Industrial Salt Market Report Scope & Overview:

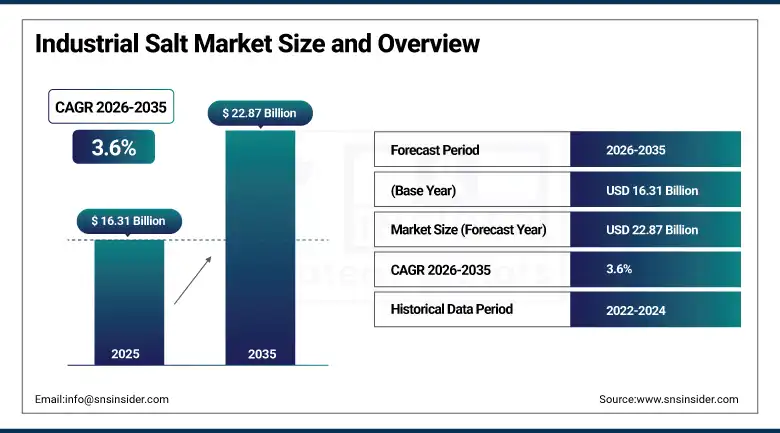

The Industrial Salt Market was valued at USD 16.31 Billion in 2025 and is expected to reach USD 22.87 Billion by 2035, growing at a CAGR of 3.6% from 2026–2035.

The global industrial salt market is advancing at a reliable and commercially broad-based pace. Industrial salt, sodium chloride sourced from underground mines, natural brines, and sea evaporation, serves as a foundational raw material across chemical processing, water treatment, de-icing, oil and gas drilling, and agricultural applications. Chemical processing, particularly chlor-alkali production generating chlorine and caustic soda, consumes the largest industrial salt volume globally. Growing urbanisation and infrastructure development are sustaining de-icing demand in cold-climate regions. Water treatment expansion for municipal drinking water and industrial effluent is creating structured demand.

In February 2023, Invest International provided a USD 13.6 million loan facility for Egyptian Salt Industry Co. (ESIC) to establish a salt refining industrial plant in Egypt using technology and equipment from Titan Salt B.V., a Dutch firm. The investment reflects the growing commercial interest in developing industrial salt refining capacity in the Middle East and Africa to serve regional chemical processing, water treatment, and food industry demand reducing dependence on salt imports from established production markets.

Market Size and Forecast

-

Market Size in 2026E: USD 16.90 Billion

-

Market Size by 2035: USD 22.87 Billion

-

CAGR: 3.6% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Industrial Salt Market - Request Free Sample Report

Industrial Salt Market Trends

-

Chlor-alkali industry expansion in Asia Pacific and emerging markets is creating above-average industrial salt demand as new chlorine and caustic soda capacity commissioned for PVC.

-

Eco-friendly de-icing salt development including magnesium chloride and calcium magnesium acetate formulations is responding to environmental concerns about sodium chloride's impact on vegetation, and infrastructure corrosion in cold-climate applications.

-

Water treatment industry expansion driven by municipal infrastructure investment and industrial effluent treatment regulatory compliance is creating growing demand for softening salt and brine regeneration applications across municipal and industrial water treatment facilities.

-

Vacuum salt production process adoption is growing as food-grade and pharmaceutical-grade industrial salt specifications require the higher purity, controlled crystal size.

-

Solar salt production facility investment is expanding capacity across Australia, India, and the Middle East where climate conditions enable cost-competitive large-scale solar evaporation whose environmental footprint.

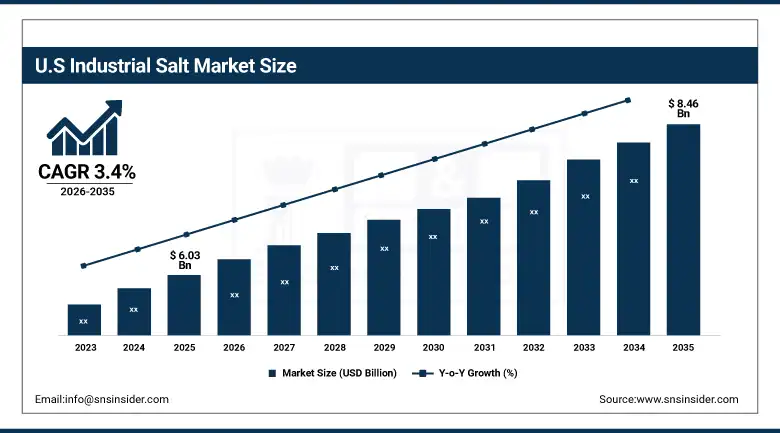

U.S. Industrial Salt Market Outlook

The U.S. Industrial Salt Market was valued at approximately USD 6.03 Billion in 2025 and is expected to reach approximately USD 8.46 Billion by 2035, growing at a CAGR of approximately 3.4%.

