Magnesium Metal Market Report Scope & Overview:

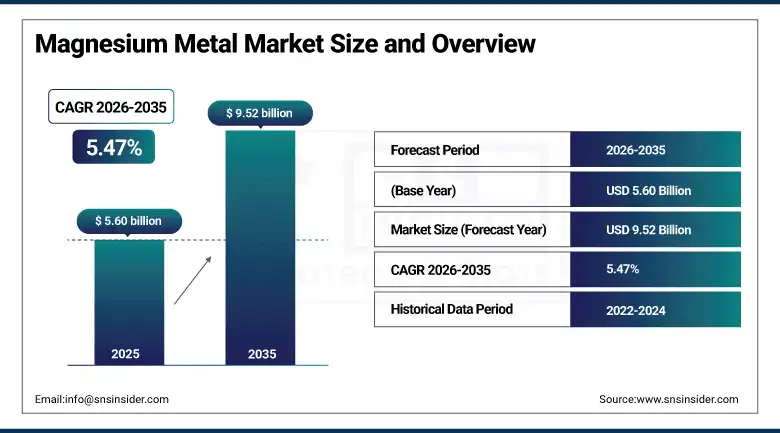

The Magnesium Metal Market was valued at USD 5.60 Billion in 2025 and is expected to reach USD 9.52 Billion by 2035, growing at a CAGR of 5.47% from 2026–2035.

The global magnesium metal market is advancing at a commercially reliable pace driven by the automotive industry’s escalating lightweighting investment, the aerospace sector’s growing adoption of magnesium alloy structural and interior components, and the electronics industry’s demand for the lightest structural metal commercially available for chassis, housing, and heat dissipation applications. Magnesium is approximately 36% lighter than aluminium and 78% lighter than steel while delivering competitive strength-to-weight ratios that make it the material of choice for weight-critical applications where dimensional constraints prohibit further thinning of alternative materials.

In April 2025, the International Magnesium Association and the China Magnesium Association formalised collaboration on global magnesium supply chain transparency and sustainability standards, recognising that China produces approximately 87% of global magnesium supply and that coordinated governance of production quality, environmental standards, and trade practices is essential for the market’s long-term credibility with automotive and aerospace OEM customers who are progressively applying material supply chain sustainability criteria to their procurement specifications.

Market Size and Forecast

-

Market Size in 2026E: USD 5.91 Billion

-

Market Size by 2035: USD 9.52 Billion

-

CAGR: 5.47% from 2026 to 2035

-

Fastest Growing Region: North America

-

Largest Region: Asia Pacific

To Get more information On Magnesium Metal Market - Request Free Sample Report

Magnesium Metal Market Trends

-

Rising automotive EV platform lightweighting investment is accelerating magnesium alloy adoption in battery enclosures, crossmembers, door inners, and seat structures.

-

Growing aerospace adoption of magnesium alloys in aircraft interior structures, engine housings, and gearbox casings is driven by the aviation sector’s relentless weight reduction imperatives.

-

Increasing investment in corrosion-resistant magnesium alloy development and surface treatment technologies is expanding the viable application range for magnesium.

-

Rising development of high-purity magnesium through electrolytic process advancement is creating new application opportunities in pharmaceutical, nuclear, and advanced electronics sectors.

-

Growing magnesium recycling infrastructure investment is improving the secondary magnesium supply chain’s commercial viability as scrap recovery from automotive and electronics end-of-life streams.

