IT & Telecom Cyber Security Market Report Scope & Overview:

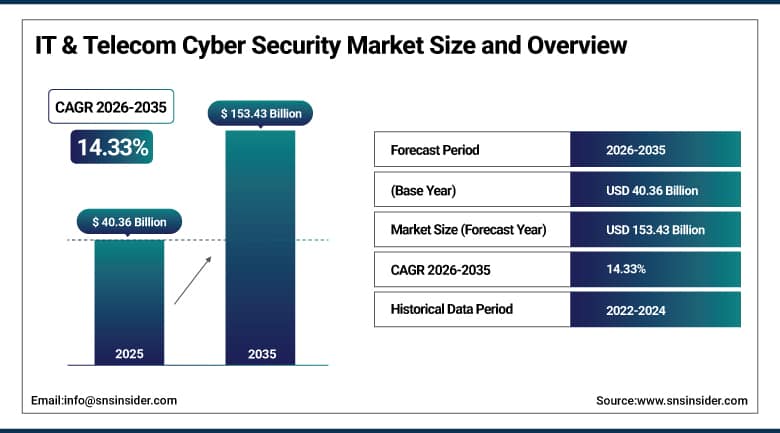

The IT & Telecom Cyber Security Market was valued at USD 40.36 Billion in 2025 and is expected to reach USD 153.43 Billion by 2035, growing at a CAGR of 14.33% from 2026 to 2035.

The global IT and telecom cyber security market is experiencing robust and accelerating growth as expanding digital infrastructure, the proliferation of connected devices, the mass adoption of cloud services, and the extraordinary pace of 5G network deployment collectively create an attack surface of unprecedented scale and complexity. The market is driven by a rapidly intensifying threat landscape encompassing ransomware campaigns, state sponsored network intrusions, supply chain attacks, distributed denial of service assaults, and insider threats whose frequency and sophistication continue escalating beyond the capability of conventional perimeter security architectures.

In 2024, Palo Alto Networks launched its AI driven Precision AI security platform, integrating real time threat intelligence from its Unit 42 research team with automated threat prevention across network, cloud, and endpoint security domains. The platform's machine learning models process more than one trillion security events daily to identify and block novel attack patterns before signature-based detection systems can update their threat databases, creating a proactive security posture that reduces mean time to detection and mean time to response across enterprise IT and telecom network environments.

Market Size and Forecast:

-

Market Size in 2026E: USD 46.15 Billion

-

Market Size by 2035: USD 153.43 Billion

-

CAGR: 14.33% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

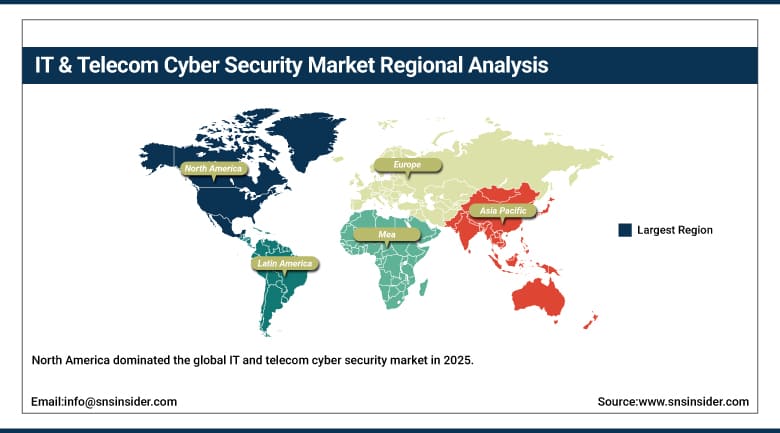

Largest Region: North America

To Get More Information On IT & Telecom Cyber Security Market - Request Free Sample Report

IT & Telecom Cyber Security Market Trends:

-

AI and machine learning are enhancing cybersecurity platforms by enabling automated threat detection, behavioral analytics, and faster incident response across enterprise environments

-

Growing adoption of zero trust security architectures is driving demand for continuous authentication, identity verification, least-privilege access, and network micro-segmentation solutions

-

Expansion of 5G networks is increasing investment in advanced cybersecurity technologies to protect network slicing, edge computing, and large-scale IoT deployments

