Medical Clothing Market Report Scope & Overview:

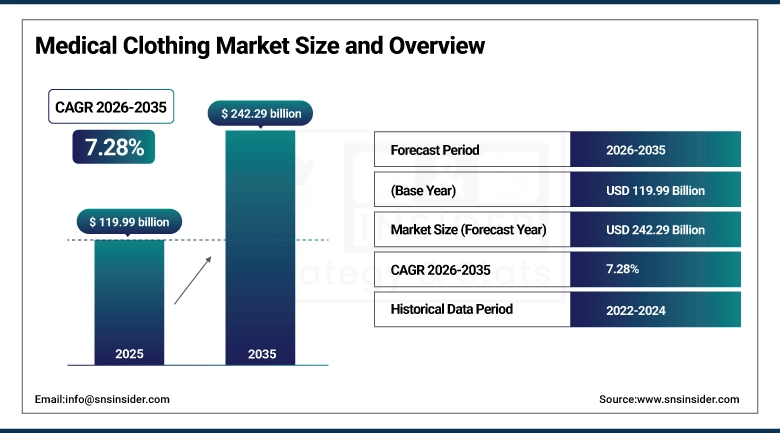

The Medical Clothing Market size was valued at USD 119.99 Billion in 2025 and is projected to reach USD 242.29 Billion by 2035, growing at a CAGR of 7.28% during 2026–2035.

The Medical Clothing Market is growing steadily, and the main reason behind this is the increased health awareness, the number of surgeries being performed, and the infection control guidelines. The need for hygienic, long-lasting, and comfortable clothing, both for the patients and the medical staff, is driving the market. The advancements in technology, especially regarding fabric, are also contributing to the growth of the Medical Clothing Market. The growth in the healthcare infrastructure and the need to keep the workers safe are also contributing to the growth of the Medical Clothing Market, along with the use of disposable and eco-friendly clothing.

Medical Clothing Market Size and Forecast:

-

Market Size in 2025: USD 119.99 Billion

-

Market Size by 2035: USD 242.29 Billion

-

CAGR: 7.28% during 2026–2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Medical Clothing Market - Request Free Sample Report

Medical Clothing Market Key Trends:

-

Increasing adoption of antimicrobial and fluid-resistant fabrics to enhance infection control and safety.

-

Rising demand for disposable medical clothing driven by hygiene concerns and hospital-acquired infection prevention.

-

Growing focus on sustainable and eco-friendly materials in medical apparel production.

-

Integration of advanced textiles offering improved comfort, breathability, and durability for healthcare professionals.

-

Expansion of healthcare infrastructure and surgical volumes boosting demand for medical clothing.

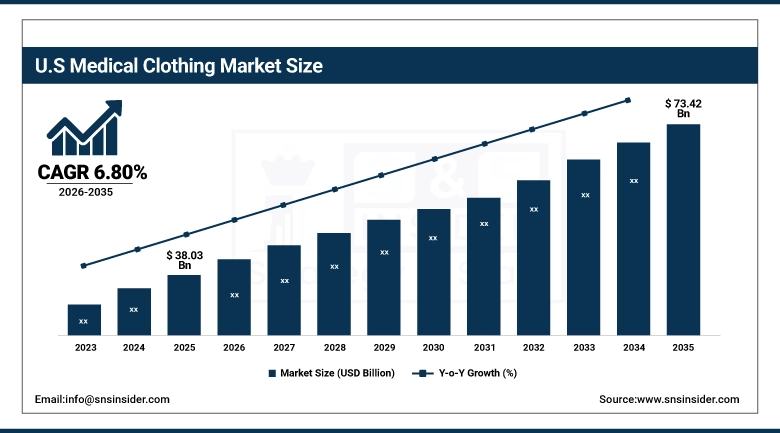

The U.S. Medical Clothing Market has been valued at USD 38.03 Billion in 2025 and is expected to reach USD 73.42 Billion in 2035, growing at a CAGR of 6.80% from 2026 to 2035, Growth is driven by rising surgical procedures, increasing infection control awareness, expanding healthcare infrastructure, and strong demand for disposable and protective apparel. Technological advancements in fabric materials and stringent regulatory standards further support adoption across healthcare settings.

Medical Clothing Market Drivers

-

Rising infection control awareness and increasing surgical procedures drive demand for medical clothing.

