Molecular Imaging Market Report Scope & Overview:

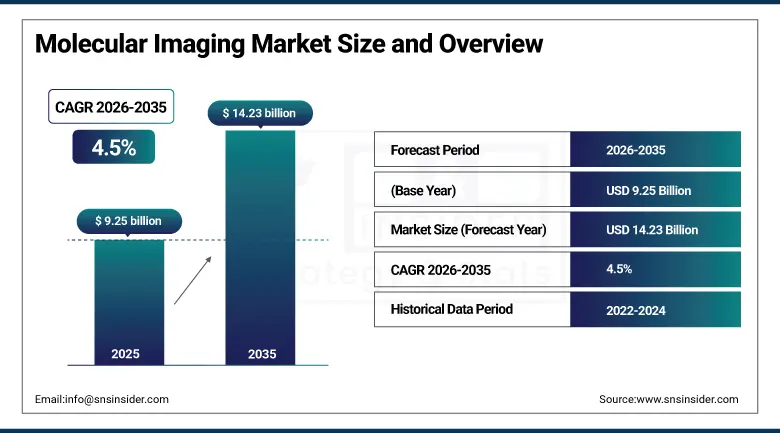

The Molecular Imaging Market was valued at USD 9.25 Billion in 2025 and is expected to reach USD 14.23 Billion by 2035, growing at a CAGR of 4.5% from 2026–2035.

The global molecular imaging market is advancing steadily. Molecular imaging provides non-invasive visualisation of biological processes at the cellular and molecular level, enabling early disease diagnosis, treatment planning, and therapy monitoring with precision that conventional anatomical imaging cannot achieve. Rising cancer incidence, growing cardiovascular disease burden, and increasing neurological disorder prevalence are the primary clinical demand drivers.

In 2023, the FDA approved Siemens Healthineers’ new PET-CT scanner with enhanced imaging resolution for early cancer detection. In late 2023, GE Healthcare launched a next-generation SPECT/CT system improving diagnostic efficiency in cardiology and oncology. These consecutive launches within a single year reflect the competitive pace of clinical-grade molecular imaging innovation whose successive modality improvements progressively expand the patient populations for whom molecular imaging delivers superior diagnostic value relative to conventional radiological alternatives.

Market Size and Forecast

-

Market Size in 2026E: USD 9.67 Billion

-

Market Size by 2035: USD 14.23 Billion

-

CAGR: 4.5% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Molecular Imaging Market - Request Free Sample Report

Molecular Imaging Market Trends

-

AI-assisted image analysis is improving diagnostic accuracy and throughput in molecular imaging, enabling automated lesion detection and computer-aided reporting that reduces radiologist time per study.

-

Hybrid imaging system adoption combining PET-CT, SPECT-CT, and PET-MRI into single integrated platforms is growing as dual-modality systems deliver anatomical.

-

Targeted radiopharmaceutical development for novel imaging agents is expanding clinical indications beyond traditional oncology into Alzheimer’s disease and infection imaging, creating new application categories.

-

Point-of-care and portable molecular imaging device development is creating diagnostic access opportunities in outpatient and community settings where bulky conventional systems cannot be deployed economically.

-

Government-funded cancer research investment and growing precision oncology programme adoption are creating structured institutional demand for molecular imaging in clinical trial drug development, companion diagnostic development, and treatment response assessment.

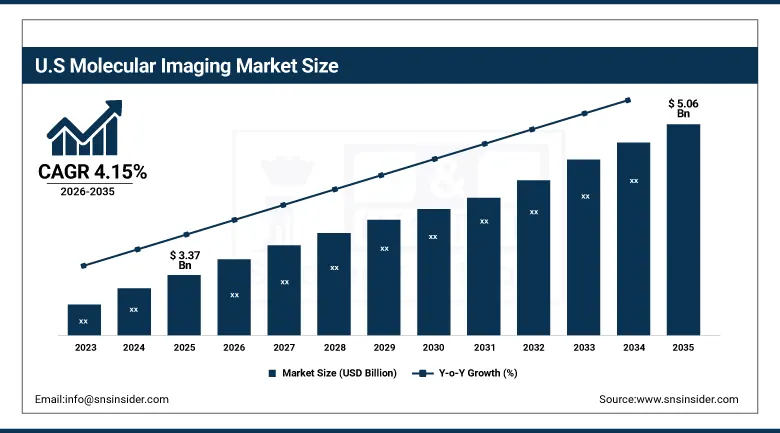

U.S. Molecular Imaging Market Outlook

The U.S. Molecular Imaging Market was valued at approximately USD 3.37 Billion in 2025 and is expected to reach approximately USD 5.06 Billion by 2035, growing at a CAGR of approximately 4.15%.

