Lab-on-a-Chip Market Report Scope & Overview:

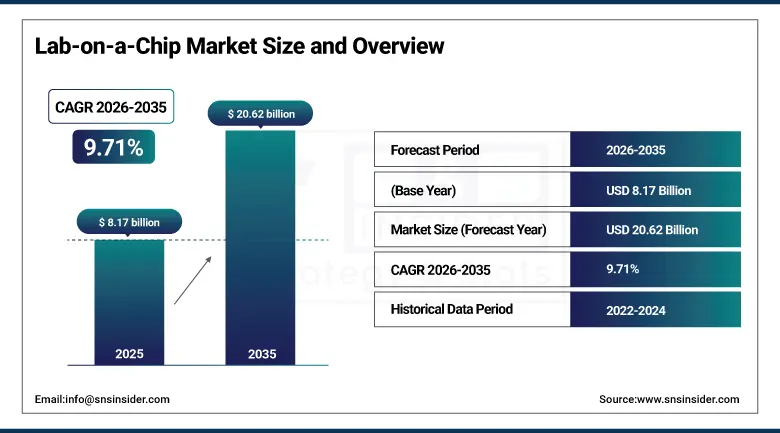

The Lab-on-a-Chip Market size was valued at USD 8.17 billion in 2025 and is expected to reach USD 20.62 billion by 2035, growing at a CAGR of 9.71% from 2026-2035.

The market for Lab-on-a-Chip (LoC) is witnessing significant growth, owing to breakthrough technologies being developed in areas such as microfluidics, biosensors, and device miniaturization, which are together revolutionizing the field of diagnostic tools that can be portable, fast, and cheap. The LoC is a tool that integrates one or multiple functions of a lab into a chip, which is only a few square centimeters in size. It performs better compared to conventional laboratory tests in terms of speed, accuracy, and efficiency. LoC is becoming essential for PoC diagnostics, especially in developing countries, as it offers quick and sensitive results with the use of small samples. An increasing prevalence of chronic and infectious diseases globally, along with the growing trend of personalized medicines and real-time patient monitoring, are factors driving the demand for LoC.

Moreover, the integration of Lab-on-a-Chip platforms with IoT connectivity and laboratory automation is enabling seamless data sharing, remote diagnostics, and enhanced workflow efficiency expanding both the reach and the clinical utility of LoC-based solutions.

Market Size and Forecast

-

Market Size in 2025: USD 8.17 Billion

-

Market Size by 2035: USD 20.62 Billion

-

CAGR: 9.71% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Lab-on-a-Chip Market - Request Free Sample Report

Lab-on-a-Chip Market Trends

-

Fast growth in point-of-care diagnostic testing, resulting in an increasing number of LoC devices being used in large quantities.

-

Increased use of AI and machine learning capabilities in LoC systems for instant data processing, predictive diagnostics, and remote patient monitoring.

-

High demand for drug discovery technologies using LoC devices from pharmaceutical and biotechnology industries.

-

More use of organ-on-a-chip technologies in place of animal testing as a more effective and affordable method for drug development.

-

Microfluidic fabrication advancements, such as 3D printing and soft lithography, leading to lower fabrication costs and faster prototyping.

-

Application of LoC technology in genomic testing, liquid biopsy, and next-generation sequencing as part of the precision medicine paradigm.

-

Increasing investments in research and development of Lab-on-a-Chip platforms by governments and the private sector for infectious disease detection, environmental monitoring, and food safety tests.

U.S. Lab-on-a-Chip Market Size Outlook:

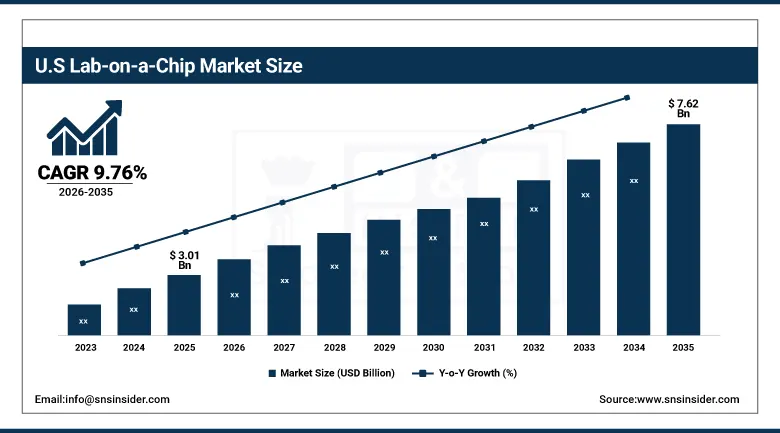

The U.S. Lab-on-a-Chip Market was valued at USD 3.01 billion in 2025 and is expected to reach USD 7.62 billion by 2035, registering a CAGR of 9.76% during 2026-2035. The United States is among the biggest markets for the Lab-on-a-chip due to its well-established healthcare infrastructure, abundant government funding of biomedical research, and presence of many top-ranking research universities and biotechnology companies. Major research institutions such as Massachusetts Institute of Technology, Harvard Medical School, and many more have been working on the development of the microfluidic and biosensor technologies. Some leading biotechnology companies including Fluidigm Corporation, Thermo Fisher Scientific, Abbott Laboratories, and Danaher Corporation have been involved in the creation of commercial uses of the LoCs in different areas.

Funding from the government through programs such as the NIH, BARDA, and DARPA is helping to develop the next generation of LoCs that could help combat the spread of infectious diseases and be used in the field of war, and also for quick genetic testing of the patient.

Lab-on-a-Chip Market Segment Insights

-

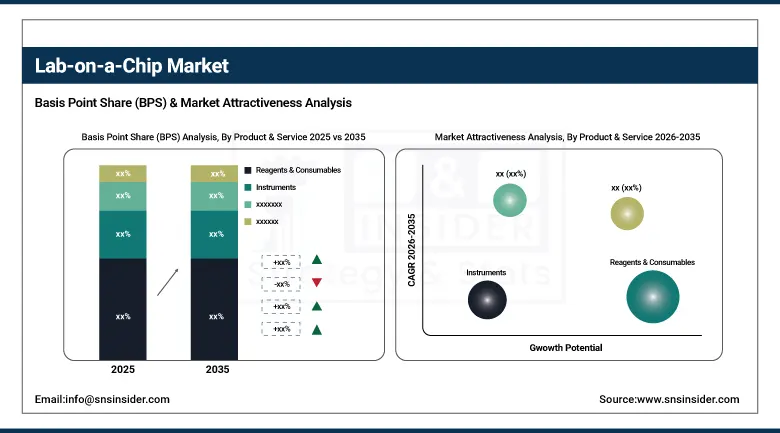

Based on Product & Service, Reagents & Consumables accounted for the largest market share (~38%) in 2025; Software & Services expected to be the fastest-growing segment (CAGR).

-

Based on Technology, Microfluidics Technology accounted for the largest market share (~54%) in 2025; Optical Technology expected to be the fastest-growing segment (CAGR).

-

Based on Application, Clinical Diagnostics accounted for the largest market share (~51%) in 2025; Drug Discovery & Development expected to be the fastest-growing segment (CAGR).

-

Based on End Use, Hospitals & Diagnostic Centers accounted for the largest market share (~47%) in 2025; Academic & Research Institutes expected to be the fastest-growing segment (CAGR).

By Product & Service, Reagents & Consumables segment dominates the Lab-on-a-Chip Market, Software & Services segment expected to grow fastest

The Reagents & Consumables category occupied the largest share of the Lab-on-a-Chip market, contributing roughly 38% to the overall market value in 2025. It is mainly due to the nature of the demand for these items, including microfluidic chips, assay cartridges, reagent kits, and sample preparation products, being consumable in nature and critical for the diagnostic or research processes of the healthcare industry, pharmaceutical companies, and academic organizations. In contrast to instruments that represent one-time expenses, reagents and consumables provide stable sources of income because of their recurrent need. The emergence of innovative uses for LoC assays in the diagnosis of infectious diseases, cancer, and metabolic conditions will further increase the potential market size.

The Software & Services category is projected to exhibit the highest growth rate during the forecast period. The growing complexity of LoC systems, along with increasing digitization trends, is expected to fuel the demand for software products that optimize the functionality of the devices, support AI-powered analysis of diagnostic results, and enable connection with hospital databases or EHRs. Such tools are essential for maximizing the value proposition offered by LoC platforms to hospitals, academic institutions, and other organizations implementing these systems.

