Industrial Control Systems Market Report Scope & Overview:

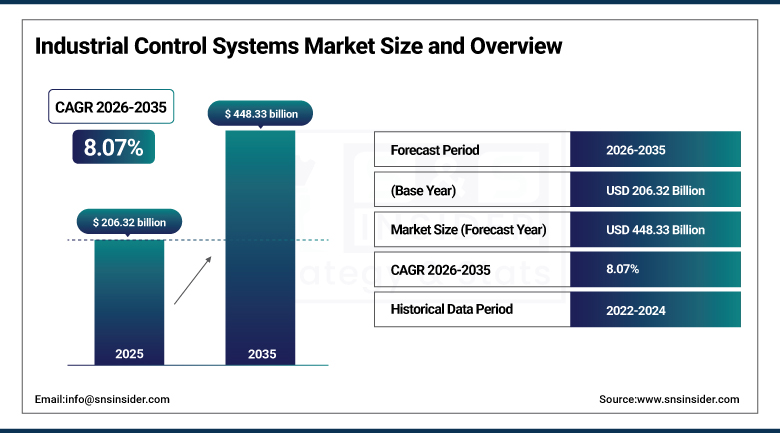

The Industrial Control Systems Market size was valued at USD 206.32 Billion in 2025 and is projected to reach USD 448.33 Billion by 2035, growing at a CAGR of 8.07% during 2026–2035.

The increasing implementation of automation in the entire plethora of industries would boost growth of the global industrial control systems market during the forecast period. Today, increasingly sophisticated ICS technologies enhanced by IoT, artificial intelligence and big data analytics are being deployed by manufacturers and industrial operators investing in digital automation solutions to minimize manual intervention and reduce operational costs. Globally, the momentum of smart manufacturing, trends like Industry 4.0, rising emphasis on safety and regulatory compliance across the oil and gas, healthcare, and manufacturing sectors are inspiring sustainable and broad-based demand for advanced integrated control systems spanning the 2026–2035 forecast period.

Structural demand driving ICS market growth: Some 58% of manufacturing executives, according to Deloitte 2024 survey, have plans to invest in automation technologies to drive productivity and lower costs, while 70% of manufacturers are expected to have embraced Industry 4.0 technologies, including IoT and AI, by 2025 per the World Economic Forum.

Industrial Control Systems Market Size and Forecast:

-

Market Size in 2025: USD 206.32 Billion

-

Market Size by 2035: USD 448.33 Billion

-

CAGR: 8.07% (from 2026 to 2035)

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Industrial Control Systems Market - Request Free Sample Report

Industrial Control Systems Market Highlights:

-

Rising automation adoption across manufacturing, energy, and utilities driving strong and sustained demand for advanced ICS solutions

-

Integration of IoT, AI, and big data analytics enhancing ICS capabilities with real-time monitoring, predictive maintenance, and intelligent process control

-

Industry 4.0 and smart manufacturing initiatives accelerating investment in integrated, connected industrial control infrastructure globally

-

Growing cybersecurity focus in ICS environments as increasing connectivity expands the attack surface and regulatory scrutiny intensifies

-

SCADA and HMI segments recording fastest growth as real-time data monitoring and user-friendly interfaces become operational priorities

-

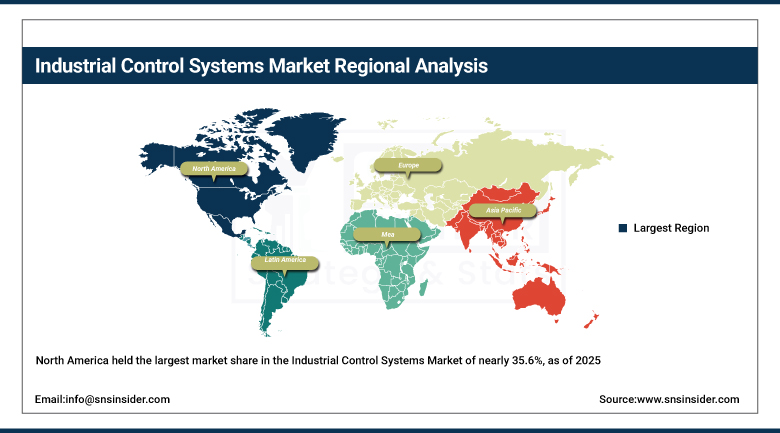

North America leads with 35.6% share in 2025, while Asia-Pacific is expected to register the fastest CAGR through 2026–2035