-

Organizations are increasingly adopting Extended Detection and Response (XDR) platforms to unify endpoint, network, cloud, and identity security for improved threat visibility and response

-

Rising focus on quantum-resistant cryptography is accelerating investments in next-generation encryption technologies as organizations prepare for future post-quantum cybersecurity requirements

U.S. IT & Telecom Cyber Security Market Outlook:

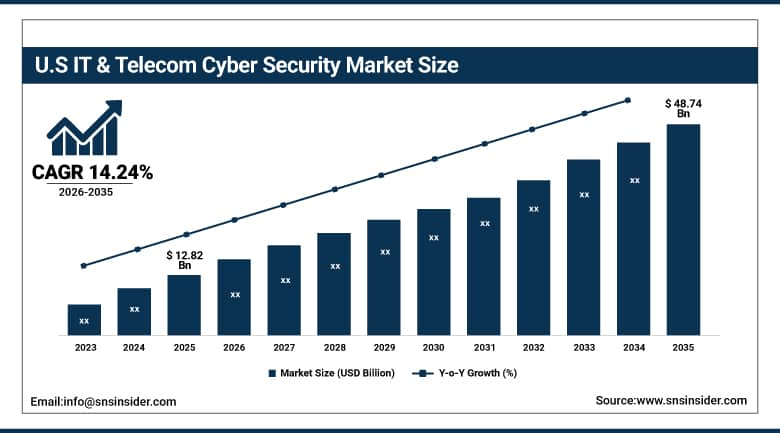

The U.S. IT & Telecom Cyber Security Market was valued at approximately USD 12.82 Billion in 2025 and is expected to reach approximately USD 48.74 Billion by 2035, growing at a CAGR of approximately 14.24%.

The U.S. is the world's most commercially significant IT and telecom cyber security market, hosting the global headquarters of Palo Alto Networks, CrowdStrike, Cisco Systems, Fortinet, IBM Security, and Microsoft Security, whose combined platform and service revenues define the commercial benchmark for enterprise cybersecurity spending globally. The CISA's mandatory cybersecurity incident reporting requirements for critical infrastructure operators, the SEC's cybersecurity disclosure rules for publicly traded companies, and the FCC's telecom network security standards collectively create a layered compliance environment that sustains non-discretionary cybersecurity investment across IT and telecom enterprises of all sizes.

In 2023, CrowdStrike expanded its Falcon XDR platform with enhanced cloud workload protection and identity threat detection capabilities, enabling unified visibility across endpoint, cloud, identity, and data domains within a single agent-based architecture. This integration directly addresses the lateral movement attack patterns that adversaries use to escalate privileges from initial endpoint compromise through identity infrastructure to cloud workload environments, creating a detection and response capability that siloed single domain security tools cannot provide.

IT & Telecom Cyber Security Market Segment Analysis:

-

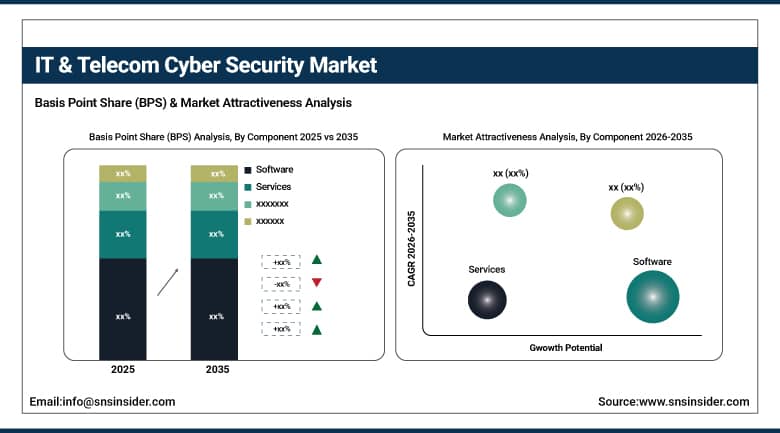

By Component, the Software segment dominated the IT & Telecom Cyber Security Market with approximately 47% share in 2025, while the Services segment is the fastest growing.