The main driver for the Medical Clothing Market is the increased focus on infection prevention and control in medical settings. The increased number of surgeries and hospitalizations is significantly contributing to the increased demand for medical clothing. In addition, strict regulatory guidelines for patient safety and worker safety, along with technological advancements in fabric technology, are further propelling the market. The increased rate of adoption of disposable medical clothing is also contributing to market growth.

Medical Clothing Market Restraints

-

High costs of advanced medical textiles and environmental concerns over disposables limit market growth.

The market faces challenges due to the high cost associated with advanced medical fabrics that offer enhanced protection and durability. These costs can be a burden for smaller healthcare facilities. Additionally, the widespread use of disposable medical clothing raises environmental concerns due to increased medical waste generation. Regulatory pressures regarding waste management and sustainability, along with fluctuating raw material prices, further restrain market growth.

Medical Clothing Market Opportunities

-

Innovation in sustainable materials and smart textiles creates new growth opportunities.

In addition, the increasing need for sustainability has also created more opportunities for eco-friendly and reusable medical clothing materials. For example, more investments are being made in biodegradable and recyclable materials. On the other hand, smart medical clothing materials with temperature control and antimicrobial properties are also gaining more importance. With more innovation in fabric materials and investments and awareness in healthcare, more opportunities are being created for market players to flourish in the medical clothing market.

Medical Clothing Market Segments:

-

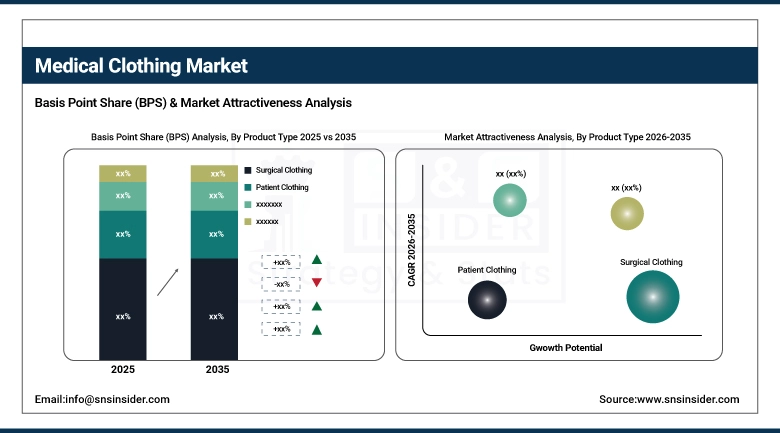

By Product Type: In 2025, Surgical Clothing dominated with 42% share; Protective Clothing fastest growing segment during 2026-2035

-

By Material: In 2025, Nonwoven dominated with 58% share; Woven fastest growing segment during 2026-2035

-

By Distribution Channel: In 2025, Offline dominated with 65% share; Online fastest growing segment during 2026-2035

-

By End User: In 2025, Hospitals dominated with 61% share; Ambulatory Surgical Centers fastest growing segment during 2026-2035

Medical Clothing Market Segment Analysis:

By Product Type: Surgical Clothing Dominate, Protective Clothing Fastest-Growing

Surgical Clothing has the largest share in the Medical Clothing Market, attributed to the high volume of surgeries and hygiene standards maintained in medical facilities. These products play a crucial role in maintaining a sterile environment, thereby reducing the risk of infection. The high rate of surgeries has contributed significantly to this segment.

Protective Clothing has been one of the fastest-growing segments in the Medical Clothing Market, attributed to increasing awareness about healthcare worker safety and infection control. The increasing rate of infectious diseases and the use of personal protective equipment (PPE) have contributed significantly to the growth of this segment. Furthermore, advancements in protective clothing materials and disposable protective wear have contributed to the growth of this segment.

By Material: Nonwoven Dominate, Woven Fastest-Growing

Non-woven materials are leading in the Medical Clothing Market because these materials are cost-effective and have excellent barrier properties, especially for use in medical clothing that is disposable. The use of these materials is highly preferred for surgical and protective clothing, especially because they are able to prevent any penetration of fluids, hence eliminating the risk of contamination. The fact that these materials are light and can be produced on a large scale also contributes to their dominance in the market.

