Immersive Virtual Reality Market Report Scope & Overview:

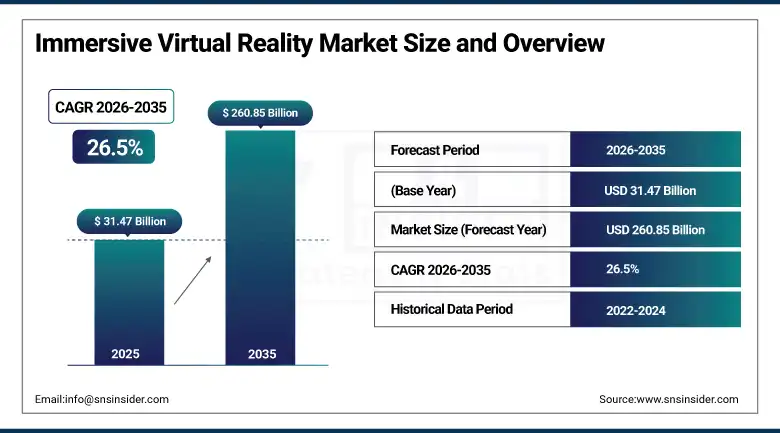

The Immersive Virtual Reality Market was valued at USD 31.47 Billion in 2025 and is expected to reach USD 260.85 Billion by 2035, growing at a CAGR of 26.5% from 2026–2035.

The global immersive virtual reality market is growing at an exceptional pace. Immersive virtual reality (VR) is an advanced technology that transports users into fully interactive, three-dimensional computer-generated environments through head-mounted displays, motion tracking systems, and haptic feedback devices whose combined sensory immersion creates the perception of physical presence in virtual space. The market is gaining traction across entertainment, healthcare, education, and automotive sectors driven by growing gen-Z population demanding realistic interactive content, continuous technological advancement in display resolution and tracking precision, and expanding enterprise training and collaboration applications.

In 2024, Meta Platforms launched Quest 3S, an entry-level mixed reality headset at USD 299 targeting the mainstream consumer market with color passthrough AR and standalone wireless VR capability, progressively lowering the price threshold that prevents mass consumer VR adoption. The USD 299 price point represents a significant accessibility milestone whose commercial implication for consumer VR market democratization creates new first-time buyer adoption from demographics whose USD 499 Quest 3 price previously created purchase hesitation.

Market Size and Forecast

-

Market Size in 2026E: USD 39.81 Billion

-

Market Size by 2035: USD 260.85 Billion

-

CAGR: 26.5% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific (~27.9% CAGR)

-

Largest Region: North America

To Get more information On Immersive Virtual Reality Market - Request Free Sample Report

Immersive Virtual Reality Market Trends

-

Adoption of standalone wireless VR headsets is increasing rapidly due to improved mobility, ease of use, and the elimination of external PC and cable requirements

-

Growing demand for immersive virtual collaboration and social VR platforms is supporting enterprise adoption for remote work, training, and communication applications

-

Healthcare providers are increasingly utilizing VR solutions for therapy, rehabilitation, pain management, surgical training, and mental health treatment

-

AI-powered content creation tools are reducing VR development costs and expanding the availability of immersive applications and experiences

-

Integration of eye-tracking technology is enhancing VR headset performance through foveated rendering, intuitive user interaction, and improved device efficiency

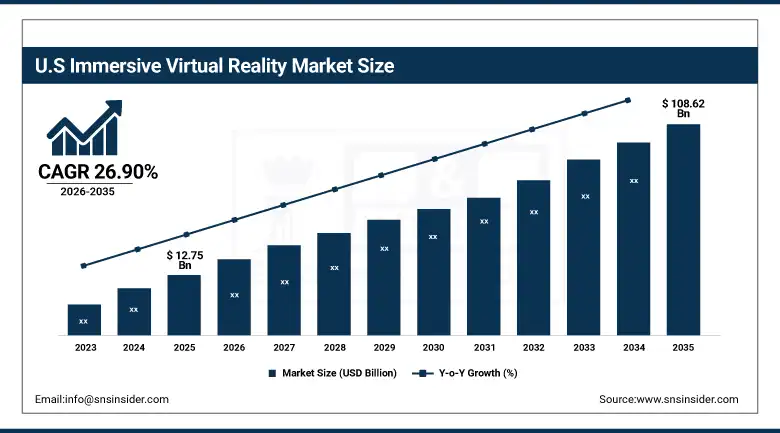

U.S. Immersive Virtual Reality Market Outlook

The U.S. Immersive Virtual Reality Market is estimated to be USD 12.75 Billion in 2025 and is projected to reach USD 108.62 Billion by 2035, growing at a CAGR of 26.90% during 2026–2035.