By Technology, Microfluidics Technology segment dominates the Lab-on-a-Chip Market, Optical Technology segment expected to grow fastest

The Microfluidics Technology segment held the largest market share in the Lab-on-a-Chip industry in 2025 and accounted for about 54% of total revenue. Microfluidics serves as the backbone enabling technology that provides for the manipulation of small volumes of liquid ranging from nanoliter to picoliter levels to be utilized for various diagnostic, biochemical analysis, and pharmaceutical screening processes. This technology enables several benefits such as the use of less reagents, shorter process time, high-throughput and capability of performing multiple assays in one single chip. Such benefits are what has made this technology the leader in clinical, pharmaceutical and research LoCs.

Optical technology is estimated to grow at the highest CAGR during the period of 2026 to 2035. The need for more advanced techniques that ensure sensitive and non-invasive detections through real-time monitoring continues to increase. These optical techniques include the fluorescence technique, absorbance technique, and surface plasmon resonance, among others. They continue to be embedded into microfluidic chip technology to improve biomarker detections in point-of-care settings, life science researches, and environmental testing.

By Application, Clinical Diagnostics segment dominates the Lab-on-a-Chip Market, Drug Discovery & Development segment expected to grow fastest

In 2025, Clinical Diagnostics was the largest end-use application in terms of market revenue share, accounting for about 51%. This trend can be attributed to the rapidly rising demand for rapid, accurate, and accessible testing for infectious diseases, chronic conditions, and oncology biomarkers. In fact, Lab-on-a-chip technology can provide quick diagnostic results using small samples and thus is well-suited for use within hospitals' emergency rooms, clinics, and other medical environments that require quick decisions for patient treatment. Moreover, the lessons learned from the COVID-19 pandemic, such as the need to scale up decentralization efforts to ensure adequate diagnostic capacity, have strengthened institutional commitment to Lab-on-a-Chip technology-based clinical diagnostics.

It is expected that Drug Discovery & Development will have the fastest growth rate in revenue in 2026-2035. Increasing pressure on pharmaceutical and biotechnology firms to streamline and reduce their R&D expenses is evident, and it seems that LoC may serve as a helpful solution to this problem. Since LoC technology is better than existing in vitro techniques in simulating physiological processes in humans, it will make a great tool for drug discovery – screening compounds, assessing toxicity and validating targets.

By End Use, Hospitals & Diagnostic Centers segment dominates the Lab-on-a-Chip Market, Academic & Research Institutes segment expected to grow fastest

The segment of Hospitals & Diagnostic Centers held a substantial 47% share in the revenue generation of the LoC market during 2025. The need for fast and precise POCT/clinical lab analysis with low operational costs is driven by the vast number of patients that undergo tests in hospitals and diagnostic centers. It is possible to conduct different types of LoC tests (pathogen detection panel, metabolomics, and genomics), which are essential for the diagnosis and treatment of patients.

The most remarkable growth rate will be observed in the segment of Academic & Research Institutes between 2026 and 2035 due to the increasing interest of the global community in biomedical research and the development of innovative diagnostic tools based on microfluidics, organ-on-a-chip technologies, and LoC instruments. Scientific research is being conducted not only on the applications of LoC technologies in genomics and proteomics but in environmental biosensors as well. Grants and collaboration projects funded by governmental organizations are responsible for the increased demand for LoCs in universities and other academic institutions around the world.

