Cybersecurity in Critical Infrastructure Market Report Scope & Overview:

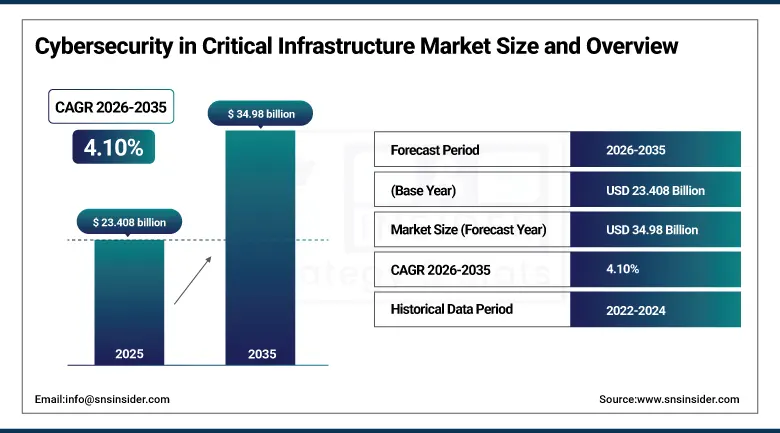

The Cybersecurity in Critical Infrastructure Market was valued at USD 23.408 billion in 2025 and is expected to reach USD 34.98 billion by 2035, growing at a CAGR of 4.10% from 2026–2035.

The global cybersecurity in critical infrastructure market addresses one of the most urgent and consequential national security imperatives in the digital age, as the world's essential service systems encompassing energy grids, water treatment, transportation networks, financial institutions, healthcare systems, and telecommunications infrastructure become progressively more digitally interconnected, automated, and dependent on internet-connected operational technology that simultaneously improves operational efficiency and dramatically expands the cyber-attack surface available to sophisticated adversaries. Critical infrastructure cyber incidents are no longer theoretical risks but documented, recurring, and increasingly damaging events the 2021 Colonial Pipeline ransomware attack disrupting fuel supply across the U.S. Eastern Seaboard, Ukraine's power grid cyber-attacks plunging hundreds of thousands into darkness, and the SolarWinds supply chain compromise penetrating multiple U.S. federal agencies demonstrate that cyber-attacks on critical infrastructure can produce physical, societal, and economic damage on a scale comparable to conventional military action. The market encompasses both the cybersecurity segment addressing digital threats to information technology and operational technology networks, and the physical security segment encompassing video surveillance, access control, perimeter defense, and intrusion detection that collectively protect critical facilities from physical infiltration and sabotage.

They reflect the conventional structural demand that stems from the digital transformation of critical infrastructure systems that is constantly increasing cybersecurity investment requirements, along with the ongoing increase in regulatory mandates provided by CISA, NIS2 and sectoral cyber security via non-compliance fines as voluntary best practice is turned into compulsory compliance investments across all sectors of critical infrastructure.

Market Size and Forecast

-

Market Size in 2026E: USD 24.36 Billion

-

Market Size by 2035: USD 34.98 Billion

-

CAGR (2026-2035): 4.10% from 2026 to 2035

-

Fastest Growing Region: Asia-Pacific

-

Largest Region: North America

To Get more information on Cybersecurity in Critical Infrastructure Market - Request Free Sample Report

Cybersecurity in Critical Infrastructure Market Trends

-

Rapid adoption of zero-trust architecture in critical infrastructure, replacing perimeter-based trust with continuous verification and least-privilege access across IT/OT environments.

-

Increasing use of AI-driven threat detection in SOCs for real-time anomaly detection across SCADA, ICS, and OT systems at scale.

-

Rising OT cybersecurity investment due to IT–OT convergence eliminating traditional air-gap isolation and increasing exposure to cyber threats.

-

Strengthening regulatory compliance requirements under frameworks such as CISA CPG, EU NIS2, and sector-specific mandates, shifting cybersecurity from optional to mandatory.