The U.S. Immersive Virtual Reality Market is the world’s most commercially significant national VR market within North America’s dominant position. Meta Platforms’ Quest ecosystem, Sony’s PlayStation VR2, Apple’s Vision Pro, and Valve’s Steam VR collectively define the domestic consumer and enterprise VR commercial landscape. The U.S.’s advanced gaming culture, enterprise digital collaboration investment, and healthcare AI adoption create the most commercially diverse VR application deployment of any national market. Military and defense’s virtual training programme creates premium enterprise VR procurement whose security requirements create structured institutional commercial relationships.

Sony Interactive Entertainment expanded its PlayStation VR2 game library in 2024 with over 300 VR-exclusive and VR-compatible titles, demonstrating the commercial commitment to content ecosystem development whose library breadth creates platform adoption motivation that hardware specification alone cannot sustain. The content library expansion reflects the commercial recognition that VR platform success requires software ecosystem density whose game variety creates daily usage motivation that prevents the headset abandonment that limited content libraries historically created in prior VR platform generations.

Immersive Virtual Reality Market Segment Analysis

-

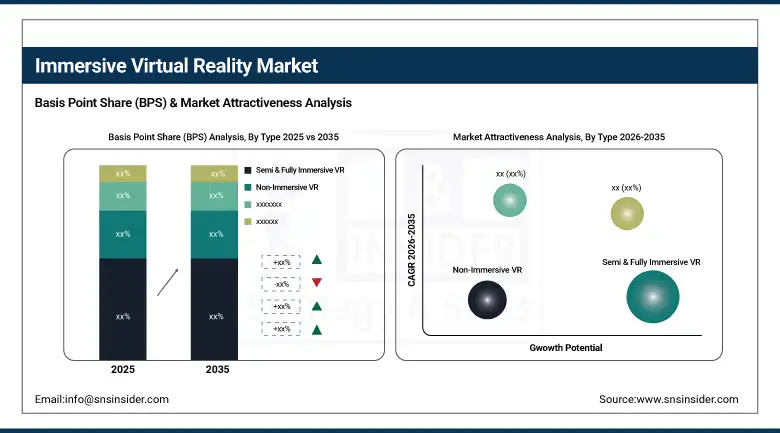

By Type, the Semi & Fully Immersive VR segment dominated the Immersive Virtual Reality Market with approximately 80% share in 2025, while the Non-Immersive VR segment is the fastest growing with a CAGR of approximately 29.97%.

-

By Component, the Hardware segment dominated the Immersive Virtual Reality Market with approximately 55% share in 2025, while the Software segment is the fastest growing.

-

By Application, the Gaming & Entertainment segment dominated the Immersive Virtual Reality Market with approximately 39% share in 2025, while the Healthcare segment is the fastest growing with a CAGR of approximately 31.56%.

-

By End User, the Consumer segment dominated the Immersive Virtual Reality Market with approximately 58% share in 2025, while the Enterprise/Commercial segment is the fastest growing.

By Type, semi & fully immersive dominates, non-immersive grows fastest

Semi and fully immersive VR retained the dominant type position with approximately 80% of the immersive virtual reality market in 2025. The six-degrees-of-freedom tracking, inside-out positional tracking, and visual immersion that high-end headsets create collectively define the VR experience whose quality drives consumer adoption and enterprise specification. Meta Quest 3’s color passthrough mixed reality, Sony PSVR2’s eye tracking and adaptive trigger controllers, and Apple Vision Pro’s spatial computing environment collectively demonstrate the commercial breadth of semi and fully immersive VR hardware whose premium per-unit pricing creates above-commodity revenue contribution. The gaming sector’s demand for the most immersive possible experience, the healthcare training programme’s simulation fidelity requirement, and the military’s operational environment replication needs collectively sustain semi and fully immersive VR’s dominant market position.