Lab-on-a-Chip Market Regional Insights

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

~82% |

|

Europe |

Germany |

~29% |

|

Asia Pacific |

China |

~44% |

|

Middle East & Africa |

UAE |

~32% |

|

Latin America |

Brazil |

~48% |

North America Lab-on-a-Chip Market Insights

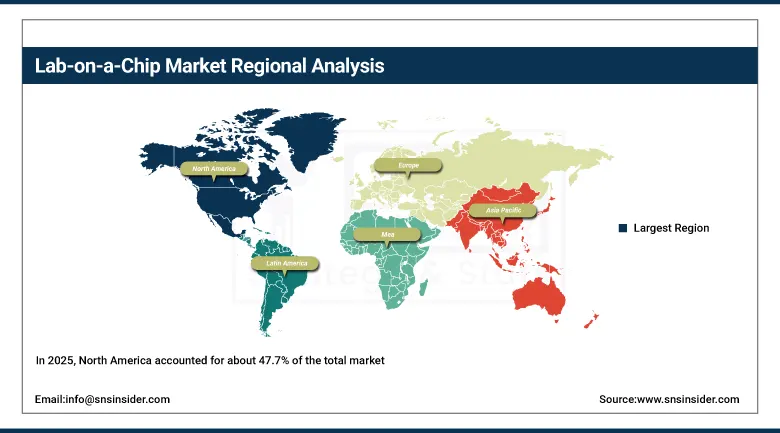

In 2025, North America accounted for about 47.7% of the total market size, making it the most dominant region in the Lab-on-a-Chip market segment. The key contributors to North America's dominance are the U.S.'s renowned healthcare facilities and investments made by the government in biomedical research, coupled with the presence of advanced LoC product manufacturers and clinical diagnostics companies. Universities like Massachusetts Institute of Technology, Broad Institute, and Johns Hopkins are involved in fundamental research of microfluidic chips that go on to become commercial products. North America benefits from favorable regulations for IVDs, availability of private capital for life science ventures, and increased awareness among clinicians regarding POC diagnostics until 2035.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Lab-on-a-Chip Market Insights

The Asia Pacific is estimated to exhibit the highest CAGR compared to other regional segments between 2026 and 2035, fueled by rapidly growing healthcare infrastructure, rising prevalence of chronic diseases, and growing government investment in biomedical research and diagnostics technologies. China, India, and Japan are some of the key growth countries, having considerable activity of academia and industry in microfluidics and biosensor research and development. Tsinghua University, Indian Institute of Technology (IIT) Bombay, and RIKEN are contributing fundamental innovation for the commercial success of LoC in the region. Large populations suffering from untreated ailments along with government health insurance and growing network of diagnostics laboratories make favorable structural trends for LoC.

Europe Lab-on-a-Chip Market Insights

Europe possessed a considerable market share in LoC technology in 2025, with Germany being the leading country market, owing to the high levels of development of the pharmaceutical sector, hospital sector, and academia in the region. The continuous support from the European Union in health-related research initiatives such as Horizon Europe, among others, ensures that several EU countries invest in microfluidics-based technology development in diagnostic tools. Apart from Germany, other key contributors to the region's market include the UK, France, and the Netherlands. These countries feature numerous LoC technology start-ups and IVD manufacturers offering LoC technology solutions for clinical diagnostics, food safety, and environmental monitoring, among other areas.

Middle East & Africa and Latin America Lab-on-a-Chip Market Insights

The Middle East & Africa region and Latin America are considered new growth markets for the Lab on a Chip industry with the factors that will drive adoption to be growth in public health initiatives, greater spending on hospitals' upgrading, and increased awareness of point of care diagnosis products. The UAE and Saudi Arabia can be considered key adopters of the technology in the Middle East & Africa region thanks to their vision for a digitized healthcare system and Life Sciences investments under their Vision 2030 initiatives. As for Latin America, Brazil will take the lead due to a larger population base, a strong pharmaceuticals industry, and the growing need for rapid diagnostic tests.

Growth Drivers: Revolutionizing healthcare with point-of-care diagnostics and miniaturized Lab-on-a-Chip devices

The key factor driving the growth of the Lab-on-a-Chip market is the profound effect that LoC point-of-care diagnostics have had on healthcare delivery systems around the world. Through the process of miniaturization whereby complex laboratory processes are condensed into a portable chip the size of a credit card, the Lab-on-a-Chip device makes it possible to perform clinical-grade diagnostic procedures away from the lab environment - in hospitals, rural medical facilities, pharmacies, or even at home. For poorer countries, which lack proper laboratory equipment, this can be a huge leap forward. The global pandemic has underlined the need for scalable and rapid testing outside laboratories, and governments around the world are making significant investments in point-of-care diagnostic devices.

Industry data consistently shows that LoC-based point-of-care tests deliver diagnostic turnaround times of minutes compared to hours or days for traditional laboratory assays, enabling earlier clinical intervention, improved patient outcomes, and more efficient use of healthcare resources. The FDA's pre-certification program for IVD devices and analogous regulatory frameworks in the EU and Asia Pacific are further streamlining market access for innovative LoC diagnostic solutions.

