Laxatives Market Report Scope & Overview:

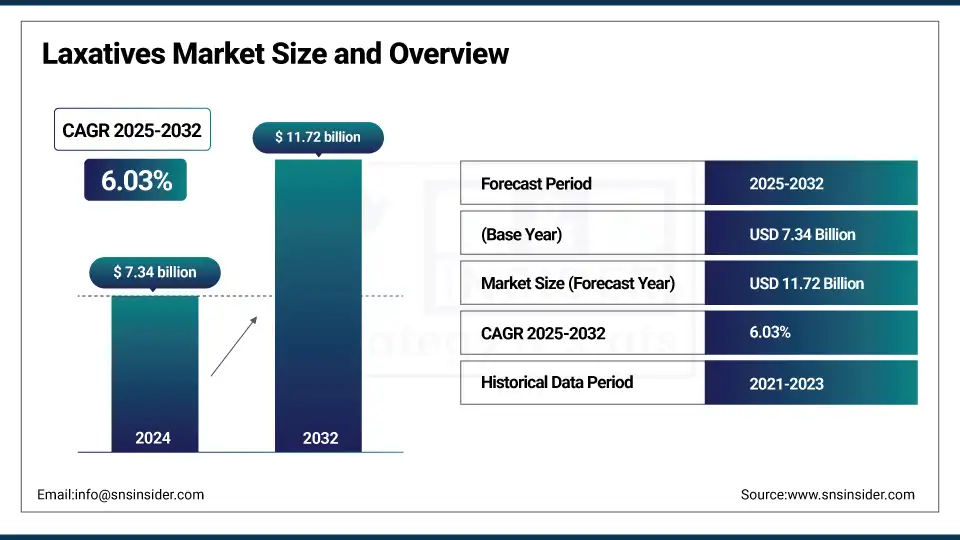

The laxatives market size was valued at USD 7.34 billion in 2024 and is expected to reach USD 11.72 billion by 2032, growing at a CAGR of 6.03% over 2025-2032.

The increasing incidence of chronic constipation, irritable bowel syndrome (IBS-C), overuse of laxatives in slimming routines, and the opioid-induced constipation cases (OIC) among geriatric population & sedentary lifestyle enthusiasts are some of the macro-economic factors responsible for fuelling demand for laxatives. Due to the Increasing occurrence of digestive disorders globally, demand for bulk-forming, stimulant, and natural-source laxatives is increasing rapidly, leading to surging sales in the global laxatives market, especially in the U.S., due to high OTC availability in regions. Besides, the increasing consumer awareness related to gut health, along with the rapid proliferation of products through online channels as well as pharmacies, are other prominent factors that are expected to pave the way for growth, impacting the laxatives market share.

To Get more information On Laxatives Market - Request Free Sample Report

Manufacturers of laxatives, including GlaxoSmithKline, Takeda, Bayer, and Sanofi, are focusing on developing advanced formulations with fewer side effects and improved palatability. Emerging regulatory favorability, including approval of chloride channel activators and microbiome-targeted solutions, will have a substantial impact on the demand aspect in the global laxatives market landscape. Moreover, increasing health care expenditure, improvement in drug delivery systems, and increased demand for personalized digestive care will propel the global laxatives market in the years to come.

As per the industry data, the laxatives market is witnessing a growing requirement in elderly care and post-operative recovery. Some of the other factors fueling the market include a well-established market for natural and plant-based laxatives and higher adoption of digital tools to manage GI health. Growing investments in R&D, especially in the U.S. laxatives market, also depict a promising outlook for therapeutic and OTC segments. The inclusion of coverage for chronic constipation treatments in reimbursement guidelines in several countries further inspires supply-side confidence, expanding the global laxatives market share.

In May 2024, Bayer showcased the development of a plant-based osmotic laxative with minimal side effects for IBS-C patients without causing addiction, showing innovations in natural-source product pipelines.

In February 2024, Takeda Pharmaceuticals extended its U.S. clinical trial program for next-gen laxatives that help satiate motility regulation along with microbiome support, an indication of increasing R&D focus and individualization in the laxatives market segment.