The U.S. is the world's most commercially significant industrial salt market within North America's leading revenue position. Cargill Salt, Compass Minerals, and Morton Salt collectively serve the majority of U.S. commercial procurement across de-icing, chemical processing, and water treatment applications. The U.S. de-icing market, concentrated in the northeastern and midwestern states' highway maintenance programmes, creates above-average per-capita salt procurement relative to temperate climate markets. The chemical processing industry's chlor-alkali production, centred in the Gulf Coast, represents the highest-value single industrial salt application in the domestic market whose procurement sustains consistent above-average commercial demand through chemical commodity cycle variation.

In 2024, Morton Salt partnered with Cargill to expand vacuum salt production capacity in the Great Lakes region, targeting growing demand from water softening and food-grade industrial salt applications. The partnership reflects the commercial recognition that vacuum salt's superior purity specification increasingly differentiates it from lower-purity rock and solar salt alternatives in the premium water treatment and food processing market segments whose specification requirements sustain premium pricing above commodity salt alternatives.

Industrial Salt Market Segment Analysis

-

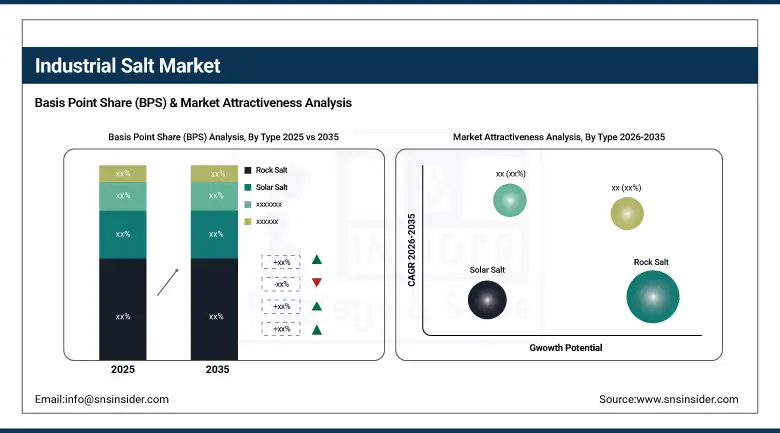

By Type, the Rock Salt segment dominated the Industrial Salt Market with approximately 45% share in 2025, while the Solar Salt segment is the fastest growing with a CAGR of approximately 4.8%.

-

By Source, the Natural Brine segment dominated the Industrial Salt Market with approximately 55% share in 2025, while the Salt Mines segment is the fastest growing.

-

By Application, the Chemical Processing segment dominated the Industrial Salt Market with approximately 36.7% share in 2025, while the Chemical Processing segment also holds the fastest CAGR.

-

By End User, the Chemical Industry segment dominated the Industrial Salt Market with approximately 40% share in 2025, while the Water Utilities segment is the fastest growing with a CAGR of approximately 5.2%.

By Type, rock salt dominates, solar salt grows fastest

Rock salt retained the dominant type position with approximately 45% of the industrial salt market in 2025. Its commercial primacy reflects the geological abundance of rock salt deposits in North America, Europe, and China whose proven reserve base sustains large-scale conventional mining at competitive cost levels. Rock salt's suitability for road de-icing applications, where particle size uniformity, spreading equipment compatibility, and bulk transport economics favour conventional mined salt over alternative forms, creates consistent high-volume procurement in cold-climate markets whose transportation and municipal infrastructure maintenance programmes generate above-average annual demand. The U.S. highway salt market alone consumes tens of millions of tonnes annually from established Midwestern and Appalachian rock salt mining operations.

Solar salt is the fastest-growing type at approximately 4.8% CAGR because large-scale solar evaporation investment in Australia, India, Mexico, and the Middle East is expanding cost-competitive salt production capacity for chemical processing and chlor-alkali applications whose bulk procurement economics favour solar salt's lower per-tonne production cost relative to vacuum-evaporated alternatives. Each new solar salt facility commissioned creates multi-decade production capacity whose competitive pricing drives market share expansion against conventional mining in transport-cost-accessible markets.