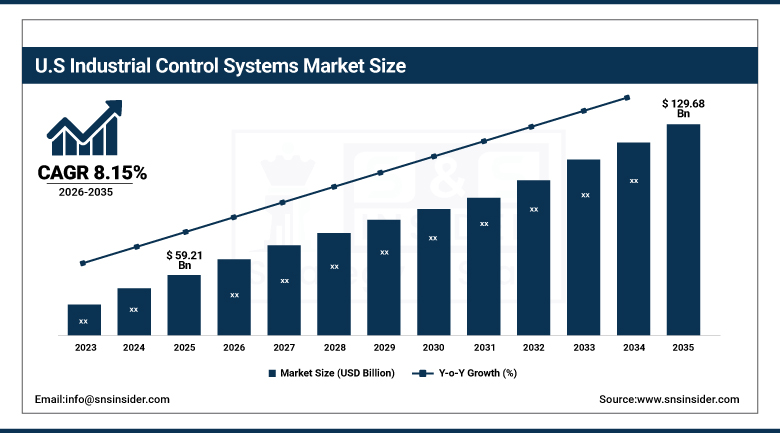

The U.S. Industrial Control Systems Market size was valued at USD 59.21 Billion in 2025 and is projected to reach USD 129.68 Billion by 2035, growing at a CAGR of 8.15% during 2026–2035.

Growth in the U.S. Industrial Control Systems Market is driven by U.S. has high existing industrial infrastructure investment, in the U.S. the presence of leading ICS developers like General Electric, Honeywell, consistent adoption of smart manufacturing technologies across energy, aerospace and advanced manufacturing sectors. As such, investment by Federal and state-level agencies in infrastructure modernization and transition to clean energy, are further fueling the demand for advanced ICS solutions, with one that is compatible with the new demands of renewable generation management and smart grid operations, through the forecast period.

AI-powered automation can increase manufacturing productivity by up to 20%, while improved safety management systems have demonstrated up to 40% reductions in incidents across the oil and gas industry quantifiable outcomes that are directly accelerating ICS investment across industrial sectors globally.

Industrial Control Systems Market Segment Highlights:

-

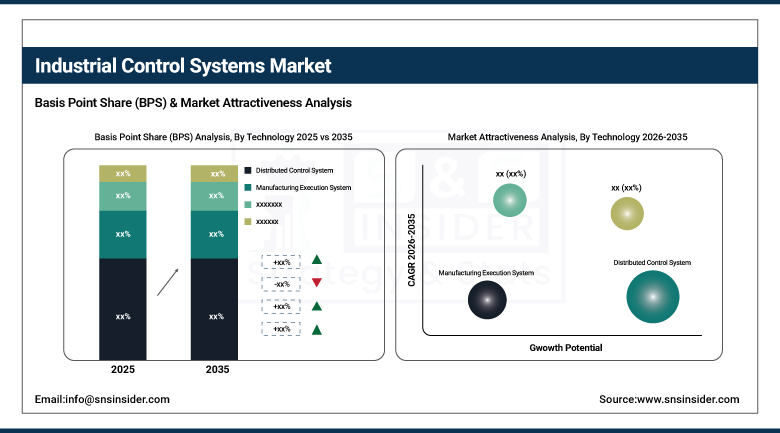

By Technology: Distributed Control System (Dominant – 32.6% share in 2025); SCADA (Fastest Growing through 2026–2035)

-

By Component: Remote Terminal Unit (Dominant – 24.6% share in 2025); Human-Machine Interface (Fastest Growing through 2026–2035)

-

By End Use: Manufacturing (Dominant – 16.6% share in 2025); Healthcare (Fastest Growing through 2026–2035)

Industrial Control Systems Market Segment Analysis:

By Technology - Distributed Control System Dominating and SCADA Fastest-Growing

The Distributed Control System segment dominated the Industrial Control Systems Market with an estimated revenue share of 32.6% in 2025 due to its proven capability and great flexibility to control various continuous industrial processes in oil & gas, chemicals, and power generation industry verticals. DCS architecture (distributed control system architecture) is better for highly reliable, fault-tolerant, and scalable large-scale system managements, and also well integrate with other contiguous technologies.

