Industrial Traction Battery Market Report Scope & Overview:

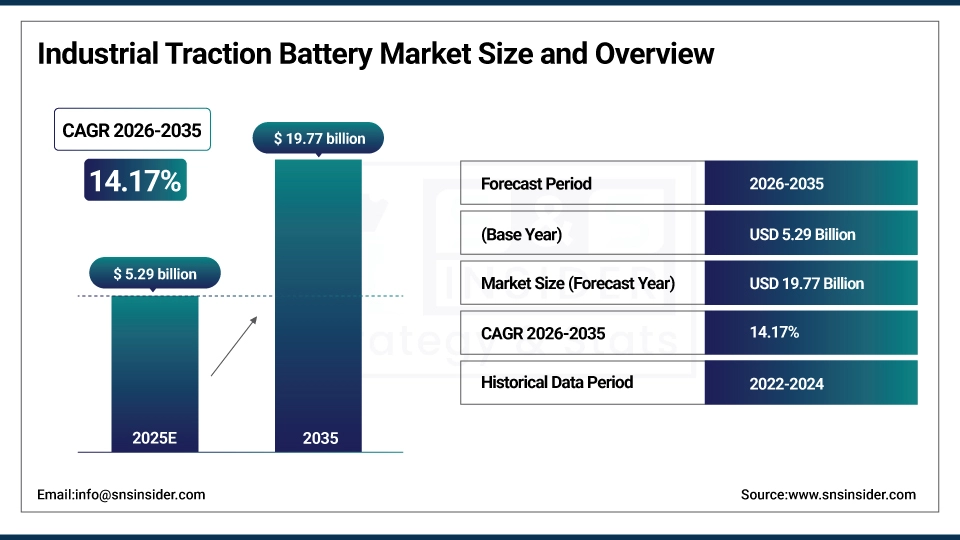

The Industrial Traction Battery Market was valued at USD 5.29 billion in 2025 and is expected to reach USD 19.77 billion by 2035, growing at a CAGR of 14.17% from 2026-2035.

The industrial traction battery market is growing due to high demand for electric forklifts, automated guided vehicles and other material handling equipment in warehouses and manufacturing units. The high-performance batteries demand is further energized by the rising focus on industrial automation, along the lines of energy efficiency and sustainability. Rise in lithium-ion technology, better battery duration & battery charging along with Government initiatives, targeting clean energy is accelerating the market growth as it has been aiding the industry in reducing the capital cost considerably and improving productivity around the globe.

As of 2024, approximately 1.2 million battery-electric forklifts have been purchased worldwide, significantly outpacing hydrogen forklifts (~50,000 units) and demonstrating strong traction for battery-powered industrial vehicles.

Additionally, the U.S. Department of Energy (DOE) provides support for industrial decarbonization initiatives, offering up to USD 23 million in assistance, which indirectly facilitates the adoption of energy-efficient technologies, including electric industrial vehicles and traction batteries.

Industrial Traction Battery Market Size and Forecast

-

Industrial Traction Battery Market Size in 2025: USD 5.29 Billion

-

Industrial Traction Battery Market Size by 2035: USD 19.77 Billion

-

CAGR: 14.17% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Industrial Traction Battery Market - Request Free Sample Report

Industrial Traction Battery Market Trends

-

Rising demand for electrification of material handling and industrial vehicles is driving the industrial traction battery market.

-

Growing adoption in forklifts, automated guided vehicles (AGVs), and electric warehouse equipment is boosting market growth.

-

Expansion of e-commerce, logistics, and manufacturing sectors is fueling deployment.

-

Increasing focus on longer battery life, fast charging, and operational efficiency is shaping adoption trends.

-

Advancements in lithium-ion, lead-acid, and solid-state battery technologies are enhancing performance and reliability.

-

Rising need for sustainable energy storage and reduced carbon emissions is supporting market expansion.

-

Collaborations between battery manufacturers, equipment OEMs, and energy management solution providers are accelerating innovation and global adoption.

