Insurance Analytics Market Report Scope & Overview:

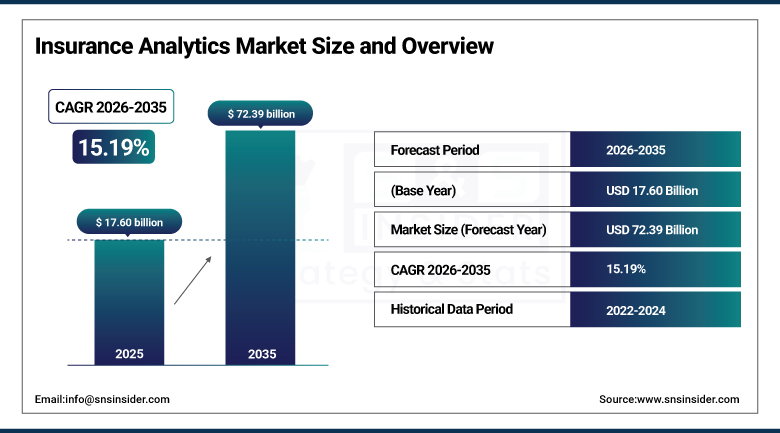

The Insurance Analytics Market was valued at USD 17.60 billion in 2025 and is expected to reach USD 72.39 billion by 2035, growing at a CAGR of 15.19% from 2026–2035.

Insurance analytics encompasses the full spectrum of data science, machine learning, and advanced statistical techniques that insurance companies deploy to extract commercially valuable insights from the enormous volumes of structured and unstructured data that the insurance business generates across its policy underwriting, claims processing, customer service, fraud investigation, risk portfolio management, and regulatory compliance functions. The market's extraordinary growth trajectory reflects the convergence of three simultaneous drivers: the escalating availability of alternative data sources including IoT sensor networks, satellite imagery, and digital behavioral data that provide granular risk visibility previously unachievable from conventional insurance records alone; the maturation of machine learning and generative AI platforms whose analytical capabilities have outpaced traditional actuarial modelling in predictive accuracy for claims frequency, severity, fraud likelihood, and customer churn risk; and the intensifying competitive and regulatory pressure on insurance organizations to improve underwriting discipline, reduce claims leakage from fraud and error, and deliver the personalized product and pricing experiences that digitally native insurtech competitors are establishing as the new consumer expectation benchmark. Insurance fraud alone costs the global insurance industry over USD 80 billion annually, and analytics platforms demonstrating measurable fraud detection rate improvement provide the most immediately quantifiable commercial return on investment that justifies analytics technology procurement across all insurance lines.

The Insurance Information Institute's 2025 industry technology survey finding that 78% of large insurance carriers have deployed or are actively deploying predictive analytics for claims management, and 64% for underwriting automation, confirms that insurance analytics has transitioned from early-adopter experimentation to mainstream operational deployment across the insurance industry's largest and most commercially significant institutions.

Market Size and Forecast

-

Market Size in 2026E: USD 20.27 Billion

-

Market Size by 2035: USD 72.39 Billion

-

CAGR (2026 to 2035): 15.19%

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Insurance Analytics Market - Request Free Sample Report

Insurance Analytics Market Trends

-

Rapid adoption of generative AI and large language model-powered insurance analytics applications including automated claims letter drafting, policy document analysis, subrogation recovery identification, and regulatory filing preparation that augment human insurance professionals' productivity while reducing the per-transaction cost of complex administrative tasks that have historically required skilled legal, medical, and financial expertise.

-

Growing deployment of real-time telematics analytics for usage-based insurance underwriting, where continuous vehicle sensor data streams enable per-mile and per-behavior pricing that rewards safe drivers with lower premiums and creates actuarially sounder risk pools than traditional demographic proxy variables whose correlations with individual risk are considerably weaker than directly measured driving behavior.

-

Increasing integration of satellite imagery, drone inspection data, and computer vision analytics into property and casualty insurance underwriting and claims workflows, enabling remote property condition assessment, post-catastrophe damage estimation across thousands of properties simultaneously, and wildfire or flood exposure monitoring that improves portfolio risk concentration management without requiring physical inspection.

