Large Language Model Powered Tools Market Report Scope & Overview:

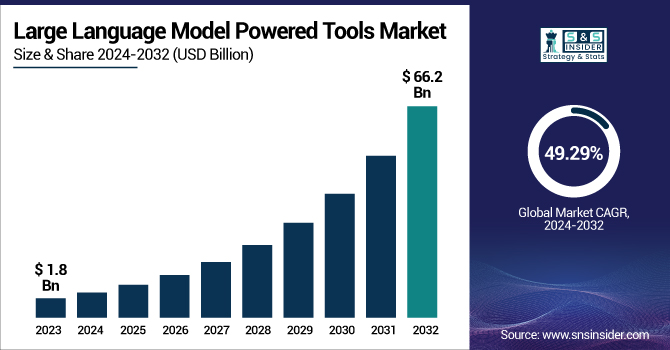

The Large Language Model Powered Tools Market was valued at USD 1.8 Billion in 2023 and is expected to reach USD 66.2 Billion by 2032, growing at a CAGR of 49.29% from 2024-2032.

To Get more information on Large Language Model Powered Tools Market - Request Free Sample Report

The Large Language Model Powered Tools Market is witnessing increased adoption of AI-driven text generation, summarization, and conversational AI across various industries. Enterprises, including SMEs, are rapidly integrating these tools for customer engagement and content creation. Enhanced integration capabilities with enterprise software, such as CRM and ERP systems, are driving seamless automation and operational efficiency. These tools are significantly transforming business automation and decision-making by optimizing workflows, providing data-driven insights, and minimizing manual tasks, ultimately improving productivity and strategic planning.

Market Dynamics

Drivers

-

Businesses are increasingly adopting LLM-powered tools to enhance workflow efficiency, automate tasks, and improve customer engagement.

The growth of AI-powered tools for automating repetitive tasks, augmenting workflow efficiency, and enriching customer engagement is a prime factor driving the Large Language Model Powered Tools Market. Businesses are utilizing LLM tools for generating content, code generation, customer support, and data analysis, helping to minimize human effort and operational costs. Demand in the market is fueled further as LLM tools become more integrated with enterprise software such as CRM and ERP systems. With the identity of multiple organizations digitally transforming themselves, the need for AI-powered automation is only going to grow bigger, leading to advancements in LLM features like multi-lingual handling, business-centric fine-tuning and real-time conversational AI solutions.

Restraints

-

The deployment of LLM tools demands significant computing power, cloud resources, and high operational costs, limiting accessibility for SMEs.

One of the biggest challenges with deploying LLM-powered tools is getting the computational power and cloud resources to maintain them along with the AI infrastructure. Running and training large language models require high-end GPUs, a large amount of storage, and a continuous power supply, which will increase such operational costs. Moreover, server systems have to be sophisticated for processing and inference in real-time, which makes it an unrealistic option for all but the costliest companies. The growing complexity of AI models contributes to energy consumption and carbon footprint, hampering their wide adoption. The accessibility for smaller organizations is limited due to these cost and infrastructure barriers, thus, a constant evolution in efficient AI processing technologies is required.

Opportunity

-

The development of industry-specific and customizable LLMs enables businesses to tailor AI models for specialized applications, driving market growth.

This emergence of domain-specific and easily customizable LLMs expands a huge growth opportunity in the market. The demand for contextualized, more accurate, language-related processing systems is pushing businesses in sectors like healthcare, finance, and legal services to look for tools that best fit their specific functional and operational content. By fine-tuning LLM with proprietary data, organizations can personalize and streamline its use with open-source LLM frameworks and API-driven solutions. Furthermore, as edge AI and on-device processing increase, the need for a cloud becomes less necessary, and AI tools become more widely used and available. We believe this transition towards tailored, domain-specific AI models will fuel further innovation and growth of LLMs into numerous distinct use cases.