The U.S. is the world’s largest molecular imaging market. It accounted for approximately 76% of North American revenues in 2023. The U.S. healthcare system’s high adoption of advanced diagnostic technology, robust NIH and NCI research funding, and the commercial presence of GE Healthcare, Siemens Healthineers, and Lantheus create a technically advanced and commercially active market. Medicare and Medicaid reimbursement for PET imaging in oncology creates volume-sustaining institutional procurement.

Lantheus Holdings expanded its PYLARIFY PET imaging agent commercial access in 2024, achieving broader Medicare coverage across additional clinical indications in prostate cancer staging and biochemical recurrence detection. The expansion reflects the growing reimbursement infrastructure for novel diagnostic radiopharmaceuticals whose commercial success sustains the clinical adoption that enables further coverage expansion through payer evidence accumulation.

Molecular Imaging Market Segment Analysis

-

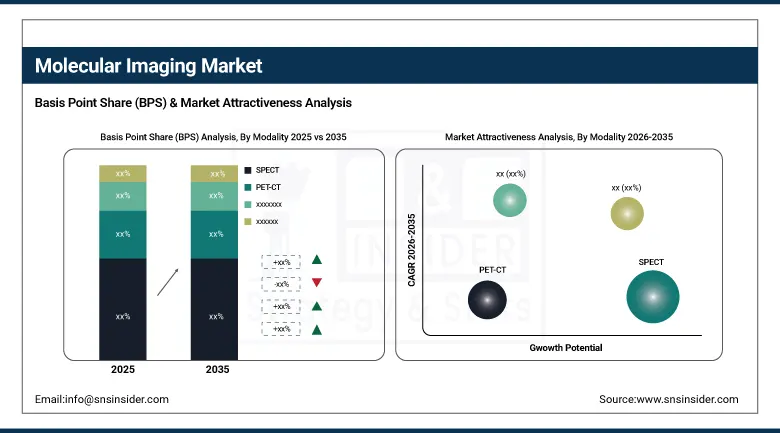

By Modality, the SPECT segment dominated the Molecular Imaging Market with approximately 42.00% share in 2025, while the PET-CT segment is the fastest growing with a CAGR of 5.80% during the forecast period.

-

By Application, the Oncology segment dominated the Molecular Imaging Market with approximately 32.00% share in 2025, while the Neurology segment is the fastest growing with a CAGR of 5.40% during the forecast period.

-

By Product, the Systems/Equipment segment dominated the Molecular Imaging Market with approximately 58.70% share in 2025, while the Radiopharmaceuticals segment is the fastest growing with a CAGR of 5.90% during the forecast period.

-

By End User, the Hospitals segment dominated the Molecular Imaging Market with approximately 54.20% share in 2025, while the Research Institutes segment is the fastest growing with a CAGR of 5.30% during the forecast period.

By Modality, SPECT dominates, PET-CT grows fastest

SPECT retained the dominant modality position with 42% of the molecular imaging market in 2025. Its commercial primacy reflects the large installed base of SPECT and SPECT/CT systems in hospitals globally, the broad availability of technetium-99m radiopharmaceuticals for myocardial perfusion, bone, and brain imaging, and the modality’s cost-effectiveness relative to PET-CT that makes it accessible to a broader range of healthcare facilities. SPECT’s ongoing technical advancement through cadmium-zinc-telluride detector technology is improving sensitivity and resolution while reducing scan time, maintaining its clinical relevance alongside newer modalities.

PET-CT is the fastest-growing modality because its superior sensitivity, three-dimensional functional imaging capability, and simultaneous anatomical localisation provide diagnostic information quality that SPECT alone cannot match in oncology staging, treatment response assessment, and recurrence detection. Each new targeted PET radiopharmaceutical approved for clinical use expands the patient population for whom PET-CT delivers superior diagnostic value over alternative imaging. The approval and commercial launch of PSMA PET agents for prostate cancer, amyloid and tau PET agents for Alzheimer’s, and FDG PET’s continued oncology expansion are collectively driving PET-CT procedure volume growth.

