Language Service Market Report Scope & Overview

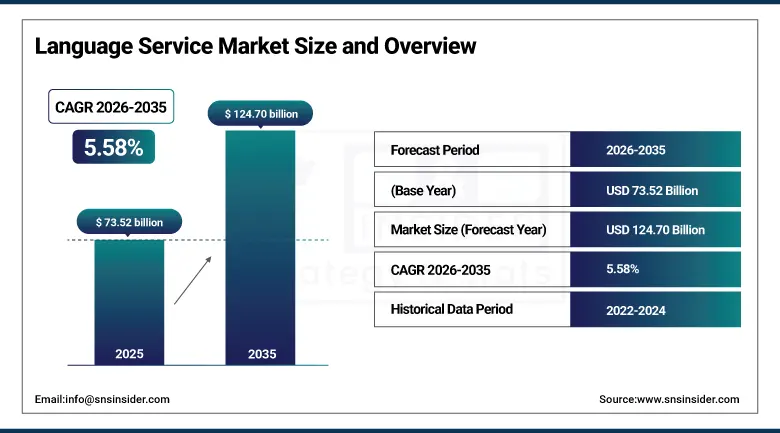

The Language Service Market was valued at USD 73.52 billion in 2025 and is expected to reach USD 124.70 billion by 2035, growing at a CAGR of 5.58% from 2026–2035.

The global language service market is experiencing sustained expansion as the intersection of globalisation, digital transformation, and artificial intelligence is fundamentally reshaping how organisations communicate across linguistic boundaries. The market encompasses a broad spectrum of professional language services including translation, interpretation, localisation, transcription, subtitling, dubbing, and machine translation post-editing, all of which are being transformed by the progressive integration of AI-powered translation engines, neural machine translation platforms, and large language model technology that is simultaneously increasing productivity, reducing per-word costs, and expanding the quality ceiling of automated language conversion across an ever-growing range of language pairs and content categories. The expansion of cross-border e-commerce, the proliferation of multilingual digital content requirements across streaming entertainment, enterprise software, and public-facing government digital services, and the growing regulatory requirement for translated medical, legal, and financial documentation across healthcare systems, court jurisdictions, and financial services regulators are collectively generating a structural demand expansion that transcends the economic cycles which historically drove translation volumes in line with international trade growth. AI-powered translation technology’s extraordinary productivity improvements are simultaneously expanding the addressable market by enabling language service providers to take on lower-value, higher-volume translation tasks that were previously uneconomical at human-only productivity rates, while freeing human linguists to focus on higher-value creative, cultural adaptation, and quality assurance tasks where the nuanced judgement and cultural intelligence of trained translators remains essential for achieving the communication quality that brand reputation and legal precision requirements demand.

The expanding deployment of real-time AI interpretation platforms across international business video conferencing, multilingual customer service operations, and government immigration and healthcare interpretation services is creating a new market segment that operates on fundamentally different economics from traditional consecutive and simultaneous interpretation services, potentially reaching the vast population of organisations that previously could not afford to fund professional interpretation for routine multilingual interactions and which have historically relied on informal bilingual employee assistance that delivers inconsistent quality and creates liability exposure.

Market Size and Forecast

-

Market Size In 2026E: USD 77.62 Billion

-

Market Size By 2035: USD 124.70 Billion

-

CAGR: 5.58% From 2026 To 2035

-

Fastest Growing Region: Asia Pacific

-

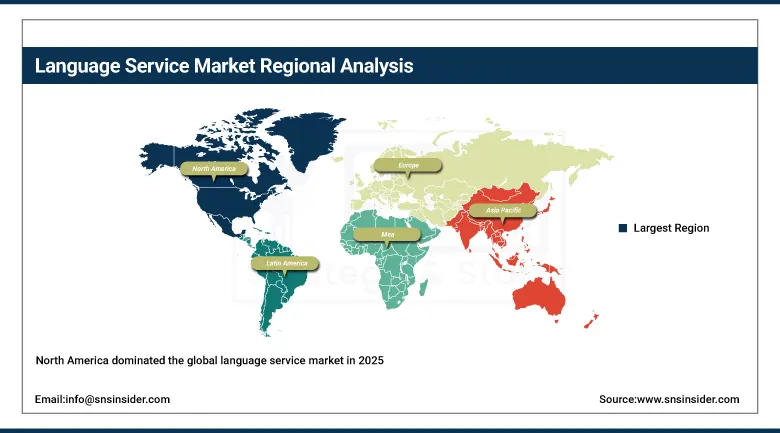

Largest Region: North America

To Get more information on Language Service Market - Request Free Sample Report

Language Service Market Trends

-

Accelerating adoption of AI-assisted translation and machine translation post-editing workflows across enterprise language service buyers that are demanding faster turnaround times, lower per-word costs, and consistent quality across large-volume multilingual content programmes that human-only translation workflows cannot economically support at the scale that digital content proliferation across websites, applications, marketing assets, and regulatory documentation is generating.

