide. This deployment acceleration demonstrates that hydrogen trucking has progressed beyond demonstration programmes into initial commercial adoption, with logistics operators and government incentive frameworks simultaneously creating the demand pull and economic support that sustains early market development ahead of the cost reductions that manufacturing scale-up will eventually deliver.

Hydrogen Truck Market Size and Forecast

-

Market Size in 2026E: USD 3.93 Billion

-

Market Size by 2035: USD 21.61 Billion

-

CAGR: 20.86% from 2026 to 2035

-

Fastest Growing Region: North America

-

Largest Region: North America

To Get More Information On Hydrogen Truck Market - Request Free Sample Report

Hydrogen Truck Market Trends

-

Growing government mandates for zero-emission commercial vehicles in the EU, California, and other major jurisdictions are accelerating fleet operator evaluation and procurement of hydrogen truck alternatives to diesel, particularly for long-haul freight routes where battery electric range limitations create operational constraints.

-

Rising investment in hydrogen refuelling infrastructure by energy companies, governments, and OEM-affiliated networks is progressively reducing the refuelling availability barrier that has been the primary operational constraint on hydrogen truck commercial adoption beyond fleet depot-based operation.

-

Increasing collaboration between hydrogen truck OEMs and logistics companies including DHL, Amazon, and IKEA whose sustainability commitments create early adopter demand is establishing commercial proof points that reduce perceived risk for subsequent fleet procurement decisions across the broader logistics sector.

-

Advancing fuel cell system efficiency, durability, and cost reduction through manufacturing scale-up is progressively improving hydrogen truck total cost of ownership parity with diesel, reducing the financial incentive requirement needed to justify fleet operator adoption decisions on commercial rather than purely regulatory grounds.

-

Growing integration of green hydrogen supply agreements between truck operators and renewable energy producers is enabling fleet operators to demonstrate end-to-end zero-carbon freight credentials that multinational corporate shipper sustainability reporting requirements increasingly demand from logistics service providers.

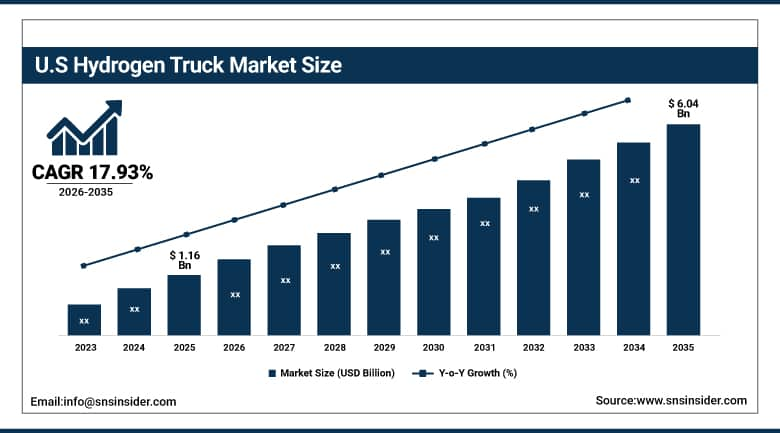

U.S. Hydrogen Truck Market Outlook

The U.S. Hydrogen Truck Market was valued at approximately USD 1.16 Billion in 2025 and is expected to reach approximately USD 6.04 Billion by 2035, growing at a CAGR of approximately 17.93%.

The United States is the world’s largest hydrogen truck market by revenue, driven by the combination of the most stringent commercial vehicle zero-emission mandate frameworks in California whose Advanced Clean Trucks regulation is compelling large fleet operators to begin transitioning from diesel to zero-emission alternatives, substantial federal and state financial incentives for hydrogen commercial vehicle procurement and infrastructure development under the Inflation Reduction Act and DOE Hydrogen Earthshot programme, and the active commercial deployment programmes of U.S.-headquartered hydrogen truck companies including Nikola Corporation and Hyzon Motors.

