Logistics Software Market Report Scope & Overview:

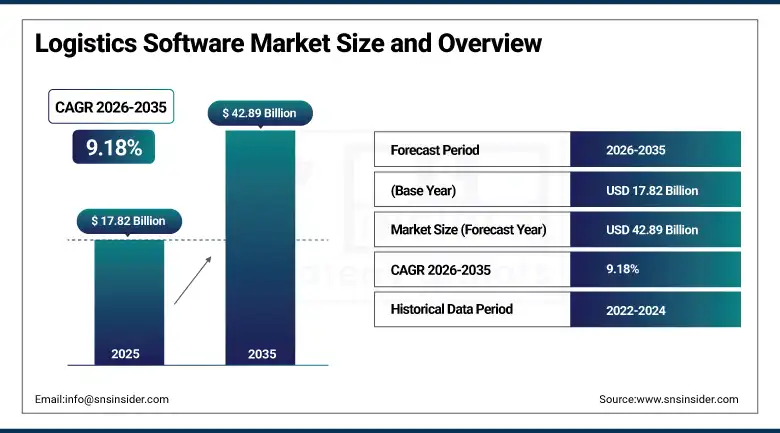

The Logistics Software Market is valued at USD 17.82 billion in 2025 and is expected to reach USD 42.89 billion by 2035, growing at a CAGR of 9.18% from 2026-2035.

The Logistics Software Market is growing owing to the high demand for visibility in the supply chain, transportation optimization, and improved warehousing management within various sectors. The growth in e-commerce transactions and increased global trade is spurring the adoption of better logistics software which enhances accuracy and efficiency. Companies are employing cloud technology, AI, predictive analytics, and automation in their logistics operations to achieve enhanced productivity. There is an increased adoption of technologies such as real-time tracking, inventory management, and fleet management systems which support the market's development.

According to the World Trade Organization (WTO), global merchandise trade exceeds USD 24 trillion annually, generating substantial demand for transportation management, freight tracking, and supply chain optimization software. The United Nations Conference on Trade and Development (UNCTAD) reports that global maritime trade surpasses 12 billion tons of cargo annually, underscoring the growing need for digital logistics coordination, port management, and shipment visibility solutions. In 2025, logistics software adoption surged as 78% of global operators leveraged cloud platforms and AI analytics enhancing supply chain visibility, cutting delivery errors by 32%, and streamlining cross-border operations amid booming e-commerce and omnichannel demands.

Market Size and Forecast

-

Market Size in 2026E: USD 19.46 Billion

-

Market Size by 2035: USD 42.89 Billion

-

CAGR: 9.18% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Logistics Software Market - Request Free Sample Report

Logistics Software Market Trends

-

Rising adoption of cloud-based logistics software for real-time tracking, inventory management, and supply chain optimization

-

Growing integration of AI and machine learning to enhance route planning, demand forecasting, and operational efficiency

-

Increasing use of IoT-enabled devices for fleet monitoring, cargo tracking, and predictive maintenance in logistics operations

-

Expansion of e-commerce and last-mile delivery services driving demand for advanced transportation management systems

-

Rising focus on sustainability and carbon footprint reduction through software-enabled route optimization and resource planning

The U.S. Logistics Software Market Outlook

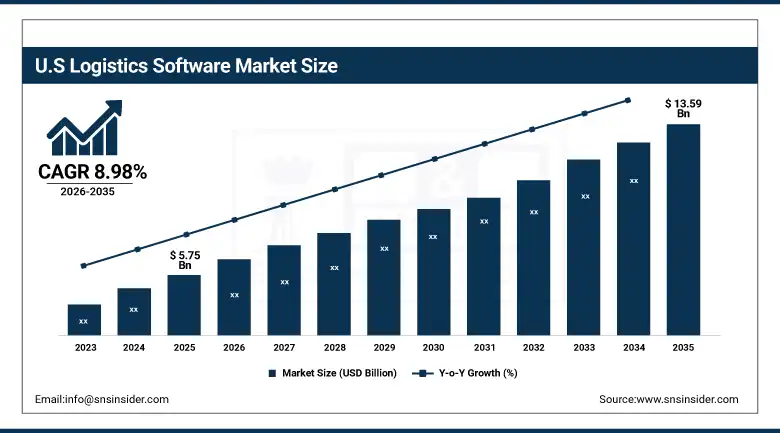

U.S. Logistics Software Market is valued at USD 5.75 billion in 2025 and is expected to reach USD 13.59 billion by 2035, growing at a CAGR of 8.98% from 2026-2035.