-

Growing importance of video localisation services including subtitling, dubbing, and audio description driven by the extraordinary global expansion of streaming entertainment platforms whose content libraries are being localised across 20 to 40 languages to serve subscriber bases across Asia Pacific, Latin America, and the Middle East and Africa whose linguistic diversity makes multilingual localisation a commercial requirement for subscriber acquisition and retention.

-

Rising enterprise demand for language service platform integration with content management systems, product information management systems, and customer relationship management platforms that create automated multilingual content workflows where source content changes trigger translation process initiation without manual intervention, dramatically reducing translation process cycle times and administrative overhead for organisations managing continuously updated multilingual digital asset libraries.

-

Growing specialisation of language service providers around regulated industry verticals including clinical trial documentation translation, medical device regulatory submission localisation, legal discovery translation, and financial prospectus multilingual production where domain expertise, regulatory compliance, certified translator qualification, and quality assurance process rigour create defensible competitive differentiation that price-based competition from technology-only translation platforms cannot readily overcome.

-

Expanding market for real-time interpretation services enabled by AI-powered consecutive interpretation platforms, remote simultaneous interpretation technology, and over-the-phone interpretation services that are making professional language access economically and logistically feasible for healthcare providers, legal proceedings, government service delivery, and enterprise multinational communication contexts that previously relied on in-person interpreter arrangements whose cost and scheduling complexity limited their practical accessibility.

U.S. Language Service Market Outlook

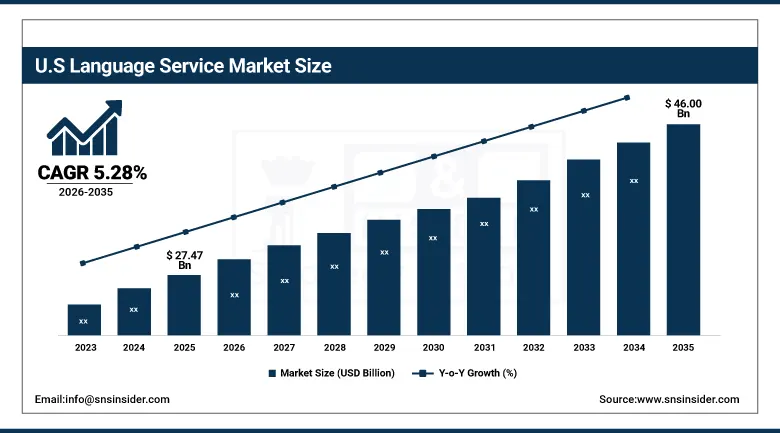

The U.S. language service market was valued at USD 27.47 billion in 2025 and is expected to reach USD 46.00 billion by 2035, growing at a CAGR of 5.28% from 2026–2035, driven by the world’s most linguistically diverse immigrant population generating enormous demand for healthcare interpretation, legal translation, and government document localisation, the global entertainment industry’s largest content production base requiring comprehensive multilingual localisation for international distribution, and the country’s leading position in enterprise software development whose products require comprehensive localisation programmes to serve their international customer bases.

The U.S. federal government’s language access requirements across agencies including the Department of Health and Human Services, the Department of Justice, and immigration courts are creating substantial and consistently renewing language service procurement volumes for specialised government language service contractors whose security clearance requirements, certified translator qualification verification, and federal procurement compliance capabilities create meaningful barriers to entry that sustain the commercial sustainability of the specialised government language service market segment.