-

Expanding parametric insurance analytics platforms that combine weather data, agricultural satellite monitoring, and financial modelling to design, price, and automatically trigger parametric insurance products for natural disaster, weather-event, and commodity price risk that require continuous monitoring analytics infrastructure to operate effectively at scale.

-

Rising adoption of customer lifetime value analytics and behavior-based personalization that enable insurers to identify high-value customer retention opportunities, optimize cross-sell and upsell timing for additional coverage, and design loyalty programme interventions calibrated to individual customer risk and profitability profiles.

The U.S. Insurance Analytics Market Outlook

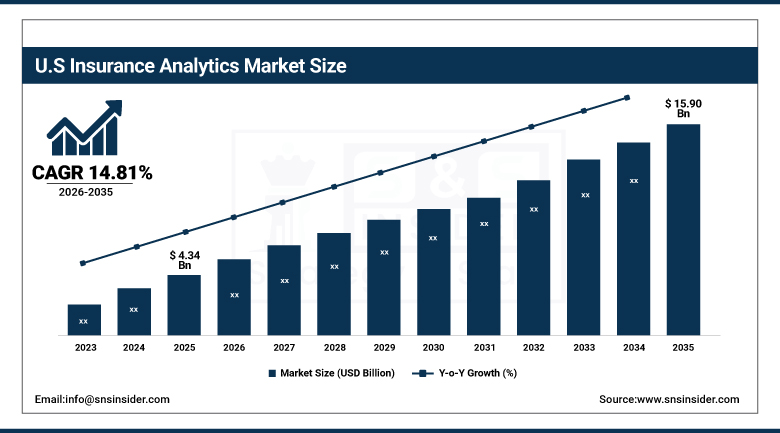

The U.S. Insurance Analytics Market was valued at approximately USD 4.34 billion in 2025 and is expected to reach approximately USD 15.90 billion by 2035, growing at a CAGR of 14.81%, driven by insurers' rapid adoption of cloud, big data, and artificial intelligence technologies, a highly competitive insurance market creating strong incentives for analytical differentiation, and the most sophisticated insurtech innovation ecosystem globally generating continuous analytics capability advancement.

The United States is the world's largest insurance analytics market through the combination of the highest absolute insurance premium volumes creating the largest data asset base for analytics application, the most mature and competitive commercial insurance market where analytical differentiation in underwriting accuracy, claims efficiency, and customer experience is a commercially significant competitive weapon, and the most active insurtech investment ecosystem where companies including Kin Insurance, Hippo, Root, Lemonade, and hundreds of analytics-focused insurtech startups are deploying cutting-edge analytics capabilities that legacy carriers must match or partner with to maintain competitive relevance. The regulatory environment for insurance data use in the United States, where state insurance regulatory frameworks govern permissible rating factors and the use of alternative data in underwriting decisions, creates a complex compliance layer around analytics deployment that specialist insurance analytics vendors help carriers navigate while maximizing the commercial value extracted from available data assets.

The National Association of Insurance Commissioners' ongoing engagement with AI and predictive analytics in insurance, including its work on algorithmic fairness frameworks that establish guardrails for analytics-driven underwriting decisions, is creating the regulatory clarity that enables insurers to invest confidently in advanced analytics deployments while managing compliance risk associated with the use of novel data sources and machine learning models in rate-setting decisions.

Insurance Analytics Market Segment Analysis

-

By Component, software dominated with approximately 64.18% in 2025; services are the fastest-growing at a CAGR of 12.22%.

-

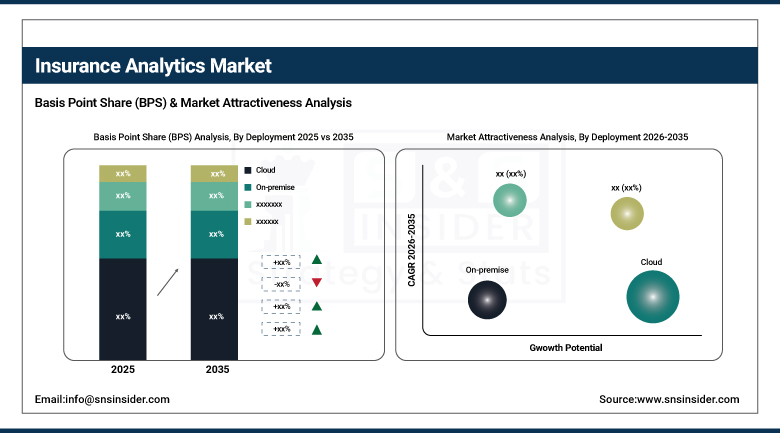

By Deployment, cloud led the market with approximately 65.18% in 2025; on-premise is the fastest-growing segment at a CAGR of 16.04%.

