Medical Transcription Software Market Report Size Analysis:

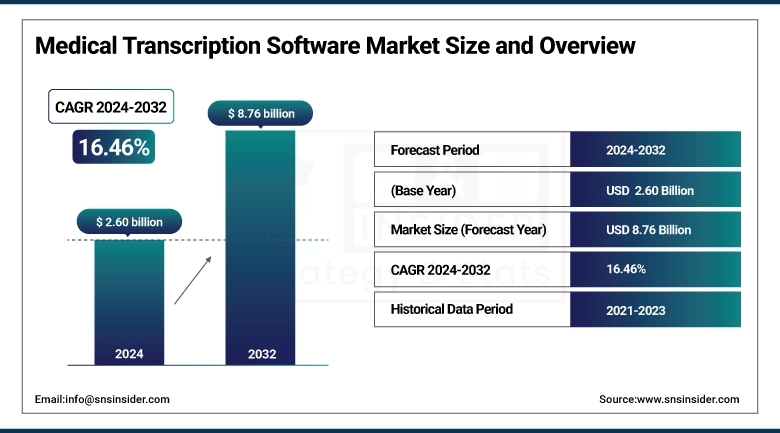

The Medical Transcription Software Market size was valued at USD 2.60 billion in 2024 and is expected to reach USD 8.76 billion by 2032, growing at a CAGR of 16.46% over the forecast period of 2025-2032.

The global medical transcription software market is expanding robustly with increasing need for efficient clinical documentation, increased adoption of electronic health record integration, and enhanced voice recognition and artificial intelligence technology. Healthcare professionals utilize these technologies to reduce administrative burdens and improve accuracy in medical reporting. The transition toward cloud-based transcription tools and increasing telehealth services further drives market growth. Growing markets, especially those in Asia Pacific, are driving future growth with increased healthcare digitization initiatives.

To Get more information on Medical Transcription Software Market - Request Free Sample Report

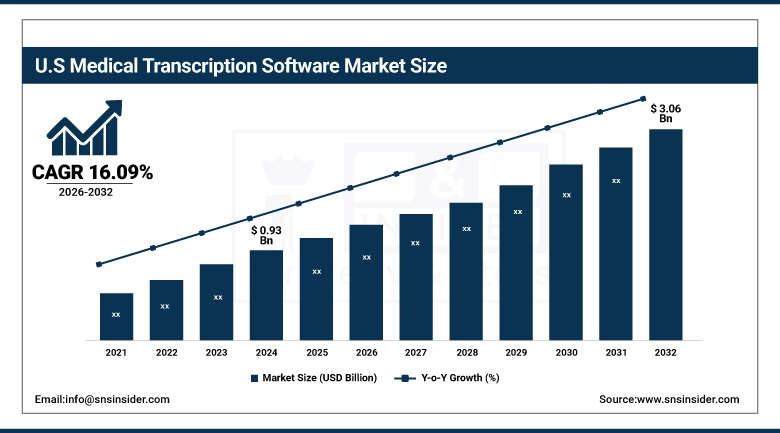

The U.S. medical transcription software market size was valued at USD 0.93 billion in 2024 and is expected to reach USD 3.06 billion by 2032, growing at a CAGR of 16.09% over the forecast period of 2025-2032. The U.S. leads the North American medical transcription software market owing to its sophisticated healthcare infrastructure, adoption of electronic health records (EHR), and heavy investment in AI and speech recognition technologies.

For instance, according to NCBI, Quantitative information collected from EHR systems, medical transcription software, and speech recognition (SR) products exhibited significant improvements in provider satisfaction, documentation quality, and operational efficiency as a result of SR technology implementation. The research reported an 81% decrease in monthly transcription expenses, an increase in electronic clinical documentation adoption from 20% to 77%, and a 74% total adoption rate of SR products.

The existence of prominent players, such as Nuance Communications and 3M, also consolidates the leadership of the U.S. Furthermore, growing demand for effective and accurate clinical documentation within healthcare institutions has helped to maintain the leadership of the U.S. in the market.