By Application, oncology dominates, neurology grows fastest

Oncology retained the dominant application position with 32% of the molecular imaging market in 2025. Cancer’s extraordinary clinical imaging demand reflects the modality’s unique ability to detect metabolic activity changes that precede anatomical changes detectable by CT or MRI, enabling earlier detection and more sensitive treatment response assessment. Global cancer incidence exceeding 20 million new cases annually creates a structurally large and growing base of patients requiring molecular imaging at diagnosis, during treatment, and for surveillance. PET-CT in oncology represents the highest-revenue application category whose per-study reimbursement and procedure volume compound to sustain the market’s commercial foundation.

Neurology is the fastest-growing application because the Alzheimer’s disease molecular imaging market has entered a new commercial phase following FDA approval of amyloid-lowering therapies whose patient selection requires amyloid PET confirmation. Each patient prescribed lecanemab or donanemab requires an amyloid PET scan to confirm treatment eligibility, creating a structured clinical imaging requirement tied directly to therapy prescription volume. Tau PET imaging for disease staging and neuroinflammation imaging agents for multiple neurological conditions represent additional neurology imaging applications whose clinical validation is progressing through approval pathways.

By Product, systems dominate, radiopharmaceuticals grow fastest

Systems and equipment retained the dominant product position in the molecular imaging market in 2025. Capital equipment procurement for PET-CT scanners, SPECT systems, and cyclotron production infrastructure represents the highest-value individual procurement category. Each new hospital imaging centre or department upgrade generates capital equipment revenue that establishes the installed base whose ongoing clinical use creates radiopharmaceutical and service revenue. Siemens Healthineers, GE Healthcare, and Philips collectively define the premium systems market whose installed base and replacement cycle sustain consistent capital equipment procurement.

Radiopharmaceuticals are the fastest-growing product category because their consumption model creates recurring revenue that scales with procedure volume and expands with each new clinical indication approved. Unlike systems purchased once per multi-year refresh cycle, radiopharmaceuticals are consumed per procedure, creating revenue that grows proportionally with imaging programme utilisation. Novel targeted imaging agents including PSMA-PET tracers, amyloid and tau agents, and fibroblast activation protein inhibitor tracers are creating new premium-priced radiopharmaceutical categories whose clinical adoption drives above-average market growth.

By End User, hospitals dominate, research institutes grow fastest

Hospitals retained the dominant end user position in the molecular imaging market in 2025. Hospital-based nuclear medicine departments and PET imaging centres operate the majority of the world’s molecular imaging systems and perform the largest volume of clinical procedures. Hospital procurement is driven by the combination of clinical demand, insurance reimbursement infrastructure, and the operational scale that justifies capital investment in high-cost imaging systems. Academic medical centres simultaneously serve clinical and research functions, creating dual procurement motivation that sustains the most technically advanced installed bases.

Research institutes are the fastest-growing end user segment because precision medicine programme investment, oncology clinical trial activity, and neurological disease research are creating above-average molecular imaging procurement in academic and commercial research settings. Clinical trials increasingly use PET imaging as a primary endpoint for drug response assessment, creating structured research imaging demand that grows proportionally with pharmaceutical R&D investment in oncology, neurology, and cardiology. Each new precision oncology programme launched at a major cancer research centre creates institutional molecular imaging infrastructure investment.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

76.0% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Molecular Imaging Market Insights

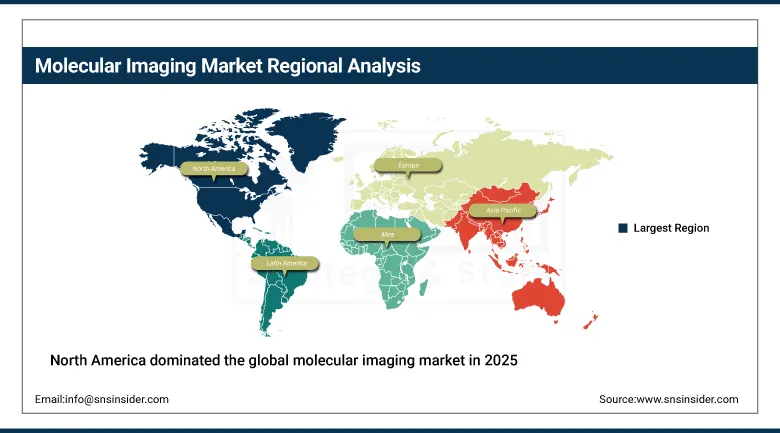

North America dominated the global molecular imaging market in 2025. The United States accounted for approximately 76% of North American revenues in 2025 driven by robust NIH and NCI research funding, high adoption of advanced diagnostic technology, and comprehensive Medicare reimbursement for PET imaging in oncology. The commercial presence of GE Healthcare, Lantheus, Curium, and Bracco creates a complete value chain of imaging systems and radiopharmaceuticals sustaining the most commercially active molecular imaging ecosystem globally.