-

By Enterprise Type, large enterprises dominated with approximately 68.40% in 2025; SMEs are the fastest-growing at a CAGR of 15.80%.

-

By End-User, insurance firms dominated with approximately 72.34% in 2025; government agencies are the fastest-growing at a CAGR of 16.04%.

By Deployment, cloud dominates, on-premise is expected to grow fastest

Cloud deployment retained the dominant position with approximately 65.18% of the insurance analytics market in 2025, as the cloud delivery model's combination of subscription-based cost structure eliminating large upfront infrastructure investment, elastic scaling enabling analytics capacity to match seasonal claims volume fluctuations and catastrophe event processing spikes, and continuous platform updates providing access to the latest machine learning and AI capabilities without internal development investment have collectively made cloud-based analytics the default deployment choice for the majority of insurance analytics platform procurement decisions. The major cloud analytics vendors including SAS, Majesco, Duck Creek Technologies, and Guidewire have each developed cloud-native insurance analytics platforms whose architecture provides the data integration, security, and compliance capabilities that carrier procurement requirements specify, sustaining the cloud segment's market share dominance as the primary deployment architecture for new analytics investments across all carrier size tiers.

On-premise is the fastest-growing deployment segment at a CAGR of 16.04% through 2035, as the largest and most data-sensitive insurance organizations whose policyholder data volumes, regulatory data residency requirements, and institutional data governance frameworks create compelling arguments for retaining data analytics processing within their own managed infrastructure rather than transmitting sensitive claims, medical, and financial data to external cloud environments. The EU's GDPR, CCPA, and sector-specific insurance data privacy regulations in multiple jurisdictions create compliance complexity around cloud-hosted analytics that favors on-premise deployment for insurers with significant European or California policyholder populations whose data processing must demonstrably comply with the most stringent applicable regulatory framework.

By End-User, insurance firms dominate, government agencies are expected to grow fastest

Insurance firms retained the dominant end-user position with approximately 72.34% of insurance analytics market revenues in 2025, as the commercial insurance industry's direct financial motivation to improve underwriting profitability through better risk selection, reduce claims expense through faster adjudication and fraud detection, and improve customer retention through personalized engagement creates the strongest and most directly quantifiable ROI case for analytics investment of any end-user category. The claims analytics application, where machine learning models identify claims with high fraud probability for investigator assignment, predict claims severity to reserve accuracy, and classify routine claims for automated straight-through processing, delivers among the highest documented returns on analytics investment in the insurance industry through the combination of fraud loss reduction, reserve accuracy improvement, and administrative cost per claim reduction that comprehensive claims analytics programmes achieve.

Government agencies are the fastest-growing end-user at a CAGR of 16.04% through 2035, reflecting the growing adoption of advanced analytics capabilities across government-administered insurance programmes including Medicare and Medicaid health insurance, crop and agricultural insurance through the USDA Risk Management Agency, flood insurance through the National Flood Insurance Programme, and workers' compensation state insurance funds whose combined scale and fraud vulnerability create compelling analytics investment cases. The U.S. government's estimate that improper payments across federal insurance programmes exceeded USD 175 billion annually provides the financial motivation for analytics-driven fraud and improper payment detection investment that dwarfs the technology cost and generates measurable programme savings that justify continued platform expansion.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