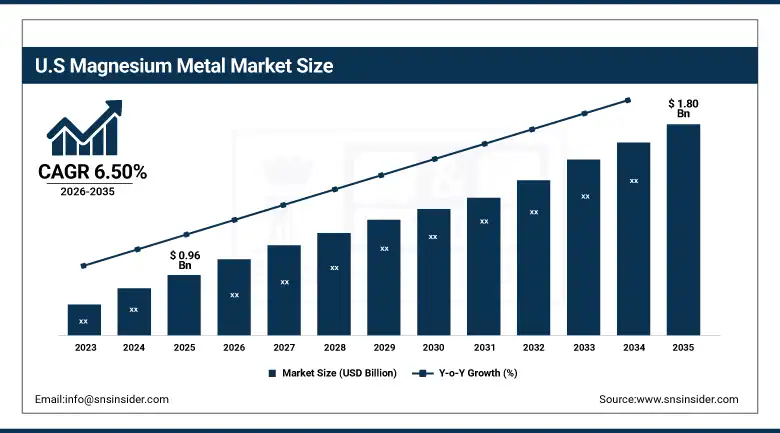

U.S. Magnesium Metal Market Outlook

The U.S. magnesium metal market was valued at approximately USD 0.96 Billion in 2025 and is expected to reach approximately USD 1.80 Billion by 2035, growing at a CAGR of approximately 6.50%.

Demand in the U.S. market is driven by the automotive industry’s lightweighting investment, aerospace and defence sector’s structural component requirements. The growing electronics sector’s demand for magnesium alloy housings and chassis components whose thermal and weight characteristics outperform competing materials. US Magnesium LLC, operating the only primary magnesium production facility in the United States from its Great Salt Lake brine extraction process, serves domestic automotive and industrial customers with domestic-origin magnesium whose supply chain security advantages are particularly commercially significant given the U.S. automotive and defence sectors’ growing strategic material sourcing requirements.

Western Magnesium Corp advanced its commercial-scale electrolytic magnesium production development in Canada in 2025, targeting the North American automotive lightweighting market with domestically produced primary magnesium that addresses OEM supply chain security concerns. The project’s progress reflects the growing commercial and strategic motivation to develop North American magnesium production capacity independent of Chinese supply chain concentration that currently creates raw material availability risk for automotive and aerospace OEM programmes.

Magnesium Metal Market Segment Analysis

-

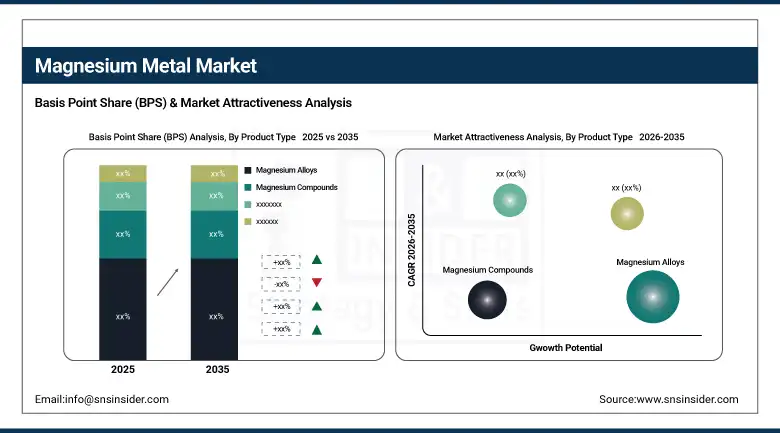

By Product Type, the Magnesium Alloys segment dominated the Magnesium Metal Market with 46.80% share in 2025, while the Magnesium Compounds segment is the fastest growing with a CAGR of 7.20%.

-

By Production Process, the Thermal Reduction Process segment dominated the Magnesium Metal Market with 49.12% share in 2025, while the Electrolytic Process segment is the fastest growing with a CAGR of 6.90%.

-

By Form, the Ingots segment dominated the Magnesium Metal Market with 38.60% share in 2025, while the Sheets & Plates segment is the fastest growing with a CAGR of 6.70%.