U.S. Industrial Traction Battery Market Size Outlook:

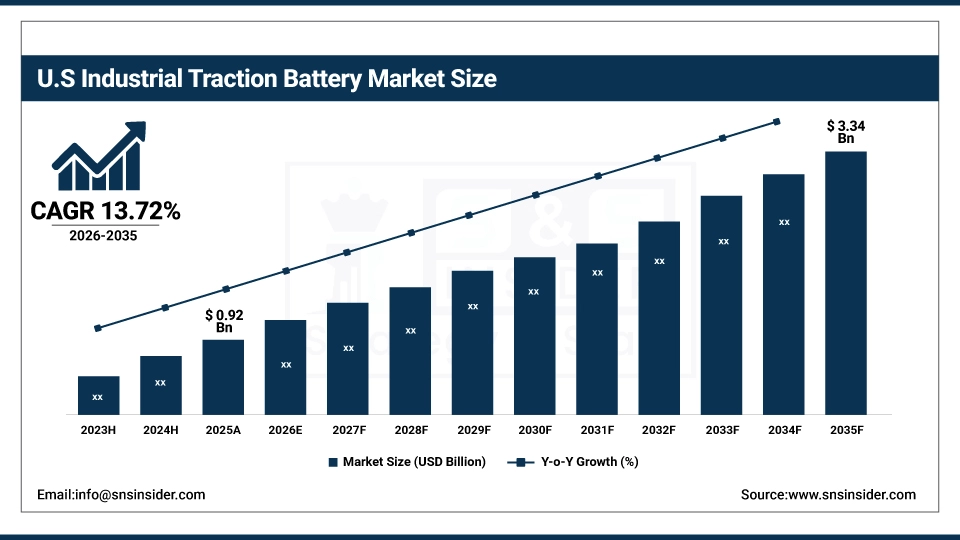

The U.S. Industrial Traction Battery Market was valued at USD 0.92 billion in 2025 and is expected to reach USD 3.34 billion by 2035, growing at a CAGR of 13.72% from 2026-2035. The U.S. Industrial Traction Battery Market is driven by increase in warehouse automation and Electric forklifts and AGVs developments, Increases in lithium-ion batteries technology development and more effort to have energy-efficient and sustainable industrial operations across manufacturing and logistics vertical.

Industrial Traction Battery Market Growth Drivers:

-

Rising demand for electric industrial vehicles to reduce operational costs and environmental impact drives traction battery adoption worldwide

Rapid adoption of electric forklift trucks, automated guided vehicles ( AGVs), and industrial cleaning gear is driving the demand for efficient industrial traction batteries. Companies are infusing cost into account-powered methods to diminish gasoline bills, weather-changing emissions, and meet steep seek after requirements. Compared to conventional batteries, lithium-ion batteries provide enhanced energy density, reduced charging time, and extensive cycle life, which boosts adoption of these technologies in various industrial sectors. The fast-paced emergence of sustainability requirements across warehousing, manufacturing and logistics sectors will sail the way for modern material handling to sustain the demand for traction batteries, as it encourages faster transition away from conventional lead-acid batteries to high-quality and performing alternatives.

Panasonic powers around 70% of AGVs in Japanese automotive manufacturing, highlighting extensive traction battery adoption in AGV fleets.

Additionally, CATL’s lithium-ion batteries are installed in over 200,000 electric forklifts across major logistics hubs in Asia and Europe, demonstrating the large-scale deployment of traction batteries in industrial operations.

Industrial Traction Battery Market Restraints:

-

Limited charging infrastructure and inconsistent power supply in developing regions hinder widespread traction battery utilization in industries

Industrial facilities, particularly those in developing economies, struggle with a lack of charging stations, unreliable power supplies, and the non-existence of standardised batteries. This infrastructure gap poses a barrier for electric industrial vehicle and traction batteries adoption. For long-term overheads, companies are also not going for high-capacity lithium-ion or lead-acid batteries since the downtime involved in operations or super-slow charging cycles at extremely low power levels leads to loss in longer productivity. Worse, these challenges are exacerbated by overcharging safety problems and the accelerated degradation of battery performance over time. Industries are still not ready to replace traditional fuel powered equipment as traction battery needs a strong infrastructure with constant access to electricity and reasonable low rates.

Industrial Traction Battery Market Opportunities:

-

Rapid technological advancements in lithium-ion and high-capacity batteries present growth opportunities for the industrial traction sector

Battery manufacturers are developing higher energy density and life upcoming next-generation lithium-ion, LiFeP04, and hybrid solutions that will charge faster. Introduction of application-tailored, modular, and scalable battery packs for forklift and AGV applications boost productivity of material handling solutions. This allows for predictive maintenance when paired with IoT-based battery monitoring systems, ultimately reducing downtime and improving cost-effectiveness. The demand for wireless and autonomous charging technologies is increasing, which is leading to the rise of the market. Automated warehouses, logistics hubs and manufacturing facilities, where the core focus area is productivity and energy efficiency, is another segment which will get a high industrial traction share for the one able to provide the best advanced, safe and reliable energy storage solutions.