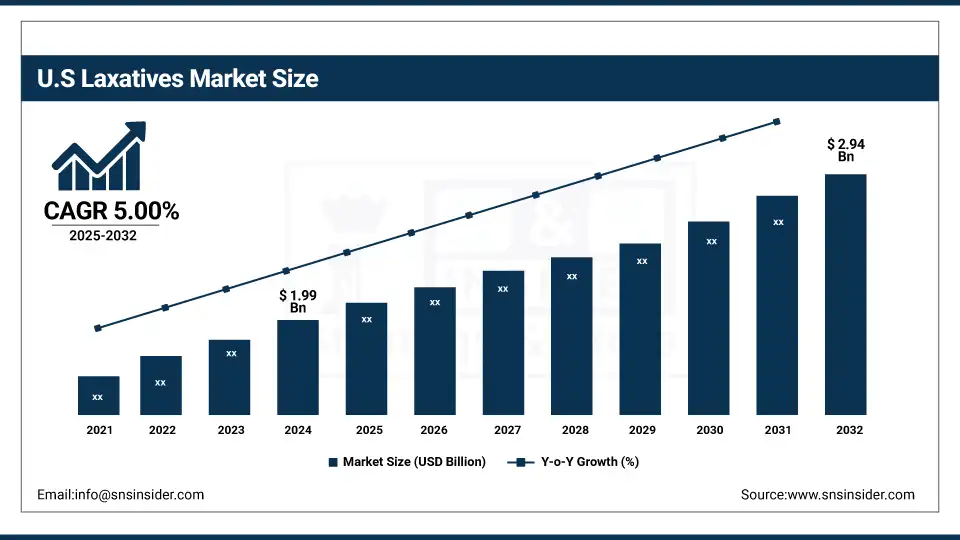

The U.S. laxatives market size was valued at USD 1.99 billion in 2024 and is expected to reach USD 2.94 billion by 2032, growing at a CAGR of 5.00% over 2025-2032. The U.S. drove the region, as extensive availability of OTC products and a high geriatric population suffering from various chronic bowel conditions boosted overall sales. The U.S. also leads in R&D spending, and has this status reinforced with a relatively friendly regulatory environment for new drug approvals. Canada is having decent growth due to increasing awareness and penetration of online pharmacies. In this region, the online pharmacies are one of the fastest-growing segments with increasing trust and convenience post the COVID-19 pandemic, in addition to being able to meet consumer needs digitally.

Market Dynamics:

Drivers:

-

Rising Incidences of Sedentary Lifestyles, Poor Dietary Habits, and a Growing Geriatric Population Globally

Approximately 20% of adults struggle with chronic constipation, driving the growing consumption of over-the-counter and prescription laxatives. Growth in the use of opioid-based pain management for cancer and orthopedic treatment has created an increase in opioid-induced constipation (OIC), which also contributes to demand. A growing number of initiatives by pharmaceutical companies for R&D; Innovative linaclotide-based therapies developed by collaborations such as AbbVie and Ironwood Pharmaceuticals, which recorded a 15% rise in clinical adoption YoY since 2022.

An increase in the demand for natural and fibre-based laxatives among consumers is also driving innovation in the range of products. In addition, various regulatory endorsements for unique chloride channel activators and guanylate cyclase-C agonists have increased market assurance. In the last three years, investment in clinical trials for dual-action laxatives (osmotic and motility effects) has doubled. Laxative sales grew 12% across e-commerce channels in 2023, and the uptake of laxative treatment through telehealth platforms and e-pharmacies has further added to global product availability.

Restraints:

-

Product Overuse, Side Effects, And Consumer Dependency, Which Deter Long-Term Adoption, Hinder the Market Expansion

Problems with safety have been raised, such as colon damage and electrolyte imbalances through overuse of stimulant laxatives. While the NIH report notes that 16% of patients on regular treatment with stimulant laxatives had GI adverse events, one possible explanation for tighter scrutiny by doctors is further supported. In some cases, regulatory bodies in countries such as Germany and Australia have reclassified OTC laxatives as prescription-only medication, making it impossible to market them commercially. In addition, low awareness levels across the emerging markets and limited accessibility to specialist care, entailing uptake of advanced laxative therapies, are restraining growth.

Chronic constipation treatments are even more limited inpatient access, as many insurance companies do not cover non-essential GI medications at all and place restrictions on reimbursement. Furthermore, there is less innovation in this space compared with other therapeutic areas; only a little over 1.5% of total GI-related research funding is allocated to R&D spending for constipation medications. There are also continued supply-side constraints, particularly with natural source laxatives, given that raw material procurement can be seasonally variable and this directly impacts consistent product availability. In addition to this, patient reluctance due to the social stigma attached to talking about bowel health still prevents individuals from seeking treatment, hindering the laxatives market.

Segmentation Analysis:

By Drug Type

Bulk-forming laxatives lead the drug type segment in 2024, accounting for 28.5% share of the global laxatives market. They are widely used agents (e.g., psyllium, methylcellulose) for chronic constipation because of their natural fiber-based formulation, good safety profile, and appropriateness for long-term use in elderly and pediatric populations. They are widely available OTC and can be combined into dietary regimens, providing durable access to the market.