Nikola Corporation’s continued deployment of its Tre FCEV hydrogen fuel cell trucks in the U.S. market, combined with the simultaneous build-out of hydrogen refuelling infrastructure through its HYLA brand, represents the integrated vehicle-plus-fuel solution strategy that is considered essential for overcoming the chicken-and-egg infrastructure challenge that constrains hydrogen truck adoption. The vertical integration of truck supply and hydrogen fuel provision under a single commercial relationship simplifies the procurement decision for fleet operators whose primary operational concern is reliable fuel access at the scale their fleet size requires.

Hydrogen Truck Market Segment Analysis

-

By Propulsion Technology, Hydrogen Fuel Cell Electric dominated the market in 2025 through superior zero-emission performance, long range capability, and fast refuelling that makes it the preferred technology for long-haul commercial freight applications where battery electric alternatives face practical range and charging time constraints; Hydrogen Internal Combustion Engine is the fastest-growing propulsion technology.

-

By Truck Type, Heavy-Duty trucks dominated the hydrogen truck market in 2025 with the largest revenue share, reflecting their alignment with the long-haul freight applications where hydrogen’s range and refuelling advantages over battery electric are most commercially compelling; Medium-Duty trucks are the fastest-growing segment.

-

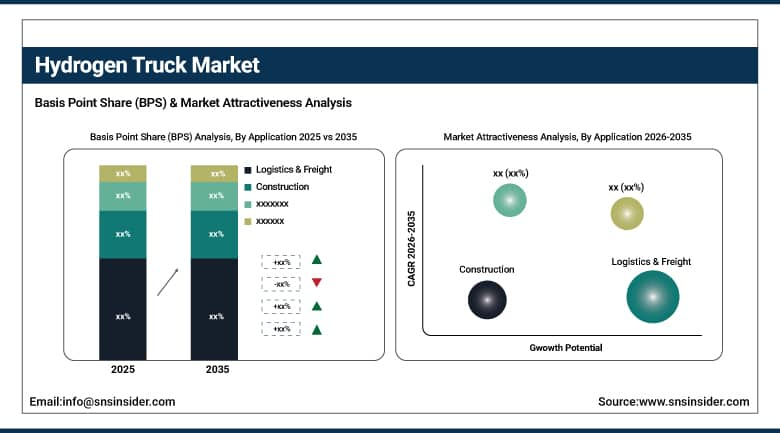

By Application, Logistics & Freight dominated the market in 2025 as the primary early adopter application where fleet operator sustainability commitments, customer demand for carbon-neutral freight services, and the long-haul mission profile that favours hydrogen over battery electric combine to create the strongest commercial adoption motivation; Construction is the fastest-growing application segment.

-

By End User, Fleet Operators dominated the hydrogen truck market in 2025 with approximately 66% revenue share, as centralised fleet ownership optimises the economics of dedicated refuelling infrastructure investment and enables operators to leverage OEM fleet purchasing programmes and government incentive aggregation that reduces per-vehicle total cost of ownership; Rental and Leasing providers are the fastest-growing end user segment.

By Application, logistics & freight dominates, construction grows fastest

Logistics and Freight retained the dominant application position in the hydrogen truck market in 2025, representing the commercial context in which hydrogen trucking’s value proposition most clearly surpasses battery electric alternatives and where the combination of fleet operator sustainability commitments, corporate shipper carbon-neutral freight demand, and long-haul mission profile requirements creates the strongest alignment of commercial motivation and technical performance matching. Major logistics companies including DHL, Schenker, and Maersk are deploying hydrogen trucks as part of emission reduction commitments that their corporate sustainability reporting frameworks and customer contract sustainability requirements make commercially necessary, creating the early adopter demand volumes that are essential for establishing the commercial viability of hydrogen truck operations before the cost trajectory reaches mass-market parity with diesel.