Language Service Market Segment Analysis

-

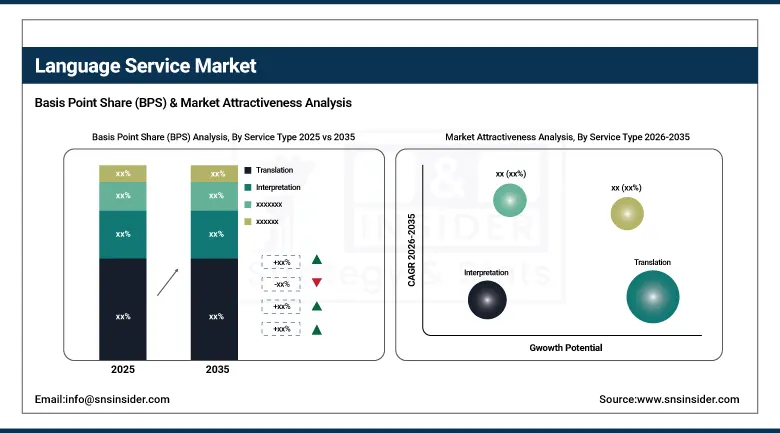

By Service Type, Translation dominated the language service market with the largest share in 2025, reflecting the foundational and universally applicable nature of document translation across every industry vertical and geographic market that requires written multilingual communication; localisation is the fastest-growing service type at a CAGR of approximately 7.20% through 2035, driven by the globalisation of software products, mobile applications, e-commerce platforms, and digital content that requires comprehensive cultural and functional adaptation beyond literal language conversion.

-

By Deployment Mode, Cloud-based solutions dominated the language service market with the largest share in 2025, owing to their scalability, accessibility across geographically distributed translation teams, and seamless integration capability with enterprise content management platforms; hybrid deployment is the fastest-growing mode driven by enterprise requirements for data sovereignty, compliance with data residency regulations, and the security requirements of regulated industry clients whose sensitive document translation cannot be processed through purely cloud-hosted language service platforms.

-

By Enterprise Size, Large enterprises held the dominant share in 2025, reflecting their greater multilingual content volume, international operations requiring systematic translation programmes, and the budget capacity to deploy comprehensive enterprise language service management platforms; SMEs are the fastest-growing enterprise size segment driven by the democratisation of AI-powered translation tools and cloud language service platforms whose consumption pricing makes professional multilingual content accessible to organisations that previously could not economically sustain comprehensive translation programmes.

-

By End Use, Healthcare led the language service market with the largest share in 2025, driven by the life-critical importance of accurate medical communication, the legal requirements for patient language access across healthcare systems, and the regulatory translation requirements of drug approvals, medical device submissions, and clinical trial documentation; media & entertainment is the fastest-growing end use driven by the global streaming content explosion requiring comprehensive multilingual subtitling, dubbing, and localisation across an expanding global subscriber base.

Translation Dominates Service Type, Localisation Grows Fastest

Translation retained the dominant service type position in the language service market in 2025, anchored by the universal requirement for written document conversion across languages that spans every industry vertical from healthcare patient consent forms and medical records through legal contracts and court documents to technical manuals, financial reports, marketing content, and software user interfaces. The translation service category’s commercial resilience derives from the non-discretionary nature of regulatory and legal translation requirements that create demand floors independent of economic conditions, as pharmaceutical drug approval submissions, court proceedings, immigration applications, and medical device regulatory filings require certified translation regardless of budget pressure cycles that affect discretionary marketing and commercial translation volumes.

Localisation is the fastest-growing service type at approximately 7.20% CAGR through 2035, propelled by the software and digital product industry’s requirement for comprehensive cultural adaptation of application interfaces, help documentation, in-app content, and user experience elements that extends well beyond translation into the technical, cultural, and functional customisation that makes digital products feel native to each target market rather than visibly adapted from a foreign original.

Healthcare Leads End Use, Media & Entertainment Grows Fastest

Healthcare retained the dominant end use position in the language service market in 2025, reflecting the combination of legally mandated patient language access requirements, regulatory translation demands across drug and medical device approvals, and the life-critical accuracy standards that medical communication requires creating the most demanding and value-intensive translation commissioning environment of any industry vertical.

Media and entertainment are the fastest-growing end use driven by the unprecedented expansion of global streaming content consumption that is making multilingual video localisation a commercial growth imperative for platforms including Netflix, Amazon Prime Video, Disney+, and their regional counterparts whose subscriber acquisition and retention across linguistically diverse global markets depends directly on the quality and breadth of their localised content libraries.

