Pharmacy Automation Devices Market Report Scope & Overview:

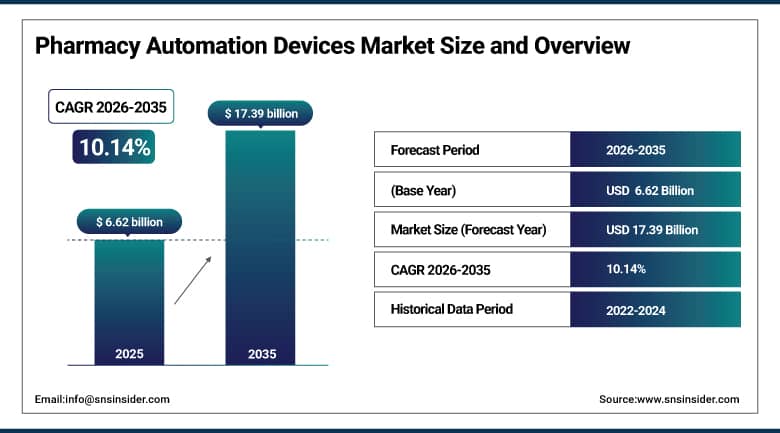

The Pharmacy Automation Devices Market size was valued at USD 6.62 billion in 2025 and is expected to reach USD 17.39 billion by 2035, growing at a CAGR of 10.14% over the forecast period of 2026–2035.

The global pharmacy automation devices market is witnessing rapid growth due to an increase in the number of prescriptions filled, an increase in the number of medication errors, and the need for healthcare institutions to reduce costs while improving patient safety outcomes. Pharmacy automation devices, including automated dispensing systems, robotic medication management systems, and pharmacy workflow management solutions, are changing the face of both inpatient and retail pharmacy practice around the world. This growth trend is further fueled by the increasing number of patients suffering from various diseases who require long-term management and the need for healthcare institutions around the world to automate their pharmacy practice while catering to an aging global populace and the increasing trend towards healthcare technology and automation.

For instance, in February 2024, a study published in the American Journal of Health-System Pharmacy reported that hospitals deploying robotic dispensing systems achieved a 92% reduction in medication dispensing errors, reinforcing institutional demand for pharmacy automation solutions across acute care settings.

Pharmacy Automation Devices Market Size and Forecast:

-

Market Size in 2025: USD 6.62 billion

-

Market Size by 2035: USD 17.39 billion

-

CAGR: 10.14% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get More Information On Pharmacy Automation Devices Market - Request Free Sample Report

Pharmacy Automation Devices Market Trends:

-

Rapid adoption of robotic dispensing systems and automated dispensing cabinets (ADCs) driven by increasing prescription volume and pharmacist workforce shortages across hospital and retail settings.

-

Integration of artificial intelligence and machine learning algorithms into pharmacy automation platforms to enable predictive inventory management and real-time medication tracking.

-

Growing deployment of centralized automation hubs within health systems to consolidate medication preparation, packaging, labeling, and distribution workflows efficiently.

-

Expansion of automated medication compounding systems in specialty and oncology pharmacy settings to ensure sterile preparation accuracy and adherence to regulatory compliance standards.

-

Rising implementation of cloud-connected pharmacy automation platforms enabling remote monitoring, software updates, and interoperability with electronic health records and clinical systems.

-

Increasing demand for tabletop tablet counters and compact dispensing solutions among independent, community, and small-chain retail pharmacy operators globally.

-

Strengthened focus on cybersecurity protocols and data integrity frameworks within connected pharmacy automation networks to comply with FDA, USP, and HIPAA regulatory requirements.

