Lithium Titanate Oxide (LTO) Battery Market Report Scope & Overview:

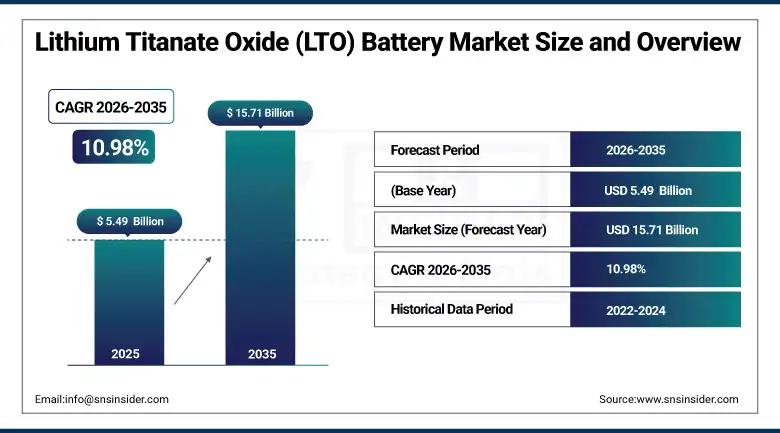

The Lithium Titanate Oxide (LTO) Battery Market was valued at USD 5.49 Billion in 2025 and is expected to reach USD 15.71 Billion by 2035, growing at a CAGR of 10.98% from 2026 to 2035.

The global lithium titanate oxide battery market is steadily expanding. Instead of utilizing a graphite anode, LTO batteries make use of lithium titanate and do not need the creation of the solid electrolyte interface layer associated with graphite batteries, limiting their charging rates and thermal capabilities. The market growth is fueled by the increase in demand for hybrid and plug-in hybrid vehicles whose characteristics match the features of LTO batteries, the rise in industrial automation and the increased need for automated guided vehicles and mobile robots whose frequent utilization makes LTO more attractive due to its better cycle life, and the existence of government incentives for clean energy and electric vehicles.

In March 2024, ZAPBATT and Toshiba Corporation made an announcement about their collaboration on a platform known as Battery Operating System (bOS). The new platform seeks to ensure that Toshiba’s unique battery chemistry of SCiB LTO is integrated into multiple applications such as those used in industry, business, and consumer segments using battery management software technology. This partnership has made it possible to integrate benefits offered by the LTO battery chemistry technology into multiple applications ranging from cordless tools, electric bicycles to industrial automation, thus proving that LTO technology is increasingly being applied commercially.

Market Size and Forecast

-

Market Size in 2026E: USD 6.10 Billion

-

Market Size by 2035: USD 15.71 Billion

-

CAGR: 10.98% from 2026 to 2035

-

Fastest Growing Region: North America

-

Largest Region: Asia Pacific

To Get more information On Lithium Titanate Oxide (LTO) Battery Market - Request Free Sample Report

Lithium Titanate Oxide (LTO) Battery Market Trends

-

LTO batteries are gaining adoption in grid frequency regulation applications due to ultra-fast response and exceptional cycling durability.

-

Electric buses and commercial vehicles increasingly utilize LTO batteries for rapid opportunity charging and enhanced operational efficiency.

-

Research into solid-state electrolyte integration with LTO anodes is advancing safer and longer-lasting next-generation battery technologies.

-

Miniaturized LTO batteries are expanding use in medical devices and wearable electronics requiring compact, long-life power solutions.

-

Renewable energy storage projects are adopting LTO batteries for frequent deep-cycling applications and long operational lifetimes.