-

Expanding cybersecurity information sharing and coordinated response programs between governments and operators through ISACs and national defense initiatives.

The U.S. Cybersecurity in Critical Infrastructure Market Size Outlook

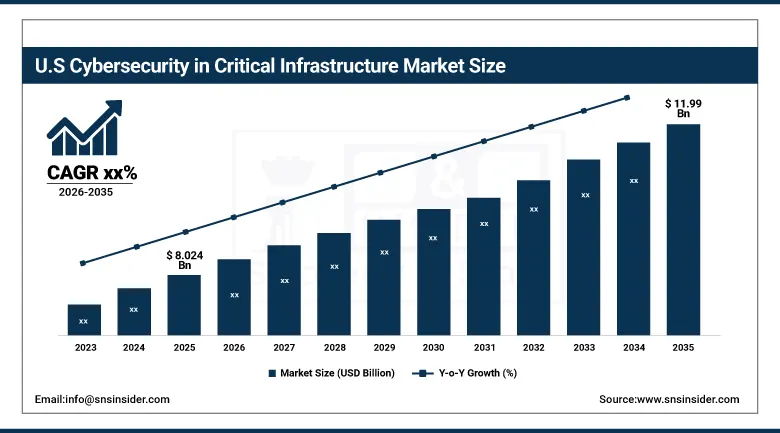

The U.S. Cybersecurity in Critical Infrastructure Market was valued at approximately USD 8.024 billion in 2025 and is expected to reach approximately USD 11.99 billion by 2035, driven by federal regulatory mandates, NSS programme investment, and private sector compliance spending.

The U.S. Cybersecurity in Critical Infrastructure Market is led by the most comprehensive federal critical infrastructure cybersecurity regulatory framework around the globe, anchored by CISA's authority over 16 critical infrastructure sectors and with the National Cybersecurity Strategy establishing mandatory minimum cybersecurity requirements as well as a White House National Security Memorandum on Critical Infrastructure Security that will create more than any national market an unprecedented government-driven mandate for cybersecurity investment. CISA's State and Local Cybersecurity Grant Programme; the DOE's Office of Cybersecurity, Energy Security, and Emergency Response; and the EPA's water system cybersecurity programme account for federal investment in critical infrastructure cybersecurity while collectively providing support to private sector investment that makes up the bulk of U.S. critical infrastructure cybersecurity spending.

In January 2025, a 46% spike in ransomware attacks on industrial operators was documented, with cybercriminals increasingly targeting OT environments to maximise disruption, confirming that the threat landscape driving critical infrastructure cybersecurity investment is intensifying at a pace that sustains market demand growth through the forecast period. The April 2025 CISA advisory on key vulnerabilities in widely deployed Siemens and Schneider Electric industrial control systems leading to a 15% increase in 30-day patching activity demonstrates the real-time regulatory enforcement mechanisms that are converting identified vulnerabilities into immediate cybersecurity investment across critical infrastructure operators.