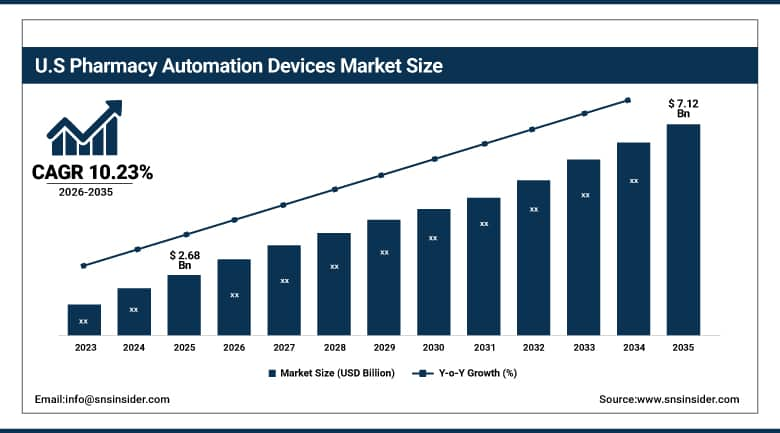

The U.S. Pharmacy Automation Devices Market was valued at USD 2.68 billion in 2025 and is expected to reach USD 7.12 billion by 2035, growing at a CAGR of 10.23% from 2026–2035. The US dominates the pharmacy automation devices market worldwide, driven by the high number of hospitals and retail pharmacies, stringent medication safety regulations, and strong capital investment bases of integrated healthcare delivery networks. Incentives for healthcare technology adoption by the US government, high prevalence of chronic diseases, and pharmacist staffing shortages are key drivers for automation adoption in all care settings. Additionally, the US takes the lead in the adoption of cutting-edge technologies for automated dispensing cabinets and robots, with established reimbursement models and a competitive vendor landscape.

Pharmacy Automation Devices Market Growth Drivers:

-

Rising Medication Errors and Patient Safety Mandates are Driving the Pharmacy Automation Devices Market Growth

The increasing concerns about medication errors in terms of dispensing, adverse drug events, and pharmacy-related patient harm are pressuring healthcare institutions and regulatory organizations to mandate the implementation of automated pharmacy systems. In fact, the Joint Commission, FDA, and CMS guidelines together emphasize the implementation of barcode medication administration systems, automated dispensing cabinets, and robotic systems to improve the accuracy of the medication use process. These patient safety initiatives are directly influencing the demand for pharmacy automation systems, thus generating a sustained and increasing addressable market opportunity in all categories of implementation worldwide.

For instance, in August 2024, CMS updated its Conditions of Participation requiring all accredited hospital pharmacies to implement electronic medication verification systems, driving accelerated procurement of pharmacy automation solutions across U.S. health systems.

Pharmacy Automation Devices Market Restraints:

-

High Capital Investment and Integration Complexities are Hampering the Pharmacy Automation Devices Market Growth

The high costs involved in procuring and maintaining pharmacy automation technologies, which include robotic dispensing systems, carousels, and medication compounding technologies, are a major factor hindering the adoption of pharmacy automation technologies. These costs are likely to affect small and independent pharmacies, which would make it difficult for them to keep up with the demand for automation technologies. In addition, issues arising from the integration process with existing electronic health records and the need for technical staff training are likely to affect the overall adoption of pharmacy automation technologies globally during the forecast period, which ranges from 2026 to 2035.

Pharmacy Automation Devices Market Opportunities:

-

AI-Powered Automation and Telepharmacy Integration Unlock Significant Growth Opportunities for the Pharmacy Automation Devices Market

The confluence of artificial intelligence technology, internet of things technology-based pharmacy automation systems, and telepharmacy systems is a new growth frontier for the pharmacy automation market. Artificial intelligence technology-based demand forecasting, smart inventory management systems, and clinical decision alerts integrated into pharmacy automation systems have the potential to mitigate wastage, stockout risks, and operational cost escalations. The integration of telepharmacy systems is also expected to expand the reach of pharmacy automation systems into rural areas. Such technology advancements are expected to create new revenue streams for the pharmacy automation market, thereby enhancing the long-term business value of the pharmacy automation market.

For instance, in June 2024, Omnicell reported that healthcare systems utilizing its AI-driven EnlivenHealth platform achieved a 34% improvement in pharmacy operational efficiency and a 28% reduction in medication waste, reinforcing the commercial impact of intelligent pharmacy automation.