Expansion of the U.S. logistics software market is guided by increasing e-commerce growth, growing demand for real-time shipment visibility and efficient warehouse management & transportation. Cloud platform adoption, automation and artificial intelligence analytics mean companies reduce their cost and speed delivery as well as significantly improve supply chain operations.

The Bureau of Transportation Statistics (BTS) states that freight valued at more than USD 55 billion moves through the U.S. transportation network each day, highlighting the scale and complexity of logistics operations that rely on advanced software platforms for efficient supply chain management and real-time decision-making.

Logistics Software Market Segment Analysis

-

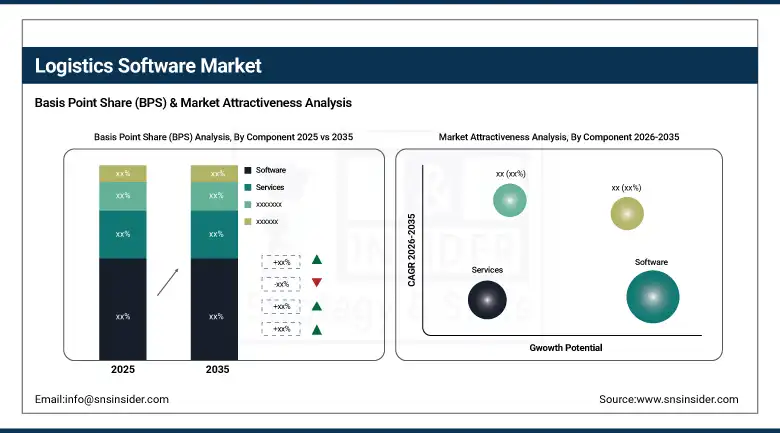

By Component, software segment dominated the logistics software market in 2025 with 42.5% share; services segment is the fastest growing segment with a cagr of 13.4%.

-

By Deployment Mode, cloud-based segment dominated the market in 2025 with 47.3% share; hybrid segment is the fastest growing segment with a cagr of 12.8%.

-

By Application, transportation management system segment dominated the market in 2025 with 38.9% share; fleet management system segment is the fastest growing segment with a cagr of 13.1%.

-

By End-User, retail and e-commerce segment dominated the market in 2025 with 36.7% share; healthcare segment is the fastest growing segment with a cagr of 12.9%.

By Component, software dominated the logistics software market, while services is the fastest-growing segment

Software dominated the Logistics Software Market owing to the crucial involvement in the management of various tasks such as transportation, warehousing, inventory management, order handling, and many others that come under logistics management. In recent years, the importance of logistics software applications has increased manifold in all kinds of businesses as they have realized the significance of using such software in their respective areas of operation.

The services segment is the fastest-growing segment, because there is an increasing demand for different kinds of professional services related to logistics software platforms. This includes implementation, integration, consultation, training, and maintenance of logistics software solutions. As more companies utilize customized and advanced logistics management software solutions, they will continue to look for professional help. It leads to the rapid development of the services segment.

By Deployment Mode, cloud-based deployment dominated the logistics software market, while hybrid deployment is the fastest-growing segment

Cloud-Based deployment dominated the Logistics Software Market due to flexibility, scalability, and cheaper implementation in contrast to on-premises options. Many companies prefer cloud-based logistics management software because it allows having greater real-time visibility and collaboration between all employees. In addition, deployment time is much shorter; it requires less effort as updates are automatically provided. The rising attention to digitalization and accessibility will favor the predominance of cloud-based deployments.

Hybrid deployment is the fastest-growing segment, owing to flexibility, security and operational management needs. With firms opting to leverage both cloud computing and on-premises software applications, there is growing popularity in the hybrid logistics software deployment to increase efficiency while still achieving compliance and protection measures of information. Firms can store their sensitive information in their own infrastructure while utilizing benefits from cloud computing for scalability and analytics. Demand for customization is fueling growth.