-

By Deployment, the On-Premise segment dominated the IT & Telecom Cyber Security Market with approximately 55% share in 2025, while the Cloud deployment segment is the fastest growing.

-

By Enterprise Size, the Large Enterprises segment dominated the IT & Telecom Cyber Security Market with approximately 68% share in 2025, while the Small and Medium-sized Enterprises segment is the fastest growing.

-

By Sub-Sector, the IT Companies segment dominated the IT & Telecom Cyber Security Market with approximately 52% share in 2025, while the Telecom Operators segment is the fastest growing.

By Component, software dominates, services grow fastest

Software retained the dominant component position with approximately 47% of the IT and telecom cyber security market in 2025. The software segment's commercial primacy reflects the fundamental role of security software as the primary investment category in enterprise cybersecurity programme’s whose threat detection, prevention, and response capability is delivered predominantly through software platforms rather than hardware appliances or human services engagement. Next generation firewall software, endpoint detection and response platforms, cloud access security brokers, security information and event management systems, and identity governance and administration tools collectively define the most commercially significant software security investment categories. Palo Alto Networks' comprehensive platform revenue exceeding USD 8 billion annually, CrowdStrike's subscription revenue growth trajectory, and Microsoft's security product revenue exceeding USD 20 billion annually demonstrate the extraordinary commercial scale of enterprise security software procurement in the IT and telecom sector.

Services are the fastest growing component because the global cybersecurity talent shortage, estimated at 3.4 million unfilled cybersecurity positions worldwide, creates structural motivation for organizations to outsource security functions they cannot staff internally. Each managed security service contract that replaces a security operations center staffing requirement with an outsourced service delivery model creates recurring services revenue whose predictable subscription structure sustains above average segment growth. Incident response retainer services, whose guaranteed response capability for security breach scenarios creates procurement motivation independent of actual incident occurrence, and penetration testing services, whose regulatory and cyber insurance compliance creates annual procurement cycles, collectively sustain services segment growth above hardware and software component alternatives.

By Deployment, on-premise dominates, cloud grows fastest

On-premise deployment retained the dominant position with approximately 55% of the IT and telecom cyber security market in 2025. Large telecom operators' network security infrastructure, data center operators' physical and logical security systems, and enterprise IT companies' perimeter and internal network security investments create on premise security procurement whose scale, customization requirement, and data sovereignty sensitivity sustain local deployment preference over cloud alternatives. Telecom operators' network core security, whose real time traffic inspection, signaling firewall, and lawful intercept functions create processing latency requirements that cloud delivery cannot satisfy, sustains on premise security deployment as the technically mandatory architecture for network infrastructure protection regardless of commercial cloud adoption progress in enterprise IT environments.

Cloud deployment is the fastest growing model because SaaS delivered security platforms' scalability, automatic update delivery, and subscription economics create adoption advantages that compound with enterprise IT workload migration to public cloud environments. Each enterprise that migrates workloads to AWS, Microsoft Azure, or Google Cloud Platform creates cloud native security procurement for cloud workload protection platforms, cloud security posture management, and data access governance tools whose native cloud integration advantage over on-premise alternatives creates specification preference. The cloud security segment's growth compounds with the overall enterprise cloud adoption trajectory whose momentum sustains above average security procurement growth through the forecast period.

By Enterprise Size, large enterprises dominate, SMEs grow fastest

Large enterprises retained the dominant enterprise size position with approximately 68% of the IT and telecom cyber security market in 2025. The commercial concentration of cybersecurity spending among large enterprises reflects their combination of extensive sensitive data assets, complex regulatory compliance obligations, large attack surfaces encompassing thousands of endpoints and applications, and the financial capacity to invest in comprehensive multi-layer security architectures. Each large IT enterprise whose annual cybersecurity budget may range from tens of millions to hundreds of millions of dollars creates procurement relationships with security platform vendors whose enterprise contract values sustain the segment's revenue dominance despite large enterprises representing a much smaller population than SMEs. Telecom operators' network security investment, whose scale reflects the critical national infrastructure designation of communications networks, sustains particularly large individual enterprise security spending that elevates the segment's commercial concentration.