Increasing demand for real-time data monitoring to remotely control the process across utilities, transportation, and manufacturing is expected to lead to the fastest growth (CAGR) of SCADA during the period 2026–2035. With industrial digital transformation maturing, integrated IoT and data analytics capabilities progressively becoming a driving force behind operational decision-making, the SCADA adoption is anticipated to increase significantly across all major industrial end-use sectors.

By Component - Remote Terminal Unit Dominating and Human-Machine Interface Fastest-Growing

Remote Terminal Unit segment dominated component market share, contributing 24.6% of revenue in 2025, on account of the basic and fundamental function of Remote terminal units along with extensive use in industrial & oil and gas automation, water treatment, manufacturing, etc. RTUs take field device data and forward it to aggregated control systems where monitoring and decision making is done in real-time, allowing decision support and operational efficiency in remote and hostile environments that standard control systems cannot reliably endure.

The market for Human-Machine Interface (HMI) systems is projected to register the highest growth rate (CAGR) through 2026–2035, with demand from industrial operators driving a need for rich interfaces that allow the human to engage more fully with the automation system, better potential action to reduce the risk of human error, and broader control of increasingly complicated automated systems. Various technological advancements in touchscreen interfaces, high-end graphics, and augmented/ virtual reality based data visualization are expected to boost the HMI penetration in industrial sectors worldwide.

By End Use - Manufacturing Dominating and Healthcare Fastest-Growing

Manufacturing segment accounted for the largest end-use share with 16.6% in 2025, driven by the sector's essential reliance on ICS for line optimization and design, quality control, downtime reduction, and operational safety administration. Manufacturing sectors have a long history of deployment of DCS and SCADA which, combined with their ongoing investment in automation upgrades, cements DCS' hold on the top slot.

Healthcare will register the highest CAGR through 2026–2035 as widespread implementation of automated control systems in healthcare infrastructure—targeting sectors like remote patient monitoring, medication management, and surgical automation—fueled demand for ICS solutions that can develop utmost reliability and precision for meeting stringent reliability and safety specifications in clinical environments..

Industrial Control Systems Market Regional Analysis:

|

Region |

Major Country |

Share (%) |

|---|---|---|

|

North America |

United States |

35.6% |

|

Europe |

Germany |

22.0% |

|

Asia Pacific |

China |

27.0% |

|

Middle East & Africa |

Saudi Arabia |

8.0% |

|

Latin America |

Brazil |

7.4% |

North America Industrial Control Systems Market Insights:

North America held the largest market share in the Industrial Control Systems Market of nearly 35.6%, as of 2025, owing to the presence of a technologically-advanced manufacturing ecosystem, a high proportion of leading ICS developers, and considerable enterprise and government investment in industrial automation technologies. The US and Canada have usually been frontrunners of smart manufacturing adoption, as well as the integration of IoT, AI, and industrial automation technologies into different industrial areas. Key developers General Electric, and Honeywell have embedded ICS solutions deep within the U.S. energy, manufacturing, and aerospace sectors, enabling fundamental baseline adoption and repeat technology refresh cycles that keep most of these regional market leaders in place through 2035.

Investment by the U.S. Department of Energy in smart grid modernization, and clean energy infrastructure is generating new deployment opportunities for advanced industrial control and monitoring systems that are focused on renewables management, grid stability optimization, and real-time, national scale, energy distribution control.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia-Pacific Industrial Control Systems Market Insights:

Asia-Pacific is expected to register the highest CAGR in the Industrial Control Systems Market from 2026–2035 due to the rapid industrialization across China, India, Japan, South Korea, and the ASEAN economies. The 'Made in China 2025' strategy aiming for Chinese domination in advanced manufacturing has resulted in a flood of governmental and enterprise funds toward industrial automation, robotics, and control systems. Top international ICS developers such as Siemens and Mitsubishi Electric are making strong moves across Asia Pacific to fulfil soaring industrial automation demand.