Challenges

-

The rising use of LLM tools raises concerns about AI bias, misinformation, and data privacy, leading to stricter regulations and compliance challenges.

However, the pervasive adoption of tools powered by these technologies presents their own set of ethical and regulatory challenges in terms of biased outcomes from generative AI, misinformation, and data privacy. With government and regulatory entities intensifying policies on AI governance, businesses will need to ensure compliance in terms of transparency, fairness and responsible AI practices. The issues of data privacy and the potential for these LLM tools to be used to create misleading or malicious content are still serious problems. Therefore, organizations need to spend on AI ethics frameworks, bias mitigation strategies, and compliance mechanisms to safeguard trust and eliminate legal risks. How market players navigate these ethical issues, while still delivering innovation without getting into ethical trouble is going to be a challenge.

Segmentation Analysis

By Type

The general-purpose tool segment dominated the market and accounted for significant revenue share in 2023. That broadness in function – multi-talented chatbots, versatile content generators – and adaptability to other use cases – makes these products attractive for organizations at any scale. This wide-scale usage is enabled by their multi-tasking capability from customer support to automated writing.

The task-specific tools segment is expected to register the fastest CAGR during the forecast period as the growing need for domain-specific tools to solve specific industry challenges. Such tools are meant to perform one or specified task with the highest accuracy and efficiency possible, and thus, they have become increasingly useful in healthcare, finance, and legal services. The adoption of AI-enabled software or task-oriented tools that are tailored or customized for the specific needs of businesses is on the rise because businesses understand that a well-designed application can provide measurable productivity and more accurate or better results.

By Deployment

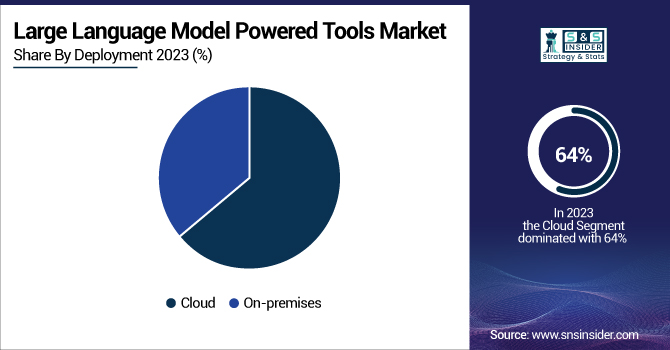

The cloud segment dominated the market in 2023 and accounted for 64% of revenue share, due to their superior scalability and flexibility, which leads many organizations to choose this option. These tools allow businesses to use and implement LLMs without any heavy upfront investment on infrastructure and help bring down costs and operational overhead. Quick cloud updates and the extraordinary scalability of cloud-based solutions have enabled rapid innovation and standing up of new solutions as market demands have changed.

The on-premises segment is expected to register the fastest CAGR over the forecast period. With the growing need for stricter data security and compliance, organizations are leaning toward in-house LLM deployments thereby driving the on premises segment. It is particularly prominent in data-sensitive industries, such as finance, healthcare, and government, where regulations are restrictive.

By Application

In 2023, the content generation segment dominated the market and accounted for the maximum share of the market. The tools help organizations create high-quality, human-like text in a shorter time with minimum use of resources. Content generation tools have become essential for virtually every industry, with their wide-ranging applications from automated blog writing to social media posts. The consistency and variability of different tones and styles they can carry has only accelerated adoption.

Personalization segment is anticipated to expand significantly during the forecast period, as companies have started looking to provide personalized experience to users. Tools that harness large language models allow businesses to provide extremely personalized content, suggestions, and engagement centered around how the user behaves and what they prefer. The increasing demands for a personalized touch in e-commerce, digital marketing, and customer service is driving this growth.

