Long Duration Energy Storage Market Report Scope & Overview:

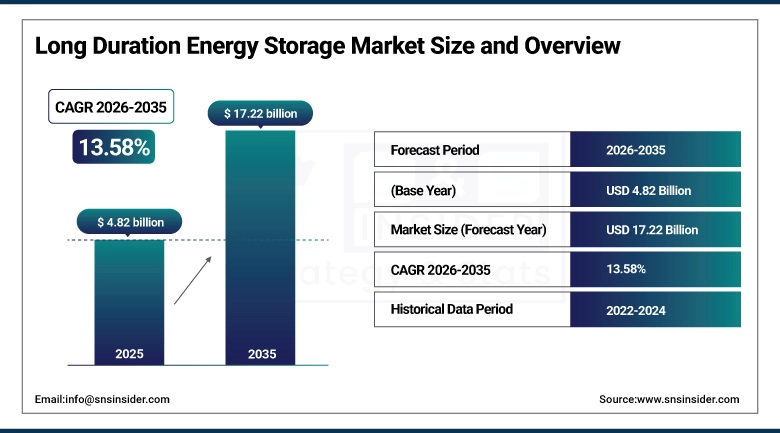

The Long Duration Energy Storage Market size was valued at USD 4.82 Billion in 2025 and is projected to reach USD 17.22 Billion by 2035, growing at a CAGR of 13.58% during 2026-2035.

The global Long Duration Energy Storage (LDES) market is emerging as one of the most strategically critical infrastructure categories in the global clean energy transition, providing the multi-hour and multi-day electricity storage capability that is fundamentally necessary for power grids to achieve high renewable energy penetration without sacrificing reliability, security, or affordability.

Market Size and Forecast:

-

Market Size in 2025: USD 4.82 Million

-

Market Size by 2035: USD 17.22 Million

-

CAGR: 13.58% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Long Duration Energy Storage Market - Request Free Sample Report

Long Duration Energy Storage Market Key Trends:

-

The market is driven by the growing need to integrate renewable energy sources such as solar and wind, which require long-duration storage to balance intermittent power generation.

-

Advanced battery chemistries, including flow batteries, sodium-based batteries, and metal-air technologies, are gaining attention for their ability to provide extended storage durations beyond traditional lithium-ion systems.

-

Governments and utilities are increasingly investing in long duration energy storage projects to enhance grid reliability, support decarbonization goals, and enable large-scale renewable energy deployment.

-

High upfront capital costs and technological maturity challenges remain key restraints, limiting widespread commercial adoption across several regions.

-

Research institutions and private companies are accelerating innovation through pilot projects and demonstration plants to improve system efficiency, scalability, and cost competitiveness.

-

Strategic partnerships between energy companies, technology developers, and government bodies are driving large-scale deployment and strengthening the future growth potential of the market.

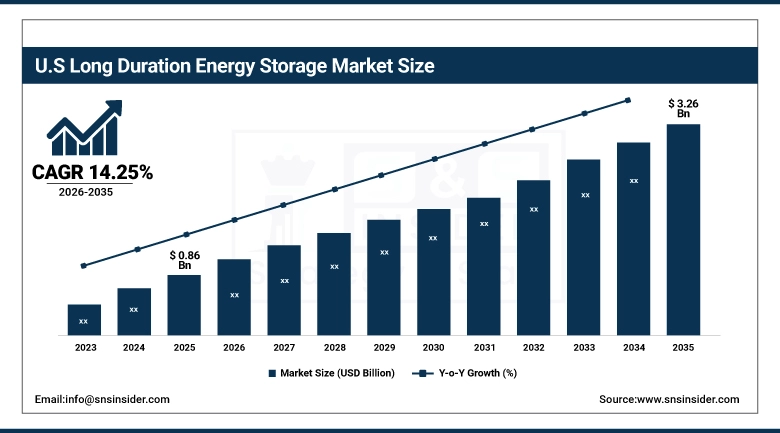

U.S. Long Duration Energy Storage Market was valued at approximately USD 1.69 billion in 2025 and is expected to reach approximately USD 6.03 billion by 2035, registering a CAGR of 13.58% during 2026–2035.