Small and medium sized enterprises are the fastest growing segment at approximately 15.66% CAGR because the increasing frequency of SME targeted cyber-attacks, the growing cyber insurance market's security requirement mandates, and the availability of affordable cloud-based security solutions are collectively creating first time and upgrade cybersecurity investment among businesses that previously underinvested in formal security programmes. Each ransomware incident affecting SMEs that generates media coverage creates market awareness among peer businesses whose motivation to avoid equivalent disruption drives security procurement. The cyber insurance market's progressive tightening of coverage requirements for minimum security controls creates structured procurement motivation that sustains SME cybersecurity market growth throughout the forecast period.

By Sub-Sector, IT companies dominate, telecom operators grow fastest

IT companies retained the dominant sub sector position with approximately 52% of the IT and telecom cyber security market in 2025. Enterprise software providers, systems integrators, data center operators, cloud service providers, and IT consulting firms create the most commercially concentrated cybersecurity investment of any sub sector through their dual role as both cybersecurity product users and delivery intermediaries. Each major system integrator that embeds cybersecurity into client engagement delivery creates security procurement at both its own enterprise and client delivery levels, creating a multiplier effect on commercial procurement volume. Cloud service providers' security investment, whose data center physical and logical security, network protection, and platform security create the most commercially intensive per facility cybersecurity procurement of any enterprise category, sustains IT companies' dominant sub sector revenue concentration.

Telecom operators are the fastest growing sub sector because 5G network deployment's expanded attack surface, network function virtualization’s software defined network architecture vulnerability, and the telecom sector's critical national infrastructure designation create structured and growing cybersecurity investment compelled by regulatory mandate, commercial continuity requirements, and the catastrophic reputational consequences of network security breaches. Each 5G network slice deployment creates application specific security requirements that 4G era security infrastructure cannot address, generating new security procurement cycles. BAE Systems' telecom signaling firewall development, IBM's telecom threat intelligence deployment across 80 telecom operators, and Kaspersky's telecom fraud detection system collectively demonstrate the extraordinary commercial scale of telecoms specific cybersecurity procurement.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America IT & Telecom Cyber Security Market Insights

North America dominated the global IT and telecom cyber security market in 2025, underpinned by advanced digital infrastructure, stringent regulatory compliance requirements, high cybersecurity awareness, and the commercial presence of the world's largest cybersecurity platform vendors. The United States accounts for approximately 87.4% of North American revenues through Palo Alto Networks, CrowdStrike, Cisco Systems, Fortinet, IBM Security, and Microsoft Security's enterprise procurement relationships that define global security platform market standards.

Canada contributes approximately 12.6% of North American revenues through its telecommunications sector's network security investment, the financial services industry's data protection compliance, and the federal government's critical infrastructure cybersecurity mandate that creates structured public sector procurement from both enterprise and government security buyers.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe IT & Telecom Cyber Security Market Insights

Europe is a technically sophisticated and compliance driven cybersecurity market where the GDPR's data protection requirements, the NIS2 Directive's expanded critical entity security obligations, and the EU's Cybersecurity Act's certification framework create a layered regulatory environment that sustains substantial non-discretionary cybersecurity investment across IT and telecom enterprises. Germany accounts for approximately 22.3% of European revenues through its manufacturing and IT sector digital security investment, Deutsche Telekom's network security programme, and the BSI's federal cybersecurity standards that create procurement compliance motivation.

The United Kingdom, France, and the Netherlands are significant secondary markets where NCSC's cyber resilience guidance, BNP Paribas and ING's financial sector security investment, and the Amsterdam Internet Exchange's critical infrastructure protection create consistent procurement. Atos SE's European cybersecurity practice and Thales Group's cybersecurity division sustain regional supply capability.

Asia Pacific IT & Telecom Cyber Security Market Insights

Asia Pacific is the fastest growing regional IT and telecom cyber security market, driven by China's extraordinary digital economy scale, India's IT sector growth and cybersecurity regulation strengthening, Japan's critical infrastructure protection investment, South Korea's advanced telecommunications security, and the ASEAN region's accelerating digital transformation. China accounts for approximately 44.8% of Asia Pacific revenues through its IT enterprise security investment scale, the telecommunications sector's network security procurement, and the government's cybersecurity law compliance requirement that creates mandatory security investment across critical information infrastructure operators.

