Low Sodium Refining Agent Market Report Scope & Overview:

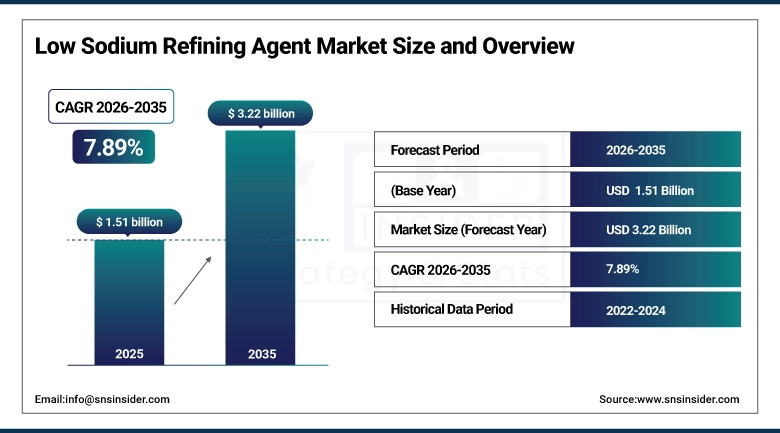

The Low Sodium Refining Agent Market was valued at USD 1.51 Billion in 2025 and is expected to reach USD 3.22 Billion by 2035, growing at a CAGR 7.89% of from 2026-2035.

The Low Sodium Refining Agent Market includes specialized fluxes and refining additives with reduced sodium content, widely used in steel, aluminum, and foundry operations to improve metal purity and process performance. Market growth is driven by increasing global steel and aluminum production, stricter environmental and low-alkali regulations, rising adoption of advanced ladle metallurgy practices, reduced slag formation, improved inclusion removal efficiency, and the need to extend refractory life while maintaining consistent product quality.

Market Size and Forecast:

-

Market Size in 2025: USD 1.51 Billion

-

Market Size by 2035: USD 3.22 Billion

-

CAGR: 7.89%

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Low Sodium Refining Agent Market - Request Free Sample Report

Trends in the Low Sodium Refining Agent Market

-

Rising adoption of low-alkali refining formulations to meet stricter environmental regulations

-

Growing use of synthetic and customized refining agents for improved metal purity

-

Increased deployment in secondary and ladle metallurgy operations

-

Focus on slag reduction and refractory life extension to lower operational costs

U.S. Low Sodium Refining Agent Market Size Outlook:

The U.S. Low Sodium Refining Agent Market is projected to grow from USD 0.22 Billion in 2025 to USD 0.43 Billion by 2035, at a CAGR of 5.41%. Growth is driven by demand for high-purity steel and aluminum, stricter environmental regulations, advanced ladle metallurgy adoption, plant modernization, and the need to improve refining efficiency while reducing slag and refractory wear.

Low Sodium Refining Agent Market Growth Drivers:

-

Expansion of Automotive, Construction, and Infrastructure Activities

Growth in automotive, construction, and infrastructure sectors is a major driver of the Low Sodium Refining Agent Market. Construction and infrastructure projects represent a significant share of global steel consumption, while automotive manufacturing remains a key consumer of high-quality steel and aluminum. Increasing urbanization, transportation projects, and vehicle production are raising demand for refined metals, encouraging greater adoption of low sodium refining agents to enhance material performance, reduce impurities, and comply with evolving quality and environmental requirements.

Low Sodium Refining Agent Market Restraints:

-

Limited Awareness and Technical Expertise in Refining Operations

Limited awareness and insufficient technical expertise act as key restraints in the Low Sodium Refining Agent Market. Many steel and foundry operators lack in-depth understanding of low sodium formulations, optimal dosing, and process compatibility. Improper selection or integration can reduce refining efficiency, increase costs, or affect metal quality. Smaller facilities, in particular, face challenges in training personnel and upgrading processes, slowing adoption despite the long-term operational and environmental benefits offered by low sodium refining agents.

Low Sodium Refining Agent Market Opportunities:

-

Rising Adoption of Sustainable and High-Efficiency Metallurgical Solutions

The Low Sodium Refining Agent Market presents strong opportunities driven by the global shift toward sustainable and high-efficiency metal production. Increasing focus on green steel initiatives, emission reduction, and energy-efficient refining processes is encouraging manufacturers to adopt low-alkali refining agents. Growing investments in advanced ladle metallurgy, expansion of aluminum applications in electric vehicles and renewable energy, and rising demand for high-purity metals create significant opportunities for innovation, customized formulations, and long-term supplier partnerships across global metallurgical industries.