Non-immersive VR is the fastest-growing type at approximately 29.97% CAGR because the desktop-based VR software’s accessibility without headset investment creates adoption in education, business collaboration, and web-based applications whose participants lack either the budget or inclination for full headset VR investment. Each educational institution that deploys virtual campus tours, virtual laboratory simulations, or 360-degree field trip experiences through desktop non-immersive platforms creates adoption that compounds with digital education transformation. The metaverse collaboration platform’s non-immersive browser-based participation option creates enterprise adoption without VR hardware prerequisite.

By Application, gaming dominates, healthcare grows fastest

Gaming and entertainment retained the dominant application position with approximately 39% of the immersive virtual reality market in 2025. The gaming sector’s extraordinary VR content investment, encompassing major VR-exclusive titles, multiplayer social VR experiences, and the esports community’s VR format exploration, creates the most commercially significant aggregate VR application category. Each new VR gaming title release creates hardware adoption motivation whose content-hardware feedback loop sustains the gaming segment’s commercial leadership. The gaming community’s enthusiast culture creates above-average willingness to invest in premium VR hardware whose per-unit commercial value sustains hardware revenue growth.

Healthcare is the fastest-growing application at approximately 31.56% CAGR because VR’s clinical efficacy evidence is progressively creating structured institutional adoption beyond pilot programme deployment. Surgical training simulation’s documented error rate reduction, VR therapy’s clinical trial evidence for phobia treatment and PTSD management, and VR pain management’s opioid-reduction application collectively create clinical adoption motivation whose evidence-based character sustains procurement independent of technology enthusiasm. Each hospital that integrates VR surgical simulation into its residency training curriculum creates institutional procurement whose multi-year programme creates commercial stability.

By Component, hardware dominates, software grows fastest

Hardware retained the dominant component position with approximately 55% of the immersive virtual reality market in 2025. Head-mounted display’s per-unit commercial value, motion controller’s accessory procurement, and haptic feedback device’s premium specification collectively create hardware’s dominant commercial contribution to the VR market. Each new headset generation’s display resolution improvement, field of view expansion, and form factor reduction creates upgrade procurement whose timing compounds with consumer electronics replacement cycles. The enterprise’s multi-headset training lab investment creates institutional hardware procurement whose scale reflects the organization’s workforce training programme size.

Software is the fastest-growing component because the VR application ecosystem’s progressive maturation creates commercial content and platform investment whose growth rate exceeds hardware as the installed base creates developer monetization opportunity. Each VR game studio, medical simulation developer, and enterprise training content creator creates software ecosystem procurement whose aggregate across the growing VR content economy sustains software’s fastest-growing commercial momentum.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

United Kingdom |

28.4% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America Immersive Virtual Reality Market Insights

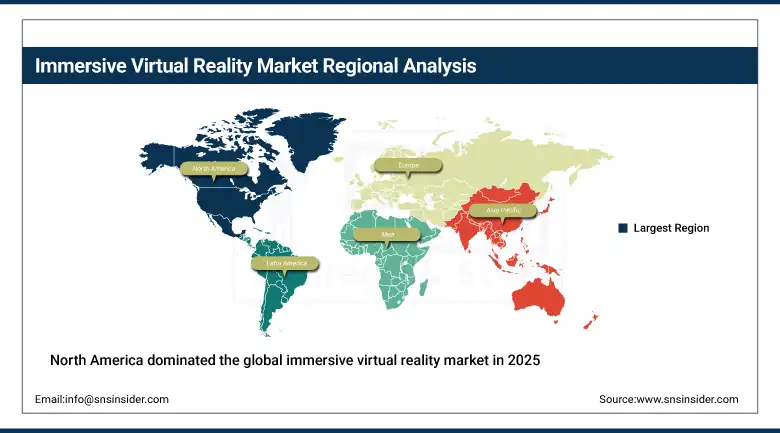

North America dominated the global immersive virtual reality market in 2025 with the largest revenue share of 34.6%. The United States accounts for approximately 87.4% of North American revenues through Meta Platforms’ Quest ecosystem leadership, Sony’s PlayStation VR2, Apple Vision Pro’s spatial computing premium market, and the enterprise VR training sector’s structured procurement. The U.S.’s advanced gaming culture and enterprise digital transformation investment sustain the world’s most commercially sophisticated VR market.