The United States is the world's most commercially active long duration energy storage market, driven by the Inflation Reduction Act's investment tax credits for standalone energy storage projects that for the first time make LDES projects financially bankable without co-location with generation assets, the DOE's Long Duration Storage Shot programme targeting 90% cost reduction to unlock mass commercial deployment, and the growing frequency of multi-day renewable energy drought events in high-penetration renewable electricity markets.

Form Energy's commercial utility contracts for iron-air battery systems capable of 100-hour discharge duration represent a milestone in LDES commercialisation that fundamentally validates the economic case for multi-day storage at utility scale using earth-abundant iron as the primary active material. These commercial contracts, combined with the IRA's investment tax credit making standalone LDES projects financially viable for the first time, are establishing the U.S. as the global LDES commercialisation leader and creating the first generation of operational LDES reference projects that will catalyse international commercial adoption through the 2026 to 2035 forecast period.

Long Duration Energy Storage Market Segment Insights

-

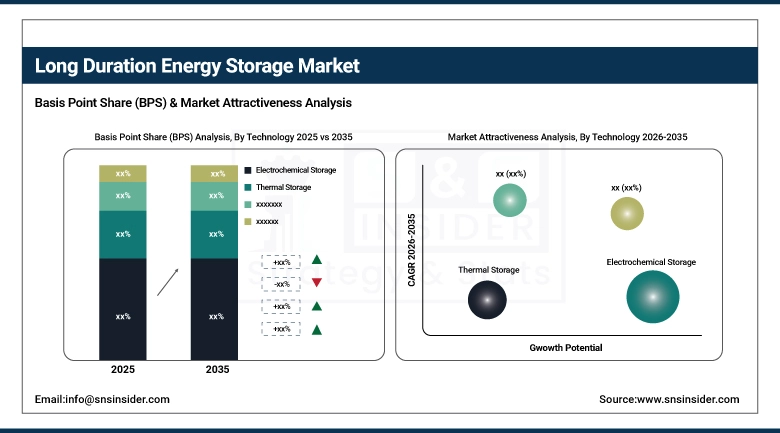

According to Technology, Electrochemical Storage dominated with approximately 59.88% market share in 2025 as battery-based systems including lithium-ion and flow batteries are the most commercially mature LDES technology category; Chemical Storage is the fastest-growing technology at a CAGR of approximately 14.26% driven by hydrogen-based energy storage and power-to-gas technology investment.

-

In terms of Duration, the 8 to 24 Hours segment holds the largest share of approximately 48.60% in 2025 as this duration range serves daily grid balancing, renewable energy smoothing, and peak load management needs that constitute the most immediate commercial LDES opportunity; the More than 36 Hours segment is the fastest-growing driven by multi-day renewable drought management requirements.

-

By Capacity, the More than 100 MW segment is the fastest-growing at a CAGR of approximately 17.54%, driven by rising grid-scale storage demand, renewable integration requirements, and large-capacity infrastructure investments that require utility-scale LDES deployments.

-

By Application, Grid Balancing and Renewable Energy Integration dominate as the largest application categories; Industrial Applications are among the fastest-growing as manufacturing electrification and data centre power security drive enterprise LDES demand.

-

By End-User, Utilities dominated with the largest revenue share in 2025 through grid-scale LDES procurement for renewable integration and grid stability; Commercial and Industrial is the fastest-growing end-user segment as corporate renewable energy commitments and power security requirements drive enterprise LDES investment.

Long Duration Energy Storage Market Segment Analysis

By Technology: Electrochemical Storage dominates, Chemical Storage grows fastest

Electrochemical Storage retained the dominant technology segment position in the Long Duration Energy Storage Market in 2025 with approximately 59.88% of global revenues, reflecting the commercial maturity and proven operational reliability of flow battery systems including vanadium redox, iron-flow, and zinc-bromine chemistries that provide the multi-hour discharge capability that defines LDES, combined with grid-scale lithium-ion installations at the shorter end of the LDES duration range.

Chemical Storage is projected to grow at the fastest technology segment CAGR of approximately 14.26% through 2035, driven by the expanding commercial investment in hydrogen-based energy storage including power-to-gas systems that convert surplus renewable electricity into green hydrogen through electrolysis, store hydrogen in compressed, liquid, or material-bound form, and regenerate electricity through fuel cells or hydrogen turbines when grid power is needed.