Construction is the fastest-growing application in the hydrogen truck market, driven by the recognition that heavy-duty construction vehicle operations represent one of the most practically suitable environments for hydrogen fuel cell technology given the combination of high-torque load requirements, extended operational hours without opportunity for charging, and the expanding environmental compliance requirements of construction project specifications that are increasingly mandating zero-emission construction equipment as a contract condition in municipal and government-funded infrastructure projects. Infrastructure development programmes in Europe, North America, and Asia Pacific are creating direct demand for zero-emission construction vehicles, and hydrogen trucks’ ability to deliver the torque, range, and fast refuelling that construction site operations require without the charging infrastructure limitations that battery electric alternatives face in remote or temporary construction site environments makes them the preferred zero-emission solution for heavy construction haulage and materials transport applications.

By Propulsion Technology, fuel cell electric dominates, hydrogen ICE grows fastest

Hydrogen Fuel Cell Electric retained the dominant propulsion technology position in the hydrogen truck market in 2025, establishing its commercial leadership through the superior zero-emission profile, long-distance range capability, and fast refuelling experience that make it the technology of choice for the heavy-duty long-haul freight applications that define the hydrogen truck market’s highest commercial value segment. Fuel cell electric trucks from Hyundai’s XCIENT platform, Daimler Truck’s Mercedes-Benz GenH2 Truck, and Nikola’s Tre FCEV collectively define the current commercial frontier of hydrogen truck capability, delivering operational range of 400 to 1,000 kilometres per fill and refuelling times of 10 to 20 minutes that provide a practical operational experience comparable to diesel long-haul trucking without the emissions that increasingly stringent commercial vehicle regulations are mandating away from fossil fuel alternatives.

Hydrogen Internal Combustion Engine trucks are the fastest-growing propulsion technology segment, driven by the technology’s unique commercial position as a near-zero emission alternative that leverages existing internal combustion engine manufacturing infrastructure, established supply chains, and familiar service and maintenance protocols in ways that fuel cell electric systems, whose components and service requirements are substantially different from conventional diesel powertrains, cannot replicate. The hydrogen ICE approach provides a lower-cost and more immediately manufacturable path to near-zero commercial vehicle emissions that is commercially attractive for fleet operators and OEMs in markets where fuel cell system cost remains prohibitive at current production volumes. Engine manufacturers including Cummins, Bosch, and Weichai Power are actively developing hydrogen ICE systems for commercial truck applications whose development timelines and production cost structures are more compatible with near-term fleet transition economics than full fuel cell electric system deployment.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

61.7% |

|

Middle East & Africa |

Saudi Arabia |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America Hydrogen Truck Market Insights

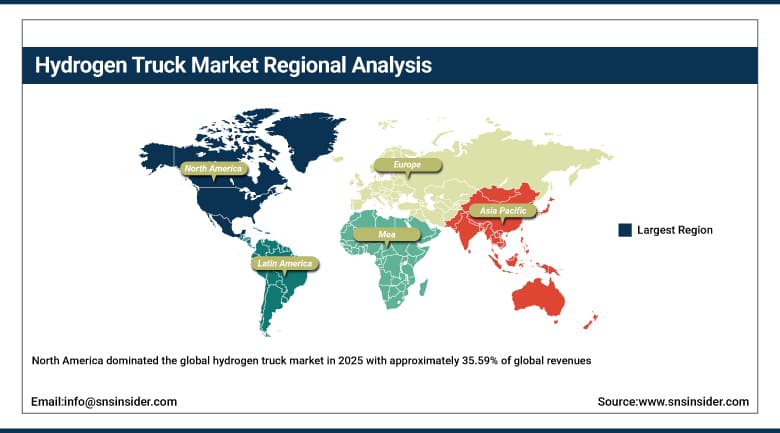

North America dominated the global hydrogen truck market in 2025 with approximately 35.59% of global revenues and is simultaneously the fastest-growing regional market at a projected CAGR of approximately 22.50% through 2033. The United States accounts for approximately 87.4% of North American revenues through its combination of the most commercially active hydrogen truck deployment programmes, the most substantial federal and state financial incentive framework, and the most advanced hydrogen truck commercial infrastructure development of any major market. California’s Advanced Clean Trucks regulation, which mandates progressive zero-emission vehicle sales percentages for truck manufacturers selling in the state, is creating compliance-driven demand that is pulling hydrogen truck procurement forward on timelines that commercial economics alone would not have produced at this stage of technology and infrastructure maturity.