Cybersecurity in Critical Infrastructure Market Segment Analysis

-

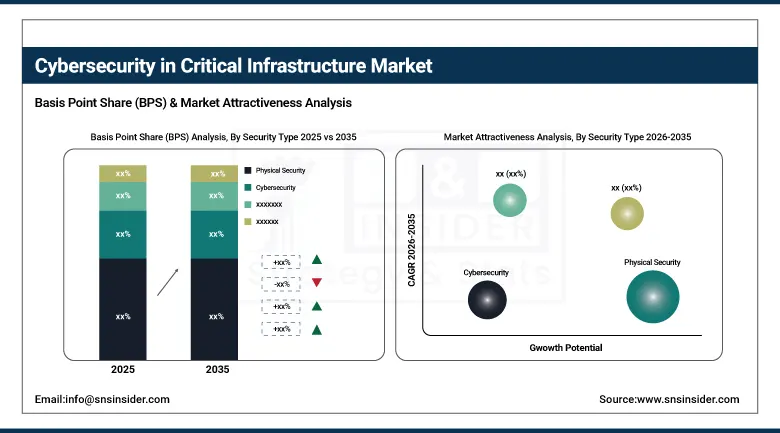

By Security Type, Physical Security dominated with approximately 69% revenue share in 2025 through surveillance, access control, and perimeter defense solutions essential across critical facilities; Cybersecurity is the fastest-growing segment at approximately 5.95% CAGR from 2026 to 2035, driven by rising ransomware, data breach, and OT network attack incidents.

-

By Solution, Firewall and SCADA Security solutions dominated as foundational network perimeter protection; Managed Services is the fastest-growing service type at approximately 5.80% CAGR as operators turn to external expertise for continuous threat monitoring and incident response.

-

By End-User, BFSI dominated with approximately 24% market share in 2025 as the highest-value target for cybercrime requiring the most stringent security frameworks; Oil and Gas is the fastest-growing end-user at approximately 7.13% CAGR driven by growing cyber and physical threats to exploration, production, and distribution facilities.

By Security Type, physical security dominates the cybersecurity in critical infrastructure market, cybersecurity is expected grows fastest

Physical Security retained the dominant Security Type position with approximately 69% of the cybersecurity in critical infrastructure market in 2025, due to a large installed base and continued investment in foundational measures such as video surveillance, perimeter defense, intrusion detection and access control technologies across all facility types regardless of digital transformation maturity level. Physical security at critical infrastructure facilities including power stations, water treatment plants, transportation hubs and financial institution data centres concerns with the immediate and instantly understood threat of physical infighting infiltrating on, sabotage or theft which has been enduringly invested in in by facility operators for decades and is currently being increased upon with each passing year through AI-powered video analytics capabilities, biometric access control and drone detection systems that progressively enhance capability to detect threats across 75% of overall Threat sensitivity.

Cybersecurity is the fastest-growing segment at approximately 5.95% CAGR from 2026 to 2035, due to an increasing volume and complexity of digital attacks targeting critical infrastructure operational technology systems; a growing digitally-connected attack target surface, driven largely by Industry 4.0 OT modernization programmers and increasingly vast regulatory directives mandating formally documented risk mitigation strategies across critical infrastructure operators. The 46% increase in ransomware attacks on industrial operators in January 2025 that has been documented and the increasingly severe national-state cyber threat from adversaries targeting energy, water, and financial infrastructure all point to cybersecurity investment as one of the fastest growing critical-infrastructure security priorities through the forecast period.

By Solution, firewall and Scada security dominates the cybersecurity in critical infrastructure market, managed security services are expected to grows fastest

By solution, Firewall and SCADA security solutions dominate the cybersecurity in critical infrastructure market as essential foundational layers for network perimeter defense and operational technology protection, particularly across energy, utilities, transportation, and industrial control systems. These solutions remain critical for safeguarding legacy and modern infrastructure from unauthorized access and system disruptions.

Managed Security Services is the fastest-growing segment, expanding at approximately 5.80% CAGR, because critical infrastructure operators increasingly depend on external cybersecurity expertise to help them maintain threat visibility, advanced analytics as well as rapid incident response capabilities. The complexity of cyber threats is increasing, in-house resources are sparse and organizations need round-the-clock security operations in diverse environments that always seem to be interconnected and mission-critical.

By End-User: BFSI dominates the cybersecurity in critical infrastructure market, oil and gas is expected to grows fastest

BFSI is the dominant end-user position with approximately 24% of the cybersecurity in critical infrastructure market in 2025, reflecting financial institutions' status as the highest-value and most frequently targeted critical infrastructure sector for cybercrime and fraud, combined with the most stringent and globally harmonized regulatory cybersecurity requirements encompassing PCI DSS, DORA, Basel III operational resilience requirements, and sector-specific national regulations that mandate continuous cybersecurity investment and audit compliance documentation. Financial infrastructure's systemic importance to the global economy, where successful cyber-attacks on payment systems, securities exchanges, and banking infrastructure can cascade into broader economic instability, creates political and regulatory imperatives for the highest cybersecurity investment standards of any critical infrastructure sector.