Top vendors Siemens and Mitsubishi Electric are each making significant investments to expand their Asia-Pacific manufacturing automation operations in China and India, viewed by numerous manufacturing automation suppliers as the largest net global opportunities in advanced factory automation, distributed control systems and industrial IoT integration solutions through 2035 in the overall ICS market..

Europe Industrial Control Systems Market Insights:

Europe captured a sizeable portion of the Global Industrial Control Systems Market in 2025 owing to a robust industrial sector base, stringent regulatory legislation promoting safety and compliance along with strong adoption of Industry 4.0 technologies across manufacturing, chemical and energy sectors in the region. The base market includes Germany, France, Italy and the United Kingdom, all home to major ICS manufacturers, systems integrators and industrial automation users. Investment in advanced ICS solutions that support operational efficiency and environmental compliance requirements as the region focuses on energy transition, sustainable manufacturing, and cyber-resilient industrial infrastructure to meet needs through 2035.

Germany popularised the term "Industrie 4.0" and is now the prime market in Europe for smart manufacturing and industrial automation adoption, with its manufacturers among the most active worldwide deployers of integrated ICS solutions which combine DCS, SCADA, AI-based predictive maintenance and industrial IoT connectivity.

Middle East & Africa and Latin America Industrial Control Systems Market Insights:

Industrial control systems market in Middle East and Africa and Latin America witnessed a steady growth during 2025 owing to the expansion of oil and gas operations, surge in mining and metals sectors, and increase in government investment for modernization of industrial infrastructure. Oil and gas ICS deployments are a particularly significant segment of regional demand, with Saudi Arabia, the UAE, and South Africa the major Middle Eastern and African contributors. Brazil and Mexico have the largest Latin American markets, both featuring growing manufacturing and energy sectors that consistently procure ICS. From the forecast period, growing local demand for automation solutions, along with developing regional industrial infrastructure is complementing the market growth.

As the kingdom works to broaden its industrial base, Saudi Arabia is pursuing a Vision 2030 industrial diversification strategy that is behind significant investment in advanced manufacturing and energy infrastructure that will drive new ICS deployment opportunities in non-oil sectors, including petrochemicals, water management, and renewable energy.

Industrial Control Systems Market Drivers:

-

Cloud-based solutions and digital transformation accelerate adoption of flexible, scalable industrial control infrastructure globally

One of the biggest market trends is the move to cloud-based ICS solutions, where organizations migrate from expensive on-premises systems toward cloud architectures, providing increased flexibility, remote monitoring capability, and lower cost scalability. Cloud-based ICS gives organizations the means to access real-time operational data from anywhere with internet access, markedly enhancing management responsiveness and facilitating quicker incident response.

Key findings such as the fact that in a recent PwC survey the Company discovered 67% of manufacturers have already implemented or are planning cloud-based solutions designed to improve operations and that overall cloud-monitored organizations reported 40% downtime reduction present a significant operational case for the push of this technology throughout large swathes of industrial sectors around the World through 2035.

Industrial Control Systems Market Restraints:

-

Legacy system integration challenges and escalating cybersecurity demands create significant operational and financial barriers in ICS modernization

Integrating modern technologies with the legacy control systems that remain commonplace across many critical industrial facilities is a core challenge inhibiting the growth of the ICS market, as smart technology is proven to be challenging and costly to implement. The vast majority of industries rely on control systems that may have been in operation for years, having been designed at a time when modern connectivity, cybersecurity or interoperability requirements were not even on the horizon. Moving these environments over to modern ICS architectures is typically cumbersome, involving substantial downtime for system migrations, large capital investment, and complex engineering skills that organizations often cannot identify and/or fund at the same time.

CISA Advisory for a critical RAD Data Communications industrial network devices vulnerability, June 2024: The security of legacy and transitional ICS infrastructure will remain a pervasive and commercially relevant issue, as networked vulnerabilities that may impact critical industrial operations continue to be found and exploited remotely.

