Master Data Management Market Report Scope & Overview:

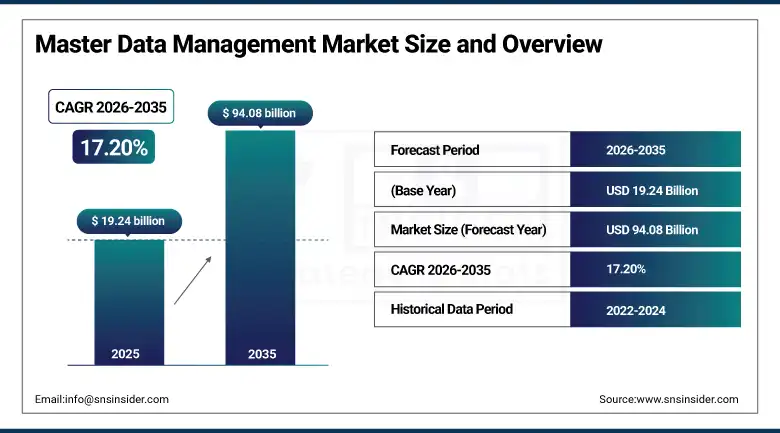

The Master Data Management Market was valued at USD 19.24 Billion in 2025 and is expected to reach USD 94.08 Billion by 2035, growing at a CAGR of 17.20% from 2026 to 2035.

The Master Data Management Market is witnessing exponential growth owing to rising data complexity in organizations and the requirement for integrated, precise, and consistent master data management throughout all business functions. Growth in the usage of cloud-based technology and digitization is further fuelling the growth of the market. The rise in the adoption of artificial intelligence, analytics, and real-time data integration is fueling the demand for MDM software. Moreover, regulatory mandates and improvements in customer experience in sectors like BFSI, healthcare, retail, and manufacturing are driving the market globally.

Across global enterprise deployments, more than 73,000 organizations across 82 countries have implemented MDM solutions, while over 41,200 enterprises operate centralized MDM systems managing customer, product, supplier, and financial data across business functions globally operations. Over 2.4 million master data domains are actively managed worldwide, with approximately 37 billion master data transactions occurring daily across industries, reflecting large-scale enterprise data complexity and continuous real-time data synchronization requirements globally.

Market Size and Forecast

-

Market Size in 2026E: USD 22.55 Billion

-

Market Size by 2035: USD 94.08 Billion

-

CAGR: 17.20% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Master Data Management Market - Request Free Sample Report

Master Data Management Market Trends

-

Rising demand for unified, accurate, and consistent enterprise data is driving the master data management (MDM) market.

-

Growing adoption across BFSI, healthcare, retail, manufacturing, and telecom sectors is boosting market growth.

-

Expansion of digital transformation initiatives and data-driven decision-making is fueling MDM deployment.

-

Increasing focus on data governance, compliance, and regulatory requirements is shaping adoption trends.

-

Advancements in cloud-based MDM platforms, AI-driven data quality tools, and real-time data integration are enhancing efficiency and accuracy.

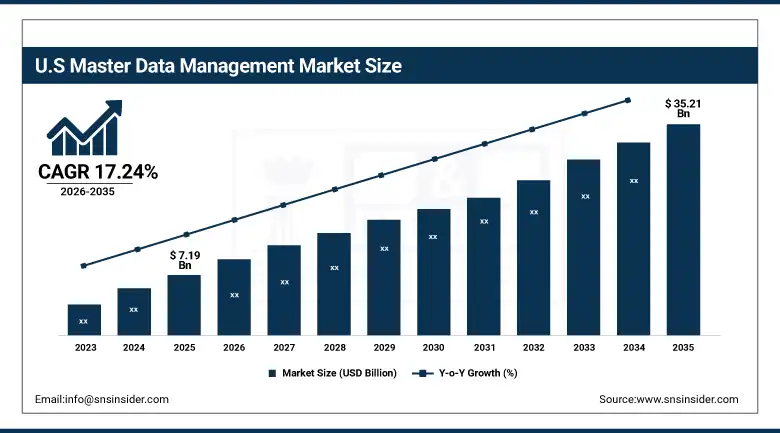

The U.S. Master Data Management Market Outlook

The U.S. Master Data Management Market was valued at approximately USD 7.19 Billion in 2025 and is expected to reach approximately USD 35.21 Billion by 2035, growing at a CAGR of approximately 17.24%.