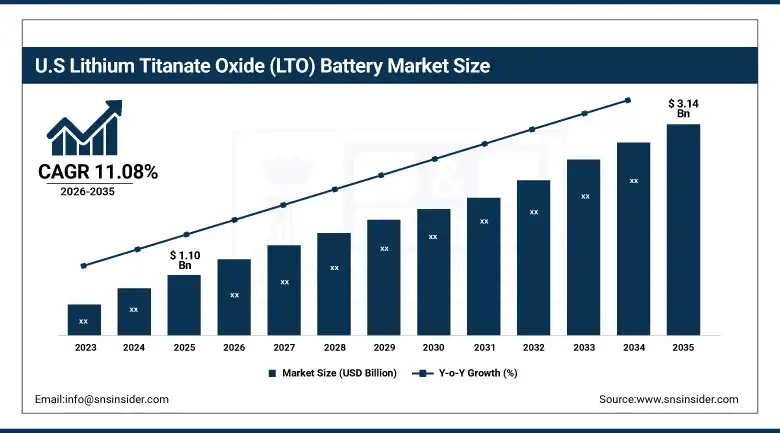

The U.S. Lithium Titanate Oxide (LTO) Battery Market Outlook

The U.S. Lithium Titanate Oxide (LTO) Battery Market was valued at approximately USD 1.10 Billion in 2025 and is expected to reach approximately USD 3.14 Billion by 2035, growing at a CAGR of approximately 11.08%.

The U.S. is the most commercially significant LTO battery market within North America's fastest growing regional position. Incentives from the government through the Inflation Reduction Act’s Advanced Manufacturing Tax Credit, increased demand for LTO batteries because of homegrown initiatives for the electrification of electric vehicles and commercial fleets, and investments in utility grid energy storage in LTO batteries as part of the frequency regulation program all support above average growth for North America’s LTO battery market. The involvement of the Department of Defense in the procurement of LTO batteries to use for military vehicles that operate efficiently in cold weather and have fast charge capabilities represents another source of growth.

In 2024, Altairnano, operating as Gree Altairnano New Energy, expanded deployment of its ALTI-ESS energy storage system incorporating LTO battery technology for utility grid frequency regulation, with systems delivered to multiple utility customers in North America and Europe demonstrating the commercial scale of utility-grade LTO energy storage in frequency regulation service markets where the technology's instantaneous response and extreme cycle durability create compelling economics over alternative battery chemistries.

Lithium Titanate Oxide (LTO) Battery Market Segment Analysis

-

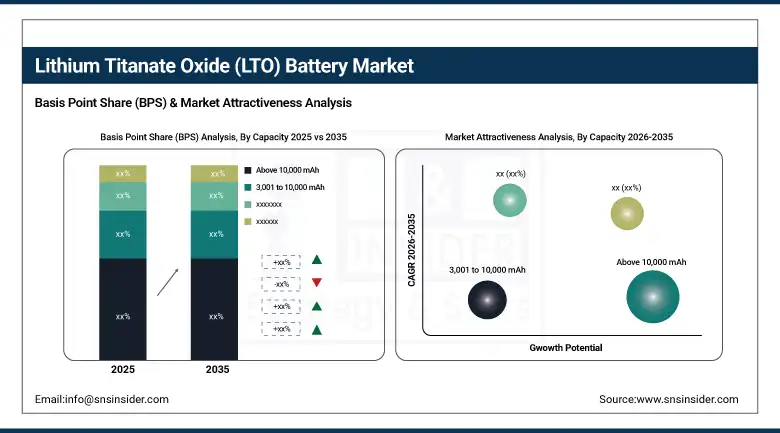

By Capacity, the above 10,000 mAh segment dominated the market with approximately 55% share in 2025, while the below 3,000 mAh segment is the fastest growing.

-

By Voltage, the medium voltage segment dominated the market with the largest share in 2025, while the high voltage segment is the fastest growing.

-

By Material, the lithium titanate segment dominated the market with approximately 43% share in 2025, while the metal oxides segment is the fastest growing.

-

By Component, the electrodes segment dominated the market with the largest share in 2025, while the electrolytes segment is the fastest growing.

-

By Application, the automotive segment dominated the market with the largest share in 2025, while the industrial segment is the fastest growing.

By Capacity, above 10,000 mAh dominates, below 3,000 mAh grows fastest

The above 10,000 mAh segment retained the dominant capacity position with approximately 55% of the LTO battery market in 2025. High-capacity LTO systems' commercial primacy reflects the application concentration in electric buses and commercial vehicles whose large battery packs require multi-kilowatt-hour energy storage, grid frequency regulation systems whose megawatt-hour scale creates extraordinary per-installation commercial value, and stationary backup power systems whose extended runtime requirements create high-capacity LTO procurement. Altairnano's ALTI-ESS grid storage system and Microvast's electric bus battery pack collectively represent the commercial scale of high-capacity LTO deployment.