By Application, chemical processing dominates and grows fastest

Chemical processing retained the dominant application position with approximately 36.7% of the industrial salt market in 2025. The chlor-alkali industry's electrolytic conversion of brine into chlorine and caustic soda, which serve as foundational raw materials for PVC, paper bleaching, pharmaceutical manufacturing, textile treatment, and water disinfection, creates the most commercially concentrated and high-value industrial salt demand of any application category. Each tonne of chlorine produced requires approximately 1.75 tonnes of sodium chloride as electrolytic feedstock, creating a structurally fixed stoichiometric relationship between chlorine production volume and industrial salt consumption that sustains procurement proportionality with chemical industry output growth.

Chemical processing is simultaneously the fastest-growing application because Asia Pacific's rapid expansion of chlor-alkali capacity for PVC and chemical manufacturing is creating above-average new demand that the established North American and European markets cannot generate through replacement demand alone. China's chlor-alkali industry capacity expansion, India's chemical manufacturing investment, and Southeast Asia's industrial development collectively represent a chemical processing salt demand growth pool whose commercial scale substantially exceeds the mature market's incremental consumption increases.

By Source, natural brine dominates, salt mines grow fastest

Natural brine retained the dominant source position with approximately 55% of the industrial salt market in 2025. Its commercial primacy reflects the production economics of brine extraction whose pipeline delivery to on-site electrolytic chlor-alkali plants eliminates the solid salt handling, dissolution, and brine preparation steps that mining-sourced salt requires. Chemical plants built adjacent to natural brine deposits integrate brine supply with electrolytic salt processing in vertically integrated operations whose total production cost is materially lower than purchased solid salt alternatives. The Great Lakes brine deposits serving U.S. chemical manufacturers and the Cheshire salt field serving UK chemical plants represent the most commercially significant brine-integrated chemical salt production systems globally.

Salt mines are the fastest-growing source because infrastructure development in cold-climate emerging markets in Eastern Europe, Central Asia, and northern China is creating above-average de-icing salt demand whose procurement favours locally accessible rock salt mining over imported alternatives. Each new highway expansion programme in cold-climate developing countries creates de-icing salt procurement infrastructure whose annual volume scales with road network expansion and maintenance standardisation.

By End User, chemical industry dominates, water utilities grow fastest

The chemical industry retained the dominant end user position with approximately 40% of the industrial salt market in 2025. Chlor-alkali plants, soda ash manufacturers, and industrial chemical producers collectively represent the most commercially concentrated industrial salt customer segment whose individual facility procurement volumes substantially exceed other end user categories in per-site consumption. Each major chlor-alkali plant operates as a single procurement relationship whose contract volumes are measured in hundreds of thousands of tonnes annually, creating commercial concentration that sustains consistent revenue independent of end-use market fragmentation. The chemical industry's long-term supply contracts and strategic brine integration create commercial relationships whose stability provides procurement predictability for salt producers.

Water utilities are the fastest-growing end user at approximately 5.2% CAGR because global municipal water treatment infrastructure investment and industrial water recycling regulatory compliance are creating structured salt demand growth across both developed and emerging markets simultaneously. Water softening applications that consume industrial salt to regenerate ion exchange resin media scale proportionally with new water treatment capacity installation. Municipal swimming pool water treatment, industrial cooling water treatment, and pharmaceutical water purification each represent additional water utility salt demand categories whose combined growth sustains the segment's above-average procurement expansion rate.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

48.6% |

|

Middle East & Africa |

UAE |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America Industrial Salt Market Insights

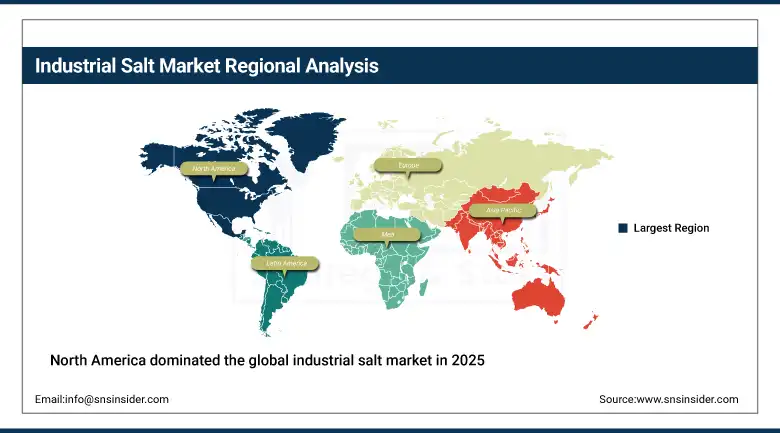

North America dominated the global industrial salt market in 2025 as the largest regional market. The United States accounts for approximately 87.4% of North American revenues through Cargill Salt, Compass Minerals, and Morton Salt's commercial dominance across de-icing, chemical processing, and water treatment procurement. The U.S. de-icing market, generating above-average per-capita salt procurement in the northeastern and midwestern states, represents the most commercially concentrated single application within North America.