The United States accounts for approximately 37.40% of global MDM market revenue, driven by the world's largest enterprise software market, the most advanced corporate AI adoption rate among major economies, and the regulatory compliance obligations of its financial services, healthcare, and data-intensive technology sectors whose data governance requirements create non-negotiable MDM investment mandates. U.S. financial institutions subject to Basel III capital adequacy reporting, healthcare organisations managing HIPAA-compliant patient data, and retailers under CCPA consumer data rights obligations each face regulatory consequences for data accuracy failures that directly justify MDM investment through a compliance cost avoidance ROI calculation.

The U.S. Department of Health and Human Services (HHS) manages massive healthcare datasets under HIPAA regulatory frameworks, requiring strict master data consistency, interoperability, and governance across providers, payers, and healthcare systems to ensure accurate and secure data exchange.

Master Data Management Market Segment Analysis

-

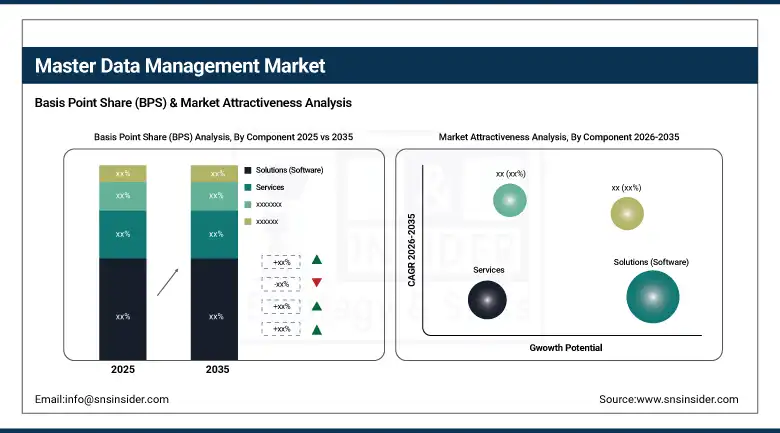

By Component, Solutions (Software) segment dominated the Master Data Management Market in 2025 with 68% share; Services (Consulting, Integration, Support) segment is the fastest growing segment.

-

By Deployment Model, On-premises segment dominated the market in 2025 with 56% share; Cloud-based segment is the fastest growing segment.

-

By Data Domain, Customer Master Data segment dominated the market in 2025 with 32% share; Product Master Data segment is the fastest growing segment.

-

By End User, Banking, Financial Services & Insurance (BFSI) segment dominated the market in 2025 with 28% share; Healthcare segment is the fastest growing segment.

By Component, solutions (software) segment dominates the master data management market, services segment expected to grow fastest

The Solutions (Software) segment dominated the Master Data Management Market in 2025 owing to the critical requirement for centralized data governance, data quality management, and master data integration platform solutions in organizations. Companies are opting for MDM solutions in order to consolidate scattered data across various systems and gain decision-making precision along with ensuring that they comply with all the relevant laws. With the increasing rate of digital transformations and the amount of data, companies are adopting software solutions as the main source of revenue generation.

The Services segment is the fastest growing due to an increase in the demand for consultancy, integration, data migration, and other services pertaining to MDM solution implementation. The inability of most firms to implement MDM solutions without the help of third parties has increased their demand for managed services significantly. With the increasing rate of cloud adoption and growing complexity of enterprise data ecosystems, the trend has accelerated.

By Deployment Model, on-premises segment dominates the master data management market, cloud-based segment expected to grow fastest

The On-premises segment dominated the market in 2025 owing to high preferences of enterprises towards control, security, and compliance adherence. Many companies still utilize legacy hardware and software, which are deeply embedded with on-premise MDM solutions. Moreover, concerns around data privacy, regulatory compliance, and customized solutions have driven more companies to use on-premise MDM solutions, especially those that deal with highly sensitive client and financial data.