Canada contributes approximately 24% of North American revenues through its publicly funded health system’s molecular imaging investment, active cancer research programmes, and growing theranostics clinical adoption across major academic medical centres in Toronto, Vancouver, and Montreal.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Molecular Imaging Market Insights

Europe is a technically sophisticated molecular imaging market where national health system reimbursement frameworks, EU Horizon research funding for medical imaging innovation, and the presence of Siemens Healthineers, Philips, and IQVIA Biotech create a comprehensive molecular imaging ecosystem. Germany accounts for approximately 22.3% of European revenues through its advanced hospital infrastructure, active oncology research centres, and Siemens Healthineers’ domestic market presence.

The United Kingdom, France, and the Netherlands are significant secondary markets where NHS and equivalent public health system molecular imaging programmes, clinical research networks, and pharmaceutical industry clinical trial activity create consistent institutional demand. European regulatory approval of novel radiopharmaceuticals through EMA is progressively expanding the available agent portfolio that sustains procedure volume growth.

Asia Pacific Molecular Imaging Market Insights

Asia Pacific is the fastest-growing regional molecular imaging market, driven by healthcare infrastructure development across China, India, Japan, South Korea, and Australia. China accounts for approximately 44.8% of Asia Pacific revenues through the Healthy China 2030 initiative’s diagnostic infrastructure investment, growing cancer incidence, and expanding private hospital molecular imaging centre development. Japan’s high cancer incidence and ageing population create above-average per-capita molecular imaging demand whose commercial scale sustains consistent system and radiopharmaceutical procurement.

India represents the most commercially dynamic emerging molecular imaging market. The expanding private hospital sector is installing PET-CT and SPECT systems in tier-1 and tier-2 cities. Government investment in affordable cancer screening and the growing theranostics clinical programme in PSMA-targeted prostate cancer therapy are creating structured institutional imaging demand that was minimal five years ago.

MEA & Latin America Molecular Imaging Market Insights

The Middle East and Africa and Latin America are growing molecular imaging markets where healthcare infrastructure investment, rising cancer incidence, and government health system modernisation are creating structured demand for diagnostic imaging capability. Saudi Arabia leads MEA revenues at approximately 31.2% through Vision 2030’s healthcare infrastructure programme, the National Cancer Institute’s oncology imaging investment, and above-average private healthcare sector sophistication in Riyadh and Jeddah.

Brazil leads Latin American revenues at approximately 44.2% through its oncology clinical infrastructure, INCA (National Cancer Institute) research programmes, and a growing private hospital sector whose cancer treatment capabilities are creating proportional molecular imaging investment. The public SUS system’s progressive incorporation of PET-CT for oncology staging is creating volume growth across Brazil’s large patient population.

Market Dynamics

Growth Drivers: Rising cancer and neurological disease prevalence and novel radiopharmaceutical approvals expanding clinical indications

Rising global cancer and neurological disease incidence is the molecular imaging market’s most structurally reliable growth driver. Global cancer incidence exceeds 20 million new cases annually and is growing with ageing populations. Each new cancer patient requires imaging at diagnosis, during treatment, and for surveillance. Alzheimer’s disease affects over 55 million people globally and the FDA approval of amyloid-lowering therapies whose patient selection requires amyloid PET confirmation has created a new structured imaging requirement that did not exist commercially before 2023.

Novel radiopharmaceutical approvals are expanding molecular imaging’s clinical addressable market with each new agent gaining regulatory approval and reimbursement. PSMA-PET tracers for prostate cancer, amyloid and tau agents for Alzheimer’s, FDG PET’s expanding oncology indications, and fibroblast activation protein inhibitor tracers for solid tumour imaging each represent new clinical use cases whose commercial adoption creates procedure volume growth independent of system installed base changes.

Restraints: High system cost limiting adoption in cost-constrained healthcare systems and radiopharmaceutical supply chain complexity

The high capital cost of PET-CT and SPECT/CT systems, whose acquisition pricing ranges from USD 1 million to over USD 3 million per unit, creates access limitations in developing market healthcare systems and smaller hospital facilities whose capital budgets cannot accommodate molecular imaging infrastructure without government funding support or shared service arrangements. This cost barrier concentrates high-technology molecular imaging in academic medical centres and major hospital networks, limiting the geographic reach of clinical service.