By Product Type, alloys dominate, compounds grow fastest

Magnesium alloys retained the dominant product type position with 46.80% of the magnesium metal market in 2025. Their commercial primacy reflects the practical commercial reality that pure magnesium’s mechanical properties, while impressive in weight terms, require alloying with aluminium, zinc, manganese, or rare earth elements to achieve the strength, ductility, creep resistance, and corrosion performance that engineering application requirements impose. AZ-series alloys containing aluminium and zinc dominate automotive die casting applications through their combination of good castability, strength, and commercial availability. AM-series alloys provide improved ductility for crash-sensitive automotive structural applications.

Magnesium compounds are the fastest-growing product type at a CAGR of 7.20% because the category’s commercial applications span multiple high-growth industries simultaneously. Magnesium oxide serves as a flame retardant in construction materials, cables, and electronics whose fire safety regulation tightening creates growing demand. Magnesium hydroxide functions as a non-halogenated flame retardant whose environmental profile advantages over bromine-based alternatives are creating regulatory and commercial substitution motivation. Magnesium sulphate serves agricultural, pharmaceutical, and industrial chemical applications whose diverse demand creates a resilient commercial base independent of any single sector’s investment cycle variation.

By Form, ingots dominate, sheets & plates grow fastest

Ingots retained the dominant form position with 38.60% of the magnesium metal market in 2025. Their commercial primacy reflects the role of magnesium ingots as the universal feedstock form that enables downstream processing flexibility across the broadest range of end applications. Die casting operations that produce automotive and electronics components require magnesium ingots as their primary input material, whose melting and injection into permanent moulds creates the complex geometries that automotive structural and bracket components demand at the production volumes and dimensional consistency that OEM assembly programmes require.

Sheets and plates are the fastest-growing form at a CAGR of 6.70% because the automotive and aerospace industries’ expanding adoption of wrought magnesium in stamped and formed structural components creates growing demand for flat-rolled magnesium products whose mechanical properties, achieved through hot rolling and thermomechanical processing, substantially exceed die cast magnesium in tensile strength, ductility, and fatigue performance.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

28.4% |

|

Asia Pacific |

China |

76.3% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

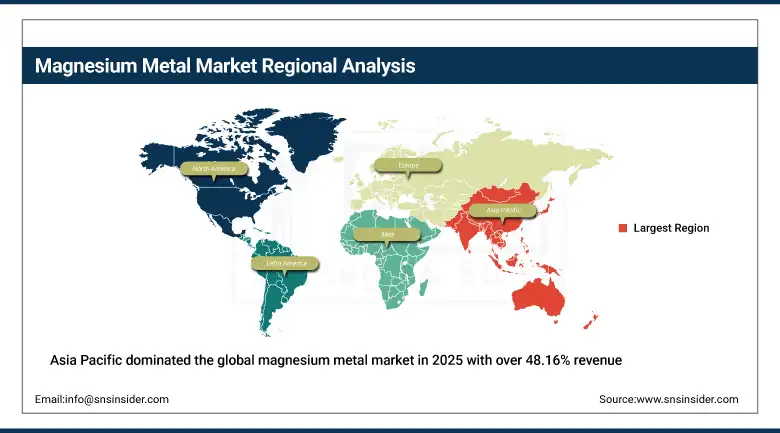

Asia Pacific Magnesium Metal Market Insights

Asia Pacific dominated the global magnesium metal market in 2025 with over 48.16% revenue share, driven by China’s extraordinary position as the source of approximately 87% of global primary magnesium production whose production scale, concentrated in Shanxi Province’s dolomite-rich geological environment, creates the commercial foundation upon which the global magnesium supply chain is built.

China accounts for approximately 76.3% of Asia Pacific revenues through its combination of massive primary production capacity, a large and growing domestic automotive and electronics industry that creates domestic consumption alongside export volume, and a downstream magnesium alloy processing industry whose die casting and alloying operations serve both domestic OEM customers and international material supply contracts.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Magnesium Metal Market Insights

North America is the fastest-growing regional magnesium metal market at a CAGR of 6.54%, driven by increasing automotive lightweighting investment, growing aerospace and defence magnesium alloy adoption, and the strategic motivation to develop domestic North American magnesium production capacity that reduces dependence on Chinese import supply.