Flux Power Holdings, Inc. partnered with a major forklift OEM to supply advanced lithium-ion S-Series batteries, certified for enhanced safety and industrial deployment, expanding access to high-performance battery solutions.

Similarly, BSLBATT introduced a next-generation forklift lithium battery emphasizing modularity, connectivity, and safety to meet modern warehousing and logistics requirements.

Industrial Traction Battery Market Segment Highlights

-

By Application, Electric Forklifts dominated the Industrial Traction Battery Market with ~71% share in 2025; Automated Guided Vehicles fastest growing (CAGR).

-

By Sales Channel, OEMs dominated the Industrial Traction Battery Market with ~41% share in 2025; Online Retailers fastest growing (CAGR).

-

By Voltage Range, 36V–48V dominated the Industrial Traction Battery Market with ~28% share in 2025; 80V–96V fastest growing (CAGR).

-

By Capacity Range, 100–200 Ah dominated the Industrial Traction Battery Market with ~26% share in 2025; Over 600 Ah fastest growing (CAGR).

-

By Battery Chemistry, Lithium-Ion dominated the Industrial Traction Battery Market with ~60% share in 2025; Lithium-Ion fastest growing (CAGR).

By Application, Electric Forklifts segment dominates the Market, Automated Guided Vehicles expected to grow fastest

Electric forklifts segment dominated the Industrial Traction Battery Market in 2025 facilities. These are the sustainable and green material handling challenges which such machines have a solution to. Due to the massive operations of large industrial traction batteries, they have high energy consumption and operational periods.

Automated guided vehicles segment is expected to grow at the fastest CAGR from 2026-2035 due to the increasing adoption of warehouse automation and automation robotics. These machines require compact, high-performance traction batteries for minimal downtime and continuous 24/7 operation while providing precision handling. Rising reliance on automated systems in logistics and manufacturing will continue to drive demand for advanced battery solutions.

By Sales Channel, OEMs segment dominates the Market, Online Retailers expected to grow fastest

OEMs segment dominated the Industrial Traction Battery Market in 2025 because manufacturers of industrial equipment prefer to source directly from original equipment manufacturers. Thus guaranteeing matching, reliability, and strong after-sales support to cover for operational disruptions. It is also an inevitable way that industries can follow to minimising their maintenance costs, ensuring their quality standards Continued without compromising the value (price) of the battery, and optimizing battery performance for forklifts, AGVs, and other industrial machineries operating in challenging conditions.

Online Retailers segment is expected to grow at the fastest CAGR from 2026-2035 owing to growing e-commerce penetration and convenience of buying industrial battery through online retailers. Using online resources saves time and makes it easy to secure replacements, often at competitive prices, and available within a short timeframe. The industries have become over reliant on online platforms for instant procurements, as it minimizes the downtimes and creates a smooth running of operations.

By Voltage Range, 36V–48V segment dominates the Market, 80V–96V expected to grow fastest

36V–48V segment dominated the Industrial Traction Battery Market in 2025 as this operating range of voltage is the most common for most industrial equipment including forklifts, utility vehicles and cleaning machines. This offers the sweet spot between powering and enabling for many industrial vehicle operational needs, whilst also allowing enough number of charging cycles and a safe power output on a daily basis.

80V–96V segment is expected to grow at the fastest CAGR from 2026-2035 owing to the demand for the high-power batteries for high-capacity industrial vehicles and automated system equipment. Higher voltage systems lead to longer run times, heavy duty operations, less down time, etc. Its demand has been driven by the increasing use of automated material handling systems where the industrial vehicles operated are needed high energy density in traction batteries.

By Capacity Range, 100–200 Ah segment dominates the Market, Over 600 Ah expected to grow fastest

100–200 Ah segment dominated the Industrial Traction Battery Market in 2025 as this segment meets a majority of energy needs for industrial vehicles at low cost. This range of capacity levels evenly divides performance, weight, and charge cycles, and is ideal for forklifts, AGVs, and utility vehicles. This allows it to continually operate in warehouses and production centers without needing to be replaced or serviced as needed.