Canada contributes approximately 12.6% of North American revenues through its gaming industry’s VR content development, the enterprise training sector’s VR adoption, and the healthcare system’s clinical VR programme investment.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Immersive Virtual Reality Market Insights

Europe is a technically sophisticated VR market with a 22.4% global revenue share, driven by the UK’s strong gaming community, Germany’s industrial training VR adoption, and the healthcare system’s medical simulation investment. The United Kingdom leads European revenues at approximately 28.4% through its gaming industry’s VR development, the NHS’s clinical VR programme, and the enterprise training sector’s adoption.

Germany, France, and the Netherlands are significant secondary markets where industrial training simulation, automotive design VR, and healthcare training create consistent above-average enterprise VR procurement.

Asia Pacific Immersive Virtual Reality Market Insights

Asia Pacific is the fastest-growing regional VR market with a CAGR of approximately 27.9%, driven by China’s extraordinary gaming market’s VR adoption, South Korea’s advanced gaming culture, Japan’s enterprise VR training investment, and India’s rapidly growing consumer technology market. China accounts for approximately 44.8% of Asia Pacific revenues through its gaming sector’s VR hardware adoption, the government’s metaverse investment programme, and the enterprise training sector’s industrial simulation deployment.

South Korea’s Samsung and SK Telecom’s VR platform investment, Japan’s Sony’s PlayStation VR2 domestic market, and India’s growing gaming sector create significant secondary markets whose combined procurement sustains Asia Pacific’s fastest-growing regional status.

MEA & Latin America Immersive Virtual Reality Market Insights

UAE leads MEA revenues at approximately 38.4% through its extraordinary technology investment, the gaming and entertainment sector’s VR adoption, and the government’s metaverse initiative creating structured public sector VR procurement. Brazil leads Latin American revenues at approximately 44.2% through its large gaming community’s VR adoption, the growing enterprise training sector, and the healthcare system’s clinical VR programme.

Market Dynamics

Growth Drivers: Gaming content ecosystem maturation and enterprise workforce training VR adoption

The gaming content ecosystem’s progressive maturation is the immersive VR market’s most commercially consistent consumer demand driver. Each major game studio that develops VR-exclusive titles creates content that sustains hardware adoption motivation, and each VR hardware generation’s performance improvement sustains developer investment that expands the content library. The positive feedback loop between content quality improvement and hardware adoption creates self-reinforcing commercial momentum whose compound effect sustains above-average market growth. The streaming gaming platform’s cloud VR rendering capability is progressively creating quality VR experiences on lightweight wireless headsets whose convenience advantage creates consumer adoption accessibility.

Enterprise workforce training’s VR adoption creates the most commercially certain professional sector demand driver whose safety training, procedural skills development, and team collaboration applications create measurable ROI that sustains investment beyond technology enthusiasm. Boeing’s documented training time reduction, medical residency programme’s surgical simulation adoption, and military’s operational environment training collectively demonstrate enterprise VR’s financial justification whose measurement sustains procurement.

Restraints: VR motion sickness limiting session duration and high-quality content production cost

VR-induced motion sickness from display latency, refresh rate limitations, and vestibular-visual conflict creates user experience barriers that limit session duration and reduce the addressable consumer demographic below the potential addressable market. Each user whose motion sickness sensitivity creates physical discomfort in VR creates adoption barrier whose prevalence among approximately 25-40% of first-time VR users moderates mass consumer market penetration pace.

High-quality VR content production cost, requiring specialized development skills, extended development timelines, and above-standard game engine complexity, creates content availability limitations that prevent comprehensive application coverage across all potential VR use cases. Each new VR application category that requires custom content development creates investment barriers whose recovery requires sufficient installed base to justify the development economics.