Oil and Gas is the fastest-growing end-user segment at approximately 7.13% CAGR from 2026 to 2035, with the rise of digital transformation across exploration, production and distribution infrastructure, unique challenges posed by high consequence operational technology environments in energy supply chains as well as IPOGEO and adversarial targeting of energy supply chains creating new vulnerabilities that threat access to critical data likely disrupting operations which is expected to drive investment. These high-consequence OT environments motivate premium cybersecurity investment because cyber attacks can lead to catastrophic physical safety events, environmental damage, and energy supply disruption offshore platform operational technology, onshore pipeline SCADA systems and liquefied natural gas terminal control systems. SCADA and ICS infrastructure of the sector was developed for reliability and availability more than cyber security, manifesting fundamental vulnerability remediation requirements for which end-users invest faster than all other sectors grow, by investments.

Regional Analysis:

|

Region |

Major Country |

Share within Region,2025 (%) |

|---|---|---|

|

North America |

United States |

83% |

|

Europe |

Germany |

29% |

|

Asia Pacific |

China |

43% |

|

Middle East & Africa |

Saudi Arabia |

29% |

|

Latin America |

Brazil |

43% |

North America Cybersecurity in Critical Infrastructure Market Insights

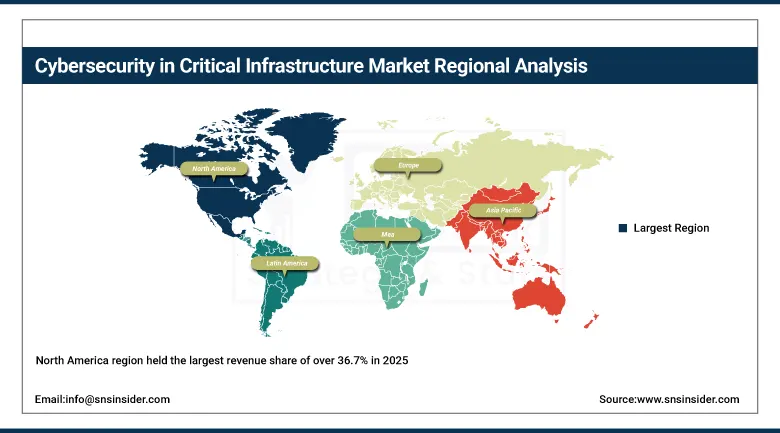

The North America region held the largest revenue share of over 36.7% in 2025 which was led by positioned to manage (U.S.) capturing close to 83% of its shareout revenues across North American markets. CISA's broad critical infrastructure cybersecurity authority; the world's largest federal investment in critical infrastructure protection, DOD and NSA/Cyber Command threat intelligence driving our defensive posture, and major private sector investments by the nation's energy, financial services, transportation, and healthcare critical infrastructure operators meeting sector-specific cybersecurity requirements cement U.S. market leadership.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Cybersecurity in Critical Infrastructure Market Insights

Europe is a mature critical infrastructure cybersecurity market, influenced by requirements of the NIS2 Directive for cybersecurity obligations to be extended to a wider range of critical entities, together with Dutch strength in industrial cybersecurity and UK drive towards national resilience due to designation of Critical Infrastructure as a Tier 1 national security priority

Asia Pacific Cybersecurity in Critical Infrastructure Market Insights

Asia Pacific is the fastest-growing regional market at approximately 6.87% CAGR through 2035, owing to supporting factors such as rapid industrialization expanding critical infrastructure footprint across China, India, Japan and Southeast Asia; government investment in national cybersecurity frameworks protecting strategic infrastructure and smart city programmes developing novel interconnected critical infrastructure that requires cybersecurity from deployment. Cybersecurity investment requirements for domestic critical infrastructure operators are increasingly comprehensive and mandatory through mechanisms such as the national critical information infrastructure protection regulations in China and the NCIIPC framework in India.

