Leak Detection Market Report Scope & Overview:

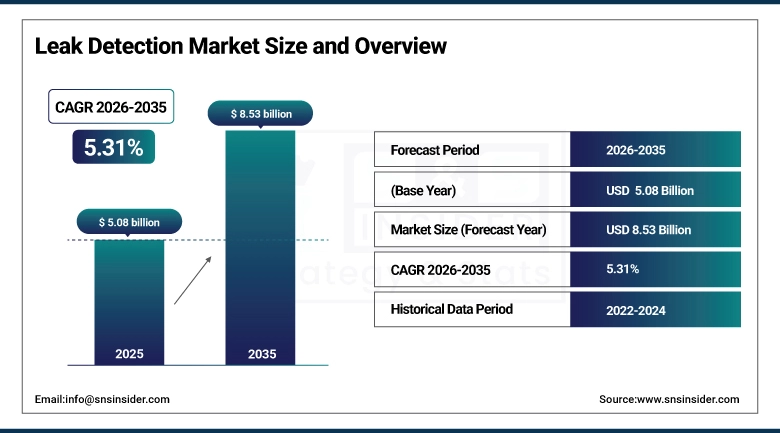

The Leak Detection Market was valued at USD 5.08 billion in 2025 and is expected to reach USD 8.53 billion by 2035, growing at a CAGR of 5.31% from 2026-2035.

Leak Detection Market growth is being propelled by factors such as rising global water scarcity issues, aging infrastructure, and stringent environmental norms. Companies are embracing sophisticated leak detection technologies in order to minimize losses of valuable resources and cut down on expenses while also ensuring safety. Moreover, fast-growing urbanization along with the expansion of industries including oil & gas, chemicals, and water are also boosting the market demand.

The U.S. EPA estimates that methane emissions from oil and gas operations account for approximately 30% of total U.S. methane output. The EPA's Methane Emissions Reduction Program under the Inflation Reduction Act mandates comprehensive leak monitoring across covered facilities starting 2024.

Leak Detection Market Size and Growth Forecast

-

Market Size in 2025: USD 5.08 Billion

-

Market Size by 2035: USD 8.53 Billion

-

CAGR: 5.31% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Leak Detection Market - Request Free Sample Report

Leak Detection Market Trends

-

UAV-based gas detection is moving from pilot program status to standard operating procedure in large oil field and refinery environments where ground inspections are slow and dangerous.

-

Optical Gas Imaging cameras are being integrated into fixed continuous monitoring arrays rather than used solely as periodic inspection tools, changing the economics of the technology.

-

Regulatory pressure around fugitive methane emissions is pushing upstream oil and gas operators toward certified leak detection and repair (LDAR) programs with third-party verification requirements.

-

Water utilities globally are deploying acoustic correlator networks across distribution systems to identify pipe leaks before they surface, reducing non-revenue water losses.

-

Artificial intelligence is being applied to sensor data streams to distinguish genuine leak signatures from background noise and equipment vibration, cutting false alarm rates significantly.

-

Cloud-based LDAR management platforms are consolidating inspection records, sensor alerts, and repair documentation into auditable compliance databases that satisfy regulatory reporting requirements.

-

The miniaturization of multi-gas detection sensors is enabling integration into wearable personal safety monitors that double as facility-wide distributed sensing nodes.

U.S. Leak Detection Market Size Outlook:

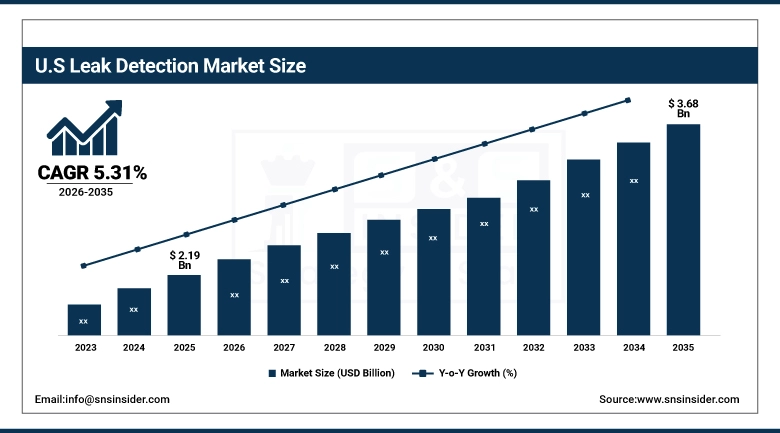

The U.S. Leak Detection Market was valued at USD 2.19 billion in 2025 and is expected to reach USD 3.68 billion by 2035, growing at a CAGR of 5.31% from 2026-2035. The U.S. sits at the intersection of several forces that make it the world's largest leak detection market by a comfortable margin. It has the most extensive pipeline network on earth over 3 million miles of pipelines carrying oil, gas, hazardous liquids, and water and much of that infrastructure was built decades ago and is now at a stage in its service life where monitoring investment is operationally and legally necessary. Federal regulations enforced by the Pipeline and Hazardous Materials Safety Administration (PHMSA) require operators of high-consequence area pipelines to implement integrity management programs that include leak detection as a core component.

PHMSA has awarded over USD 41 million in grants to improve pipeline safety and leak detection technology deployment across U.S. operators. The agency's Gas Gathering Rule extended federal safety regulations to over 400,000 miles of previously unregulated gathering lines.

Leak Detection Market Segment Analysis

-

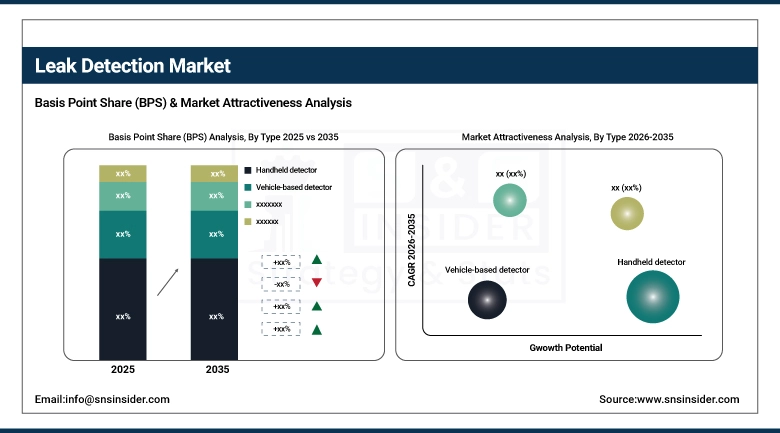

By Type, Handheld Detector segment dominated the Leak Detection Market with ~47% share in 2025; UAV-Based Detector segment fastest growing (CAGR ~7.54%).

-

By Technology, Volatile Organic Compound Analyzer segment dominated the Leak Detection Market with ~31% share in 2025; Optical Gas Imaging segment fastest growing (CAGR ~7.29%).

-

By End User, Oil & Gas segment dominated the Leak Detection Market with ~39% share in 2025; Chemical & Petrochemical segment fastest growing (CAGR ~7.44%).

By Type, Handheld Detector segment dominates the Leak Detection Market, UAV-Based Detector segment expected to grow fastest

Handheld detectors carried approximately 47% of the market in 2025 and are likely to hold a meaningful lead for years to come. The reason is practical: they are affordable, require minimal infrastructure, and can be deployed by any trained technician without the operational planning overhead that fixed systems or drone flights require. For smaller facilities, routine inspection rounds with portable gas detectors or VOC analyzers remain the most cost-effective leak detection approach available. In larger facilities, handheld units serve as the verification tool after a fixed sensor or continuous monitoring system flags a potential event the operator brings in a handheld to locate precisely where in a process section the leak is originating. That complementary role keeps handheld detector volumes high even as more sophisticated technologies grow around them.

UAV-based detectors represent the fastest-growing segment at a projected CAGR of 7.54%, and the use case driving that growth is compelling. Inspecting tens of miles of pipeline corridor, scanning a refinery complex, or surveilling a large compressor station on foot or by vehicle is slow, expensive, and exposes inspection personnel to unnecessary hazard. A drone equipped with a methane-sensing payload whether laser absorption spectrometry or cavity ring-down spectroscopy can cover the same area in a fraction of the time, log GPS-tagged concentration data at every point, and generate a georeferenced emissions map without a single person entering a hazardous zone. As regulatory bodies in the U.S. and Europe increasingly accept drone-generated data for LDAR compliance purposes, the operational case for UAV investment becomes straightforward.

By Technology, VOC Analyzer segment dominates the Leak Detection Market, Optical Gas Imaging segment expected to grow fastest

Volatile Organic Compound analyzers held approximately 31% of the market in 2025, reflecting the technology's broad applicability across oil and gas, chemical, and manufacturing facilities where VOC emissions are both a regulatory compliance concern and a process efficiency indicator. Real-time VOC monitoring provides facility managers with continuous visibility into emission levels, early warning of process upsets, and the concentration data needed to prioritize repair response. Photoionization detector-based VOC analyzers in particular have become standard equipment in refineries and chemical plants because of their sensitivity across a wide range of organic compounds and their straightforward operation in continuous monitoring configurations.