Low Sodium Refining Agent Market Segment:

-

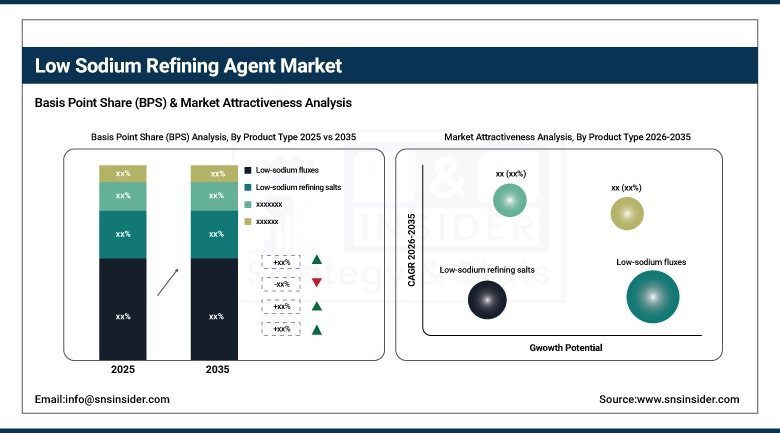

By Product Type: In 2025, Low-sodium fluxes dominated with 49% share; Synthetic refining agents fastest growing segment during 2026-2035

-

By Metal Type: In 2025, Steel dominated with 64% share; Aluminum fastest growing segment during 2026-2035

-

By Application: In 2025, Inclusion removal dominated with 37% share; Slag conditioning fastest growing segment during 2026-2035

-

By End-Use Industry: In 2025, Iron & steel manufacturing dominated with 59% share; Automotive & industrial manufacturing fastest growing segment during 2026-2035

By Product Type: Low-Sodium Fluxes Dominate as Synthetic Refining Agents Emerge as Fastest-Growing

Low-sodium fluxes dominate the product type segment due to their widespread use in steel and aluminum refining for effective inclusion removal and slag control. Their cost efficiency and compatibility with existing processes support high adoption.

Synthetic refining agents represent the fastest-growing segment, driven by demand for precise chemistry control, improved refining efficiency, and compliance with low-alkali environmental standards.

By Metal Type: Steel Leads While Aluminum Records Strong Growth

Steel dominates the metal type segment as low sodium refining agents are widely used in deoxidation, desulfurization, and ladle metallurgy across large-scale steel plants. Continuous global steel production, infrastructure development, and automotive demand support dominance.

Aluminum is the fastest-growing segment as automakers increasingly replace steel with lightweight aluminum to improve fuel efficiency and electric vehicle range. Rising demand for high-purity aluminum in battery enclosures, structural components, and renewable energy applications further accelerates adoption of low sodium refining agents.

By Application: Inclusion Removal Dominates as Slag Conditioning Expands

Inclusion removal dominates the application segment as manufacturers prioritize improved metal cleanliness, mechanical properties, and product consistency. Low sodium refining agents help reduce non-metallic inclusions without increasing alkali levels.

Slag conditioning is the fastest-growing application, supported by rising demand for improved slag fluidity, reduced metal loss, lower energy consumption, and extended refractory life in refining operations.

By End-Use Industry: Iron & Steel Manufacturing Leads While Automotive Grows Fast

Iron and steel manufacturing dominates the end-use industry segment due to continuous demand for refined steel in construction, infrastructure, and industrial applications. High-volume production and strict quality requirements drive adoption of low sodium refining agents.

Automotive and industrial manufacturing is the fastest-growing segment, supported by increasing vehicle production, demand for high-strength alloys, and precision metal components.

Regional Analysis:

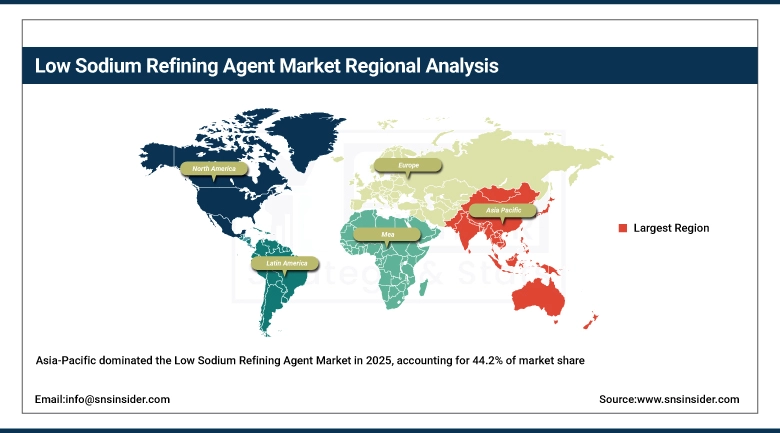

Asia-Pacific Low Sodium Refining Agent Market Insights:

In 2025, Asia-Pacific holds the largest market share of approximately 44.2%, making it both the dominant and fastest-growing region in the Low Sodium Refining Agent market, with an expected CAGR of 8.94% during 2026-2035. Growth is driven by expanding steel and aluminum production in China, India, and Southeast Asia, supported by large-scale infrastructure and construction projects. Rising automotive manufacturing, increased adoption of advanced ladle metallurgy, stricter environmental regulations, and growing demand for high-purity metals further accelerate regional market expansion.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Low Sodium Refining Agent Market Insights:

North America represents a mature and technologically advanced market for low sodium refining agents, supported by strong steel and aluminum production capabilities. Growth is driven by stringent environmental regulations, widespread adoption of advanced ladle metallurgy practices, and continuous modernization of metallurgical facilities. Demand remains steady from automotive, aerospace, and industrial manufacturing sectors requiring high-purity metals and improved refining efficiency.