Canada contributes approximately 12.6% of North American revenues through its de-icing programme's substantial highway maintenance salt procurement, the chemical processing industry's chlor-alkali salt demand, and the petroleum industry's oil sands water treatment and brine management requirements that create consistent industrial salt procurement.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Industrial Salt Market Insights

Europe is really sophisticated when it comes to the industrial salt market. The EU's chemical industry needs tons of salt for chlor-alkali and soda ash, and there's lots of de-icing required up north and in central Europe too. Plus, water treatment plants are expanding, which means they're buying more salt consistently.

Germany, in particular, dominates with around 22.3% of European revenue from stuff like K+S AG's mining and INEOS's chemical manufacturing. And let's not forget, they spend above average on water treatment infra.

The UK, France, and Poland follow as important players in this game. Take Poland's CIECH Soda Polska for example—they've got a long-term brine supply deal with Inowroclaw Salt Mines, good 'til 2035. This shows how key reliable, long-term supplies are for big chemical processes in Europe.

Asia Pacific Industrial Salt Market Insights

Asia Pacific is the fastest-growing regional industrial salt market, driven by China's rapid industrial development whose chlor-alkali capacity expansion, chemical manufacturing growth, and industrial water treatment investment collectively create above-average salt demand. China accounts for approximately 48.6% of Asia Pacific revenues as both a major salt producer and the largest regional consumer. India, Vietnam, Indonesia, and Thailand represent the most commercially dynamic emerging markets whose industrial development is creating first-time structured procurement growth.

India's chlor-alkali industry expansion, the rapidly growing water treatment sector, and increasing oil and gas exploration activity are collectively creating above-average salt demand growth whose commercial scale is progressively attracting international salt producers to establish regional supply infrastructure. Sojitz Corporation's 2024 partnership with a Middle Eastern company to establish a new solar salt production facility reflects the commercial recognition of Asia Pacific's growing salt demand.

MEA & Latin America Industrial Salt Market Insights

The Middle East and Africa and Latin America are growing industrial salt markets where desalination, oil and gas, and chemical processing create structured demand. UAE leads MEA revenues at approximately 38.4% through its desalination infrastructure's brine management requirements, oil and gas industry's drilling fluid procurement, and chemical processing investment. Egypt's ESIC salt refining facility development with Invest International's USD 13.6 million financing represents the most commercially significant MEA industrial salt infrastructure investment of 2023.

Brazil leads Latin American revenues at approximately 44.2% through its chemical industry's chlor-alkali salt demand, oil and gas sector procurement, and agricultural sector's animal nutrition salt consumption. Rio Tinto Group's salt operations and Cargill's Latin American salt business collectively serve the region's diverse industrial procurement requirements across multiple application categories.

Market Dynamics

Growth Drivers: Chlor-alkali chemical industry expansion and water treatment infrastructure investment driving structured demand

Chlor-alkali chemical industry expansion is the industrial salt market's most commercially concentrated growth driver. Each new chlorine production capacity commissioned requires proportional brine or solid salt feedstock procurement whose volume scales with plant nameplate capacity and operating utilisation. Asia Pacific's chlor-alkali capacity expansion for PVC, paper, and pharmaceutical chemical manufacturing creates the most commercially significant new procurement volumes in the global market, whose aggregate addition to chlor-alkali salt demand is growing the chemical processing application segment at above-average market growth rates.

Water treatment infrastructure investment is simultaneously creating the most geographically distributed and commercially certain industrial salt demand growth. Municipal water treatment expansion for drinking water quality improvement, industrial effluent treatment regulatory compliance, and desalination plant development across water-stressed regions collectively create procurement whose compliance-driven motivation sustains investment through economic cycle variation. Each new water treatment facility commissioned represents a long-duration procurement relationship whose annual salt consumption sustains consistent market demand.

Restraints: Environmental concerns about de-icing salt runoff and competition from alternative chemical alternatives

Environmental concerns about sodium chloride road salt's impact on freshwater ecosystems, vegetation, soil chemistry, and infrastructure corrosion are creating regulatory pressure in North American and European markets whose municipalities are progressively implementing salt management programmes that reduce per-lane-mile application rates. Each reduction in average application rate reduces the total salt procurement volume that road maintenance programmes generate, creating a de-icing market growth constraint that partially offsets volume increases from road network expansion.