84.6% |

|

Europe |

United Kingdom |

26.3% |

|

Asia Pacific |

China |

41.8% |

|

Middle East & Africa |

UAE |

28.4% |

|

Latin America |

Brazil |

43.7% |

North America Insurance Analytics Market Insights

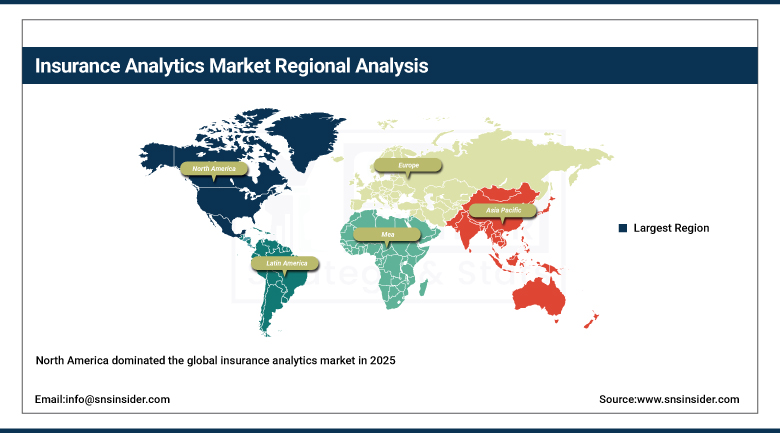

North America dominated the global insurance analytics market in 2025, with the United States accounting for approximately 84.6% of North American revenues as the world's largest insurance market by premium volume, the home of the most commercially active insurtech innovation ecosystem, and the geography where the most advanced analytics capabilities have been commercially deployed at the largest scale. The region's market leadership reflects the combination of a highly competitive commercial insurance market that makes analytical underwriting differentiation commercially necessary, comprehensive digital data infrastructure that enables the alternative data integration on which advanced analytics capabilities depend, and a regulatory environment that while complex is progressively establishing the frameworks for permissible analytics use that enable investment confidence.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Insurance Analytics Market Insights

Europe is a sophisticated insurance analytics market characterized by GDPR compliance requirements shaping the data use and privacy-preserving analytics approaches that European insurers can deploy, Solvency II risk modelling requirements sustaining investment in actuarial analytics infrastructure, and the progressive adoption of AI-powered analytics by major European insurance groups including Allianz, AXA, Zurich, and Generali whose scale and investment capacity support the most advanced analytics deployments in the European market. The United Kingdom accounts for approximately 26.3% of European revenues as the most commercially competitive and analytically advanced national insurance market in the region, where Lloyd's of London's specialty insurance marketplace has driven sophisticated risk analytics adoption and where the FCA's innovation-friendly regulatory posture has enabled insurtech analytics experimentation that has established commercially proven capabilities for broader market adoption.

Asia Pacific Insurance Analytics Market Insights

Asia Pacific is the fastest-growing insurance analytics market, driven by the rapid expansion of insurance penetration across China, India, South Korea, Japan, and Southeast Asian markets where growing middle-class populations are purchasing insurance for the first time, combined with the extraordinary digital data availability from highly connected Asian consumer populations whose smartphone usage, digital payment behavior, and social media engagement generate rich alternative data streams for insurance risk assessment. China accounts for approximately 41.8% of Asia Pacific insurance analytics revenues through its combination of the world's second-largest insurance market by premium volume, sophisticated domestic technology company involvement in insurance analytics including Ant Group's digital insurance analytics capabilities and Ping An's world-leading healthcare and motor insurance AI platforms, and government support for insurance sector technology modernisation.

MEA & Latin America Insurance Analytics Market Insights

The Middle East and Africa and Latin America are growing insurance analytics markets where expanding insurance sector development, increasing digital insurance distribution, and growing regulatory attention to insurance fraud and market conduct are creating initial but expanding analytics investment opportunities. UAE leads MEA insurance analytics revenues at approximately 28.4% of regional revenues through its well-developed financial services sector, sophisticated InsurTech regulatory sandbox enabling analytics innovation, and the concentration of regional insurance and reinsurance operations in the Dubai International Financial Centre. Brazil leads Latin American revenues at approximately 43.7% through its large insurance market, active InsurTech ecosystem, and growing regulatory focus on claims fraud that creates compelling analytics investment justification for Brazilian insurers.

Market Dynamics

Growth Drivers: Escalating insurance fraud burden and underwriting loss ratio pressure creating financially compelling ROI for analytics investment combined with AI and alternative data availability

The primary structural growth drivers for the insurance analytics market are the financially quantifiable returns on analytics investment available through fraud detection improvement, underwriting loss ratio reduction, claims adjudication cost reduction, and customer retention improvement that create commercially compelling business cases for analytics platform procurement independent of technology trend motivation, combined with the progressive availability of alternative data sources including telematics, IoT sensor networks, satellite imagery, and digital behavioral data that enable analytics capabilities for granular individual risk assessment that conventional actuarial modelling of historical loss data cannot replicate.