Over 600 Ah segment is expected to grow at the fastest CAGR from 2026-2035 because of the high requirement for automated & high-capacity commercial vehicles as well as heavy industrial vehicles. For which they require extended life, high energy density and reliable performance. High-capacity traction batteries are becoming increasingly popular as a solution to guarantee permanent operations and higher operational efficiency at industrial facilities that plan large scale automation investments.

By Battery Chemistry, Lithium-Ion segment dominates the Market and is expected to grow fastest

In 2025, Lithium-Ion segment is expected to dominate Industrial Traction Battery Market as these types provide high energy density, longer charge cycles, and low maintenance as compared to the lead acid batteries. Industries love to use them in forklift, AGV, and industrial cleaning equipment because they charge their batteries fast, have lower downtime, and are consistent with performance. Incorporating advantages such as high efficiency, low weight, low cost, long cycle life, and integration into smart battery systems, the segment is projected to see the fastest growth over the 2026-2035 timeframe to assist in industrial automation, warehouse electrification, and high-performance functionality in logistics and manufacturing.

Industrial Traction Battery Market Regional Analysis

Asia Pacific Industrial Traction Battery Market Insights

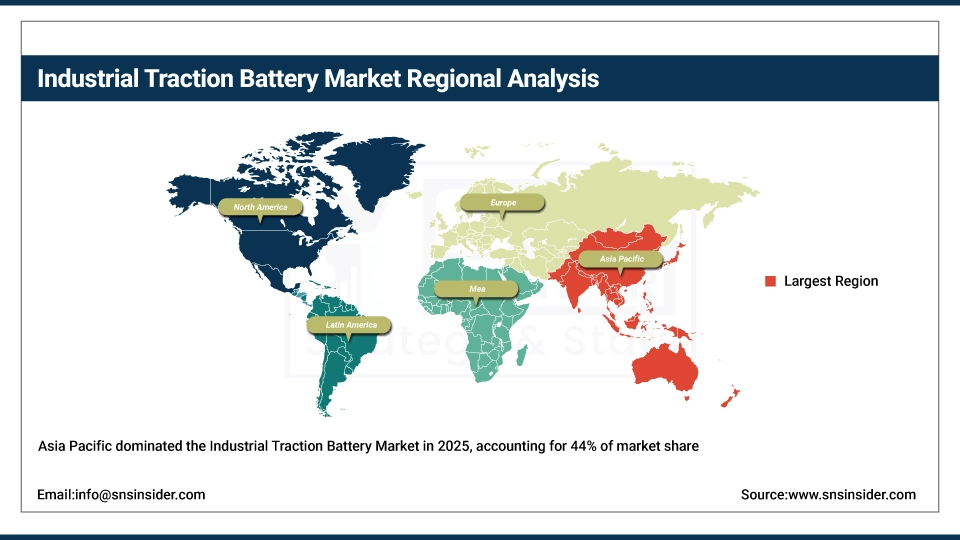

Asia Pacific dominated the Industrial Traction Battery Market in 2025 with the highest revenue share of about 44% due to competitive capacity, industrialization, advancement in warehousing and logistics sector along with higher penetration of electric Forklifts and automated guided vehicles in the region. Supporting demand: Growth of manufacturing activities, increasing government initiatives for supporting clean energy and increasing investment for industrial automation. In addition, the leading battery manufacturers and also the cheap cost of manufacturing capacities in the region mainly in China, India and Japan strongly support the growth of industrial traction battery market also in this area.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Industrial Traction Battery Market Insights

The North America region remains an important contributor to the Industrial Traction Battery Market since the region has advanced warehouse automation with high adoption of electric forklift as well Industrial infrastructure. The presence of dominating battery manufacturers and the continuous government initiatives to reduce dependency on a non-renewable source of energy will spur a growth spree in the market of Lift Truck Battery. Analyst Jefferies said, however, that the region has a strong industrial base for battery investment and is building this up through increased investment in high-capacity and lithium-ion traction batteries.

Europe Industrial Traction Battery Market Insights

Europe is one of the major industrial traction battery market due to strict environmental regulations, sustainable material handling activities, as well as, widespread application of electric forklifts and automated guided vehicles. An established industrial infrastructure, combined with significant government incentives for clean energy technologies and advanced manufacturing practices provide traction battery demand in the state with a strong stimulus. Continued growth of the European industrial battery market is backed by the high adoption of lithium-ion and of high-density batteries within warehouse spaces, logistic centres as well as industrial plants.