However, chloride channel activators were the fastest growing segment of this market because this category of drugs exploited a new mechanism of action that promoted intestinal fluid secretion and so were quite useful in patients with IBS-C, as well as had been shown to be effective in OIC. This is due to their expanding utilization in prescription-based therapies and positive clinical results, which have driven demand for them in various developed healthcare markets.

By Indication

In 2024, the segment of chronic constipation accounted for the dominant share of the laxatives market portfolio, which is because a considerable portion of the aging population suffers from this condition, as well as individuals with sedentary lifestyles. In addition, increased consumption of processed food and reduced physical activity have also been major factors in its global distribution. The market for bulk-forming and osmotic laxatives has suffered a significant reduction in prices over time, but there is still high demand for these products to treat chronic constipation, based on the growing number of patients. This is in sharp contrast to OIC, the fastest-growing indication fueled by increasing global use of opioid-based medications morphine and related analgesics, for pain management, such as cancer treatment. The heightened awareness has created a significant need for more advanced prescription laxatives that target OIC, such as peripherally acting μ-opioid receptor antagonists (PAMORAs).

By Route of Administration

The oral segment of administration accounted for over 71.4% of the global market share in 2024 and was the leading route of administration of laxatives as well. Oral formulations (tablets, powders, capsules, liquids) are preferred due to ease of administration, widespread availability, and clinical applicability for acute as well as chronic use. The easy availability of OTC oral laxatives in retail and online pharmacies also encourages their recognition. The rectal route expanded most sharply, especially in the hospital and SND segments (for quick relief in acute or serious conditions). The rapid onset of action of rectal laxatives (enemas, suppositories) makes them ideal approaches for preoperative preparation and post-surgical bowel management, which has expanded their clinical use.

By Sales Channel

In 2024, retail pharmacies are the dominant phase of sale due to huge penetration and recommendation by pharmacists, along with a wide presence that offers easy access for consumers typically buying OTC products. Still, these outlets are leading in urban and semi-urban areas. However, the online pharmacy was identified as the most rapidly growing channel as a result of digital health uptake, home delivery convenience, subscription-based services for treating chronic constipation, and the increase in internet access. In the post-pandemic age, consumers are more addicted to buying personal care and wellness products online, laxatives being no exception. In addition, expanded product selection and price comparisons have enabled the channel to grow at a faster pace than the market.

By Availability

Based on availability, in 2024, over-the-counter (OTC) laxatives accounted for 62.8% market share, as they are mainly preferred by consumers for self-treatment and easy purchase without a prescription. Physician-prescribed stimulant laxatives, stool softeners, and fiber supplements are all available over the counter in most retail and online pharmacies. Even more important, though, was the Prescription (Rx) segment growth, which was the most rapid due in large part to an influx of advanced therapy options like PAMORAs and chloride channel activators that have proven their value for treating difficult GI conditions such as IBS-C and OIC. Both primary care and specialty GI tracks show overlapping growth areas, with more physicians recommending targeted therapies for patients not responding to OTC options, which drives the Rx track up.

Regional Analysis:

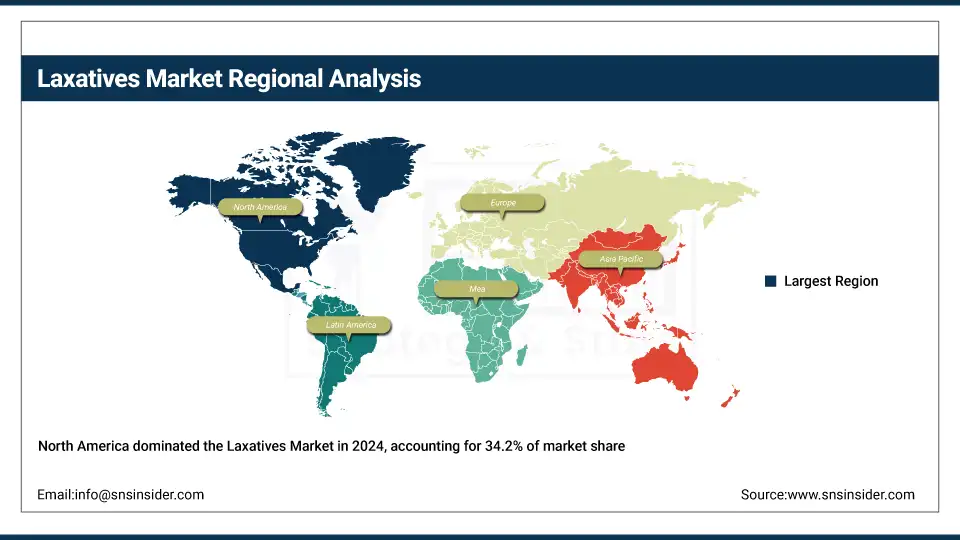

In 2024, North America led the laxatives market with over 34.2% share of the global revenue owing to a higher sedentary lifestyle, opioid-induced constipation (OIC) incidence, and an established pharmaceutical industry in this region.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific is the fastest-growing region and holds the potential to grow significantly as urbanization grows along with health awareness and dietary transition, leading to increased cases of chronic constipation. This region has about a 21.7% market share in 2024. China's upsurge in healthcare expenditure and expanding pool of patients with lifestyle-associated constipation. Increasing retail pharmacies and growing demand for herbal laxatives and combination laxatives have helped India to grow. Age-concentrated Japan, the most common OTC laxative market. With increasing investment in primary health care, ASEAN countries are emerging markets.

Key Players:

Notable players offering laxatives include AstraZeneca, Boehringer Ingelheim, Bayer AG, GlaxoSmithKline plc, Abbott Laboratories, Takeda Pharmaceutical Company, Braintree Laboratories, Purdue Pharma, Sucampo Pharmaceuticals, F. Hoffmann-La Roche Ltd., Mylan N.V., Teva Pharmaceutical Industries Ltd., Sanofi, Pfizer Inc., Novartis AG, Merck & Co., Inc., Johnson & Johnson Services, Inc., Dr. Reddy's Laboratories Ltd., Lupin Limited, and Aurobindo Pharma.

Recent Developments:

In June 2024, India-based Glenmark introduced LaxaGo, an over-the-counter PEG‑3350 osmotic laxative with balanced electrolytes and neutral taste, designed for gentle, non-stimulant constipation relief.

In December 2023, Lupin Life launched Softovac Liquifibre, a 100% herbal liquid laxative combining psyllium fiber with herbal actives such as Sonamukhi and Saunf, flavored with mango, targeting consumers seeking natural, non-habit-forming options.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 7.34 billion |

| Market Size by 2032 | USD 11.72 billion |

| CAGR | CAGR of 6.03% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Drug Type (Bulk-forming Laxatives, Stimulant Laxatives, Stool Softeners (Emollients), Lubricant Laxatives, Hyperosmotic Laxatives, Saline Laxatives, Chloride Channel Activators, and Others (herbal remedies, combination drugs, and emerging therapeutic classes)) • By Indication (Chronic Constipation, Irritable Bowel Syndrome with Constipation (IBS-C), Opioid-Induced Constipation (OIC), Acute Constipation, and Others (pregnancy-induced constipation, neurological constipation, and post-surgical constipation)) • By Route of Administration (Oral, Rectal, and Others (investigational or alternative routes)) • By Sales Channel (Retail Pharmacies, Hospital Pharmacies, Online Pharmacies, Elderly Care Centers, and Others (direct sales, drug wholesalers, and healthcare clinics)) • By Availability (Over-the-Counter (OTC), and Prescription (Rx)) |

| Regional Analysis/Coverage | North America (U.S., Canada), Europe (Germany, France, UK, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, Egypt, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America) |

| Company Profiles | AstraZeneca, Boehringer Ingelheim, Bayer AG, GlaxoSmithKline plc, Abbott Laboratories, Takeda Pharmaceutical Company, Braintree Laboratories, Purdue Pharma, Sucampo Pharmaceuticals, F. Hoffmann-La Roche Ltd., Mylan N.V., Teva Pharmaceutical Industries Ltd., Sanofi, Pfizer Inc., Novartis AG, Merck & Co., Inc., Johnson & Johnson Services, Inc., Dr. Reddy's Laboratories Ltd., Lupin Limited, and Aurobindo Pharma. |

Frequently Asked Questions

Innovations include microbiome-modulating laxatives, combination therapies, and personalized GI solutions.

The growing geriatric population suffers from reduced bowel motility and comorbidities, increasing laxative consumption.

There is a rising demand for gentle, fast-acting, and flavor-enhanced OTC laxatives. Consumers are increasingly preferring natural and bulk-forming options for routine use.

Key players include GlaxoSmithKline, Sanofi, Pfizer, Boehringer Ingelheim, Dr. Reddy’s, Takeda, and AstraZeneca.

Rising cases of chronic constipation, sedentary lifestyles, and increased use of opioid medications are major drivers.

Get in Touch