Optical Gas Imaging is the fastest-growing technology segment with a projected CAGR of 7.29%. OGI cameras render otherwise invisible gas clouds as visible plumes on a thermal imaging display a visual intuition that is simply more actionable in the field than a numeric concentration reading. Inspectors can sweep a large process area quickly, immediately spot leaks from flanges, valves, or pump seals, and record video evidence in a format that satisfies regulatory documentation requirements. The technology gained significant momentum from the EPA's OGI-specific provisions in its LDAR regulations, and ongoing price reductions in OGI camera hardware are steadily expanding the addressable market beyond large tier-one operators.

By End User, Oil & Gas segment dominates the Leak Detection Market, Chemical & Petrochemical segment expected to grow fastest

Oil and gas retained the dominant end-user position at approximately 39% of market revenue in 2025 a share built on the sector's unique combination of regulatory pressure, operational risk, and financial consequence from leakage events. Pipeline ruptures, wellhead releases, and compressor seal failures can each trigger regulatory investigations, remediation liabilities, and asset shutdowns that cost far more than any leak detection investment. The PHMSA's integrity management rules, the EPA's Quad O and OOOOa regulations for the upstream sector, and state-level methane rules in California, Colorado, and Pennsylvania collectively create a regulatory environment where continuous monitoring is increasingly the default rather than the exception.

Chemical and Petrochemical is the fastest-growing end-user segment at roughly 7.44% CAGR, driven by two converging forces: rapid capacity expansion across Asia and the Middle East, and tightening chemical process safety regulations globally. New petrochemical complexes in China, Saudi Arabia, and India are being built with modern leak detection infrastructure integrated from day one rather than retrofitted later, which tends to mean more sophisticated and comprehensive monitoring systems than aging facilities carry. Meanwhile, chemical industry regulators in Europe and North America are updating process safety management requirements in ways that specifically require enhanced fugitive emission monitoring, adding compliance-driven demand on top of the new-construction growth.

Leak Detection Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

88% |

|

Europe |

Germany |

28% |

|

Asia Pacific |

China |

48% |

|

Middle East & Africa |

Saudi Arabia |

40% |

|

Latin America |

Brazil |

50% |

North America Leak Detection Market Insights

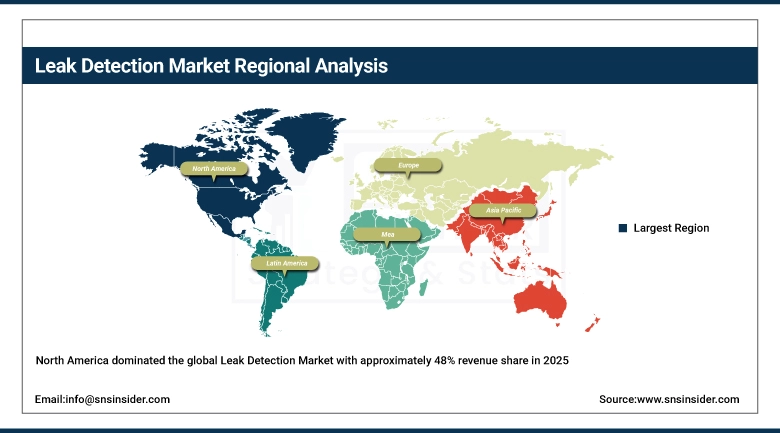

North America dominated the global Leak Detection Market with approximately 48% revenue share in 2025. The combination of the world's most extensive pipeline network, the most proactive regulatory environment for leak monitoring, and a dense concentration of oil, gas, chemical, and water infrastructure creates the conditions for both high baseline demand and a continuous upgrade cycle as older systems are replaced with smarter technology. The U.S. natural gas distribution system alone serves over 78 million customers through roughly 1.2 million miles of distribution piping, a substantial portion of which is aging cast iron or unprotected steel requiring active monitoring programs. Canada's oil sands infrastructure and extensive gas gathering networks add another significant demand center within the region.