The Cloud-based segment is the fastest growing as companies seek data management solutions that are highly flexible and scalable at lower costs. Cloud-based deployment allows for quick deployment, updating, and greater access through distributed teams. Growing digital transformation efforts, expanding hybrid IT, and increasing needs for data synchronization are boosting cloud-based MDM deployment. Moreover, cloud MDM solutions are less demanding on infrastructure and facilitate advanced analytics.

By Data Domain, customer master data segment dominates the master data management market, product master data segment expected to grow fastest

The Customer Master Data segment dominated the market in 2025 because of its significance to have accurate, consistent, and complete customer data. Companies need customers' data for marketing activities, personalized content, compliance management, fraud detection, and customer experience management. The growing trend of organizations adopting customer centricity, along with omnichannel experiences, makes customer master data essential in the data architecture, making the implementation of MDM highly popular.

The Product Master Data segment is the fastest growing due to the increased complexity of product catalogs. Companies are increasingly trying to improve accuracy, standardization, and consistency of their product data. There is an increase in the need to manage product data in light of omnichannel commerce and a growing digital ecosystem around a particular product.

By End User, banking, financial services & insurance (BFSI) segment dominates the master data management market, healthcare segment expected to grow fastest

The Banking, Financial Services & Insurance (BFSI) segment dominated the Master Data Management Market in 2025 because of the high level of reliance on data governance and security measures in financial institutions. The BFSI industry handles substantial amounts of personal data, which must be managed effectively to facilitate risk management, compliance with laws and regulations, fraud detection, and reporting. The stringent regulations and initiatives promoting digital banking have also played a critical role in the adoption of more advanced MDM solutions in the BFSI industry.

The Healthcare segment is the fastest growing because of the increasing digitalization of medical records, increasing use of EHRs, and the requirement for integrated management of medical data. Master Data Management solutions are being increasingly adopted by healthcare providers, insurance companies, and researchers as they help provide better healthcare coordination, minimize data duplication, and meet regulatory requirements. The increasing trend towards precision medicine and clinical decision making based on data is driving the adoption of master data management within the healthcare industry.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

84.73% |

|

Europe |

Germany |

28.47% |

|

Asia Pacific |

China |

38.47% |

|

Middle East & Africa |

UAE |

24.73% |

|

Latin America |

Brazil |

43.84% |

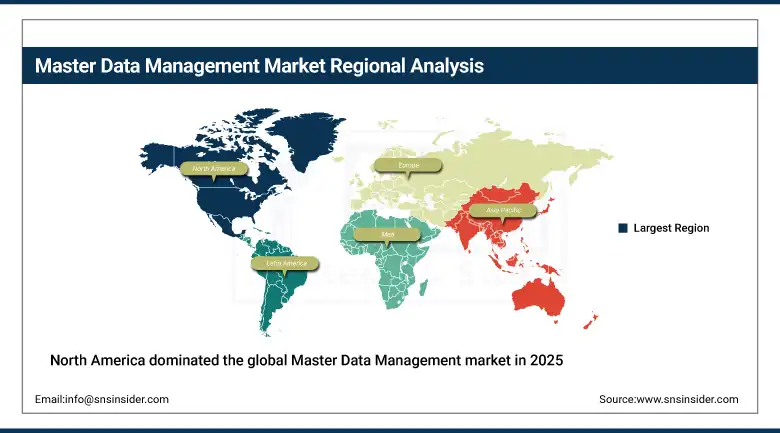

North America Master Data Management Market Insights

North America dominated the global Master Data Management market in 2025, holding approximately 37.40% of global revenues. The United States accounts for approximately 84.73% of regional revenue through its combination of the world's most commercially active enterprise software market, the highest corporate AI adoption rate among major economies creating data quality dependencies, and regulatory compliance obligations across financial services, healthcare, and consumer data sectors that create non-discretionary MDM investment mandates. The concentration of MDM platform vendors, global system integrators, and sophisticated enterprise buyers in the United States creates a self-reinforcing commercial ecosystem whose innovation pace and adoption velocity sustain North American market leadership.