Restraints: High development complexity and device validation challenges limiting commercialization pace

A major constraint in the expansion of Lab-on-a-Chip applications is the complex nature of the engineering and regulation associated with bringing novel LoC devices to market as either diagnostics or research tools. The need for device consistency across production runs, clinical equivalence or superiority versus current diagnostics, and clearance through the IVD regulatory process can take considerable time and financial resources. Small companies and academic spinoffs, which make up a large portion of LoC developers, may not have the means to bring LoC technology from concept to product. Further, the implementation of LoC devices into the clinic poses technological hurdles related to integration into existing diagnostic platforms and electronic medical records systems.

Opportunities: Expanding opportunities driven by AI integration, organ-on-chip development, and diverse application growth

The intersection of Lab-on-a-Chip technology with artificial intelligence and machine learning capabilities offers the potential for one of the most promising areas of growth in the market until 2035. AI-enabled LoC systems that have the ability to independently analyze biological signals, detect disease biomarkers using multiparametric analysis, and provide clinically meaningful results in real-time are no longer just theoretical concepts but are already transitioning into commercially viable products. In drug discovery, the development of organ-on-chip platforms, which act as advanced human-relevant platforms for studying disease biology and assessing drug efficacy, is shaping a lucrative market niche with substantial interest from major pharmaceuticals and biotech firms keen on lowering failure rates during late-stage drug development. Outside healthcare, innovative uses of LoC technology in food safety testing, water quality assessment, crop pathogen screening, and biodefense for military purposes present additional market opportunities.

Recent Developments:

-

2025 (March): Thermo Fisher Scientific unveiled the Vulcan Automated Lab – an AI-driven electron microscopy lab featuring robotics to facilitate the analysis of semiconductors and expedite atomic-level TEM measurements. The device is built to optimize productivity, minimize expenses, and facilitate seamless integration of data collected in the lab and manufacturing facilities.

-

2025 (February): Siemens Healthineers increased its U.S. parts and components stock by about 30 percent by opening two additional logistics centers in New Jersey and California, providing robust support to the company's supply chain and ensuring timely delivery of diagnostic equipment and lab instruments components within North American healthcare organizations.

Lab-on-a-Chip Companies are:

-

Thermo Fisher Scientific

-

Danaher Corporation

-

Agilent Technologies

-

Siemens Healthineers

-

PerkinElmer

-

Fluidigm Corporation

-

Microsys

-

Becton Dickinson

-

Stanford Biotech

-

Life Technologies

-

InSphero

-

Dolomite Microfluidics

-

Blacktrace Holdings

Lab-on-a-Chip Market Report Scope

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 8.17 Billion |

| Market Size by 2035 | USD 20.62 Billion |

| CAGR | CAGR of 9.71% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product & Service (Reagents & Consumables, Instruments, Software & Services) • By Technology (Microfluidics Technology, Optical Technology, Electrochemical Technology, Others) • By Application (Clinical Diagnostics, Drug Discovery & Development, Others) • By End Use (Hospitals & Diagnostic Centers, Academic & Research Institutes, Pharmaceutical & Biotechnology Companies, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Abbott Laboratories, Thermo Fisher Scientific, Danaher Corporation, Agilent Technologies, Siemens Healthineers, PerkinElmer, Bio-Rad Laboratories, Fluidigm Corporation, Microsys, Becton Dickinson, Stanford Biotech, Life Technologies, InSphero , Dolomite Microfluidics, Blacktrace Holdings. |

Frequently Asked Questions

The Lab-on-a-Chip Market is expected to grow at a CAGR of 9.71% from 2026 to 2035.

North America dominated the Lab-on-a-Chip Market in 2025, holding approximately 47.7% of global market share, led by the United States.

The Clinical Diagnostics segment dominated the Lab-on-a-Chip Market in 2025, with approximately 51% revenue share.

The Microfluidics Technology segment dominated the Lab-on-a-Chip Market in 2025, accounting for approximately 54% of total market revenue.

The increasing demand for point-of-care diagnostics, rising prevalence of chronic and infectious diseases, growing personalized medicine adoption, and integration of AI and IoT into Lab-on-a-Chip platforms.

The Lab-on-a-Chip Market was valued at USD 8.17 billion in 2025.

Get in Touch