The below 3,000 mAh segment is the fastest growing because consumer electronics miniaturization, medical device design evolution, and IoT sensor battery requirements are creating growing demand for compact LTO cells whose fast charging, long lifespan, and safety advantages create differentiated value in small device applications that conventional lithium-ion coin cells and cylindrical cells cannot match on cycle life or charging speed. Nichicon's SLB Series compact LTO batteries' direct circuit board soldering design demonstrates the commercial innovation in miniaturized LTO formats whose space efficiency advantage relative to conventional mounting bracket-equipped alternatives creates specification preference in space-constrained wearable, medical implant, and compact industrial sensor applications.

By Application, automotive dominates, industrial grows fastest

Automotive retained the dominant application position in the LTO battery market in 2025. Hybrid and plug-in hybrid electric vehicles' above-average LTO adoption reflects the technology's alignment with PHEV battery performance requirements that differ from pure battery electric vehicle specifications in emphasizing cycle durability, fast recharge, and cold weather reliability over maximum energy density. Each PHEV whose smaller battery pack undergoes multiple daily charge-discharge cycles creates total lifetime cycle requirements that graphite-anode batteries reach well before vehicle end-of-life but that LTO batteries comfortably accommodate within their 20,000-cycle operational life.

Industrial is the fastest growing application because the electrification of material handling equipment including automated guided vehicles, autonomous mobile robots, and electric forklifts creates LTO procurement from logistics and manufacturing operators whose multi-shift continuous operation creates daily battery cycling intensity that rapidly accumulates total cycles beyond conventional lithium-ion battery warranty limits. Each warehouse that operates AGV fleets across 16 to 24 hours per day creates battery cycling demands that LTO's 20,000-cycle life serves for over 27 years of daily cycling versus 3 to 7 years for graphite-anode alternatives.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Lithium Titanate Oxide (LTO) Battery Market Insights

North America is the fastest growing regional LTO battery market, driven by rising government incentives for electric vehicles and renewable energy storage, substantial grid storage investment from U.S. utilities for frequency regulation, and the growing industrial automation sector's material handling electrification. The United States accounts for approximately 87.4% of North American revenues through Microvast, Altairnano, and the commercial operations of Toshiba, Leclanché, and international LTO cell manufacturers’ U.S. distribution and integration networks.

Canada contributes approximately 12.6% of North American revenues through its renewable energy sector's grid storage investment, the transit authority's electric bus fleet electrification, and the industrial sector's material handling equipment electrification programmes in Ontario and British Columbia.

Europe Lithium Titanate Oxide (LTO) Battery Market Insights

Europe is a technically sophisticated LTO battery market where the EU's emission reduction mandates, PHEV incentive programmes, and grid storage investment create structured institutional demand. Germany constitutes around 22.3% of the revenue generation in Europe through its automotive OEM PHEV manufacturing, industrial automation industry material handling electrification, and energy industry grid frequency regulation investments. Leclanche’s Switzerland-headquartered and Europe-operated business ensures regional supply of LTO batteries manufactured by an established European company.

France, the UK, and Scandinavia make up important secondary markets, which feature LTO purchase opportunities through investments in electric bus fleets, incentives for PHEV, and renewable energy storage. The EU's Industrial Emissions Directive on electrification of equipment creates rising interest in LTO industrial adoption.

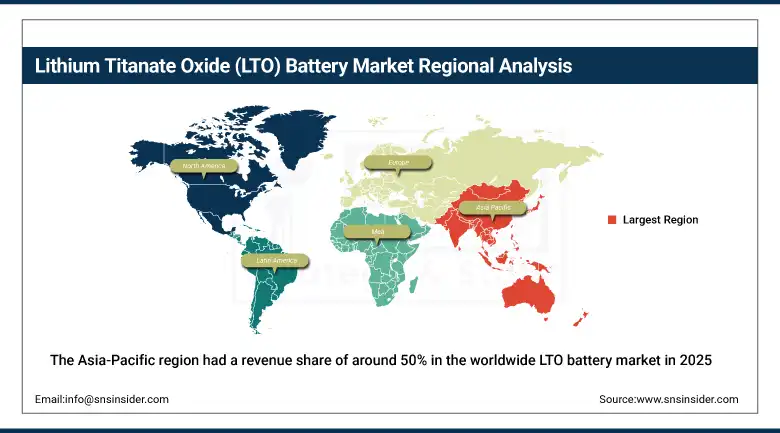

Asia Pacific Lithium Titanate Oxide (LTO) Battery Market Insights

The Asia-Pacific region had a revenue share of around 50% in the worldwide LTO battery market in 2025 due to rapid developments within the electric vehicles market within China, Japan, and South Korea, focus on developing energy sources that are more environmentally friendly, and the region's incredible capacity for manufacturing batteries. China makes up a significant proportion of about 44.8% of the Asia-Pacific market revenues because of their large number of electric buses used domestically, installation of grid storage, and electrified material handling.

