LNG Terminal Market Report Scope & Overview:

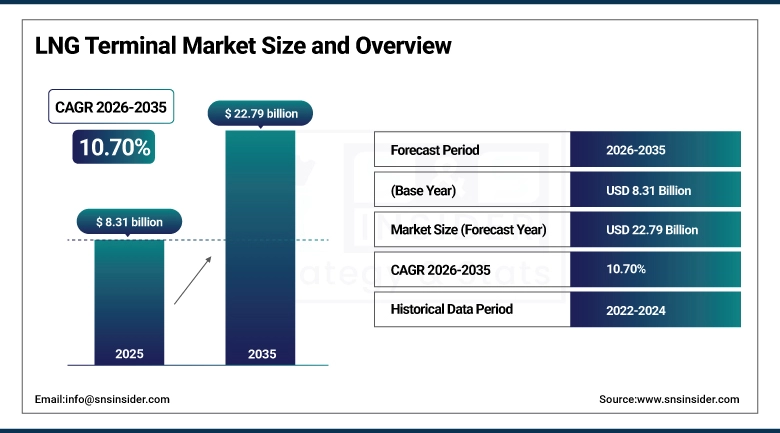

The LNG Terminal Market was valued at USD 8.31 billion in 2025 and is expected to reach USD 22.79 billion by 2035, growing at a CAGR of 10.70% from 2026-2035.

The increase in global energy consumption and the shift towards cleaner fuel sources compared to coal and oil is contributing to the expansion of the LNG Terminal Market. The growing demand for LNG and diversification in supply is leading to the increased investment in terminal infrastructure. Other factors contributing to market expansion include industrial growth, government initiatives, and the adoption of natural gas for energy generatio.

The International Energy Agency (IEA) reports that roughly 300 billion m³/year of new LNG export capacity is projected to be added by 2030, primarily led by new liquefaction capacity in countries like the United States and Qatar, indicating major upcoming LNG infrastructure needs including export terminals.

LNG Terminal Market Size and Growth Forecast

-

Market Size in 2025: USD 8.31 Billion

-

Market Size by 2035: USD 22.79 Billion

-

CAGR: 10.70% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on LNG Terminal Market - Request Free Sample Report

LNG Terminal Market Trends

-

Rising global demand for cleaner energy sources is driving the LNG terminal market.

-

Growing LNG trade and cross-border gas transportation are boosting market growth.

-

Expansion of liquefaction and regasification infrastructure is fueling deployment.

-

Increasing focus on energy security, diversification of supply, and reduced dependence on pipeline gas is shaping adoption trends.

-

Advancements in floating storage and regasification units (FSRUs) and small-scale LNG terminals are enhancing flexibility and cost efficiency.

-

Rising investments in natural gas infrastructure and government support are supporting market expansion.

-

Collaborations between energy companies, EPC contractors, and technology providers are accelerating innovation and global adoption.

U.S. LNG Terminal Market Size Outlook:

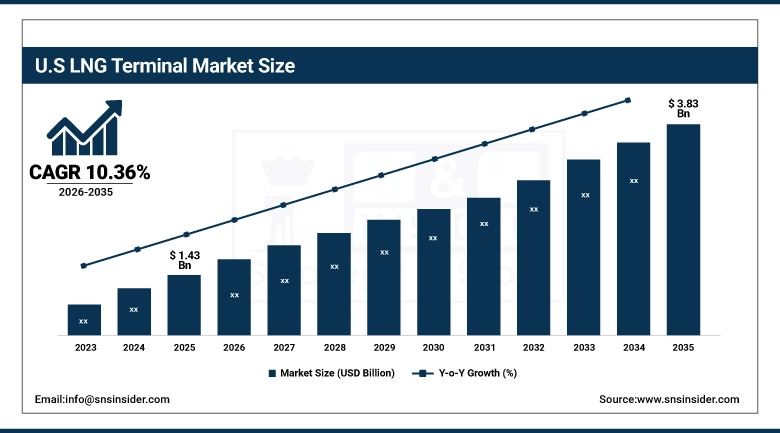

The U.S. LNG Terminal Market was valued at USD 1.43 billion in 2025 and is expected to reach USD 3.83 billion by 2035, growing at a CAGR of 10.36% from 2026-2035. The U.S. LNG Terminal Market is experiencing growth owing to the availability of shale gas in the country and rising demand for LNG exports in other countries. Growth can be attributed to increased investments in liquefaction capacity, long-term export agreements, and robust infrastructural development.