Radiopharmaceutical supply chain complexity creates operational challenges from the short half-lives of most diagnostic imaging agents. Fluorine-18 has a 110-minute half-life requiring co-location of cyclotron production with PET imaging facilities or rapid regional distribution from dedicated production centres. This logistical constraint limits rural and remote facility access to PET imaging and creates supply disruption risk from cyclotron maintenance downtime that conventional pharmaceutical supply chains do not face.

Opportunities: Theranostics integration creating combined diagnostic and therapeutic demand, AI-enhanced image analysis, and Asia Pacific infrastructure development

Theranostics represents the most commercially transformative molecular imaging opportunity because it fundamentally changes the economic model from standalone diagnostic to integral component of a precision therapy programme whose combined diagnostic and therapeutic value justifies above-standard reimbursement. PSMA-targeted prostate cancer theranostics programmes using PSMA PET for staging and PSMA-targeted lutetium therapy create imaging demand tied directly to therapeutic programme volume. Each patient entering a theranostics programme requires multiple imaging studies whose aggregate value exceeds standalone diagnostic imaging economics.

AI-enhanced molecular imaging analysis is creating commercial value by improving diagnostic accuracy, reducing reading time per study, and enabling quantitative functional assessment that manual image interpretation cannot achieve consistently at volume. AI platforms that automatically segment lesions, quantify SUV metrics, and compare serial imaging studies accelerate radiologist workflow and create reimbursable quantitative reporting capabilities whose clinical value sustains premium software procurement alongside capital system investment.

Recent Developments:

-

2023: The FDA approved Siemens Healthineers’ new PET-CT scanner in 2023, enhancing imaging resolution for early cancer detection, demonstrating the regulatory advancement of next-generation molecular imaging instrumentation whose improved sensitivity expands the patient population benefiting from PET-based cancer staging.

-

2023: GE Healthcare launched a next-generation SPECT/CT system in late 2023, improving diagnostic efficiency in cardiology and oncology through enhanced image quality and reduced scan time that improves patient throughput in high-volume nuclear medicine departments.

-

2024: Lantheus Holdings expanded PYLARIFY commercial access in 2024 by achieving broader Medicare coverage across additional prostate cancer clinical indications, demonstrating the progressive reimbursement expansion pathway for novel diagnostic radiopharmaceuticals whose clinical evidence accumulation sustains coverage broadening.

Molecular Imaging Market Key Players

-

GE Healthcare

-

Siemens Healthineers

-

Philips Healthcare

-

Canon Medical Systems

-

Hitachi Medical

-

Toshiba Medical Systems

-

Bracco Diagnostics

-

Lantheus Holdings

-

Curium

-

Positron Corporation

-

Navidea Biopharmaceuticals

-

Molecular Templates

-

IBA

-

Sofie Biosciences

-

NovaBay Pharmaceuticals

Molecular Imaging Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 9.25 Billion |

| Market Size by 2035 | USD 14.23 Billion |

| CAGR | CAGR of 4.5% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Modality (SPECT, PET-CT, PET, MRI, Others) • By Application (Oncology, Neurology, Cardiology, Others) • By Product (Systems/Equipment, Radiopharmaceuticals, Software) • By End User (Hospitals, Research Institutes, Diagnostic Centres, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | GE Healthcare, Siemens Healthineers, Philips Healthcare, Canon Medical Systems, Hitachi Medical, Toshiba Medical Systems, Bracco Diagnostics, Lantheus Holdings, Curium, Positron Corporation, Navidea Biopharmaceuticals, Molecular Templates, IBA, Sofie Biosciences, NovaBay Pharmaceuticals |

Frequently Asked Questions

The Molecular Imaging Market is expected to grow at a CAGR of 4.5% from 2026 to 2035.

The Molecular Imaging Market was valued at USD 9.25 Billion in 2025.

Rising global cancer and neurological disease incidence creating clinical imaging demand, novel radiopharmaceutical approvals expanding the addressable molecular imaging market into new disease categories, and theranostics programme growth creating combined diagnostic and therapeutic procurement that sustains above-average clinical imaging volume.

SPECT dominated the Molecular Imaging Market with 42% share in 2025, while PET-CT is the fastest growing modality.

North America dominated the Molecular Imaging Market in 2025, with the United States accounting for approximately 76% of North American revenues.

Get in Touch