Japan can be considered one of the most advanced countries for its LTO batteries with Toshiba's SCiB LTO Battery having already been implemented into commercial use in railways, automobile and industries. South Korea with its rapidly developing battery industry and increasing adoption of electric vehicles creates a structured LTO demand through integration programs in automotive Original Equipment Manufacturer (OEM). India presents a high potential for LTO adoption with its developing economy.

Get Customized Report as per Your Business Requirement - Enquiry Now

MEA & Latin America Lithium Titanate Oxide (LTO) Battery Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through NEOM's renewable energy storage investment, Vision 2030's industrial electrification programme, and the grid modernization initiative creating LTO energy storage procurement. The UAE's renewable energy storage and industrial automation add complementary Gulf demand. Brazil leads Latin American revenues at approximately 44.2% through its growing industrial automation sector, the renewable energy storage market, and the electric bus fleet expansion programme. Mexico's manufacturing sector automation and Chile's renewable energy investment collectively sustain regional LTO market development through 2035.

Market Dynamics

Growth Drivers: Industrial automation electrification creating intensive cycling demand and PHEV adoption leveraging LTO fast charging advantage

Industrial automation electrification is the LTO battery market's most commercially significant near-term structural growth driver. The global AGV and AMR market's extraordinary expansion, driven by e-commerce fulfilment automation, manufacturing Industry 4.0 investment, and logistics center robotic integration, creates battery procurement from fleet operators whose multi-shift operational intensity creates annual cycle counts that exhaust conventional lithium-ion battery warranties within 2 to 3 years but represent only a small fraction of LTO's 20,000-cycle operational life. Each AGV fleet operator that switches from conventional lithium-ion to LTO through total cost of ownership analysis creates above-average per-vehicle LTO battery investment whose economics improve proportionally with fleet operational intensity.

PHEV adoption growth driven by government incentives, consumer range anxiety mitigation, and automotive OEM PHEV model portfolio expansion creates growing LTO automotive procurement. LTO batteries' 10-to-20-minute fast charge capability for PHEV battery packs aligns with the opportunity charging usage pattern of commuter vehicles that charge during workplace parking, shopping center visits, and transit corridor stops without the extended session requirement that home overnight charging provides. Each PHEV buyer who relies on public fast charging rather than home overnight charging creates a usage profile that specifically rewards LTO's charging speed advantage over graphite alternatives.

Restraints: Higher cost relative to conventional lithium-ion and limited manufacturing capacity

The higher production cost of LTO batteries relative to conventional graphite-anode lithium-ion alternatives creates a commercial barrier in price-sensitive market segments whose total cost of ownership calculation does not adequately capture LTO's cycle life and operational advantage over the comparison timeframe relevant to procurement decision-making. High-quality lithium and titanium raw material costs, specialized LTO anode material synthesis requirements, and lower production scale relative to mainstream lithium-ion chemistries collectively create per-kilowatt-hour pricing that is 30 to 50 percent above equivalent lithium iron phosphate alternatives in applications where cycle life advantage is not factored into procurement comparison.

Limited manufacturing capacity relative to mainstream lithium-ion chemistries constrains LTO supply availability in large-scale deployment programmes whose volume requirements exceed established LTO production capacity. The concentration of LTO manufacturing capacity among a small number of producers including Toshiba, Microvast, Leclanché, and Gree Altairnano creates supply chain concentration risk for large procurement programmes whose dependency on limited supplier options moderates procurement confidence relative to the commodity lithium-ion supply base.