Medical Transcription Software Market Dynamics:

Drivers:

-

Adoption of Electronic Health Records (EHRs) is Driving the Market Growth

The increased use of EHR systems among healthcare institutions has dramatically driven the need for medical transcription software market trends. These applications exist natively on EHR platforms, enabling clinicians to transcribe voice notes into clear digital records with ease. This integration delivers 100% documentation accuracy and helps users to reduce manual entries, making it more efficient for the workflow. As healthcare providers become more concentrated on digitization and interoperability, transcription software is now a part of the digital documentation infrastructure.

There was a major change in 2024 toward cloud-based EHR systems, providing scalability, cost-effectiveness, and accessibility. The systems ensured flexible data storage, improved security with built-in encryption, and guaranteed disaster recovery options, turning out to be game-changers for organizations earlier struggling with data storage and access bottlenecks.

-

Advances in Voice Recognition and AI Technologies are Propelling the Market Growth

The latest advancements in voice recognition and artificial intelligence (AI) have transformed the art of medical transcription. AI-powered transcription programs can now recognize medical jargon, comprehend numerous accents, and provide near real-time documentation with high accuracy. Natural language processing (NLP) and machine learning technologies enhance transcription performance on an ongoing basis by learning from user feedback. These advancements accelerate transcription, reduce errors, and lower manual corrections, making the technology more reliable and attractive to healthcare professionals.

For instance, according to the Financial Times, Investment in AI-based medical note-taking applications increased in 2024, more than doubling from USD 390 million in 2023 to USD 800 million. Microsoft, Amazon, and some startups, including Nabla and Corti, are creating AI-based tools that enable doctors to create clinical summaries and transcripts in no time to enhance patient interactions.

Restraints:

-

Inaccuracy in Voice Recognition Tools is Restraining the Medical Transcription Software Market Growth

Even as voice recognition technology has come a long way, there are problems in ensuring consistency of accuracy, especially in complex medical settings. Accent, dialect, background noise, and uneven speech speeds or clarity can all affect the transcription quality. Moreover, medical vocabulary is often obscure and highly technical and, therefore, can be misinterpreted or inadequately documented if the software lacks advanced medical language processing features. These inaccuracies not only hasten the need for human intervention corrections but also present the possibility of potential medical errors, discouraging some medical professionals from entirely relying on these devices.

Medical Transcription Software Market Segmentation Analysis:

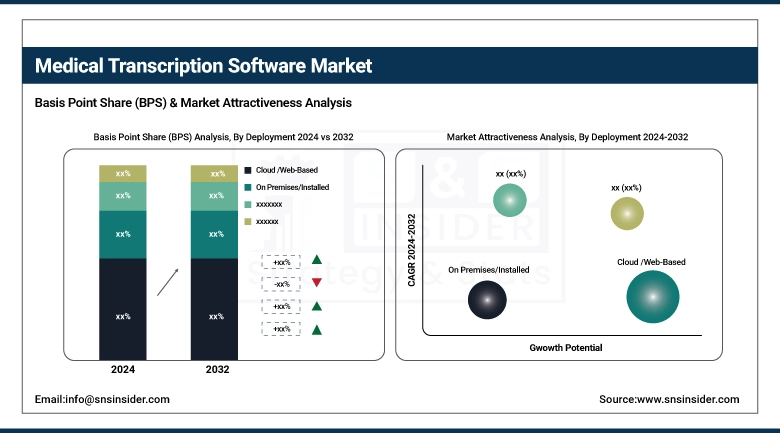

By Deployment

The cloud/web-based medical transcription software segment led the market, with a share of approximately 40% in the market in 2024, as it is scalable, cost-effective, and flexible. Cloud-based solutions are designed with ease of access in mind across sites and devices, making them ideal for multi-site hospitals, telemedicine platforms, and even outpatient clinics. These systems eliminate the need for massive upfront investment in infrastructure and offer real-time reporting, automated backups, and enhanced collaboration between healthcare professionals. Furthermore, cloud-based solutions tend to integrate seamlessly with electronic health record (EHR) systems, making workflow easier and documentation quality better. Increasing demand for telehealth services and the global shift toward digital health further solidified the dominance of cloud-based transcription software.

The on-premises/installed segment is expected to experience the highest growth during the forecast period due to the increasing security concerns regarding data, patient privacy, and compliance. In most nations with stringent data privacy laws or without adequate cloud infrastructure, the majority of large healthcare centers and specialty clinics insist on on-premises deployments to keep sensitive patient data close. On-premises systems are more adaptable when it comes to customization and do not rely on internet connectivity to operate, hence suitable for applications where network connectivity is an unknown factor.