In March 2026, U.S. LNG exports hit a record ~11.7 million metric tons, driven by plants operating above capacity and new terminal production ramp‑ups amid Middle East supply disruptions.

U.S. LNG producers are on track to sign near‑record contract volumes in 2025 (~29.5 million tonnes per year of SPAs), more than four times the annual volume signed in 2024, signaling robust long-term demand and commercial investment.

LNG Terminal Market Growth Drivers:

-

Rising global energy demand and transition toward cleaner fuels are accelerating LNG terminal infrastructure investments worldwide significantly

The rising global demand for energy and a shift towards clean fuel is positively impacting the LNG terminal market. Natural gas is perceived as a cleaner fuel than coal and oil. Therefore, there is a significant rise in the use of LNG in power plants, industries, and households. Nations are focusing on importing and exporting LNG through terminals to secure their energy resources and diversify their energy suppliers. The fast-paced urbanization and industrialization processes have increased the use of natural gas. The favorable government policy environment promoting green energy is another major factor influencing the market growth.

LNG Terminal Market Restraints:

-

Stringent environmental regulations and concerns over greenhouse gas emissions are restricting approvals and expansion of LNG terminal projects worldwide

The strict environmental laws and rising criticism regarding the release of greenhouse gases have restricted the growth of LNG terminals. The governments and the environmental bodies have voiced their concerns regarding the release of methane gas, carbon footprint, and environmental impact due to the establishment of LNG facilities. Meeting environmental standards calls for more investments in technologies that reduce emissions, thus raising the cost of operations. Obtaining environmental clearance and resistance from the local population have caused delays in executing the projects. With an increasing global shift toward green sources of energy, the pressure on LNG terminals is expected to grow.

LNG Terminal Market Opportunities:

-

Expansion of floating LNG terminals and small scale infrastructure is creating flexible and cost efficient solutions for emerging markets globally

Growing popularity of floating LNG terminals is an area of great potential for the market of LNG terminals. FSRUs are fast-to-install solutions that require relatively small investments compared to their onshore counterparts and also provide greater flexibility. Small-scale LNG terminals will also see an upturn in demand for the purpose of serving distant locations where conventional infrastructure cannot reach due to financial limitations. Growing need for flexible, decentralized power generation facilities and rapid implementation of projects have fueled innovations in modular and floating LNG terminal solutions.

LNG Terminal Market Segment Highlights

-

By Technology, Liquefaction dominated the LNG Terminal Market with ~58% share in 2025; Regasification fastest growing (CAGR).

-

By Terminal Type, Onshore dominated the LNG Terminal Market with ~71% share in 2025; Floating fastest growing (CAGR).

-

By Function, Import dominated the LNG Terminal Market with ~52% share in 2025; Bifunctional fastest growing (CAGR).

-

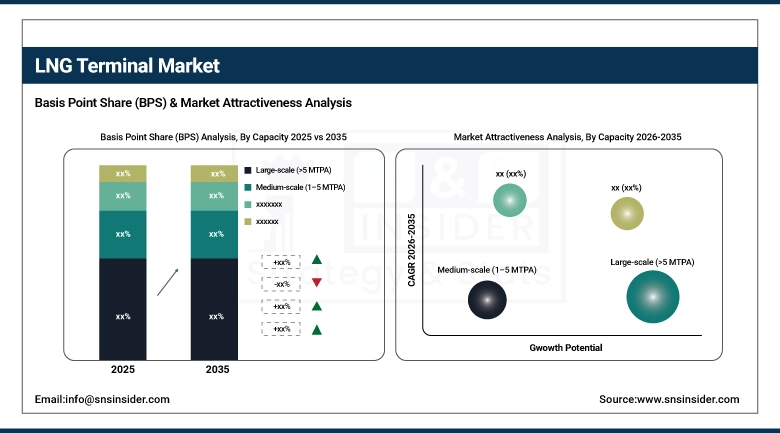

By Capacity, Large-scale (>5 MTPA) dominated the LNG Terminal Market with ~44% share in 2025; Small-scale (<1 MTPA) fastest growing (CAGR).