Regional Analysis

|

Region |

Major Country |

Share Within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

61.7% |

|

Middle East & Africa |

Saudi Arabia |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America Language Service Market Insights

North America dominated the global language service market in 2025 with the United States accounting for approximately 87.4% of North American revenues, driven by the world’s largest enterprise software localisation market, the global entertainment industry’s primary content production base requiring international distribution localisation, the most linguistically diverse national population generating healthcare and government interpretation demand, and the highest concentration of headquartered multinational corporations whose global operations require systematic multilingual communication programmes. Canada contributes approximately 12.6% of North American revenues through its official bilingual French and English federal government language service requirements that sustain a large domestic translation sector, alongside the international business operations of major Canadian financial institutions, resource companies, and technology firms that require multilingual content and regulatory documentation programmes.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Language Service Market Insights

Europe is the world’s most linguistically complex major economic region, where the European Union’s 24 official languages, the regulatory requirement for all EU legislation and official documentation to be published in all official languages, and the single market’s commercial imperative for cross-border communication across national language boundaries collectively create the most institutionally structured language service demand environment globally. Germany accounts for approximately 22.3% of European language service revenues as the region’s largest national market, with a major domestic manufacturing and export economy generating large technical documentation translation volumes, the world’s largest domestic language services company base, and a B2B enterprise translation market characterised by high technical precision requirements and quality standards that support premium pricing for specialist certified translation services. The European language service market is being transformed by the EU AI Act’s requirements for multilingual AI system documentation and the GDPR’s language access provisions that are creating new regulatory translation demand streams alongside the established commercial and government translation sectors.

Asia Pacific Language Service Market Insights

Asia Pacific is the fastest-growing regional language service market, driven by the extraordinary linguistic complexity of a region spanning dozens of major national and hundreds of regional languages whose economic integration through ASEAN, RCEP, and bilateral trade agreements is generating growing cross-border multilingual business communication demand, the global streaming entertainment market’s expanding investment in Asian-language content requiring both domestic and international localisation, and the technology sectors of China, Japan, South Korea, and India whose global software and hardware product launches require comprehensive multilingual localisation programmes. China accounts for approximately 61.7% of Asia Pacific language service revenues as the dominant national market, combining the world’s largest domestic Chinese language translation requirement for international content localisation with a growing outbound translation demand as Chinese companies expand globally and require multilingual marketing, legal, and technical communication programmes for their international markets.

Latin America and MEA Language Service Market Insights

Latin America and the Middle East and Africa are growing language service markets where expanding digital economy participation, growing cross-border trade, and rising investment in healthcare and government digital services are creating commercially meaningful translation and localisation demand beyond the major developed market centres that have historically dominated global language service procurement. Brazil accounts for approximately 44.2% of Latin American language service revenues through its status as the region’s largest economy requiring Portuguese-English and Portuguese-Spanish translation services across its internationally active financial services, agricultural commodity export, and technology sectors, and a growing domestic streaming content market requiring localisation into and from Brazilian Portuguese. Saudi Arabia leads Middle East and Africa language service revenues at approximately 38.4% of the regional total, driven by Vision 2030’s extensive government digital transformation and international investment attraction programmes requiring Arabic-English translation and multilingual communication services, and the Kingdom’s international business community whose operational language requirements span Arabic, English, and multiple South Asian languages serving the country’s diverse expatriate workforce.

Market Dynamics

Growth Drivers: Global digital content proliferation creating multilingual communication requirements across enterprise, government and media channels, AI-powered translation tools expanding market accessibility and productivity, and regulated industry translation mandates creating non-discretionary demand floors

The primary structural growth drivers for the language service market are the extraordinary expansion of digital content production across enterprise, government, and entertainment sectors that is creating multilingual communication requirements at a scale and velocity that manual translation workflows cannot efficiently serve without AI productivity augmentation, combined with the progressive globalisation of commerce, regulation, and digital services that is generating new translation demand across previously domestically focused sectors and geographies. The healthcare sector’s growing compliance requirements for patient language access across diverse national healthcare systems, the pharmaceutical industry’s global regulatory submission translation requirements, and the financial services industry’s cross-border disclosure and client communication regulatory obligations collectively create a large and consistently growing non-discretionary translation demand base that sustains language service market revenues through economic cycles that compress discretionary commercial translation volumes.