Regional Landscape

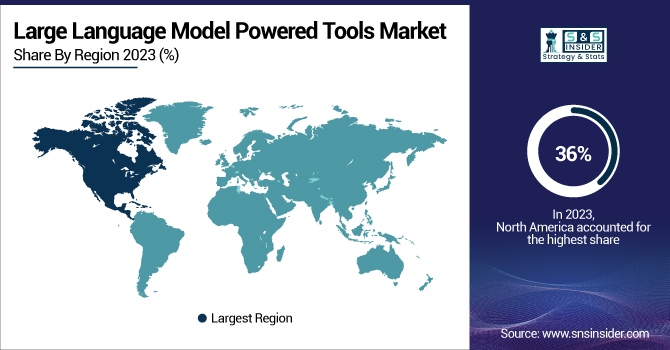

In 2023, North America dominated the market and accounted for 36% of revenue share, owing to the strong technological framework and high adoption rate of AI across various industry verticals in the region. Major AI hubs like Silicon Valley are stimulating innovation which will assist market growth.

Asia Pacific is expected to register the fastest CAGR during the forecast period. due to the shift towards digital transformation in countries such as China, India, and Japan. APAC businesses are moving towards LLMs for better customer experiences, enhancing operational automation, and industry-driven innovation in areas like e-commerce & telecommunications.

Get Customized Report as per Your Business Requirement - Enquiry Now

Key players

The major key players along with their products are

-

Google LLC – Gemini

-

Microsoft Corporation – Azure OpenAI Service

-

OpenAI – ChatGPT

-

Amazon Web Services (AWS) – Amazon Bedrock

-

IBM Corporation – Watsonx

-

Meta Platforms, Inc. – LLaMA

-

Anthropic – Claude AI

-

Cohere – Cohere Command R+

-

Hugging Face – Transformers Library

-

Salesforce, Inc. – Einstein GPT

-

Mistral AI – Mistral 7B

-

AI21 Labs – Jurassic-2

-

Stability AI – Stable LM

-

Baidu, Inc. – Ernie Bot

-

Alibaba Cloud – Tongyi Qianwen

Recent Developments

-

February 2024 – OpenAI: Released GPT-4.5, featuring a reduced hallucination rate and enhanced understanding across various topics.

-

March 2024 – Baidu: Announced an upgraded version of its AI model, Ernie, with improved reasoning and multimodal capabilities, allowing it to process diverse data formats.

-

March 2024 – Anthropic: Raised $3.5 billion in funding to advance AI systems, expand computational capacity, and enhance research into AI interpretability and alignment.

|

Report Attributes |

Details |

|

Market Size in 2023 |

USD 1.8 Billion |

|

Market Size by 2032 |

USD 66.2 Billion |

|

CAGR |

CAGR of 49.29% From 2024 to 2032 |

|

Base Year |

2023 |

|

Forecast Period |

2024-2032 |

|

Historical Data |

2020-2022 |

|

Report Scope & Coverage |

Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

|

Key Segments |

• By Type (General-Purpose Tools, Domain-Specific Tools, Task-Specific Tools) |

|

Regional Analysis/Coverage |

North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

|

Company Profiles |

Google LLC, Microsoft Corporation, OpenAI, Amazon Web Services (AWS), IBM Corporation, Meta Platforms, Inc., Anthropic, Cohere, Hugging Face, Salesforce, Inc., Mistral AI, AI21 Labs, Stability AI, Baidu, Inc., Alibaba Cloud |

Frequently Asked Questions

Ans- The rising use of LLM tools raises concerns about AI bias, misinformation, and data privacy, leading to stricter regulations and compliance challenges.

Ans- Businesses are increasingly adopting LLM-powered tools to enhance workflow efficiency, automate tasks, and improve customer engagement.

Ans- Asia-Pacific is expected to register the fastest CAGR during the forecast period.

Ans- The CAGR of the Large Language Model Powered Tools Market during the forecast period is 49.29% from 2024-2032.

Ans - The Large Language Model Powered Tools Market was valued at USD 1.8 Billion in 2023 and is expected to reach USD 66.2 Billion by 2032

Get in Touch