Pharmacy Automation Devices Market Segment Analysis

-

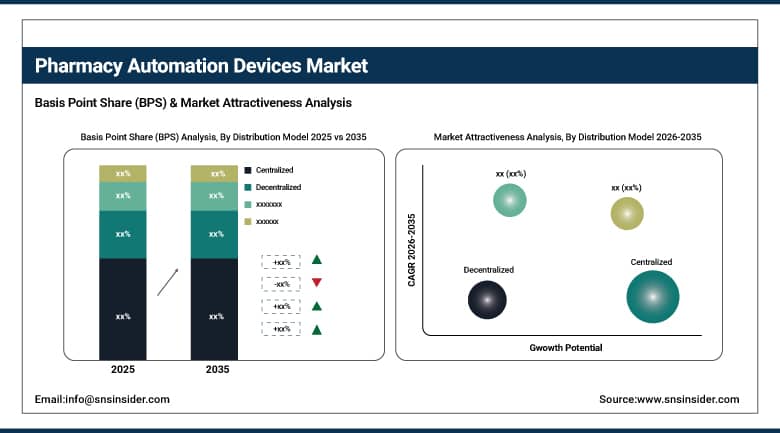

By distribution model, the centralized segment dominated the market with approximately 62.47% share in 2025, while the decentralized segment is expected to register the highest growth with a CAGR of 11.58%.

-

By product, medication dispensing systems held the largest share of approximately 48.35% in 2025, and the packaging and labeling systems segment is expected to register the highest growth with a CAGR of 11.23%.

-

By end-use, inpatient pharmacies accounted for the leading share of nearly 45.18% in 2025, and pharmacy benefit management organizations and mail-order pharmacies are expected to register the highest growth with a CAGR of 12.07%.

By Distribution Model, the Centralized Segment Dominates, While the Decentralized Segment Shows Rapid Growth

In 2025, the bulk of the revenue, accounting for 62.47%, came from centralized distribution as a result of pharmacy operations consolidation, low-cost redundancy of drug inventories and economies of scale. With sophisticated robotics systems that can process large quantities of medication at high speed, assurance processes to ensure quality and low-overhead operations management, the automation hubs are designed for a new future. Approximately 11.58% CAGR from 2026 to 2035 high growth rate of sector transformation in decentralized interest due to increasing point-of-care dispensing at nursing units, emergency departments, and ambulatory clinics. The segment is primarily driven by the demand for faster medication access points at clinical care delivery, decreased nurse retrieval time, and enhanced security of controlled substances at the nursing units.

By Product, Medication Dispensing Systems Lead the Market, While Packaging and Labeling Systems Register Fastest Growth

The medication dispensing systems segment held the largest revenue share of 48.35% in 2025 due to the extensive use of automated dispensing cabinets, robotic dispensing systems, and carousels in inpatient and outpatient pharmacies. This segment meets significant needs in terms of medication dispensing accuracy, management of controlled substances, and tracking of inventory in a clinical environment. In contrast, the packaging and labeling systems segment is predicted to attain the maximum CAGR of 11.23% during 2026 to 2035, influenced by the expanding need for unit-dose blister packaging automation systems and multi-dose blister packaging automation systems in retail pharmacies and mail-order pharmacies. The growth determinants are attributed to the growing need for medication adherence packaging systems, serialization requirements, and retail pharmacy chains’ adoption of automated systems to efficiently process a large number of prescriptions.

By End-Use, Inpatient Pharmacies Lead, and Pharmacy Benefit Management Organizations Register Fastest Growth

The highest share of 45.18% was seen in inpatient pharmacies in 2025, fueled by stringent medication safety standards, high patient census, and regulatory requirements for controlled substance traceability in hospital settings. Inpatient pharmacy operations stand to benefit the most from automated dispensing cabinet and robotic solutions, which can efficiently manage intricate inpatient pharmacy workflows. Pharmacy benefit management organizations and mail-order pharmacy operations are poised to experience the highest CAGR of 12.07% from 2026 to 2035, driven by increasing prescription volumes, inpatient pharmacy operations in specialty drug dispensing, and the need for high throughput fulfillment automation solutions. Growth in direct-to-patient medication delivery and specialty adherence programs adds to the adoption of automation solutions in this high growth segment.