By Application, transportation management system (TMS) dominated the logistics software market, while fleet management system is the fastest-growing segment

Transportation Management System (TMS) dominated the Logistics Software Market due to its necessity in planning, implementing, and optimizing the freight process. Companies utilize TMS solutions for better route planning, reduction of costs associated with transportation, improved delivery process, and enhanced visibility throughout the supply chain. Increased demands for effective transportation management associated with the rapid development of international business and e-commerce activities are contributing to the dominance of the segment. Technological innovations that enable real-time tracking and analytics play a crucial part in maintaining the segment's market leadership.

Fleet Management System is the fastest-growing segment, owing to an increasing demand for vehicle tracking systems, fuel optimization solutions, driver monitoring systems, and efficiency improvements. Providers of logistics services become more interested in implementing innovative fleet management solutions in order to optimize their spending on transportation, improve asset utilization and ensure compliance with regulations.

By End-User, retail and e-commerce dominated the logistics software market, while healthcare is the fastest-growing segment

Retail and E-commerce dominated the Logistics Software Market due to the fast rise in online shopping and changing customer demands for speedier and more accurate deliveries. Logistics software is used in retail and e-commerce for various functions such as managing the company's inventory, optimizing transportation and warehousing activities, and improving order fulfillment efficiency. Rising omnichannel retail strategies and the popularity of cross-border e-commerce have boosted the segment demand. Investments in digitalizing the logistics operations continue to support its dominance.

Healthcare is the fastest-growing end-user segment, due to the rising need for effective management of medical supplies and pharmaceuticals, which require strict adherence to temperature conditions. By implementing logistics software, healthcare companies can increase the efficiency of inventory management, comply with all regulations related to handling sensitive products, and increase their supply chain transparency. Growing digitalization of the healthcare industry and the rising need for faster delivery of medical products are contributing to market development.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

84.73% |

|

Europe |

Germany |

28.47% |

|

Asia Pacific |

China |

38.47% |

|

Middle East & Africa |

UAE |

22.84% |

|

Latin America |

Brazil |

43.84% |

North America Logistics Software Market Insights

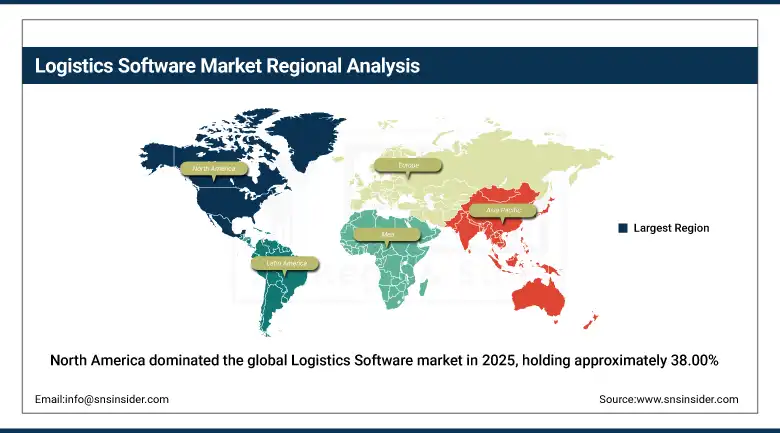

North America dominated the global Logistics Software market in 2025, holding approximately 38.00% of global revenues. The United States accounts for approximately 84.73% of regional revenue through its world-leading freight economy scale, the commercial concentration of major logistics software vendors, and the aggressive technology adoption of its retail, manufacturing, and logistics service provider sectors. The U.S. market's TMS adoption rate among mid-to-large enterprises exceeds 70%, the highest in any major economy, creating a well-penetrated market whose growth comes from platform replacement and capability upgrade cycles rather than greenfield adoption.