Canada contributes approximately 12.6% of North American hydrogen truck revenues through provincial government clean transportation programmes in British Columbia and Ontario, the growing adoption of hydrogen trucks in mining and industrial logistics operations where hydrogen’s performance advantages over battery electric are most pronounced, and the developing relationship between Canada’s substantial clean hydrogen production potential and the commercial hydrogen truck fleet operations that can be served by domestically produced low-carbon hydrogen from renewable and nuclear sources whose cost trajectory is favourable relative to imported alternatives.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Hydrogen Truck Market Insights

Europe is a commercially sophisticated hydrogen truck market whose development is driven by the EU’s Fit for 55 and CO2 emission standards for heavy-duty vehicles whose progressive tightening is creating regulatory compliance motivation for hydrogen truck adoption among European truck manufacturers and fleet operators. Germany accounts for approximately 22.3% of European hydrogen truck revenues as the region’s largest national market, anchored by the domestic truck manufacturing presence of Daimler Truck and MAN Truck & Bus whose hydrogen truck development programmes are creating domestic supply, and the German logistics and freight industry’s early engagement with hydrogen truck pilot programmes that are building operator experience and commercial confidence. The European Hydrogen Backbone initiative and national hydrogen strategies across Germany, France, and the Netherlands are creating the public infrastructure investment that commercial hydrogen truck operators require for route-based long-haul operation beyond depot-based fleet charging.

Volvo Trucks’ and Scania’s European hydrogen truck development programmes, combined with Hyundai’s XCIENT commercial deployments in Switzerland and Germany, collectively demonstrate the commercial maturity of hydrogen truck technology for European operating conditions and regulatory environments. The EU’s Alternative Fuels Infrastructure Regulation mandating hydrogen refuelling station deployment along the Trans-European Transport Network core corridors is creating the infrastructure certainty that fleet operators require before committing to hydrogen truck procurement decisions at the scale that the market needs for commercially viable route network operation.

Asia Pacific Hydrogen Truck Market Insights

Asia Pacific is a large and rapidly growing hydrogen truck market whose development is led by China’s extraordinary combination of the world’s largest commercial vehicle fleet, the most ambitious domestic hydrogen vehicle deployment programmes, and the most substantial public hydrogen infrastructure investment of any national market globally. China accounts for approximately 61.7% of Asia Pacific hydrogen truck revenues through the commercial deployment programmes of domestic hydrogen truck manufacturers including Foton, Dongfeng, SAIC, and CNHTC whose production volumes are growing rapidly under National Hydrogen Energy Industry Development Plan support. The Rockcheck Group’s August 2025 deal to deploy 1,000 hydrogen-powered heavy-duty trucks by 2026 in a zero-carbon freight corridor in Baotou, Inner Mongolia exemplifies the scale of commercial deployment that Chinese government-backed programmes are enabling ahead of the cost parity timeline that unsubsidised market economics would produce.

South Korea represents the most technically advanced secondary hydrogen truck market in Asia Pacific, where Hyundai’s global leadership in hydrogen fuel cell truck technology is grounded in the company’s domestic commercial deployment experience and government-funded hydrogen mobility programme participation. Japan’s hydrogen society strategy and Toyota’s joint development of hydrogen fuel cell trucks with Hino Motors are creating a sophisticated domestic market and technology export capability whose commercial maturity is progressively demonstrating the viability of hydrogen truck technology across the range of operating conditions and logistics requirements that define commercial freight in developed Asian markets.

MEA & Latin America Hydrogen Truck Market Insights

The Middle East and Africa and Latin America are emerging hydrogen truck markets where sovereign wealth fund investment in green hydrogen production, industrial decarbonisation ambitions, and growing environmental awareness among large commercial fleet operators are creating the initial conditions for hydrogen truck market development ahead of the mass-market cost parity that would be required for adoption without public incentive support. Saudi Arabia leads Middle East and Africa hydrogen truck revenues at approximately 38.4% of the regional total, driven by NEOM’s commitment to operating 100% on renewable energy, which includes zero-emission freight and construction vehicle requirements, and the Kingdom’s substantial green hydrogen production ambition under Vision 2030 whose commercial realisation requires domestic hydrogen consumption markets including commercial vehicle fleets to anchor demand ahead of export market development.