India represents the most commercially dynamic emerging market within Asia Pacific where the IT and business process outsourcing sector's data protection compliance, the CERT-In's mandatory cybersecurity incident reporting framework effective from 2022, and the rapidly growing telecom sector's 5G security investment create above average cybersecurity market growth from both compliances driven and commercially motivated procurement sources.

MEA & Latin America IT & Telecom Cyber Security Market Insights

The UAE leads MEA revenues at approximately 31.2% through its smart city infrastructure security investment, ADNOC's operational technology cybersecurity programme, and the Abu Dhabi and Dubai financial sector's data protection compliance creating structured institutional demand. Saudi Arabia's NCA cybersecurity regulatory framework adds substantial complementary Gulf demand. Brazil leads Latin American revenues at approximately 44.2% through its LGPD data protection regulation compliance investment, the financial services sector's security procurement, and the telecom sector's 5G security deployment. Mexico's IT sector and Colombia's digital transformation collectively sustain regional growth through 2035.

Market Dynamics:

Growth Drivers: Escalating cyber threat frequency and 5G network deployment expanding the attack surface requiring dedicated security investment

The escalating frequency, sophistication, and financial impact of cyber-attacks targeting IT and telecom enterprises is the market's most commercially compelling structural growth driver. The IBM Cost of a Data Breach Report documented the average cost of a data breach at USD 4.88 million globally in 2024, representing the highest recorded average and creating financial loss exposure that dwarfs cybersecurity investment requirements at most enterprise scales. Each ransomware campaign that encrypts operational systems, each state sponsored intrusion that exfiltrates intellectual property, and each supply chain attack that compromises trusted software distribution channels creates market awareness and procurement urgency that sustains above average security investment growth across the IT and telecom sector.

5G network deployment's architectural transformation of telecommunications infrastructure creates the most commercially significant new security investment driver in the telecom sub sector. Network slicing, network function virtualization, edge computing deployment, and the connection of more than one billion IoT devices through 5G infrastructure collectively expand the telecom attack surface beyond the perimeter that 4G security architecture was designed to protect. Each telecom operator whose 5G network deployment requires purpose-built security controls for virtualized network functions, network slice isolation enforcement, and edge computing workload protection creates new security procurement categories with no direct 4G predecessor.

Restraints: Global cybersecurity talent shortage and high implementation cost for comprehensive security architectures

The global cybersecurity talent shortage, estimated at 3.4 million unfilled cybersecurity positions by ISC2's 2023 Cybersecurity Workforce Study, creates a structural constraint on organizations’ ability to implement, operate, and maintain comprehensive security programme’s regardless of budget availability. Each security operations center that requires 24 by 7 analyst coverage for threat monitoring and incident response creates staffing requirements that the available talent pool cannot satisfy at current compensation rates in most markets, motivating managed security service adoption as the operational alternative.

High implementation cost for comprehensive zero trust security architecture, whose identity, network, endpoint, application, and data security domain investment collectively creates total programme costs ranging from millions to tens of millions of dollars for large enterprises, creates budget allocation challenges that delay or compromise the scope of security architecture modernization. Each legacy security infrastructure replacement programme whose migration complexity creates multiyear transition timelines creates interim security posture gaps that sustain risk exposure during the transition.

Opportunities: AI powered security automation and quantum safe cryptography migration investment

AI powered security automation represents the most commercially transformative near-term opportunity whose autonomous threat detection, investigation, and response capability creates security operations scale that human analyst teams cannot achieve at equivalent cost. Each security platform deployment whose AI automation reduces tier 1 analyst workload by 70 to 80 percent creates measurable ROI that sustains premium platform pricing above conventional SIEM and security operations center tooling alternatives. The market for AI security automation compounds with the cybersecurity talent shortage, whose staffing gap creates commercial motivation for automation investment that sustains above market growth in the AI security segment.