Canada’s Western Magnesium Corp development programme and the broader North American strategy of leveraging domestic dolomite resources and electrolytic production technology to establish a supply chain-secure magnesium production base reflect the growing political and commercial motivation to treat magnesium as a critical mineral whose domestic production capability is strategically essential for automotive electrification and defence industrial base programmes.

Europe Magnesium Metal Market Insights

Europe is a technically sophisticated magnesium metal market where the automotive industry’s weight reduction imperative, the aerospace sector’s component lightweighting investment, and the supply chain security motivation to develop non-Chinese magnesium supply sources are collectively creating structured demand and supply diversification investment.

Germany accounts for approximately 28.4% of European revenues as the region’s largest market through its concentration of automotive OEM and Tier-1 supplier operations whose magnesium alloy die casting and structural component programmes represent the most technically demanding European end-use applications.

MEA & Latin America Magnesium Metal Market Insights

The Middle East and Africa and Latin America are growing magnesium metal markets where expanding automotive manufacturing, construction industry demand for magnesium compounds in building materials, and the healthcare sector’s pharmaceutical magnesium compound requirements are creating structured procurement.

Saudi Arabia leads MEA revenues at approximately 31.2% of the regional total through its automotive assembly sector’s magnesium alloy component procurement and the construction industry’s demand for magnesium oxide-based flame retardant and building material products whose fire safety performance requirements create consistent institutional demand.

Brazil leads Latin American revenues at approximately 44.2% of the regional total through its large automotive manufacturing sector, including significant Tier-1 die casting operations serving both domestic OEM assembly and export markets, and the agricultural sector’s demand for magnesium sulphate fertilisers and soil amendment products whose commercial scale in Brazilian intensive crop production creates consistent procurement volumes.

Market Dynamics

Growth Drivers: Automotive EV lightweighting investment creating structural component demand, and regulatory CO2 emission standards creating compliance-driven material substitution motivation

The EV industry’s lightweighting imperative is the magnesium market’s most commercially significant near-term growth driver. Electric vehicle range extension is directly proportional to vehicle mass reduction at constant battery capacity, creating a quantifiable kilogram-to-kilometre economic return on lightweight material investment that automotive engineers can calculate precisely and present to programme investment decision-makers. Magnesium alloys deliver the highest mass reduction per cubic centimetre of replaced steel or aluminium of any commercially available structural metal, positioning them as the technically optimal material for EV applications where maximum weight reduction is achievable within current manufacturing and corrosion protection technology constraints.

Aerospace sector adoption is creating a high-value commercial growth pathway that is strategically complementary to the automotive sector’s commodity-volume demand. Aircraft programme decisions to incorporate magnesium alloys in gearbox housings, auxiliary power unit cases, seat structures, and interior ceiling panels create per-kilogram commercial value many times higher than automotive die casting applications, sustaining premium material development investment whose technological benefits progressively migrate into the automotive market as manufacturing maturity improves and costs decline.

Restraints: China’s near-monopoly supply creating geopolitical risk and price control vulnerability and corrosion susceptibility limiting unprotected application environments

China’s approximately 87% share of global primary magnesium production creates the most commercially significant single-country supply concentration risk of any major structural metal in global industrial supply chains. The 2021 European energy crisis that temporarily reduced Chinese magnesium production created a global supply shock whose price impact demonstrated the market’s vulnerability to Chinese production policy, energy cost, and regulatory decisions that importing countries cannot influence or predict. This supply concentration risk is motivating automotive OEM procurement teams to require supply diversification from their magnesium material suppliers and is creating policy motivation for domestic production investment in North America, Europe, and Australia.