Brazil leads Latin American hydrogen truck revenues at approximately 44.2% of the regional total through its mining and resource extraction sector whose heavy-duty vehicle operations are exploring hydrogen truck alternatives for deep-mine applications where diesel fume elimination improves worker safety and where the high operational hours and remote site locations create a practical use case for hydrogen trucks whose fast refuelling and high torque characteristics align with the operational requirements of large-scale open-cut and underground mining fleets in the country’s major iron ore, copper, and agricultural commodity export production regions.

Market Dynamics

Growth Drivers: Tightening zero-emission commercial vehicle regulations compelling fleet adoption, government incentive programmes reducing total cost of ownership premium

The primary structural growth driver for the hydrogen truck market is the progressive tightening of commercial vehicle emission regulations across major markets whose compliance requirements are creating non-discretionary fleet procurement motivation that moves hydrogen truck adoption from voluntary sustainability investment to regulatory necessity for the largest fleet operators most immediately affected by zero-emission vehicle mandate timelines. The government incentive landscape is simultaneously reducing the financial premium of hydrogen truck adoption, with purchase subsidies, tax credits, and favourable leasing terms collectively reducing the upfront cost differential that has historically been the primary barrier to operator adoption decisions. Infrastructure investment programmes including the EU’s Alternative Fuels Infrastructure Regulation and California’s hydrogen station development grants are creating the refuelling network density that commercial route-based operation requires, progressively expanding the geographic territory within which hydrogen truck commercial deployment is operationally viable.

Restraints: High vehicle purchase cost and hydrogen fuel price premium relative to diesel, limited refuelling infrastructure coverage creating range anxiety for non-depot-based operations

The most significant commercial restraint on the hydrogen truck market is the substantial vehicle purchase price premium relative to diesel equivalents, which ranges from two to four times the diesel purchase price at current production volumes, creating a financial barrier that only fleet operators with strong regulatory compliance motivation, access to government incentive support, or long-term sustainability commitments as defined commercial objectives can routinely overcome. The limited geographic coverage of public hydrogen refuelling infrastructure outside major corridor routes in California, Germany, and South Korea creates operational range anxiety for fleet operators whose routes extend beyond established refuelling point networks, restricting commercial hydrogen truck deployment to depot-based and point-to-point fixed route applications that account for only a portion of the total commercial freight market addressable by zero-emission technology.

Opportunities: Green hydrogen cost reduction trajectory improving long-term total cost of ownership competitiveness, hydrogen truck leasing and power-by-the-hour models reducing capital barriers

The green hydrogen cost reduction trajectory represents the most commercially significant long-term opportunity in the hydrogen truck market, as the combination of renewable energy cost decline, electrolyser manufacturing scale-up, and operational efficiency improvement across green hydrogen production facilities is projected to reduce green hydrogen fuel costs by 50 to 70% through the forecast period. This cost trajectory will progressively improve the total cost of ownership competitiveness of hydrogen truck operation relative to diesel without the continuing reliance on government subsidy that early commercial adoption currently requires, creating the conditions for accelerating market growth through commercial rather than regulatory and incentive-driven motivation. Power-by-the-hour and hydrogen truck leasing models that bundle vehicle, maintenance, and fuel supply into a single per-kilometre or per-hour commercial arrangement are reducing the capital barrier to adoption for mid-market fleet operators who cannot access direct government purchase incentives efficiently but can justify hydrogen truck adoption when the operational cost is packaged into a predictable operating expenditure commitment.

Recent Developments:

-

2024: Hyundai launched HTWO Grid, a global infrastructure and service platform supporting its XCIENT Fuel Cell hydrogen trucks, providing fleet operators with integrated hydrogen supply access, digital fleet management, and remote vehicle health monitoring across its growing international commercial deployment network in Europe, Asia, and North America.