Industrial Control Systems Market Opportunities:

-

Smart Manufacturing, Energy Transition, and Healthcare Automation Create Expansive ICS Growth Opportunities Through 2035

This opens up several high-value growth opportunities for ICS solution providers across a global industrial sector through 2035. Smart manufacturing and Industry 4.0 adoption has increased the demand for automated and highly integrated controls systems, capable of autonomous, real-time optimization for complex, interconnected manufacturing processes with AI capabilities. The global clean energy transition is opening up a new range of ICS deployment requirements (e.g., for wind farm control, solar energy management, battery storage optimization and smart grid infrastructure) that are not suited to traditional fossil fuel generation systems, and therefore necessitates purpose-built control architectures. Combining large scale with the need for precision and regulatory standards that require leading-edge, purpose-built control technology solutions, the rapid automation of clinical processes including robotic surgical systems, remote patient monitoring infrastructure, and automated pharmaceutical manufacturing represents one of the fastest growing ICS application markets in the healthcare sector.

Nozomi Networks launched Arc Embedded, a security sensor for Mitsubishi Electric PLCs and other vendors in July 2024, enhancing visibility into industrial automation processes and allowing teams to quickly detect and remediate cyber threats of any severity without disrupting operations demonstrating the commercial opportunity in ICS-native security solutions that protect high-value industrial automation environments.

Recent Developments:

-

In July 2024, Nozomi Networks launched Arc Embedded, a security sensor for Mitsubishi Electric PLCs, providing enhanced industrial process visibility and enabling threat detection without operational disruption across automated manufacturing environments.

-

In June 2024, CISA issued an advisory regarding a critical vulnerability in RAD Data Communications SecFlow-2 devices, warning that the flaw could be remotely exploited with low attack complexity, reinforcing investment in ICS security monitoring and patching programs.

-

In May 2024, a Ransomhub ransomware group attack compromised the SCADA industrial control system of a Spanish bioenergy plant, demonstrating the growing operational risk of cyber threats targeting industrial control infrastructure globally.

Industrial Control Systems Companies are:

-

Siemens

-

Honeywell

-

Schneider Electric

-

Emerson

-

ABB

-

General Electric

-

Yokogawa

-

Omron

-

Panasonic

-

Beckhoff Automation

-

FANUC

-

B&R Industrial Automation

-

KUKA

-

Moxa

-

Hirschmann

-

Ametek

-

National Instruments

-

Endress+Hauser

Industrial Control Systems Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 206.32 Billion |

| Market Size by 2035 | USD 448.33 Billion |

| CAGR | CAGR of 8.07% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology (Integrated Control and Monitoring System (ICMS), Manufacturing, Execution System (MES), Distributed Control System (DCS), Safety Instrumented System (SIS), Supervisory Control and Data Acquisition) • By Component (Remote Terminal Unit (RTU), Human-Machine Interface (HMI), Surge Protectors, Marking Systems, Modular Terminal Blocks, Others) • By End Use (Aerospace & Defence, Automotive, Chemical, Energy & Utilities, Food & Beverage, Healthcare, Manufacturing, Mining & Metal, Oil & Gas, Transportation, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Siemens, Honeywell, Schneider Electric, Rockwell Automation, Emerson, ABB, General Electric, Mitsubishi Electric, Yokogawa, Omron, Panasonic, Beckhoff Automation, FANUC, B&R Industrial Automation, KUKA, Moxa, Hirschmann, Ametek, National Instruments, Endress+Hauser. |

Frequently Asked Questions

Ans: North America dominated the Industrial Control Systems Market in 2025 with approximately 35.6% revenue share, while Asia-Pacific is expected to register the fastest CAGR through 2035.

Ans: Distributed Control System dominated with approximately 32.6% revenue share in 2025, while SCADA is the fastest-growing technology segment through 2035.

Ans: Growth is driven by increasing industrial automation adoption, cloud-based ICS modernization, Industry 4.0 implementation, growing cybersecurity investment in industrial environments, and expanding healthcare and energy sector automation requirements.

Ans: The Market was valued at USD 206.32 Billion in 2025 and is projected to reach USD 448.33 Billion by 2035.

Ans: The Industrial Control Systems Market is expected to grow at a CAGR of 8.07% during 2026–2035.

Get in Touch