Pharmacy Automation Devices Market Regional Highlights:

North America Pharmacy Automation Devices Market Insights:

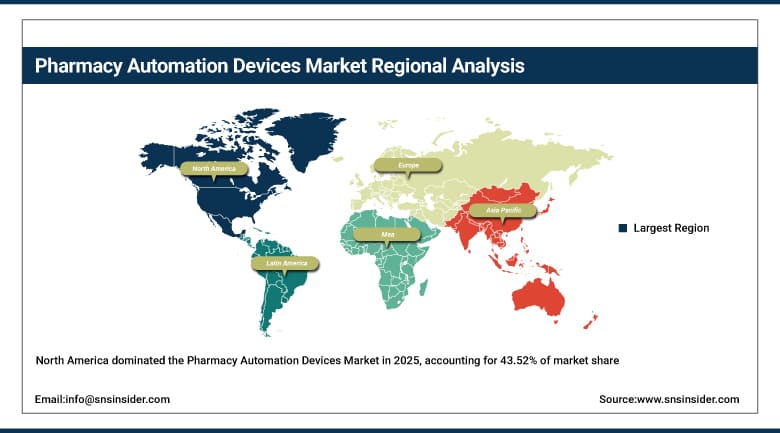

North America dominated the pharmacy automation devices market in terms of highest share of over 43.52% in 2025, driven by an advanced healthcare infrastructure, stringent medication safety standards, and institutional investment in pharmacy technology modernization. The US constitutes the major driver of demand within the North American pharmacy automation devices market, driven by institutional investment in pharmacy technology modernization, operational efficiency, and labor shortages within the US healthcare system. Federal initiatives, value-based care programs, and pharmacy workforce shortages collectively drive the North American pharmacy automation devices market share and its contribution to the multi-billion-dollar revenue contribution throughout the forecast period of 2026 to 2035.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Asia Pacific Pharmacy Automation Devices Market Insights:

The Asia Pacific segment emerges as the fastest growing segment in the global pharmacy automation devices market with a highest CAGR of 12.18%. This is because the hospital infrastructure in emerging countries like China, India, Japan, and South Korea is experiencing rapid growth and the governments in these nations are investing in healthcare, which is driving pharmaceutical regulatory reforms. The increasing prescriptions, knowledge of drug safety benchmarks, and accessibility of low-cost automation platforms have positively broadened the market growth landscape of pharmacy automation devices. The Asia Pacific segment has also been able to maintain an opportunistic scenario for growth owing to the various government initiatives for healthcare digitization, smart hospital development, and pharmaceutical manufacturing automation. Long-term growth scenario for pharmacy automation devices, given the large and aging population base combined with increasing chronic disease management rates.

Europe Pharmacy Automation Devices Market Insights:

With universal healthcare, increasing patient safety requirements, and modernization of hospitals by governments in countries like Germany, the UK, France, and the Netherlands, Europe is the second-largest market for pharmacy automation devices. Regional demand is driven by national health service procurements, data security regulations for connected devices, GDPR compliant norms and standards for use of connected devices, and the rise in adoption of unit dose automation in hospital pharmacy settings in countries such as the U.S., and Canada driving their respective market for dispensing devices over the next ten years. The pharmacy automation device market in all the important countries of the region will grow due to the cross-border effort on pharmaceutical supply chain standards, and European Medicines Agency directives, along with the focus in the pharmaceutical industry on reducing wastage.