According to the U.S. Department of Transportation (DOT), the U.S. freight system moves more than 20 billion tons of goods annually, creating substantial demand for transportation planning, shipment visibility, and logistics optimization software. The U.S. Census Bureau reports that annual e-commerce sales exceed USD 1.1 trillion, increasing the need for warehouse management, order fulfillment, and last-mile delivery solutions.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Logistics Software Market Insights

Europe held a significant share of global Logistics Software revenues in 2025. Germany, France, the United Kingdom, and the Netherlands are the leading national markets, each hosting major logistics service provider headquarters and significant manufacturing and retail sectors whose supply chain digitalisation investment drives logistics software demand. The EU's Carbon Border Adjustment Mechanism and its growing freight decarbonisation regulatory framework are creating logistics software investment in emissions analytics and sustainable transport mode optimisation that is progressively becoming a distinct investment category whose commercial scale is growing with regulatory mandate expansion.

Germany accounts for approximately 28.47% of European revenues through its automotive export logistics, dense manufacturing supply chain, and the commercial presence of SAP and DHL whose logistics technology programmes define European market standards.

According to Eurostat, the European Union transports more than 13 billion tonnes of freight annually by road, highlighting the scale of logistics operations that require efficient transportation planning, route optimization, and freight management solutions.

Additionally, the European Union accounts for approximately 14–15% of global merchandise trade, generating substantial demand for logistics visibility, inventory management, and cross-border supply chain coordination systems. These factors continue to support the adoption of advanced logistics software across the region.

Asia Pacific Logistics Software Market Insights

Asia Pacific is the fastest-growing regional Logistics Software market, projected to expand at approximately 11.12% CAGR through 2035, driven by the world's largest e-commerce market in China, the rapid expansion of organised logistics infrastructure in India and Southeast Asia, and the growing adoption of cloud-based logistics platforms that are progressively replacing the manual and spreadsheet-based operations management that characterises smaller logistics operators across the region.

China accounts for approximately 38.47% of Asia Pacific revenues through the extraordinary scale of its e-commerce fulfilment logistics, the world's largest number of express parcel deliveries exceeding 150 billion annually, and the advanced logistics technology development of domestic platform companies including Cainiao, JD Logistics, and SF Express.

China's customs authority reports that the country's goods trade exceeds USD 6 trillion annually, highlighting the immense scale of freight movement and supply chain activities that require advanced logistics management and visibility solutions. These factors continue to strengthen Asia Pacific's position as the fastest-growing market for logistics software.

MEA & Latin America Logistics Software Market Insights

Middle East and Latin America are growing Logistics Software markets where expanding e-commerce activity, increasing foreign trade, and government infrastructure investment are creating growing logistics operational complexity that software platforms address. The UAE leads MEA revenues at approximately 22.84% of the regional total through its role as a regional logistics hub whose free zone infrastructure, air and sea freight gateway position, and growing e-commerce retail sector create substantial logistics software demand across both LSP and retail sectors.

Brazil leads Latin American revenues at approximately 43.84% of the regional total through its large retail and food and beverage sectors, the scale of its domestic freight market, and its growing e-commerce sector whose fulfilment complexity is creating rapid logistics technology adoption among both retailers and third-party logistics providers.

Market Dynamics

Growth Drivers: Rising demand for real-time shipment tracking, route optimization, and warehouse management solutions is driving adoption of logistics software across global supply chains

With increased focus on supply chain visibility, streamlined operations and lower transportation cost, companies are looking for even more solutions. Logistics: Software solves the challenges associated with tracking and planning, as well as warehouse management, to ensure efficient operations and accurate deliveries. Merchants are being pushed due to customer demands for transparent, faster deliveries. Integrate with ERP and IoT for predictive analytics and decision making. The combination of these factors is inducing the rapid roll-out of logistics software in numerous industries ranging from retail & e-commerce to manufacturing and 3PL providers around the world.

In 2025, 75% of global supply chain operators deployed logistics software for real-time tracking, dynamic route optimization, and smart warehouse management reducing transit times by 28% and improving inventory accuracy by over 35%.

Restraints: Integration challenges with legacy systems and lack of technical expertise hinder smooth deployment of logistics software, slowing market growth

Most businesses utilize out-of-date IT systems and equipment that are hard and expensive to integrate with new logistics software solutions. Compatibility issues, problems with moving data, and the lack of IT expertise may lead to delays in implementation, interruptions in operations, or misuses of software products. The lack of people who know how to work with advanced logistics systems is adding up to the problem. Such challenges make firms reluctant to purchase logistics software applications, particularly in developing countries. Thus, the difficulties with integration and expertise are significant barriers to entering a largely fragmented logistics software market environment.