By Duration: 8 to 24 Hours dominates, More than 36 Hours grows fastest

The 8 to 24 Hours duration segment retained the dominant position with approximately 48.60% of the Long Duration Energy Storage Market in 2025, driven by its ability to serve the most immediate and commercially established LDES use case of daily grid balancing, where solar energy captured during mid-day peak generation periods is stored and discharged during evening demand peaks that extend beyond the 4-hour capability of short-duration storage.

The More than 36 Hours duration segment is the fastest-growing, driven by increasing penetration of renewable energy into national electricity grids that creates multi-day supply gaps when extended periods of low wind and solar generation coincide with high demand. California's and Germany's experience of multi-day renewable energy droughts that require dispatchable backup power beyond the capability of any short or medium duration storage system is establishing the policy and commercial case for ultra-long-duration storage that can sustain grid power delivery for 3 to 100 days.

By End-User: Utilities dominate, Commercial and Industrial grows fastest

Utilities retained the dominant end-user position in the Long Duration Energy Storage Market in 2025, reflecting their role as the primary buyers of grid-scale storage infrastructure that must balance renewable generation across the full demand profile of their service territories. Utility procurement of LDES is driven by renewable integration requirements encoded in state and national renewable portfolio standards, grid stability obligations mandated by electricity market regulators, and the commercial opportunity of arbitraging wholesale electricity price spreads between low-cost renewable generation periods and high-demand peak price periods.

Commercial and Industrial end-users are the fastest-growing segment through 2035, as large energy consumers including hyperscale data centres, industrial manufacturers, and commercial real estate operators increasingly invest in on-site LDES systems that provide power security, enable renewable energy self-sufficiency, and support virtual power plant participation through demand response programmes.

Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

75% |

|

Europe |

United Kingdom |

28% |

|

Asia Pacific |

China |

52% |

|

Middle East & Africa |

Saudi Arabia |

30% |

|

Latin America |

Brazil |

43% |

Asia Pacific Long Duration Energy Storage Market Insights

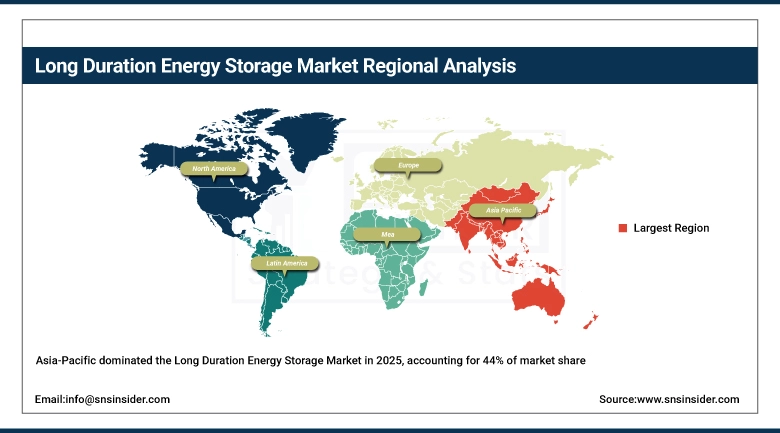

Asia Pacific dominated the global Long Duration Energy Storage Market in 2025 with the largest regional revenue share, driven by China's extraordinary renewable energy expansion that has created the world's most urgent LDES deployment imperative, with China alone accounting for approximately 73.76 GW of cumulative new energy storage capacity by end of 2024 representing over 40% of global total. China's national energy storage deployment targets, feed-in tariff support for grid-scale storage, and domestic manufacturing capability in flow battery, compressed air, and thermal storage technologies create a self-reinforcing commercial ecosystem that sustains Asia Pacific's regional LDES market leadership. Australia's world-leading renewable energy penetration creates the most commercially advanced LDES market outside China, with pumped hydro and grid-scale battery projects establishing the physical infrastructure that will anchor Australia's transition to a 90% renewable electricity system.

North America Long Duration Energy Storage Market Insights

North America is projected to grow at a strong CAGR through 2035, anchored by the United States' combination of IRA investment tax credits, DOE Long Duration Storage Shot programme support, and growing utility procurement commitments for commercial LDES deployments. The U.S. market benefits from the world's most active LDES startup ecosystem, with Form Energy, ESS Inc., Ambri, Highview Power, and Energy Vault collectively attracting hundreds of millions of dollars in venture and strategic investment that is driving rapid technology maturation and cost reduction. Canada contributes through its extensive pumped hydro resources and growing offshore wind development that requires LDES backup.