By Capacity, Large-scale (>5 MTPA) segment dominates the LNG Terminal Market, Small-scale (<1 MTPA) segment expected to grow fastest

The large-scale (>5 MTPA) market segment held the largest share of revenue in the year 2025 due to the high efficiency of the terminals and their capability of dealing with large-scale LNG trade. Such types of facilities enjoy advantages like economies of scale, low costs, and strong support from major players in the energy industry.

The Small Scale (<1 MTPA) segment will record the fastest CAGR from 2026–2035 owing to growing demand for decentralized energy solutions, as well as LNG supply in far-flung locations. This segment requires less investment, offers flexible solutions, and is ideal for marine fuels and off-grid power generation solutions.

By Technology, Liquefaction segment dominates the LNG Terminal Market, Regasification segment expected to grow fastest

The liquefaction segment held the largest market share by revenue in the LNG Terminal Market during 2025, owing to the expanding capability of LNG exports worldwide along with the growth in demand for natural gas transactions among nations. The development of massive liquefaction plants by energy-rich nations is an important factor that drives this market by facilitating easy transportation of the gas, increasing contractual agreements, and offering energy diversification options.

Regasification segment is projected to register the highest CAGR during the forecast period of 2026–2035 due to the growing import of LNG in energy-starved nations. The rapid construction of regasification plants, including floating terminals, facilitates fast access to gas, requires fewer investments, and offers flexibility.

By Terminal Type, Onshore segment dominates the LNG Terminal Market, Floating segment expected to grow fastest

Onshore segment held the dominant market position within LNG Terminal Market by generating maximum revenues in 2025. Onshore terminals feature well-developed infrastructure, increased capacity of storage, and better efficiency in operation. This allows them to be more convenient for the transportation of large volumes of LNG and therefore used by those countries which require stable consumption of this fuel.

Floating segment is projected to have the fastest CAGR during the forecast period 2026-2035 because of the rising need for flexible and economic solutions for LNG infrastructure. Fast implementation, lower investment costs, and mobility benefits allow floating terminals to become more popular in countries where there is little developed infrastructure onshore.

By Function, Import segment dominates the LNG Terminal Market, Bifunctional segment expected to grow fastest

Import Segment held the largest revenue share of LNG Terminal Market in 2025 owing to the growing dependency on imported liquefied natural gas from countries that lack indigenous natural gas reserves. The growth of energy demand, diversification of sources, and reduced dependency on pipeline gas have made investments in LNG import terminals attractive, which have made them dominant in the market.

Bifunctional Segment was projected to witness the highest CAGR during the forecast period (2026-2035), attributable to the growing need for flexibility in LNG terminals. Bifunctional terminals are capable of performing both imports and exports, making better use of facilities and responding to changing market dynamics.

LNG Terminal Market Regional Analysis

Asia Pacific LNG Terminal Market Insights

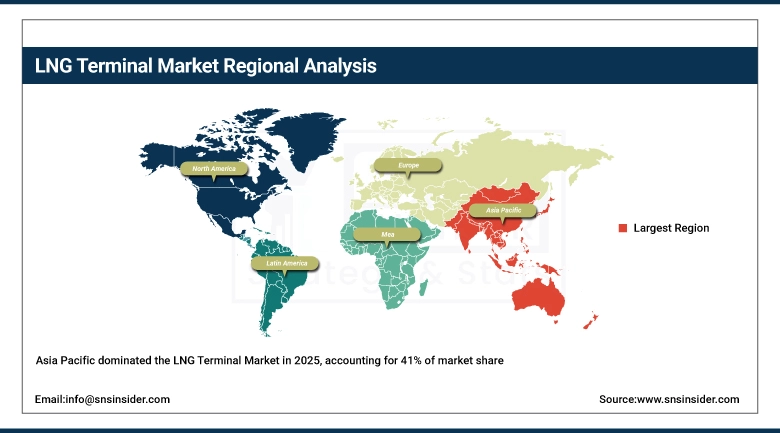

The Asia Pacific segment led the market in revenue share of approximately 41%, driven by high demand for LNG from developing countries with rapidly rising energy consumption rates in the region. The Asian economies are dependent on LNG imports owing to the limited availability of their natural gas resources. Increased urbanization in the region coupled with favorable government policies will continue to contribute towards the dominance of this region in the global LNG market in the coming years.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America LNG Terminal Market Insights

North America plays an important role in the LNG Terminal Market because of its prominence in being a leading exporter of LNG and its sophisticated liquefaction facilities. The area is fortunate enough to be endowed with vast amounts of natural gas deposits, specifically from the shale deposits, thus facilitating the construction of export terminals. Growth in the worldwide demand for LNG from the United States is propelling investments in the area.