Restraints: AI-driven unit price compression creating revenue per word margin pressure, quality consistency challenges in machine translation for specialised technical content, and talent shortage in specialised language pairs and technical domains

A significant restraint on the language service market is the progressive compression of per-word translation pricing that AI-powered machine translation and neural translation engines are creating, as clients increasingly expect language service providers to pass on the productivity benefits of AI-assisted translation workflows in the form of lower unit prices that maintain overall budget levels while enabling higher translation volumes, creating margin pressure on translation service providers whose revenue per word is declining faster than their cost per word in some commodity content translation segments.

Opportunities: Real-time AI interpretation services expanding addressable market, language service platform API integration with enterprise software ecosystems creating embedded demand, and emerging market language pair development creating first-mover advantage opportunities

The real-time AI interpretation opportunity represents the most significant addressable market expansion in the language service industry, as AI-powered simultaneous interpretation platforms whose cost structure is a fraction of traditional human interpreter arrangements are creating the first commercially viable pathway to professional-quality language access across the mass of routine multilingual interactions in healthcare, legal, and government service settings that have historically been served by informal bilingual staff rather than professional interpreters whose cost made systematic deployment across routine interaction volumes economically impractical.

Recent Developments

-

2025: TransPerfect expanded its AI-assisted translation platform capabilities with new large language model integration that enables enterprise clients to deploy customised neural machine translation engines trained on their proprietary translation memories and terminology databases, improving AI translation quality for technical and branded content beyond the performance achievable with generic public translation engines.

-

2025: LanguageLine Solutions expanded its over-the-phone and video remote interpretation service network with new AI-assisted interpreter support tools that provide real-time terminology reference, speaker context notes, and post-call quality monitoring for healthcare and legal interpretation sessions, improving interpreter performance consistency across high-volume multilingual service environments.

-

2025: RWS Holdings integrated generative AI content generation and multilingual adaptation capabilities into its life sciences regulatory documentation translation platform, enabling pharmaceutical clients to accelerate the multilingual regulatory submission preparation process through AI-assisted first draft generation that expert translators review and certify rather than producing from blank page.

-

2025: Welocalize launched expanded AI-powered video localisation services combining automated speech recognition, machine translation, and AI voice synthesis for subtitle and dubbed audio track production at significantly reduced cost and turnaround time compared to traditional human-only video localisation workflows, targeting the streaming content platform sector’s growing multilingual library expansion requirements.

-

2025: Acolad Group completed a strategic acquisition expanding its technology platform capabilities for enterprise translation management, adding automated workflow orchestration, vendor management, and quality monitoring tools that enable large enterprise clients to manage complex multilingual content programmes with reduced administrative overhead and improved translation quality consistency monitoring.

Language Service Market Key Players

-

TransPerfect

-

LanguageLine Solutions

-

RWS Holdings plc

-

Welocalize

-

Acolad Group

-

STAR Group

-

Hogarth Worldwide

-

Centific

-

LanguageWire

-

CyraCom International

-

Propio Language Services

-

AMN Language Services

-

Argos Multilingual

-

ZOO Digital

-

United Language Group

-

Pixelogic Media

-

Dubbing Brothers

-

LOGOS Group

-

TAKARA

-

Equiti

Language Service Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 73.52 Billion |

| Market Size by 2035 | USD 124.70 Billion |

| CAGR | CAGR of 5.58% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Service Type (Translation, Interpretation, Localization, Transcription, Subtitling & Dubbing, Others) • By Deployment Mode (Cloud-Based, On-Premises, Hybrid) • By Enterprise Size (Large Enterprises, SMEs) • By End Use (Healthcare, Legal, BFSI, IT & Telecom, Government, Media & Entertainment, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | TransPerfect, LanguageLine Solutions, RWS Holdings plc, Welocalize, Acolad Group, STAR Group, Hogarth Worldwide, Centific, LanguageWire, CyraCom International, Propio Language Services, AMN Language Services, Argos Multilingual, ZOO Digital, United Language Group, Pixelogic Media, Dubbing Brothers, LOGOS Group. TAKARA, Equiti |

Frequently Asked Questions

The language service market is expected to grow at a CAGR of 5.58% from 2026 to 2035.

The language service market was valued at USD 73.52 billion in 2025.

Translation dominated with the largest revenue share in 2025.

North America dominated the language service market in 2025, with the United States as the leading national market within the region.

The extraordinary expansion of global digital content production creating multilingual communication requirements across enterprise, government, and media channels, combined with AI-powered translation technology expanding market accessibility and productivity while regulated industry translation mandates across healthcare,

Get in Touch