By Type

The voice recognition segment led the medical transcription software market share with an 86.28% in 2024, as it can offer real-time, accurate, and efficient clinical documentation. The technology converts spoken words directly into formatted text, reducing healthcare professionals' time spent on manual data entry by a significant amount. Speech recognition software, such as Nuance's Dragon Medical One, has built-in superior AI and natural language processing (NLP), which is far more precise and attuned to various accents, medical jargon, and physicians' speech patterns. Speech recognition is the answer for medical transcription since the need for efficient workflows, enhanced physician productivity, and less administrative workload in hospitals and clinics keeps on rising.

The voice capture segment is anticipated to expand the fastest over the years of forecast period because healthcare professionals more and more adopting solutions that are flexible and interoperable. Voice capture technology allows clinicians to record medical conversations, which can be later transcribed and processed either by artificial intelligence or human transcriptionists. This is conducive to an asynchronous documentation style where physicians can consult patients and work on documentation later at their convenience. Growing adoption of voice capture solutions for mobile and remote healthcare documentation, particularly in regions that are broadening their telehealth program, is another factor contributing to the rising demand for these solutions.

By End-User

The clinician segment had the largest share in the market for medical transcription software, with a 76% share of the market in 2024, since the requirement for recording is an elementary need in all clinical specialties. General physicians, internists, and other specialists have a huge number of patient encounters daily, and complete medical records need to be processed with fast, reliable, and precise transcription solutions. As administrative workload grows and documentation demands to support reimbursement and quality reporting accrue, clinicians are moving toward automated transcription technology. It minimizes wasteful workflows, stops burnout, and provides doctors more face time with patients and less paperwork time, the most popular transcription software for consumers.

The radiologist's segment will experience the most rapid expansion during the forecast period due to the high quantity and technical complexity of image-associated reports to be recorded on a timely basis accurately. Radiologists are supposed to produce detailed interpretations of the diagnostic images that must be transcribed correctly for use in patient management, referrals, and planning for treatment. As medical professionals are increasingly leveraging imaging for diagnosis, automated and simplified transcription in radiology departments is a growing requirement.

By End-user Facility

The hospitals segment dominated the medical transcription software market with a market share of 92.14% in 2024 due to their huge patient volumes, complex workflows, and pervasiveness of the need for detailed medical documentation across numerous departments. Hospitals heavily depend on the timely and accurate transcription of proposals for continuity of care, healthcare regulations, and billing. Growing adoption of Electronic Health Records (EHRs) along with more advanced speech recognition technology meant that larger health systems made medical transcription software an integrated part of their electronic infrastructure.

The clinics segment is expected to experience the highest growth during the forecast period, as smaller healthcare centers are quickly adopting digital solutions to improve productivity and patient care. Clinics are resorting to medical transcription software to minimize manual record-keeping, lower administrative burden, and improve productivity, especially in resource-constrained settings. With cloud-based and mobile-optimized transcription solutions becoming more affordable and accessible, clinics can adopt them without the need for large-scale IT infrastructures.

Regional Analysis:

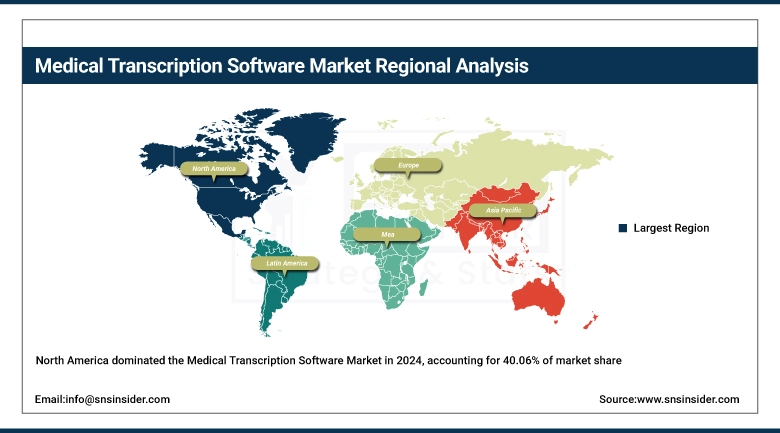

North America accounts for 40.06% of the market share in 2024, due to a highly developed healthcare system, large adoption of electronic health records (EHR), and strong market presence of players, such as 3M, Nuance Communications, and Aquity Solutions. The region has a large investment in speech recognition and artificial intelligence, the key building blocks of any modern transcription service. Additionally, the stringent regulatory environment, especially HIPAA in the U.S., has forced healthcare providers to adopt compliant and secure electronic documentation technologies. Likewise, the high physician workload and growing emphasis on minimizing administrative work have fueled the utilization of automated transcription software in specialty centers, clinics, and hospitals.

Get Customized Report as per Your Business Requirement - Enquiry Now

The Asia Pacific is the fastest-growing region in the market for medical transcription software, with a 17.16% market share during the forecast period due to the increased digitalization in the healthcare infrastructure, growing demand for cost-effective medical documentation, and increasing awareness about healthcare IT services. Countries like India, China, and Japan are investing in healthcare modernization aggressively and adopting telemedicine and digital record technology. The growing availability of English-speaking medical practitioners in countries such as India and the Philippines also contributes to the spread of transcription services.

Europe dominates the medical transcription software market analysis owing to its highly developed regulatory framework, highly developed healthcare infrastructure, and rising emphasis on digital health transformation. The majority of European countries have implemented national eHealth strategies, promoting the implementation of electronic medical records (EMR) and interoperable clinical documentation solutions, such as transcription software. The nation also has a high rate of multilingual physicians and healthcare practitioners, thus necessitating higher demand for stable and language-neutral transcription skills. Germany, the U.K., and France are among the top adopters of these technologies by their health IT system expenditure and growing focus on alleviating clinician burden by automation.

Latin America and the Middle East & Africa (MEA) witness moderate growth in the Medical Transcription Software Market, though driven by the gradual pace of adoption of healthcare IT solutions and the development of digital infrastructure. In Latin America, countries such as Brazil, Mexico, and Argentina are witnessing increasing investment in healthcare digitization and telemedicine, which is gradually fueling the demand for transcription solutions. However, expansion in the market is also restrained, in part, by limited financial resources, low availability of leading-edge technology in rural areas, and slower-than-foreign countries' integration into electronic health records (EHR).

Medical Transcription Software Market Key Players:

The major medical transcription software companies competing in the market are 3M Company, Nuance Communications, Aquity Solutions, nThrive, Global Medical Transcription, Mediscribes, RevMaxx AI, EHR Transcriptions, iScribes, VDIworks, SmartMD, and other players.

Recent Developments in the Medical Transcription Software Market:

-

February 2024 – RevMaxx AI introduced its groundbreaking AI Medical Scribe App, which captures and transcribes medical discussions in real-time. The app automatically creates precise SOAP notes and medical codes through sophisticated artificial intelligence, aiming to alleviate administrative tasks from physicians and improve their attention to patient care.

-

March 2023 – Nuance Communications, Inc., a Microsoft company, announced the launch of Dragon Ambient eXperience (DAX) Express, a fully automated clinical documentation solution. This innovative application is the first to integrate advanced conversational and ambient AI with OpenAI’s GPT-4, streamlining clinical workflows through real-time, AI-driven documentation.

Medical Transcription Software Market Report Scope:

Report Attributes Details Market Size in 2024 USD 2.60 Billion Market Size by 2032 USD 8.76 Billion CAGR CAGR of 16.46% From 2025 to 2032 Base Year 2024 Forecast Period 2025-2032 Historical Data 2021-2023 Report Scope & Coverage Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook Key Segments • By Deployment (Cloud/Web-Based, On-Premises/Installed)

• By Type (Voice Capture, Voice Recognition)

• By End-user (Radiologists, Clinicians, Surgeons, Others)

• By End-user Facility (Hospitals, Diagnostic Centers, Clinics, Others)Regional Analysis/Coverage North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) Company Profiles 3M Company, Nuance Communications, Aquity Solutions, nThrive, Global Medical Transcription, Mediscribes, EHR Transcriptions, iScribes, VDIworks, SmartMD, and other players.

Get in Touch