Europe Long Duration Energy Storage Market Insights

Europe represents a significant and rapidly growing LDES market, driven by the EU's ambitious renewable energy targets requiring 42.5% renewable electricity by 2030 and net-zero by 2050 that physically require LDES infrastructure investment to achieve without compromising grid reliability. The UK leads European LDES deployment through its Long Duration Energy Storage programme providing Contracts for Difference support for LDES projects, advanced offshore wind development creating storage demand, and the commercial operations of Highview Power in liquid air energy storage. Germany, France, and Scandinavia are significant LDES markets through offshore wind integration needs and seasonal storage requirements.

Middle East & Africa and Latin America Long Duration Energy Storage Market Insights

MEA and Latin America are growing LDES markets, driven by solar energy integration needs, energy access expansion, and renewable energy export ambitions. Saudi Arabia and the UAE are investing in LDES to support their ambitious solar and green hydrogen export programmes under Vision 2030 commitments. Brazil leads Latin American LDES revenues, anchored by its large hydropower base that faces increasing drought risk and the rapid expansion of wind and solar capacity that requires seasonal balancing storage as weather patterns become more variable.

Get Customized Report as per Your Business Requirement - Enquiry Now

Market Growth Drivers:

Deep renewable energy penetration creating multi-hour storage deficits that only LDES can economically resolve, combined with IRA and Green Deal policy investment that is de-risking commercial LDES deployment: The primary structural growth driver for the Long Duration Energy Storage Market is the physical grid reality that high-renewable electricity systems experience multi-hour and multi-day periods of insufficient generation that cannot be managed by short-duration storage, creating an irreversible LDES demand that grows in direct proportion to renewable energy penetration. The IRA's investment tax credit for standalone LDES projects, DOE's Long Duration Storage Shot programme targeting 90% cost reduction, and equivalent policy programmes across the EU, UK, Australia, and China are collectively providing the financial support structures that make LDES project development commercially viable at current technology costs, sustaining the commercial pipeline of LDES deployments through the forecast period while technology cost reduction progressively expands the market without subsidy dependence.

The U.S. DOE's Long Duration Storage Shot targeting USD 0.05/kWh storage cost by 2030 represents a 90% cost reduction from 2020 levels, and the combination of IRA investment tax credits, production tax credits for storage, and direct loan programmes from DOE's Loan Programs Office is creating the most favourable commercial environment for LDES investment in U.S. history.

Market Restraints

High upfront capital cost, technology immaturity at commercial scale, and limited offtake contract structures constraining project financing: A significant restraint on the Long Duration Energy Storage Market is the high capital cost of LDES systems relative to short-duration lithium-ion alternatives at current deployment volumes, where the per-kWh installed cost of most LDES technologies remains 3 to 5 times higher than mature lithium-ion systems, requiring revenue stacking across multiple grid services including capacity markets, frequency regulation, and energy arbitrage to achieve financially viable project returns. The technology immaturity of several LDES technology categories at commercial scale creates lender risk aversion that limits project debt financing and requires higher equity returns that compress developer economics. The absence of established long-term offtake contract structures for multi-day storage services in most electricity markets leaves LDES project developers dependent on merchant revenue exposure that conventional infrastructure project lenders regard as unacceptably uncertain for large capital commitments.

Market Opportunities

Iron-air and next-generation flow battery commercialisation, seasonal hydrogen storage development, and emerging market energy access LDES programmes: The commercialisation of iron-air batteries by Form Energy at dramatically lower material cost than vanadium or lithium alternatives represents the most transformative near-term LDES cost reduction opportunity, with iron's Earth-abundance and low commodity cost enabling structural cost reduction that could position 100-hour iron-air storage below USD 0.10/kWh at commercial scale. Seasonal hydrogen storage, where renewable electricity surplus during high-generation seasons is converted to green hydrogen for storage and winter power generation, represents the ultimate long-duration storage solution for northern hemisphere renewable energy systems and creates a multi-trillion-dollar market development opportunity as national green hydrogen strategies mature toward physical infrastructure deployment. Emerging market energy access applications, where LDES enables reliable electricity supply from solar and wind without expensive grid extension or diesel generation, represent a vast untapped LDES deployment opportunity across Sub-Saharan Africa, South Asia, and remote communities globally.