Opportunities: Grid frequency regulation and EV fleet fast charging infrastructure

Grid frequency regulation represents the most commercially premium LTO application whose instantaneous charge and discharge response at millisecond timescales creates a service capability that conventional power plants and most alternative battery chemistries cannot match for primary frequency control. Each utility's frequency regulation capacity that transitions from thermal plant dependency to LTO battery provision creates above-average revenue per megawatt-hour of battery capacity compared with energy arbitrage applications. Altairnano's ALTI-ESS system demonstrates the commercial viability of utility-scale LTO frequency regulation with its demonstrated 1,400 amp peak discharge, 86% round-trip efficiency, and above-12,000-cycle durability at full depth of discharge.

EV fleet fast charging infrastructure expansion creates growing LTO demand from fleet operators whose total vehicle uptime economics justify above-conventional-lithium-ion investment for the charging speed advantage. Each commercial vehicle fleet operator whose route economics require 5 to 15 minute opportunity charging between routes creates a LTO specification case whose per-vehicle economics improve with the charge session time savings multiplied by driver time cost and vehicle utilization improvement over an alternative slower-charging chemistry.

Recent Developments:

-

2025: Toshiba Corporation launched its next-generation SCiB battery module with approximately double the heat dissipation performance, targeting electric buses, electric ships, and stationary energy storage applications requiring continuous high-power charging and discharging.

-

2025: Toshiba Corporation commenced sample shipments of its SCiBNb battery featuring a niobium titanium oxide anode, delivering 80% charging in 10 minutes and an estimated lifespan exceeding 15,000 cycles for commercial electric vehicles.

-

2025: Microvast Holdings unveiled next-generation fast-charging battery solutions at Smart Energy Week 2025, highlighting advanced battery systems designed for commercial vehicles, energy storage systems, and industrial electrification applications.

-

2025: Leclanche SA was selected for funding under the European Union Innovation Fund battery program to support development of its planned battery manufacturing facility in Germany, strengthening advanced battery production capacity in Europe.

Lithium Titanate Oxide (LTO) Battery Market key players are:

-

Toshiba Corporation (SCiB)

-

Microvast Holdings Inc.

-

Leclanché SA

-

Gree Altairnano New Energy Inc.

-

Nichicon Corporation

-

Narada Power Source Co. Ltd.

-

Saft Groupe SA

-

EaglePicher Technologies LLC

-

Electrovaya Inc.

-

Zenaji Pty Ltd.

-

CALB Co. Ltd.

-

Yinlong Energy Co., Ltd.

-

Skeleton Technologies

-

Hitachi Energy

-

Tianneng Battery Group Co., Ltd.

-

BYD Company Limited

-

CBAK Energy Technology Inc.

-

XALT Energy LLC

-

Sinoev Technologies

-

EnerDel Inc.

Lithium Titanate Oxide (LTO) Battery Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 5.49 Billion |

| Market Size by 2035 | USD 15.71 Billion |

| CAGR | CAGR of 10.98% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Capacity (Below 3,000 mAh, 3,001 to 10,000 mAh, Above 10,000 mAh) • By Voltage (Low, Medium, High) • By Material (Lithium Titanate, Graphite, Metal Oxides) • By Component (Electrodes, Cathode, Anode, Electrolytes) • By Application (Consumer Electronics, Automotive, Aerospace, Marine, Medical, Industrial, Power, Telecommunication) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Toshiba Corporation (SCiB), Microvast Holdings Inc., Leclanché SA, Gree Altairnano New Energy Inc., Nichicon Corporation, Narada Power Source Co. Ltd., Saft Groupe SA, EaglePicher Technologies LLC, Electrovaya Inc., Zenaji Pty Ltd., CALB Co. Ltd., Yinlong Energy Co., Ltd., Skeleton Technologies, Hitachi Energy, Tianneng Battery Group Co., Ltd., BYD Company Limited, CBAK Energy Technology Inc., XALT Energy LLC, Sinoev Technologies, EnerDel Inc. |

Frequently Asked Questions

The Lithium Titanate Oxide (LTO) Battery Market is expected to grow at a CAGR of 10.98% from 2026 to 2035.

The Lithium Titanate Oxide (LTO) Battery Market was valued at USD 5.49 Billion in 2025.

Industrial automation electrification creating intensive cycling demand that rewards LTO's 20,000-cycle operational life advantage over conventional lithium-ion alternatives.

Above 10,000 mAh dominated with approximately 55% share in 2025, while the Below 3,000 mAh segment is the fastest growing.

Asia Pacific dominated the Lithium Titanate Oxide Battery Market with approximately 50% of revenues in 2025.

Get in Touch