Latin America and Middle East & Africa Cybersecurity in Critical Infrastructure Market Insights

Latin America and the Middle East & Africa (MEA) are emerging regions in the cybersecurity in critical infrastructure market, driven by increasing digital transformation and rising cyber threats targeting essential services. In Latin America, countries such as Brazil, Mexico, Chile, and Colombia are strengthening national cybersecurity frameworks to protect sectors like energy, transportation, utilities, and financial services, with Brazil leading regulatory development while Mexico enhances resilience due to its integration with global supply chains. However, the region still faces challenges such as limited cybersecurity funding, uneven regulatory maturity, and skill shortages. Similarly, the MEA region is experiencing strong growth fueled by large-scale government-led initiatives, including Saudi Vision and the UAE National Cybersecurity Strategy, alongside major investments in securing oil & gas, utilities, and smart city infrastructure. African nations such as South Africa, Kenya, and Nigeria are also improving cybersecurity readiness through CERT development and regulatory reforms. Despite rapid progress, both regions continue to face challenges related to legacy infrastructure, varying maturity levels, and workforce gaps, though ongoing investments and international collaborations are steadily strengthening their cybersecurity capabilities.

Market Dynamics:

Growth Drivers: Escalating sophisticated cyber-attack frequency targeting critical infrastructure OT systems and mandatory regulatory compliance requirements creating structural cybersecurity investment demand

The underlying structural development drivers include the recorded increase in advanced, state-sponsored and criminal ransomware assaults against basic framework functional innovation frameworks constraining imperative cybersecurity speculation needs on administrators is currently joined with progressively compulsory administrative structures across CISA's U.S. area necessities, EU NIS2 and comparable public systems are changing intentional cybersecurity into consistence obligation with monetary assents chance for non-compliance.

The April 2025 CISA advisory of Siemens and Schneider Electric industrial control systems flaws widely used across global critical infrastructure, alongside the documentation in January 2025 of a 46% increase in ransomware attacks on industrial operators where the focus is specifically on OT environments confirm that with the rising future threat landscape combined with regulatory pressure will be increasing at the same time resulting sustains Cybersecurity in Critical Infrastructure Market's consistent growth through the forecast period 2026 to 2035.

Restraints: Legacy OT system cybersecurity incompatibility, high implementation cost for comprehensive critical infrastructure cybersecurity programmes, and workforce shortage in OT cybersecurity expertise

Legacy operational technology systems in energy, water, and transportation infrastructure were designed for operational reliability without cybersecurity controls, creating fundamental technical barriers to cybersecurity integration that require expensive custom engineering, extended implementation timelines, and careful operational risk management to address without compromising real-time operational safety. The severe shortage of OT cybersecurity specialists globally creates a human capital constraint on the pace of critical infrastructure cybersecurity programme implementation that no amount of capital budget increase can resolve without parallel investment in workforce training and development.

Opportunities: OT-specific threat detection platforms, critical infrastructure cybersecurity managed services, and cross-border threat intelligence sharing frameworks

The development of purpose-built OT cybersecurity platforms including Dragos, Claroty, and Nozomi Networks that provide passive network monitoring, asset discovery, and behavioral threat detection compatible with the real-time operational constraints of industrial control systems represents the highest-growth and highest-value product category in critical infrastructure cybersecurity. Managed security services specifically designed for critical infrastructure operators provide the expert threat monitoring and incident response capability that most operators cannot develop in-house, creating a premium recurring revenue market that grows proportionally with the expanding OT attack surface. International critical infrastructure cybersecurity cooperation frameworks enabling cross-border threat intelligence sharing and incident notification create the collective defence capabilities that individual national critical infrastructure protection programmes cannot achieve independently.