Woven materials are growing rapidly in the Medical Clothing Market, and this growth can be attributed to the increased demand for reusable and durable medical clothing. Woven materials are providing comfort, breathability, and strength, and are therefore most suitable for use in medical clothing. Sustainability and eco-friendly healthcare practices are also boosting the use of woven materials in medical clothing.

By Distribution Channel: Offline Dominate, Online Fastest-Growing

Offline distribution channels lead the market in terms of share, which is about 65%. This is due to the fact that healthcare institutions prefer to buy products directly from the suppliers or distributors, which ensures the quality of the products as well as the regulatory requirements.

Online distribution channels are growing at a rapid pace, and this is attributed to the increasing trend of e-commerce and digital procurement. The online distribution channels are becoming increasingly popular among smaller healthcare facilities, as these channels offer a variety of products and competitive prices. The trend of digitalization is also contributing to the rapid growth of this segment.

By End User: Hospitals Dominate, Ambulatory Surgical Centers Fastest-Growing

Hospitals account for the largest share in the market, and this can be attributed to the large number of admissions, surgeries, and infection control practices. The constant requirement for medical clothing in different departments and the availability of advanced healthcare facilities are also contributing to the large share of hospitals.

Ambulatory Surgical Centers account for the fastest growth rate, and this can be attributed to the growing demand for such facilities and cost-effective treatments. The growing number of minimally invasive surgeries and shorter recovery times are contributing to the demand for medical clothing in such facilities. Furthermore, the expansion of such facilities has also contributed to the growth rate of this segment.

Medical Clothing Market Regional Analysis:

North America Medical Clothing Market Insights:

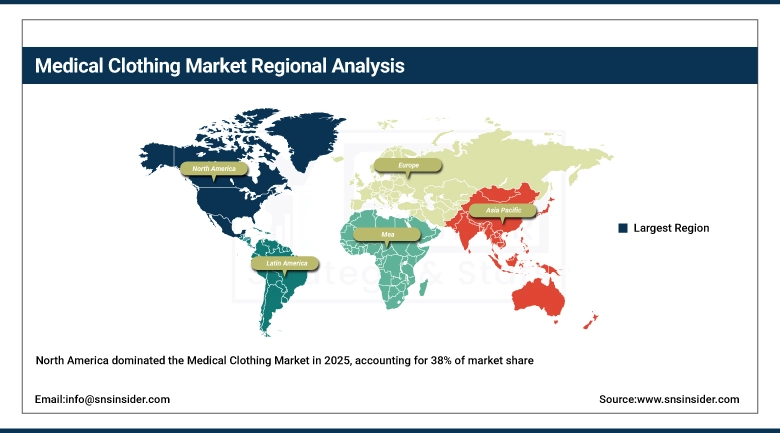

North America dominates the Medical Clothing Market, accounting for approximately 38% of the global market share. This dominance is driven by advanced healthcare infrastructure, high healthcare expenditure, and strict regulatory standards for infection control and patient safety. The region has a high volume of surgical procedures and strong adoption of disposable medical apparel. Additionally, the presence of leading market players, continuous technological advancements in medical textiles, and increasing awareness regarding healthcare worker safety further strengthen North America’s leading position in the market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Medical Clothing Market Insights:

Europe has a considerable share in the Medical Clothing Market, which is attributed to the presence of well-established healthcare infrastructure and regulatory guidelines for infection control. The region has a high penetration rate for quality medical apparel, and there is a greater emphasis on patient and worker safety. The region has seen an increase in surgical procedures, and there has been a greater demand for advanced, comfortable, and sustainable medical apparel, thereby driving the Medical Clothing Market. Moreover, there has been constant innovation and presence of major players, thus driving the Medical Clothing Market in this region.

Asia-Pacific Medical Clothing Market Insights:

Asia-Pacific is the fastest-growing segment of the Medical Clothing Market due to the rapid development of infrastructure in the region and the growing investments in the health sector. Moreover, the growing population and the number of surgeries are significantly contributing to the growth of the medical clothing market. In addition to this, the awareness of maintaining hygiene and controlling infections is further adding to the growth of the medical clothing market. Moreover, the presence of emerging economies in the region is adding to the growth of the medical clothing market.

Latin America Medical Clothing Market Insights:

Latin America, contributes a moderate share to the Medical Clothing Market, owing to an improving healthcare infrastructure and increasing healthcare expenditure. Awareness regarding infection prevention and hygiene is also increasing, and this is boosting the demand for medical clothing. Furthermore, an increasing number of surgical procedures and a growing trend towards the use of disposable medical clothing are also fueling the region's steady growth. The government is also improving healthcare facilities and increasing access to healthcare, which is also adding to the region's steady growth.