Recent Developments:

-

2025: Form Energy commenced delivery of its first commercial iron-air battery systems to utility customers under multi-year offtake agreements, marking the first commercial deployment of 100-hour iron-air LDES technology that uses earth-abundant iron as the primary active electrode material.

-

2025: ESS Inc. expanded its iron-flow battery commercial deployment programme across multiple U.S. and European utility customers, with new multi-MW installations providing 8 to 12 hours of storage duration for daily renewable energy balancing applications.

-

2025: Highview Power advanced development of its commercial liquid air energy storage facilities in the UK and Europe, with its 50 MW/250 MWh cryogenic energy storage plant in the UK representing the world's largest liquid air energy storage installation.

-

2024: The U.S. DOE awarded USD 325 million in grants under its Long Duration Energy Storage demonstration programme to support 15 LDES pilot projects spanning iron-air, flow battery, thermal, and compressed air technologies across diverse U.S. grid environments.

-

2025: Invinity Energy Systems expanded its vanadium flow battery manufacturing capacity and secured commercial contracts for grid-scale LDES systems in Europe and Asia Pacific, advancing the commercial scaling of vanadium redox flow technology toward utility-scale project economics.

Long Duration Energy Storage Market Key Players

-

Form Energy Inc.

-

ESS Tech Inc.

-

Highview Power

-

Energy Vault Holdings Inc.

-

Ambri Inc.

-

Invinity Energy Systems plc

-

Sumitomo Electric Industries Ltd.

-

EnerVault (now Avalon Battery)

-

CMBlu Energy AG

-

Malta Inc. (X/Alphabet)

-

GKN Hydrogen

-

VFlowTech Pte Ltd.

-

Primus Power Corporation

-

Eos Energy Enterprises Inc.

-

RheEnergise Ltd.

-

MAN Energy Solutions SE

-

Hydrostor Inc.

-

Quidnet Energy Inc.

-

Brenmiller Energy Ltd.

-

VoltStorage GmbH

Long Duration Energy Storage Market Report Scope

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 4.82 Billion |

| Market Size by 2035 | USD 17.22 Billion |

| CAGR | CAGR of 13.58% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology (Electrochemical Storage, Mechanical Storage, Thermal Storage, Chemical Storage) • By Duration (Less than 8 Hours, 8 to 24 Hours, 24 to 36 Hours, More than 36 Hours) • By Capacity (Less than 10 MW, 10 to 100 MW, More than 100 MW) • By Application (Grid Balancing, Renewable Energy Integration, Off-Grid Power, Industrial Applications, Others) • By End-User (Utilities, Commercial and Industrial, Residential, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Form Energy Inc.; ESS Tech Inc.; Highview Power; Energy Vault Holdings Inc.; Ambri Inc.; Invinity Energy Systems plc; Sumitomo Electric Industries Ltd.; EnerVault (now Avalon Battery); CMBlu Energy AG; Malta Inc. (X/Alphabet); GKN Hydrogen; VFlowTech Pte Ltd.; Primus Power Corporation; Eos Energy Enterprises Inc.; RheEnergise Ltd.; MAN Energy Solutions SE; Hydrostor Inc.; Quidnet Energy Inc.; Brenmiller Energy Ltd.; VoltStorage GmbH |

Frequently Asked Questions

Asia Pacific dominated the Long Duration Energy Storage Market in 2025 with the largest revenue share, anchored by China's extraordinary renewable energy expansion representing over 40% of global new energy storage capacity, combined with Australia's world-leading renewable penetration creating urgent commercial LDES deployment needs and Japan's grid-scale flow battery deployment programme.

The 8 to 24 Hours segment held the largest market share of approximately 48.60% in 2025.

Electrochemical Storage dominated the market in 2025 with approximately 59.88% of revenues.

The Long Duration Energy Storage Market was valued at USD 4.82 billion in 2025.

The Long Duration Energy Storage Market is expected to grow at a CAGR of 13.58% from 2026 to 2035.

Get in Touch