Middle East & Africa and Latin America Industrial Traction Battery Market Insights

Continuous industrialization and expansion in logistics and warehousing sectors coupled with increasing penetration of electric forklifts, automated guided vehicles, and material handling equipment are supporting the growth of Industrial Traction Battery Market in developing countries of Middle East & Africa and Latin America region. Market Dynamics The growth of lithium ion battery market is primarily driven by factors such as environmental regulations, government initiatives for clean energy, government initiatives for industrial modernization and sustainable practices, demand and market expansion for lithium-ion/high-capacity batteries in major countries in both the regions along with growing investment in li-ion battery.

Industrial Traction Battery Market Competitive Landscape:

EnerSys

EnerSys is the global leader in stored energy solutions for industrial applications specializing in industrial traction, motive power and reserve power battery systems. The company produces batteries and chargers, along with integrated energy management solutions over the backdrop of manufacturing/warehousing and logistics. Maintenance-free technologies, advanced lead-acid and lithium-ion chemistries, and higher energy density, cycle life, and operational efficiency are all on display from various manufacturers, such as EnerSys. ATEQ develops battery monitoring, fleet management and aftermarket solutions that enable greater reliability, uptime, and sustainability for industrial traction and material handling applications.

-

2023: EnerSys acquired Industrial Battery and Charger Services Limited (IBCS) in the UK, expanding motive power battery services and distribution for industrial traction applications.

-

2024: EnerSys showcased NexSys TPPL batteries and integrated management tools at MODEX 2024, supporting industrial traction and motive power efficiency.

-

2025: EnerSys expanded NexSys TPPL battery models, improving cycle life, energy throughput, and charging flexibility for industrial forklift fleets.

BYD Co., Ltd.

BYD is a multinational company engaged in electric vehicles and core technologies of batteries including lithium-ion Blade Batteries for EV, industrial traction and energy storage. Based on sustainability, its battery systems include safety, high energy density and long lifecycle. BYD: Worldwide Supply, with Industrial Traction Solutions Supporting Forklifts, Automated Guided Vehicles, and Material Handling Fleets The Blade Battery portfolio has half the parts of a traditional EV battery, which translates to streamlined costs, less maintenance and maximum uptime while offering transformative modularity, safety and scalability to drive high-performance operation in full industrial conditions.

-

2024: BYD announced its next-generation Blade Battery lineup for 2025, emphasizing safety, energy density, and lifecycle improvements for traction applications.

-

2025: BYD confirmed the 2025 launch of its next-generation Blade Battery, designed for higher safety and performance for EVs and industrial traction systems.

Industrial Traction Battery Companies are:

-

BYD Co., Ltd.

-

EnerSys

-

East Penn Manufacturing

-

Amara Raja Batteries

-

LG Energy Solution (LG Chem)

-

Panasonic Corporation

-

HOPPECKE Batteries GmbH & Co. KG

-

Hitachi Energy / Hitachi Chemical

-

Toshiba Corporation

-

Flux Power

-

Sunlight Group (Systems Sunlight S.A.)

-

ecovolta

-

Farasis Energy

-

Guoxuan High‑tech Power Energy

-

Mutlu Corporation

-

MIDAC S.p.A.

-

Crown Battery Manufacturing Company

-

GS Yuasa Corporation

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 30.9 Billion |

| Market Size by 2035 | USD 60.25 Billion |

| CAGR | CAGR of 7.7% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (General, Support, Analytical, Clinical, Specialty) • By End-use (Research Institutions, Veterinary, Healthcare, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Thermo Fisher Scientific, Agilent Technologies, Shimadzu Corporation, Bruker Corporation, PerkinElmer Inc., Beckman Coulter, Mettler Toledo, Eppendorf AG, Sartorius AG, Waters Corporation, Bio-Rad Laboratories, GE Healthcare Life Sciences, Tecan Group Ltd., Anton Paar GmbH, Hitachi High-Tech Corporation, Labconco Corporation, Oxford Instruments plc, HORIBA Scientific, Jeol Ltd., Analytik Jena AG. |

Frequently Asked Questions

Asia Pacific dominated the Industrial Traction Battery Market in 2025.

The OEMs segment dominated the Industrial Traction Battery Market in 2025.

Rising demand for electric industrial vehicles to reduce operational costs and environmental impact drives traction battery adoption worldwide.

The Industrial Traction Battery Market was valued at USD 5.29 billion in 2025.

The Industrial Traction Battery Market is expected to grow at a CAGR of 14.17% from 2026 to 2035.

Get in Touch