Europe Low Sodium Refining Agent Market Insights:

Europe is a well-established market for low sodium refining agents, driven by strict environmental and low-alkali regulations across the steel and aluminum industries. The region emphasizes sustainable metallurgy, green steel initiatives, and advanced refining technologies to improve metal purity and reduce emissions. Continuous investment in process optimization, recycling-based metal production, and high-quality automotive and industrial manufacturing supports steady demand for low sodium refining agents.

Latin America Low Sodium Refining Agent Market Insights:

Latin America is an emerging market for low sodium refining agents, supported by growing steel and aluminum production and increasing industrial activity. Investment in infrastructure development, mining, and construction drives demand for refined metals. Gradual adoption of advanced metallurgical processes, along with improving environmental standards and modernization of foundry operations, is encouraging the use of low sodium refining agents across the region.

Middle East & Africa Low Sodium Refining Agent Market Insights:

The Middle East & Africa market is developing steadily, driven by expanding steel production, infrastructure investments, and industrial diversification initiatives. Growth is supported by increasing adoption of modern metallurgical practices, rising demand for high-quality construction steel, and gradual alignment with environmental and operational efficiency standards. Ongoing investments in industrial facilities and regional manufacturing capacity continue to create opportunities for low sodium refining agent adoption.

Competitive Landscape:

BASF SE, headquartered in Ludwigshafen, Germany, is a leading player in the low sodium refining agent market through its advanced chemical solutions for steel and aluminum refining. The company focuses on low-alkali fluxes and synthetic refining additives that enhance metal purity, improve slag control, and support sustainable metallurgical operations across global steel and foundry industries.

-

In March 2025: BASF expanded its low-sodium metallurgical additives portfolio to support improved inclusion removal and reduced refractory wear in secondary steel refining.

Albemarle Corporation, headquartered in Charlotte, North Carolina, is a prominent supplier of specialty chemicals used in low sodium refining agents for metallurgical applications. The company leverages its expertise in performance materials to deliver refining salts and flux solutions that enable efficient deoxidation and desulfurization in steel and aluminum processing.

-

In February 2025: Albemarle announced process optimization initiatives to enhance low-alkali refining formulations for aluminum smelting applications.

Solvay S.A., headquartered in Brussels, Belgium, plays a key role in the low sodium refining agent market through its advanced specialty chemicals used in steel and non-ferrous metal refining. The company emphasizes sustainable, low-alkali formulations that improve metal cleanliness while meeting stringent environmental and emission standards.

-

In January 2025: Solvay introduced upgraded low-sodium refining solutions designed to reduce slag volume and improve refining efficiency in ladle metallurgy operations.

Low Sodium Refining Agent Market Key Players:

-

BASF SE

-

Albemarle Corporation

-

Solvay S.A.

-

Clariant AG

-

LANXESS AG

-

Arkema S.A.

-

Imerys S.A.

-

Ferroglobe PLC

-

Haldor Topsoe A/S

-

Nouryon

-

Kuraray Co., Ltd.

-

Mitsubishi Chemical Group

-

Kobe Steel Chemicals

-

POSCO Chemical

-

Tata Chemicals Limited

-

Linde plc

-

RHI Magnesita

-

Foseco (Vesuvius plc)

-

Sibelco

-

Omya AG

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.51 Billion |

| Market Size by 2035 | USD 3.22 Billion |

| CAGR | CAGR of 7.89% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type: (Low-sodium fluxes, Low-sodium refining salts, Synthetic refining agents) • By Metal Type: (Steel, Aluminum, Copper & other non-ferrous metals) • By Application: (Deoxidation, Desulfurization, Inclusion removal, Slag conditioning) • By End-Use Industry: (Iron & steel manufacturing, Aluminum smelting & casting, Foundries, Automotive & industrial manufacturing) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | BASF SE, Albemarle Corporation, Solvay S.A., Clariant AG, LANXESS AG, Arkema S.A., Imerys S.A., Ferroglobe PLC, Haldor Topsoe A/S, Nouryon, Kuraray Co., Ltd., Mitsubishi Chemical Group, Kobe Steel Chemicals, POSCO Chemical, Tata Chemicals Limited, Linde plc, RHI Magnesita, Foseco (Vesuvius plc), Sibelco, Omya AG |

Frequently Asked Questions

Asia-Pacific dominated the Low Sodium Refining Agent market in 2025.

The “Steel” segment dominated during the projected period.

The key drivers of the Low Sodium Refining Agents market include rising demand for high-purity steel and aluminum, strict low-alkali regulations, advanced ladle metallurgy adoption, reduced slag generation, and extended refractory life requirements.

The market was valued at USD 1.51 Billion in 2025 and is projected to reach USD 3.22 Billion by 2035.

The Low Sodium Refining Agent market is expected to grow at a CAGR of 7.89% during 2026–2035.

Get in Touch