Restraints: Data privacy regulatory complexity constraining alternative data use in underwriting decisions, algorithmic bias concerns in AI-driven underwriting creating regulatory and reputational risk

A significant restraint on the insurance analytics market is the regulatory complexity around the use of alternative data and AI models in insurance underwriting decisions, where the permissibility of specific data types as rating factors varies significantly across jurisdictions and the algorithmic fairness concerns that arise when machine learning models use proxy variables correlated with protected characteristics create both regulatory compliance risk and reputational exposure that constrains the aggressiveness of analytics-driven underwriting transformation at major carriers operating across multiple regulatory jurisdictions.

Opportunities: Real-time claims analytics and straight-through processing eliminating manual adjudication for routine claims, climate risk analytics creating new catastrophe exposure management capabilities

The commercialization of AI-powered claims straight-through processing, where machine learning models that classify claim type, estimate severity, verify coverage, and assess fraud probability enable routine low-complexity claims to be automatically adjudicated and paid within minutes of digital submission without any human claims adjuster involvement, represents the highest-return analytics application in current deployment across multiple insurance lines including auto physical damage, travel insurance, and crop insurance, and its progressive extension to additional claim types and complexity tiers represents a sustained market growth opportunity.

Recent Developments:

-

2025: Verisk Analytics expanded its insurance analytics platform with new AI-powered aerial imagery analysis capabilities that automatically assess property condition, identify roof damage, and quantify exposure for catastrophe underwriting from high-resolution satellite and drone imagery, reducing the manual inspection requirements for property insurance risk assessment at renewal and post-catastrophe claims triage.

-

2025: SAS Institute launched its SAS Viya for Insurance platform update incorporating generative AI capabilities for automated claims documentation analysis, regulatory filing preparation, and policy document interrogation that reduce the skilled labor hours required for complex insurance administrative functions by 30 to 50% in early adopter carrier deployments.

-

2025: LexisNexis Risk Solutions expanded its insurance analytics data assets with new alternative data integrations including gig economy income verification, rental payment history, and digital banking transaction analysis that improve underwriting accuracy for consumer segments with limited conventional credit file depth.

Insurance Analytics Market key players are:

-

IBM Corporation

-

Oracle Corporation

-

SAP SE

-

SAS Institute Inc.

-

Verisk Analytics Inc.

-

LexisNexis Risk Solutions

-

Majesco

-

Guidewire Software Inc.

-

Duck Creek Technologies

-

Pegasystems Inc.

-

Sapiens International Corporation

-

EIS Group

-

Applied Systems

-

OneShield Software

-

Arity (Allstate)

-

Tractable Ltd.

-

Shift Technology

-

FRISS

-

Quantemplate

-

Bdeo

Insurance Analytics Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 17.60 Billion |

| Market Size by 2035 | USD 72.39 Billion |

| CAGR | CAGR of 15.19% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Software, Services) • By Application (Claims Management, Risk Management, Customer Management, Policy Management, Process Management, Others) • By Deployment (Cloud, On-premise) • By Enterprise Type (Large Enterprises, Small & Medium Enterprises) • By End-User (Insurance Firms, Government Agencies, Third-Party Administrators, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | IBM Corporation, Oracle Corporation, SAP SE, SAS Institute Inc., Verisk Analytics Inc., LexisNexis Risk Solutions, Majesco, Guidewire Software Inc., Duck Creek Technologies, Pegasystems Inc., Sapiens International Corporation, EIS Group, Applied Systems, OneShield Software, Arity (Allstate), Tractable Ltd., Shift Technology, FRISS, Quantemplate, Bdeo |

Frequently Asked Questions

North America dominated the insurance analytics market in 2025.

Cloud dominated with approximately 65.18% of revenues in 2025.

Escalating insurance fraud burden creating financially compelling ROI for analytics investment combined with AI and alternative data availability.

The insurance analytics market was valued at USD 17.60 billion in 2025.

The insurance analytics market is expected to grow at a CAGR of 15.19% from 2026 to 2035.

Get in Touch