Competition from alternative de-icing agents including magnesium chloride, calcium chloride, and calcium magnesium acetate creates market share pressure in premium de-icing applications where environmental sensitivity, infrastructure protection, or application performance requirements justify the higher cost of alternative products over commodity sodium chloride salt. Airport runway de-icing, bridge deck applications, and environmentally sensitive watershed areas represent application contexts where sodium chloride alternatives create competition for premium procurement.

Opportunities: Chemical processing expansion in emerging markets and eco-friendly de-icing product development

Chemical processing expansion in Asia Pacific, Africa, and Latin America represents the most commercially significant near-term growth opportunity for industrial salt producers. Each new chlor-alkali plant commissioned in India, Southeast Asia, or Africa creates a new long-term procurement relationship whose contract volumes generate predictable recurring revenue. The pharmaceutical industry's NaOH and HCl chemical requirements, the paper industry's bleaching chemical demand, and the PVC manufacturing expansion collectively create structured chemical processing salt demand whose commercial scale grows with each new industrial development programme.

Eco-friendly de-icing product development creates premium market differentiation opportunity for industrial salt producers who invest in lower-environmental-impact formulations. Kissner Group Holdings's biodegradable de-icing salt development, which saw 18% increased adoption by municipalities across Canada and the U.S. in late 2023, demonstrates the commercial validation of premium eco-friendly salt products whose price premium over commodity rock salt is justified by reduced regulatory risk and environmental performance credentials.

Recent Developments:

-

2023: Invest International provided a USD 13.6 million loan facility for Egyptian Salt Industry Co. (ESIC) in February 2023 to establish a salt refining industrial plant in Egypt using technology from Titan Salt B.V., expanding industrial salt refining capacity in the MEA region to serve regional chemical, water treatment, and food industry demand.

-

2022: CIECH Soda Polska entered into a long-term supply agreement with Inowroclaw Salt Mines "Solino" in December 2022 to ensure brine provision for production until 2035, demonstrating the commercial importance of long-duration supply security for large-scale European industrial salt chemical processing operations.

-

2024: Sojitz Corporation partnered with a Middle Eastern company in 2024 to establish a new solar salt production facility, boosting output by approximately 30% for water treatment applications and reflecting the commercial momentum of solar salt capacity expansion to serve growing regional industrial procurement demand.

Industrial Salt Market Key Players

-

Cargill Inc.

-

Compass Minerals International

-

K+S AG

-

INEOS Group

-

China National Salt Industry Corporation

-

Tata Chemicals Ltd.

-

Morton Salt Inc.

-

Rio Tinto Group

-

GHCL Ltd.

-

Dominion Salt Ltd.

-

Mitsui & Co. Ltd.

-

Nouryon

-

Archean Group

-

Kissner Group Holdings

-

Sojitz Corporation

-

Naikai Salt Industries

-

Sambhar Salts Ltd.

-

Akzo Nobel N.V.

-

Boliden Group

-

SQM S.A.

Industrial Salt Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 16.31 Billion |

| Market Size by 2035 | USD 22.87 Billion |

| CAGR | CAGR of 3.6% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Rock Salt, Solar Salt, Vacuum Pan Salt, Salt in Brine) • By Source (Natural Brine, Salt Mines/Rock Salt, Sea Salt) • By Application (Chemical Processing, De-Icing, Water Treatment, Oil & Gas, Agriculture, Food Processing, Others) • By End User (Chemical Industry, Water Utilities, Transportation & Government, Oil & Gas, Agricultural, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Cargill Inc., Compass Minerals International, K+S AG, INEOS Group, China National Salt Industry Corporation, Tata Chemicals Ltd., Morton Salt Inc., Rio Tinto Group, GHCL Ltd., Dominion Salt Ltd., Mitsui & Co. Ltd., Nouryon, Archean Group, Kissner Group Holdings, Sojitz Corporation, Naikai Salt Industries, Sambhar Salts Ltd., Akzo Nobel N.V., Boliden Group, SQM S.A. |

Frequently Asked Questions

The Industrial Salt Market is expected to grow at a CAGR of 3.6% from 2026 to 2035.

The Industrial Salt Market was valued at USD 16.31 Billion in 2025.

Chlor-alkali chemical industry expansion in Asia Pacific and emerging markets creating concentrated structural salt demand, and water treatment infrastructure investment across both developed and developing markets creating compliance-driven procurement whose motivation sustains investment through economic cycle variation.

Chemical Processing dominated the Industrial Salt Market with approximately 36.7% share in 2025 and is also the fastest growing application segment.

North America dominated the Industrial Salt Market in 2025 as the largest regional market, with the United States accounting for approximately 87.4% of North American revenues.

Get in Touch