Recent Developments:

-

April 2025: CISA issued a major advisory outlining critical vulnerabilities in widely deployed Siemens and Schneider Electric industrial control systems used across global critical infrastructure, prompting a documented 15% increase in 30-day patching activity across affected organizations.

-

June 2025: Cisco unveiled a new industrial network architecture with embedded advanced security for campus, branch, and industrial environments, improving unified threat defense and OT-IT integration for critical infrastructure operators managing converged IT and OT networks.

-

2025: Dragos expanded its OT cybersecurity platform with new threat detection capabilities covering additional industrial control system protocols and expanded threat intelligence from its growing global sensor network monitoring critical infrastructure environments.

-

2025: Palo Alto Networks advanced its OT security capabilities with new industrial protocol deep inspection and SCADA network segmentation features targeting energy, utilities, and manufacturing critical infrastructure cybersecurity programmes.

-

January 2025: CISA launched expanded cybersecurity assessment services for water and wastewater system operators, providing free vulnerability assessments and security improvement recommendations to the critical infrastructure sector facing the most acute cybersecurity investment gaps.

Cybersecurity in Critical Infrastructure Market Key Players are:

-

Palo Alto Networks Inc.

-

Fortinet Inc.

-

Cisco Systems Inc.

-

Honeywell International Inc.

-

IBM Corporation

-

Siemens AG (Siemens Energy)

-

Thales Group SA

-

BAE Systems plc

-

Raytheon Technologies Corporation

-

Lockheed Martin Corporation

-

General Dynamics Corporation

-

Northrop Grumman Corporation

-

Dragos Inc.

-

Claroty Ltd.

-

Nozomi Networks Inc.

-

Waterfall Security Solutions Ltd.

-

Yokogawa Electric Corporation

-

Schneider Electric SE

-

Rockwell Automation Inc.

-

Leidos Holdings Inc.

Cybersecurity in Critical Infrastructure Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 23.40 Billion |

| Market Size by 2035 | USD 34.98 Billion |

| CAGR | CAGR of 4.10% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Security Type (Physical Security, Cybersecurity) • By Solution (Firewall, SCADA Security, Antivirus and Malware Protection, Encryption, Intrusion Detection and Prevention Systems, Data Loss Prevention, Others) • By Service (Consulting, Risk Assessment, Managed Services, Others) • By End-User (Energy and Utilities, Transportation, BFSI, Healthcare, Government and Defense, IT and Telecom, Oil and Gas, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Palo Alto Networks Inc., Fortinet Inc., Cisco Systems Inc., Honeywell International Inc., IBM Corporation, Siemens AG (Siemens Energy), Thales Group SA, BAE Systems plc, Raytheon Technologies Corporation, Lockheed Martin Corporation, General Dynamics Corporation, Northrop Grumman Corporation, Dragos Inc., Claroty Ltd., Nozomi Networks Inc., Waterfall Security Solutions Ltd., Yokogawa Electric Corporation. |

Frequently Asked Questions

BFSI dominated with approximately 24% market share in 2025 as financial institutions represent the highest-value target for cybercrime and fraud, face the most stringent regulatory cybersecurity compliance

Physical Security dominated with approximately 69% of revenues in 2025 through extensive video surveillance, access control, perimeter defense, and intrusion detection.

The escalating frequency of sophisticated ransomware and nation-state cyber-attacks targeting critical infrastructure OT systems, documented at a 46% increase in January 2025, combined with mandatory regulatory compliance requirements from

The Cybersecurity in Critical Infrastructure Market was valued at USD 23.408 billion in 2025.

The Cybersecurity in Critical Infrastructure Market is expected to grow at a CAGR of 4.10% during 2026-2035.

Get in Touch