In 2025, 65% of logistics companies faced delays in software deployment due to legacy system incompatibility and a shortage of skilled personnel slowing digital transformation and limiting ROI from advanced logistics platforms.

Opportunities: Growing adoption of cloud-based, AI-driven, and IoT-enabled logistics software provides opportunities to enhance operational efficiency and predictive decision-making

The internet of things, the cloud and artificial intelligence are driving massive changes in how products are shipped and how current and future supply chains are managed. The cloud lowers infrastructure costs and allows scalability, while AI supports predictive analytics for demand forecasting, route optimization and inventory management. IoT sensors and devices connected to the cloud deliver real-time visibility of shipments and warehouse operations. These are the kinds of advances that enable companies to save money and operate more effectively, and to base their practices on raw data. These technologies to create a wealth of new opportunities for logistics software companies to take these and use them as a basis for innovative solutions that will be attractive across many different industries.

In 2025, 70% of logistics firms adopted cloud-based, AI-driven, and IoT-enabled software improving route optimization by 35%, reducing delivery times by 28%, and enabling predictive analytics for inventory and demand planning.

Recent Developments:

-

2025: SAP expanded its Logistics Business Network with AI-powered carrier selection and rate negotiation, demonstrating average freight cost reduction of 14% for pilot customers through automated optimal carrier identification across cost, transit time, and reliability parameters.

-

2025: Project44 launched generative AI capabilities within its Advanced Visibility Platform enabling natural language freight data queries with 94% ETA prediction accuracy on a 24-hour horizon, establishing the platform as the market-leading supply chain visibility solution by network breadth and prediction accuracy.

-

2024: Blue Yonder released its Luminate Platform AI enhancements including autonomous demand sensing, inventory optimization, and transportation execution capabilities whose integrated AI-driven supply chain management reduced forecast error by an average of 22% and improved on-time delivery rates by 15 percentage points in documented customer deployments.

Logistics Software Market Key Players are:

-

SAP SE

-

Manhattan Associates

-

BluJay Solutions

-

Descartes Systems Group

-

WiseTech Global

-

Blue Yonder Group

-

Samsara Inc.

-

Ramco Systems

-

PTV Group

-

Alpega TMS

-

Magaya Supply Chain

-

LogiNext Mile

-

HighJump (Körber)

-

Infor

-

3GTMS

-

Kinaxis Inc.

-

Epicor Software Corporation

-

JDA Software (Blue Yonder)

Logistics Software Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 17.82 Billion |

| Market Size by 2035 | USD 42.89 Billion |

| CAGR | CAGR of 9.18% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Software, Services,) • By Deployment Mode (Cloud-Based, On-Premises, Hybrid) • By Application (Transportation Management System, Warehouse Management System, Supply Chain Planning, Fleet Management System, Freight Management System, Others (Order Management System, etc.)) • By End-User (Oil and Gas, Automotive, Healthcare, IT and Telecom, Retail and E-commerce, Manufacturing, Government, Others (Aerospace and Defense, etc.)) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | SAP SE, Oracle Corporation, Manhattan Associates, BluJay Solutions, Descartes Systems Group, WiseTech Global, Blue Yonder Group, Samsara Inc., Ramco Systems, PTV Group, 4flow, Alpega TMS, Magaya Supply Chain, LogiNext Mile, HighJump (Körber), Infor, 3GTMS, Kinaxis Inc., Epicor Software Corporation, JDA Software |

Frequently Asked Questions

The Logistics Software Market is expected to grow at a CAGR of 9.18% from 2026 to 2035.

The Logistics Software Market was valued at USD 17.82 Billion in 2025.

E-commerce expansion, supply chain digitization, AI-driven optimization, cloud platform adoption, and last-mile delivery innovation are accelerating logistics software demand.

The transportation management system segment dominated the Logistics Software Market with 38.9% share in 2025.

North America dominated the Logistics Software Market in 2025, holding approximately 38.00% of global revenues.

Get in Touch