Opportunities: Metaverse enterprise collaboration and healthcare clinical VR therapy regulatory approval

Enterprise metaverse collaboration platform represents the most commercially scalable VR opportunity whose distributed workforce’s virtual presence investment creates institutional adoption that compounds with remote work culture normalization. Each enterprise that deploys virtual collaboration environments for distributed team meetings, virtual product design reviews, and remote expert assistance creates VR procurement whose ROI measurement in travel cost elimination and collaboration quality improvement sustains programme expansion.

Healthcare clinical VR therapy’s regulatory approval pathway represents the most commercially premium near-term opportunity whose FDA and CE-cleared VR therapeutic device creates clinical procurement that sustains above-commodity pricing. Each new VR therapy clinical trial that achieves regulatory endorsement creates hospital and clinic procurement whose evidence-based adoption sustains commercial development.

Recent Developments:

-

2024: Meta Platforms launched Quest 3S at USD 299 in 2024, an entry-level mixed reality headset targeting mainstream consumer market democratization with color passthrough AR and standalone wireless VR capability, lowering the price threshold for first-time VR adoption.

-

2024: Sony Interactive Entertainment expanded its PlayStation VR2 game library in 2024 with over 300 VR-exclusive and VR-compatible titles, demonstrating content ecosystem development commitment whose library breadth creates platform adoption motivation beyond hardware specification.

-

2024: Apple expanded its Vision Pro spatial computing developer programme in 2024 with new visionOS APIs for enterprise application development, targeting industrial design, remote collaboration, and medical training applications beyond the consumer entertainment launch category.

Immersive Virtual Reality Market Key Players

-

Meta Platforms Inc.

-

Sony Interactive Entertainment

-

Apple Inc.

-

Microsoft Corporation

-

HTC Corporation

-

Valve Corporation

-

Google LLC

-

Samsung Electronics

-

HP Inc.

-

Pico Technology

-

Varjo Technologies Oy

-

Vuzix Corporation

-

Magic Leap Inc.

-

Lenovo Group Limited

-

Qualcomm Technologies

-

Unity Technologies

-

Epic Games Inc.

-

NVIDIA Corporation

-

Oculus (Meta)

-

Viveport

Immersive Virtual Reality Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 31.47 Billion |

| Market Size by 2035 | USD 260.85 Billion |

| CAGR | CAGR of 26.5% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Type (Semi & Fully Immersive VR, Non-Immersive VR) • by Component (Hardware/HMDs & Controllers, Software, Services) • by Application (Gaming & Entertainment, Healthcare & Medical Training, Education & Training, Manufacturing & Industrial, Retail & E-Commerce, Real Estate, Military & Defense, Others) • by End User (Consumer, Enterprise/Commercial) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Meta Platforms Inc., Sony Interactive Entertainment, Apple Inc., Microsoft Corporation, HTC Corporation, Valve Corporation, Google LLC, Samsung Electronics, HP Inc., Pico Technology, Varjo Technologies Oy, Vuzix Corporation, Magic Leap Inc., Lenovo Group Limited, Qualcomm Technologies, Unity Technologies, Epic Games Inc., NVIDIA Corporation, Oculus (Meta), Viveport |

Frequently Asked Questions

The Immersive Virtual Reality Market is expected to grow at a CAGR of 26.5% from 2026 to 2035.

The Immersive Virtual Reality Market was valued at USD 31.47 Billion in 2025.

Growing demand for realistic interactive gaming content and continuous technology advancements in display resolution, motion tracking, and haptic feedback, and expanding enterprise training and healthcare clinical applications whose ROI measurability creates institutional adoption beyond consumer gaming.

Semi & Fully Immersive VR dominated the Immersive Virtual Reality Market with approximately 80% share in 2025 as confirmed by SNS Insider, while Non-Immersive VR is the fastest growing at approximately 29.97% CAGR.

Gaming & Entertainment dominated the Immersive Virtual Reality Market with approximately 39% share in 2025, while Healthcare is the fastest growing at approximately 31.56% CAGR.

Get in Touch