Magnesium’s propensity for ignition during machining, grinding, and cutting operations creates workplace safety requirements that add operational cost and complexity to magnesium alloy component manufacturing relative to aluminium and steel alternatives. While established safety protocols effectively manage ignition risk in well-managed manufacturing environments, the additional training, equipment, and operational discipline requirements create adoption barriers for manufacturers whose experience with magnesium alloy processing is limited and whose investment in safety infrastructure must precede the operational benefits of magnesium component production.

Opportunities: Non-Chinese primary production capacity development and biodegradable magnesium in medical implant applications

Non-Chinese primary magnesium production capacity development represents the most commercially significant structural opportunity in the magnesium metal market for North American and European producers, as the automotive and aerospace industries’ supply chain security motivation creates a premium procurement environment for geographically diversified magnesium supply. Western Magnesium’s electrolytic process, Alliance Magnesium’s Quebec silicothermic technology, and Australian brine-source projects each represent supply diversification investments whose commercial timing aligns with the automotive electrification wave’s growing demand for domestic-origin critical materials.

Biodegradable magnesium alloy medical implants represent a high-value niche application whose commercial development creates premium demand for ultra-high-purity magnesium grades. Bioresorbable bone fixation screws, vascular stents, and orthopaedic implants manufactured from biocompatible magnesium alloys provide temporary mechanical support that degrades safely within the body as natural healing progresses, eliminating the secondary surgery for implant removal that titanium and stainless-steel alternatives require. Each new biodegradable implant commercial approval creates structured demand for the pharmaceutical-grade magnesium alloy material whose production requirements are substantially more demanding than automotive die casting grades.

Recent Developments:

-

2025: The International Magnesium Association and the China Magnesium Association formalised collaboration in April 2025 on global magnesium supply chain transparency and sustainability standards, recognising the commercial necessity of coordinated governance for production quality and environmental practices given China’s approximately 87% share of global primary magnesium supply.

-

2025: Western Magnesium Corp advanced its commercial-scale electrolytic magnesium production development programme in Canada in 2025, targeting the North American automotive and aerospace markets with domestically produced primary magnesium whose supply chain security credentials address OEM strategic sourcing requirements independent of Chinese supply chain availability.

-

2024: AMG Advanced Metallurgical Group expanded its magnesium alloy processing capacity in Europe in 2024 to serve growing automotive lightweighting demand, adding new alloy development capabilities for EV-specific structural applications and investing in corrosion-resistant surface treatment infrastructure that expands magnesium alloy’s viable application range into previously constrained automotive exterior environments.

Magnesium Metal Market Key Players

-

China Magnesium Corporation

-

US Magnesium LLC

-

Magontec Limited

-

RIMA Group

-

Dead Sea Magnesium

-

AMG Advanced Metallurgical Group

-

Henan Jingu Magnesium Industry

-

Jiangsu Yongxiang Magnesium

-

SeAH Magnesium

-

Western Magnesium Corp

-

Nova Magnesium

-

Valdi Magnesium

-

Shandong Yuyuan Industrial

-

Eastern Magnesium Corp

-

Alliance Magnesium

Magnesium Metal Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 5.60 Billion |

| Market Size by 2035 | USD 9.52 Billion |

| CAGR | CAGR of 5.47% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Magnesium Alloys, Magnesium Compounds, Pure Magnesium) • By Production Process (Thermal Reduction Process, Electrolytic Process) • By Form (Ingots, Sheets & Plates, Rods & Bars, Powders & Granules, Others) • By End Use (Automotive, Aerospace & Defence, Electronics, Construction, Healthcare, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | China Magnesium Corporation, US Magnesium LLC, Magontec Limited, RIMA Group, Dead Sea Magnesium, AMG Advanced Metallurgical Group, Henan Jingu Magnesium Industry, Jiangsu Yongxiang Magnesium, SeAH Magnesium, Western Magnesium Corp, Nova Magnesium, Valdi Magnesium, Shandong Yuyuan Industrial, Eastern Magnesium Corp, Alliance Magnesium |

Frequently Asked Questions

Get in Touch