-

2025: Daimler Truck introduced TruckForce, an AI-powered digital platform for its hydrogen and conventional truck fleets providing technicians with AI-assisted diagnostic guidance and predictive maintenance scheduling that improves service efficiency and reduces unplanned downtime for fleet operators managing mixed powertrains during the diesel-to-hydrogen transition period.

-

2025: Tata Motors initiated 24-month trials of 16 hydrogen-powered heavy-duty trucks with varied payload configurations for long-haul applications in India, building the operational data and commercial experience that the company will use to develop its commercial hydrogen truck product range for the Indian and broader South Asian market.

-

2025: August 2025 saw Rockcheck Group (Inner Mongolia, China) sign a deal to deploy 1,000 hydrogen-powered heavy-duty trucks by 2026 in a zero-carbon freight corridor in Baotou, representing one of the largest single commercial hydrogen truck procurement commitments in the global market and demonstrating the scale of adoption that Chinese government-backed commercial deployment programmes are enabling.

-

2025: Volvo Group expanded its hydrogen fuel cell truck testing programme in Europe with new long-haul route trials demonstrating commercial range capability under real freight conditions, building the operational evidence base that European fleet operators and transport authorities require to support procurement decisions for hydrogen trucks in scheduled inter-city and cross-border freight applications.

Hydrogen Truck Market Key Players

-

Hyundai Motor Company (XCIENT Fuel Cell)

-

Daimler Truck AG (Mercedes-Benz GenH2)

-

Volvo Group (Volvo Trucks)

-

Nikola Corporation

-

Hyzon Motors Inc.

-

Toyota Motor Corporation (with Hino Motors)

-

IVECO Group N.V.

-

PACCAR Inc. (Kenworth, Peterbilt)

-

Scania AB (Volkswagen Truck & Bus)

-

MAN Truck & Bus SE

-

Foton Motor Co., Ltd.

-

Dongfeng Motor Corporation

-

SAIC Motor Corporation

-

CNHTC (Sinotruk)

-

Weichai Power Co., Ltd.

-

Cummins Inc.

-

Bosch GmbH

-

Ballard Power Systems Inc.

-

Loop Energy Inc.

-

Yutong International Holding Co., Ltd.

Hydrogen Truck Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.25 Billion |

| Market Size by 2035 | USD 21.61 Billion |

| CAGR | CAGR of 20.86% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Propulsion Technology (Hydrogen Fuel Cell Electric, Hydrogen Internal Combustion Engine) • By Truck Type (Heavy-Duty, Medium-Duty, Light-Duty) • By Application (Logistics & Freight, Construction, Mining, Public Transportation, Others) • By End User (Fleet Operators, Rental & Leasing, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Hyundai Motor Company (XCIENT Fuel Cell), Daimler Truck AG (Mercedes-Benz GenH2), Volvo Group (Volvo Trucks), Nikola Corporation, Hyzon Motors Inc., Toyota Motor Corporation (with Hino Motors), IVECO Group N.V., PACCAR Inc. (Kenworth, Peterbilt), Scania AB (Volkswagen Truck & Bus), MAN Truck & Bus SE, Foton Motor Co., Ltd., Dongfeng Motor Corporation, SAIC Motor Corporation, CNHTC (Sinotruk), Weichai Power Co., Ltd., Cummins Inc., Bosch GmbH, Ballard Power Systems Inc., Loop Energy Inc., Yutong International Holding Co., Ltd |

Frequently Asked Questions

The Hydrogen Truck Market is expected to grow at a CAGR of 20.86% from 2026 to 2033.

The Hydrogen Truck Market was valued at USD 3.25 Billion in 2025.

Tightening zero-emission commercial vehicle regulations compelling fleet operator adoption, government incentive programmes reducing the total cost of ownership premium.

Hydrogen Fuel Cell Electric dominated the Hydrogen Truck Market in 2025.

North America dominated the Hydrogen Truck Market in 2025 with approximately 35.59% of global revenues, also being the fastest-growing regional market.

Get in Touch