The U.S. Department of Transportation reports that pipeline incidents cause over USD 800 million in property damage annually. PHMSA's updated Pipeline Safety Improvement Act requirements mandate integrity testing and monitoring technology upgrades across regulated pipeline operators.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Leak Detection Market Insights

Asia Pacific is the fastest-growing regional market at approximately 7.48% CAGR through 2035. China's aggressive expansion of its natural gas distribution network part of the government's strategy to reduce coal dependence and improve urban air quality is creating substantial new leak detection procurement demand as thousands of miles of new urban gas mains are commissioned annually. India's rapid industrial growth, combined with the Ministry of Petroleum's pipeline expansion programs and tightening process safety rules, is generating similar demand in the subcontinent. Japan and South Korea, with their advanced industrial sectors, are applying sophisticated continuous monitoring technologies to both existing and new petrochemical and semiconductor manufacturing facilities.

China's State Administration of Work Safety has mandated IoT-based gas leak monitoring systems in all new chemical industrial parks built after 2022. India's Petroleum and Natural Gas Regulatory Board (PNGRB) requires leak detection plans for all licensed city gas distribution operators nationwide.

Europe Leak Detection Market Insights

Europe held approximately 20% of the global Leak Detection Market in 2025, with Germany, the Netherlands, Norway, and the UK as the core markets. Europe's leak detection adoption is driven by some of the world's most stringent industrial safety and environmental regulations the EU Industrial Emissions Directive, the Seveso III directive for chemical facility safety, and the EU Methane Regulation that came into force in 2024 and establishes mandatory leak detection and repair requirements for coal, oil, and gas operators across member states. These regulations are not creating demand at the margin; they are mandating specific monitoring frequencies, sensor types, and documentation requirements that effectively define the technology procurement agenda for covered operators.

The EU Methane Regulation (EU 2024/1787) requires oil and gas operators to conduct quarterly LDAR surveys using approved methods including OGI cameras and portable analyzers. Non-compliance carries penalties of up to 5% of annual turnover under member state enforcement frameworks.

Middle East & Africa and Latin America Leak Detection Market Insights

The Middle East leads MEA adoption through Saudi Arabia, UAE, and Kuwait, where major national oil companies including Saudi Aramco, ADNOC, and Kuwait Petroleum are investing in modern leak detection infrastructure as part of broader operational efficiency and environmental compliance programs. Saudi Aramco has publicly committed to reducing its upstream methane intensity to near-zero levels and is deploying continuous monitoring technology across its production facilities to track progress toward that target. In Latin America, Brazil's Petrobras operations drive the largest portion of regional demand, while growing gas distribution expansion in Mexico under the CFE's pipeline programs is adding new leak detection procurement volume to the market.

Saudi Aramco's 2030 methane intensity target of less than 0.07% has driven deployment of continuous monitoring and optical gas imaging programs across its Ghawar and offshore fields. Aramco published independently verified methane intensity data of 0.06% for 2023 operations.

Leak Detection Market Growth Drivers:

-

Escalating regulatory compliance requirements and pipeline safety concerns driving global investment in leak detection technologies

The single most powerful force behind leak detection market growth is not technology capability or commercial demand it is regulatory obligation. Operators who used to treat leak detection as best practice are now required to treat it as a legal mandate with documented procedures, inspection frequencies, and repair timelines. In the U.S., EPA methane rules and PHMSA pipeline integrity requirements together cover hundreds of thousands of facilities and miles of pipeline where certified monitoring is now non-negotiable. In the EU, the Methane Regulation is applying equivalent pressure to oil and gas operators across all member states. In Asia, China's chemical park safety rules and India's city gas distribution regulations are extending the compliance footprint further. The global regulatory convergence around fugitive emission monitoring is creating a durably growing demand base for leak detection that is largely independent of commodity price cycles.

The EPA's revised OOOOb rule finalized in 2024 extends comprehensive LDAR requirements to hundreds of thousands of previously unregulated wellsites and compressors. Industry analysts estimate compliance spending at over USD 1.5 billion annually across covered U.S. upstream operators.

Leak Detection Market Restraints:

-

High system costs and integration complexity limiting widespread leak detection deployment across price-sensitive industrial markets

The economics of leak detection are straightforward for large operators the avoided cost of a single major pipeline incident can repay years of monitoring investment. For smaller operators, the calculation is less clear. A rural gas distribution utility serving fifty thousand customers faces the same regulatory requirements as a major pipeline company but with a fraction of the budget and technical staff available to meet them. Advanced continuous monitoring systems fiber optic distributed acoustic sensing, fixed OGI cameras, drone inspection programs carry capital and operational costs that challenge smaller operators' financial models. Integration of new leak detection systems with legacy SCADA infrastructure also frequently requires engineering work that drives up total project cost well beyond hardware purchase price. These economics create a market tiering effect where the most sophisticated technologies remain concentrated in well-funded large operators.