Latin America (LATAM) and Middle East & Africa (MEA) Pharmacy Automation Devices Market Insights:

The growth of hospitals in Latin America & Middle East & Africa, increasing spending on pharmaceuticals, and government investment to modernize healthcare infrastructure are sequentially supporting the development of pharmacy automation systems. Growing demand for pharmacy automation system is anticipated from these regions as, Brazil, Mexico, UAE and Saudi Arabia hold significant growth opportunity. Growing number of affordable platforms for pharmacy automation systems, rising medical tourism and favorable reforms in healthcare policies are anticipated to drive the pharmacy automation systems market growth in these regions throughout the forecast period.

Pharmacy Automation Devices Market Competitive Landscape:

Omnicell, Inc., a company founded in 1992, is a global leader in autonomous pharmacy solutions. They provide a wide range of automated dispensing cabinets, robotic pharmacy solutions, and cloud-based medication management solutions. They use their EnlivenHealth analytics engine and XT series automated dispensing cabinets to provide “Intelligent Medication Management” in acute, ambulatory, and retail pharmacy settings.

-

In March 2025, Omnicell launched its next-generation Central Pharmacy Robot with enhanced AI-driven inventory optimization capabilities, enabling high-throughput automated dispensing for large health system pharmacy operations across North America and Europe.

Becton Dickinson and Co., BD (1897) is a diversified global medical technology company that specializes in providing pharmacy automation solutions through its dedicated division of pharmacy automation, which specializes in providing Pyxis automated dispensing systems, medication management solutions, and point-of-care dispensing solutions. BD provides its integrated pharmacy automation solutions along with its informatics solutions for medication safety and supply chain visibility in acute care settings worldwide.

-

In July 2024, BD introduced an upgraded Pyxis MedStation ES system featuring advanced biometric authentication and real-time controlled substance monitoring, strengthening its automated dispensing cabinet leadership across U.S. hospital and ambulatory pharmacy markets.

Swisslog Healthcare, established in 1959, is a worldwide company offering integrated pharmacy automation and intralogistics solutions. They specialize in robotic medication dispensing, pneumatic tube transport systems, and warehouse automation for hospital pharmacies. Their AutoStore and PillPick robots are used by large hospital groups in Europe, North America, and Asia Pacific for high-density storage and precise automated dispensing solutions.

-

In November 2024, Swisslog Healthcare expanded its PillPick automated unit-dose dispensing system into Southeast Asian healthcare markets, partnering with regional hospital networks to deploy integrated robotic pharmacy automation solutions across Singapore and Malaysia.

Pharmacy Automation Devices Market Key Players:

-

Omnicell, Inc.

-

Becton, Dickinson and Company (BD)

-

Swisslog Healthcare

-

Capsa Healthcare

-

ScriptPro LLC

-

ARxIUM

-

Parata Systems

-

Innovation Associates, Inc.

-

RxMedic Systems

-

TCGRx

-

Yuyama Co., Ltd.

-

TOSHO Inc.

-

Willach Pharmacy Solutions

-

Kirby Lester (Capsa Healthcare)

-

McKesson Corporation

-

Baxter International Inc.

-

Talyst (Omnicell)

-

Pearson Medical Technologies

-

AutoMed Technologies

-

Medline Industries, LP

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 6.62 Billion |

| Market Size by 2035 | USD 17.39 Billion |

| CAGR | CAGR of 10.14% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Packaging and Labeling Systems, Storage and Retrieval Systems, Automated Medication Compounding Systems, Tabletop Tablet Counters) • By Distribution Model (Centralized, Decentralized) • By End-Use (Retail Pharmacy, Inpatient Pharmacies, Outpatient Pharmacies, Pharmacy Benefit Management Organizations and Mail-Order Pharmacies) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Omnicell Inc., Becton, Dickinson and Company (BD), Swisslog Healthcare, Capsa Healthcare, ScriptPro LLC, ARxIUM, Parata Systems, Innovation Associates Inc., RxMedic Systems, TCGRx, Yuyama Co., Ltd., TOSHO Inc., Willach Pharmacy Solutions, Kirby Lester (Capsa Healthcare), McKesson Corporation, Baxter International Inc., Talyst (Omnicell), Pearson Medical Technologies, AutoMed Technologies, Medline Industries, LP |

Get in Touch