The U.S. Census Bureau reports that over 92% of enterprises now use cloud services, significantly increasing the complexity of distributed data environments. This trend is driving strong demand for master data management (MDM) platforms to ensure consistency, integration, and governance.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Master Data Management Market Insights

Europe held approximately 26.84% of global Master Data Management revenues in 2025. GDPR's data accuracy and data minimisation obligations, which impose legal responsibility on organisations for the quality and consistency of personal data they process, have been the most commercially significant single regulatory driver of European MDM investment since 2018. Financial services organisations subject to BCBS 239 data aggregation and reporting standards and healthcare organisations managing cross-border clinical data flows under EU data protection frameworks each face compliance-driven MDM investment requirements whose financial consequence of non-compliance substantially exceeds platform investment.

Germany accounts for approximately 28.47% of European revenues through its concentration of manufacturing, automotive, and financial services enterprises whose operational data complexity makes MDM investment a strategic necessity.

According to Eurostat, more than 75% of large EU enterprises use cloud computing services, accelerating demand for centralized and consistent master data management across distributed systems, ensuring data quality, integration efficiency, and seamless digital operations across business functions.

The European Data Strategy seeks to create data spaces across more than 14 industrial sectors, driving the need for interoperable and standardized master data frameworks that enable secure data sharing, cross-sector collaboration, and improved digital ecosystem integration.

Asia Pacific Master Data Management Market Insights

Asia Pacific is the fastest-growing regional Master Data Management market, projected to expand at a CAGR of approximately 21.84% through 2035.

According to the International Data Corporation (IDC), Asia generates over 40% of global digital data, making data governance a critical enterprise priority across industries and increasing demand for standardized master data management frameworks for large-scale digital ecosystems worldwide

China accounts for approximately 38.47% of Asia Pacific revenues through its large enterprise sector's growing adoption of data governance platforms, government digital economy development programmes, and the expansion of Chinese technology companies whose global commercial operations require consistent customer and product data management across multiple international markets. India is growing rapidly as its IT services sector's clients deploy MDM solutions and as its own enterprise sector's digital transformation investment creates domestic demand.

China’s Ministry of Industry and Information Technology (MIIT) reports over 1.1 billion internet users, creating massive digital ecosystems that require strong master data standardization, integration, and governance across enterprises, platforms, and public digital infrastructure systems.

MEA & Latin America Master Data Management Market Insights

Middle East and Latin America are growing Master Data Management markets where digital transformation investment, financial services sector modernisation, and growing regulatory data governance requirements are creating expanding institutional MDM demand. The UAE leads MEA revenues at approximately 24.73% of the regional total through its Smart Dubai and national digital economy programmes that are driving enterprise data management investment across government and financial services sectors. Saudi Arabia's Vision 2030 digital transformation agenda is creating substantial government and private sector MDM investment.

Brazil leads Latin American revenues at approximately 43.84% of the regional total through its large financial services sector, LGPD data protection legislation creating compliance-driven data quality obligations, and its growing technology sector whose platform companies require sophisticated customer data management capabilities.

Market Dynamics

Growth Drivers: Enterprise AI adoption and regulatory compliance requirements are driving strong structural demand for Master Data Management solutions.

The AI investment wave that has swept enterprise technology since 2023 has exposed a fundamental dependency that was previously less commercially visible. AI models trained on inconsistent, duplicated, or inaccurate master data produce unreliable outputs whose deployment into production business processes creates operational and reputational risk proportional to the AI application's decision authority. Enterprises that have invested heavily in AI platforms are discovering that their return on AI investment is constrained by data quality limitations that MDM systems are specifically designed to resolve. This AI-MDM dependency is creating a new commercial narrative for MDM investment whose ROI framing, centred on AI productivity enablement rather than solely data governance compliance, resonates with executive sponsors whose primary strategic priority is AI-driven competitive differentiation rather than data management process improvement.

Restraints: High implementation complexity and long deployment timelines create budget uncertainty and slow enterprise Master Data Management adoption.

Enterprise MDM implementations are consistently among the most complex software deployments in the IT portfolio. Integrating an MDM platform with dozens of existing systems, migrating historical data, establishing data governance processes requiring sustained business engagement, and managing organisational change around data ownership accountability represents a multi-year programme whose complexity frequently exceeds initial scope and budget estimates. This implementation challenge creates a credibility barrier that vendors must overcome through reference customer evidence, methodology maturity, and system integrator capability.