Leak Detection Market Opportunities:

-

AI-powered sensors and UAV technology opening vast untapped opportunities in remote pipeline leak detection globally

The convergence of AI analytics, drone platform capability, and falling sensor costs is creating a genuine inflection point in how remote and difficult-to-access infrastructure gets monitored. Pipeline corridors through mountain ranges, desert environments, and wetlands have historically been inspected on foot or by manned aircraft at low frequency not because operators did not want better coverage, but because better coverage was simply not affordable. AI-equipped drones with multi-spectral and laser absorption sensors can now fly these corridors autonomously, flag anomalies in real time, and transmit georeferenced data to cloud platforms where AI models compare current readings against historical baselines to distinguish real leaks from background variation. This capability is expanding the addressable market for leak detection into geographic and infrastructure contexts where traditional monitoring was economically impractical.

Recent Developments:

-

2026: Honeywell International launched its next-generation BACnet-connected fixed gas detection platform for industrial facilities, incorporating AI-powered multi-gas discrimination algorithms that reduce false alarm rates by up to 60% compared to threshold-based legacy systems while simultaneously meeting updated IEC 60079-29 detector performance standards for hazardous area installations.

-

2025: Siemens AG deployed its AI-based leak detection system across several major European refining and petrochemical sites under long-term service agreements, with the platform combining fixed-sensor arrays, OGI camera integration, and a cloud analytics layer that provides regulators with real-time emission inventory data compliant with the EU Methane Regulation's reporting requirements.

-

2025: Baker Hughes expanded its Waygate Technologies industrial inspection portfolio with a new drone-based methane detection service targeting U.S. midstream pipeline operators, combining LIDAR-based navigation with tunable diode laser absorption spectroscopy payloads to deliver LDAR survey data that meets EPA OOOOb acceptable alternative monitoring method criteria.

Leak Detection Companies are:

-

Honeywell International Inc.

-

Siemens AG

-

Emerson Electric Co.

-

Baker Hughes Company (Waygate Technologies)

-

MSA Safety Incorporated

-

FLIR Systems Inc. (Teledyne FLIR)

-

Xylem Inc.

-

Atmos International Ltd.

-

PSI AG

-

Krohne Messtechnik GmbH

-

Perma-Pipe Inc.

-

ROSEN Group

-

Synodon Inc.

-

Gas Technology Institute (GTI Energy)

-

Det-Tronics (United Technologies)

-

Sensit Technologies LLC

-

GasSecure AS (Drägerwerk)

-

Aquam Corporation

-

Infosys BPM Ltd. (Water Solutions)

Leak Detection Market Report Scope

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 5.08 Billion |

| Market Size by 2035 | USD 8.53 Billion |

| CAGR | CAGR of 5.31% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Handheld detector, Vehicle-based detector, UAV-based detector) • By Technology (Volatile Organic Compound (VOC) analyzer, Optical Gas Imaging (OGI), Laser absorption spectroscopy, Acoustic leak detection, Audio-visual-olfactory inspection) • By End-use Industry (Aerospace, Automotive, Chemical & petrochemical, Energy & utility, Food & beverage, Oil & gas, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Honeywell International Inc., Siemens AG, Emerson Electric Co., Baker Hughes Company (Waygate Technologies), MSA Safety Incorporated, FLIR Systems Inc. (Teledyne FLIR), Xylem Inc., Mueller Water Products Inc., Atmos International Ltd., PSI AG, Krohne Messtechnik GmbH, Perma-Pipe Inc., ROSEN Group, Synodon Inc., Gas Technology Institute (GTI Energy), Det-Tronics (United Technologies), Sensit Technologies LLC, GasSecure AS (Drägerwerk), Aquam Corporation, and Infosys BPM Ltd. (Water Solutions). |

Frequently Asked Questions

North America dominated the Leak Detection Market in 2025.

The Oil & Gas segment dominated the Leak Detection Market with approximately 39% share in 2025.

Escalating regulatory compliance requirements and pipeline safety concerns driving global investment in leak detection technologies is the primary growth driver of the Leak Detection Market.

The Leak Detection Market was valued at USD 5.08 billion in 2025.

The Leak Detection Market is expected to grow at a CAGR of 5.31% from 2026 to 2035.

Get in Touch