Quantum safe cryptography migration represents the most commercially certain long duration market opportunity whose NIST post quantum cryptography standard publication in 2024 creates a defined technical migration pathway that every organization relying on RSA or elliptic curve encryption must execute before quantum computers capable of breaking current encryption become available. Each enterprise whose encrypted data backlog or long lived cryptographic key infrastructure requires quantum safe migration creates a multiyear security investment programme whose commercial aggregate across the global IT and telecom sector sustains substantial incremental security procurement.

Recent Developments:

-

2024: Palo Alto Networks launched its AI driven Precision AI security platform in 2024, integrating real time threat intelligence from Unit 42 with automated threat prevention across network, cloud, and endpoint domains processing more than one trillion security events daily.

-

2024: CrowdStrike expanded its Falcon XDR platform in 2024 with new adversary intelligence integration and enhanced cloud security posture management capabilities, enabling unified detection and response across endpoint, identity, cloud workload, and third-party telemetry sources within a single platform architecture.

-

2023: CrowdStrike expanded its Falcon XDR platform in 2023 with enhanced cloud workload protection and identity threat detection, enabling unified visibility across endpoint, cloud, identity, and data domains to address lateral movement attack patterns used in advanced persistent threat campaigns.

-

2023: IBM deployed telecom threat intelligence systems across 80 telecom operators globally in 2023, improving network threat detection efficiency by approximately 45 percent through AI powered anomaly detection applied to network signaling, roaming, and core network traffic patterns.

-

2023: Cisco Systems launched its Security Cloud unified platform in 2023, consolidating network security, cloud security, and endpoint protection into a single integrated architecture with AI powered threat correlation that reduces the alert fatigue burden on security operations center analysts managing complex hybrid enterprise environments.

IT & Telecom Cyber Security Market Key Players:

-

Palo Alto Networks Inc.

-

CrowdStrike Holdings Inc.

-

Cisco Systems Inc.

-

Fortinet Inc.

-

IBM Corporation (IBM Security)

-

Microsoft Corporation (Microsoft Security)

-

Check Point Software Technologies Ltd.

-

Broadcom Inc. (Symantec Enterprise)

-

Trend Micro Incorporated

-

Juniper Networks Inc.

-

Zscaler Inc.

-

SentinelOne Inc.

-

Trellix (FireEye and McAfee Enterprise)

-

Rapid7 Inc.

-

Darktrace plc

-

BAE Systems plc

-

Thales Group SA

-

Atos SE

-

HCL Technologies Ltd.

-

Wipro Limited

IT & Telecom Cyber Security Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 40.36 Billion |

| Market Size by 2035 | USD 153.43 Billion |

| CAGR | CAGR of 14.33% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Component (Software, Hardware, Services) • by Deployment (On-Premise, Cloud) • by Enterprise Size (Large Enterprises, Small and Medium-sized Enterprises) • by Sub-Sector (IT Companies, Telecom Operators, Managed Service Providers, Cloud Service Providers) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Palo Alto Networks Inc., CrowdStrike Holdings Inc., Cisco Systems Inc., Fortinet Inc., IBM Corporation (IBM Security), Microsoft Corporation, Check Point Software Technologies Ltd., Broadcom Inc., Trend Micro Incorporated, Juniper Networks Inc., Zscaler Inc., SentinelOne Inc., Trellix (FireEye and McAfee Enterprise), Rapid7 Inc., Darktrace plc, BAE Systems plc, Thales Group SA, Atos SE, HCL Technologies Ltd., Wipro Limited |

Frequently Asked Questions

The IT & Telecom Cyber Security Market is expected to grow at a CAGR of 14.33% from 2026 to 2035.

The IT & Telecom Cyber Security Market was valued at USD 40.36 Billion in 2025.

Escalating cyber-attack frequency and financial impact creating non-discretionary security investment, and 5G network deployment expanding the telecom attack surface with network slicing, virtualized network functions, and IoT connectivity requiring purpose-built security controls that 4G era security infrastructure cannot provide.

Software dominated the IT & Telecom Cyber Security Market with approximately 47% share in 2025, while Services is the fastest growing segment.

North America dominated the IT & Telecom Cyber Security Market in 2025, while Asia Pacific is the fastest growing region driven by China's digital economy scale and India's cybersecurity regulatory framework expansion.

Get in Touch