Europe LNG Terminal Market Insights

Europe is one of the important regions in the LNG Terminal Market owing to its increased emphasis on energy security and diversification of its gas sourcing options. The region is developing its LNG importing and regasifying infrastructure at a fast pace in order to lower its dependency on pipelines for gas. Growing investments in the installation of floating terminals, along with favorable governmental policies, have fueled market growth in Europe.

Middle East & Africa and Latin America LNG Terminal Market Insights

The Middle East and Africa play a key strategic role in the LNG Terminal Market owing to ample reserves of natural gas and investments being made for the expansion of export terminals. This region is enhancing its capacities in liquefaction to become more involved in international trade, whereas the demand within the country is facilitating the construction of import terminals. The region of Latin America continues to grow steadily due to higher usage of LNG in power generation.

LNG Terminal Market Competitive Landscape:

Cheniere Energy Inc.

The Cheniere Energy Inc. is an American based company that produces and exports liquefied natural gas (LNG). It possesses significant facilities for processing liquefied natural gas at its terminal sites like Sabine Pass and Corpus Christi which operate on long term agreements. The Cheniere Company provides its service of enhancing energy security and transition towards green fuel with its efficient and reliable production of liquefied natural gas for international markets.

-

2026: Cheniere reported record LNG production in 2025 while expanding Corpus Christi terminal, with new trains under construction and long-term agreements strengthening global export capacity.

-

2025: Cheniere achieved substantial completion of Corpus Christi Stage 3 Train 1, marking a major milestone in expanding liquefaction capacity and reinforcing global LNG supply infrastructure.

-

2024: Cheniere produced first LNG from Corpus Christi Stage 3 Train 1, advancing terminal expansion and increasing total production capacity beyond 25 mtpa upon full completion.

LNG Terminal Companies are:

-

QatarEnergy

-

Royal Dutch Shell plc

-

CNOOC Gas & Power

-

Tokyo Gas Co., Ltd.

-

Korea Gas Corporation (KOGAS)

-

Petronet LNG Ltd.

-

Egyptian Natural Gas Holding Company (EGAS)

-

Sempra Infrastructure

-

Exxon Mobil Corporation

-

BW LNG

-

Hoegh LNG

-

Golar LNG Ltd.

-

Bechtel Corporation

-

Technip Energies N.V.

-

Saipem SpA

-

Samsung C&T Corporation

-

JGC Holdings Corporation

-

McDermott International Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 8.31 Billion |

| Market Size by 2035 | USD 22.79Billion |

| CAGR | CAGR of 10.70% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Terminal Type (Onshore, Floating) • By Capacity (Small-scale (<1 MTPA), Medium-scale (1–5 MTPA), Large-scale (>5 MTPA)) • By Technology (Liquefaction, Regasification) • By Function (Import, Export, Bifunctional) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Cheniere Energy Inc., QatarEnergy, Royal Dutch Shell plc, CNOOC Gas & Power, Tokyo Gas Co., Ltd., Korea Gas Corporation (KOGAS), TotalEnergies SE, Petronet LNG Ltd., Egyptian Natural Gas Holding Company (EGAS), Sempra Infrastructure, Exxon Mobil Corporation, BW LNG, Hoegh LNG, Golar LNG Ltd., Bechtel Corporation, Technip Energies N.V., Saipem SpA, Samsung C&T Corporation, JGC Holdings Corporation, McDermott International Inc. |

Frequently Asked Questions

Asia Pacific dominated the LNG Terminal Market in 2025.

The Large-scale (>5 MTPA) segment dominated the LNG Terminal Market in 2025.

Rising global energy demand and transition toward cleaner fuels are accelerating LNG terminal infrastructure investments worldwide significantly.

The LNG Terminal Market was valued at USD 8.31 billion in 2025.

The LNG Terminal Market is expected to grow at a CAGR of 10.70% from 2026 to 2035.

Get in Touch