Opportunities: Cloud-native multi-domain platforms and generative AI-enabled data stewardship automation are expanding Master Data Management market opportunities globally.

Cloud-native MDM architecture and generative AI stewardship capabilities are progressively reducing two major adoption barriers: implementation complexity and ongoing operational cost. Cloud-native platforms deploy in weeks, integrate through standard APIs, and eliminate infrastructure provisioning challenges that make on-premise MDM slow. Generative AI automates data match-merge decisions, entity resolution review, and business glossary maintenance, reducing steward labour requirements at enterprise data volumes. These advances make comprehensive MDM economically feasible for mid-market organisations and high-growth technology companies that previously could not justify traditional MDM programme investment.

Recent Developments:

-

2026: Reltio announced expansion of AI-driven “contextual MDM” capabilities, improving real-time golden record creation and enabling enterprises to unify 90%+ hidden enterprise data for AI-ready applications.

-

2025: Semarchy launched MDM platform integration with Snowflake AI Data Cloud, enabling enterprises to deploy master data hubs directly inside Snowflake for high-performance governance, analytics, and scalable data processing.

-

2025: SAP launched its Business Data Cloud platform integrating SAP Datasphere's MDM and data governance capabilities with Databricks Lakehouse architecture, enabling enterprise customers to manage master data governance and analytical workloads within a unified cloud data architecture that eliminates the data pipeline complexity of separate MDM and analytics infrastructure.

-

2024: Reltio reported 60% annual revenue growth driven by enterprise adoption of its cloud-native customer MDM platform, with its AI-powered graph-based entity resolution engine achieving sub-second customer identity resolution performance that satisfied real-time digital banking, insurance, and pharmaceutical commercial operations requirements.

-

2023: Informatica partnered with MongoDB to enable cloud-native Master Data Management applications using Informatica MDM SaaS and MongoDB Atlas, allowing enterprises to build 360-degree trusted data applications and replace legacy data systems.

Master Data Management Market Key Players are:

-

Informatica

-

IBM

-

SAP SE

-

Oracle Corporation

-

TIBCO Software Inc.

-

Talend S.A.

-

Stibo Systems

-

Profisee Group, Inc.

-

Reltio Inc.

-

Ataccama Corporation

-

SAS Institute Inc.

-

Teradata Corporation

-

Magnitude Software, Inc.

-

EnterWorks (Winshuttle, LLC)

-

Riversand Technologies, Inc. (Syndigo)

-

Contentserv Group AG

-

Semarchy

-

Cloudera, Inc.

-

Microsoft

-

Qlik

Master Data Management Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 19.24 Billion |

| Market Size by 2035 | USD 94.80 Billion |

| CAGR | CAGR of 17.20% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Solutions, Services) • By Deployment Model (On premises, Cloud based) • By Data Domain (Customer Master Data, Product Master Data, Supplier / Vendor Data, Finance / Reference Data, Asset & Location Data) • By End User / Industry Vertical (IT & Telecom, Banking, Financial Services & Insurance (BFSI), Healthcare, Retail & E commerce, Manufacturing, Media & Entertainment, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Informatica, IBM, SAP SE, Oracle Corporation, TIBCO Software Inc., Talend S.A., Stibo Systems, Profisee Group, Inc., Reltio Inc., Ataccama Corporation, SAS Institute Inc., Teradata Corporation, Magnitude Software, Inc., EnterWorks (Winshuttle, LLC), Riversand Technologies, Inc. (Syndigo), Contentserv Group AG, Semarchy, Cloudera, Inc., Microsoft, Qlik |

Frequently Asked Questions

North America dominated the Master Data Management Market in 2025, holding approximately 37.40% of global revenues,

The on-premise deployment segment dominated the Master Data Management Market.

Enterprise AI adoption and regulatory compliance requirements are driving strong structural demand for Master Data Management solutions.

The Master Data Management Market was valued at USD 19.24 Billion in 2025.

The Master Data Management Market is expected to grow at a CAGR of 17.20% from 2026 to 2035.

Get in Touch