Middle East & Africa (MEA) Medical Clothing Market Insights:

The Middle East & Africa region offers an emerging market for medical clothing, considering the improvement in healthcare infrastructure in the region, which in turn increases investments in the healthcare system. In addition, the awareness of infection control and the need for protective clothing in the medical field is boosting the market in the region. Moreover, the growth in the number of hospitals, clinics, and government initiatives to improve the quality of healthcare services are driving the market in the region. In addition, the incidence of chronic diseases, along with the adoption of advanced medical textiles, is boosting the market in the region.

Medical Clothing Market Competitive Landscape:

3M Company was founded in 1902 and is a diversified technology company headquartered in the USA. 3M operates across multiple sectors, including healthcare, safety, and industrial solutions, offering a wide range of products used in medical and protective applications. Its portfolio includes medical tapes, wound care products, respirators, and protective medical clothing designed to enhance safety and infection control. The company has a global presence in over 70 countries and employs thousands of professionals worldwide.

-

In May 2024: 3M expanded its healthcare product portfolio by introducing advanced medical-grade materials and protective solutions aimed at improving infection prevention and healthcare worker safety in clinical environments.

Cardinal Health, Inc. was founded in 1971 and is a multinational healthcare services company based in the USA. The company specializes in the distribution of pharmaceuticals and medical products, including a broad range of medical clothing such as surgical gowns, drapes, and personal protective equipment. Cardinal Health serves hospitals, healthcare systems, and pharmacies globally, supporting efficient supply chain management and patient care. The company operates in numerous countries and has a strong workforce worldwide.

-

In March 2024: Cardinal Health strengthened its medical products segment by expanding its portfolio of sustainable and high-performance medical apparel, focusing on enhancing supply reliability and meeting growing demand for protective healthcare clothing.

Medical Clothing Market Key Players:

-

3M Company

-

Cardinal Health, Inc.

-

Medline Industries, LP

-

Owens & Minor, Inc.

-

Kimberly-Clark Corporation

-

Halyard Health, Inc. (Owens & Minor)

-

Mölnlycke Health Care AB

-

Ansell Limited

-

DuPont de Nemours, Inc.

-

Lakeland Industries, Inc.

-

Alpha Pro Tech, Ltd.

-

Sioen Industries NV

-

Superior Uniform Group, Inc.

-

Aramark Corporation

-

Cintas Corporation

-

Tronex International, Inc.

-

Paul Hartmann AG

-

Berner International GmbH

-

Prestige Ameritech

-

Barco Uniforms, Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 119.99 Billion |

| Market Size by 2035 | USD 242.29 Billion |

| CAGR | CAGR of 7.28% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type: (Surgical Clothing, Patient Clothing, Staff Apparel, Protective Clothing) • By Material: (Nonwoven, Woven) • By Distribution Channel: (Online, Offline) • By End User: (Hospitals, Clinics, Ambulatory Surgical Centers, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | 3M Company, Cardinal Health, Inc., Medline Industries, LP, Owens & Minor, Inc., Kimberly-Clark Corporation, Halyard Health, Inc. (Owens & Minor), Mölnlycke Health Care AB, Ansell Limited, DuPont de Nemours, Inc., Lakeland Industries, Inc., Alpha Pro Tech, Ltd., Sioen Industries NV, Superior Uniform Group, Inc., Aramark Corporation, Cintas Corporation, Tronex International, Inc., Paul Hartmann AG, Berner International GmbH, Prestige Ameritech, Barco Uniforms, Inc. |

Frequently Asked Questions

Ans: The Medical Clothing Market is expected to grow at a CAGR of 7.28% during 2026–2035.

Ans: The market was valued at USD 119.99 Billion in 2025 and is projected to reach USD 242.29 Billion by 2035.

Ans: The key drivers of the Medical Clothing Market include rising surgical procedures, infection control awareness, healthcare infrastructure expansion, demand for protective apparel, technological fabric advancements, and disposable clothing adoption drive market growth.

Ans: The Surgical Clothing segment dominated during the projected period.

Ans: North America dominated the Medical Clothing Market in 2025.

Get in Touch