Metal Semiconductor Bonding Wire Market Size Analysis:

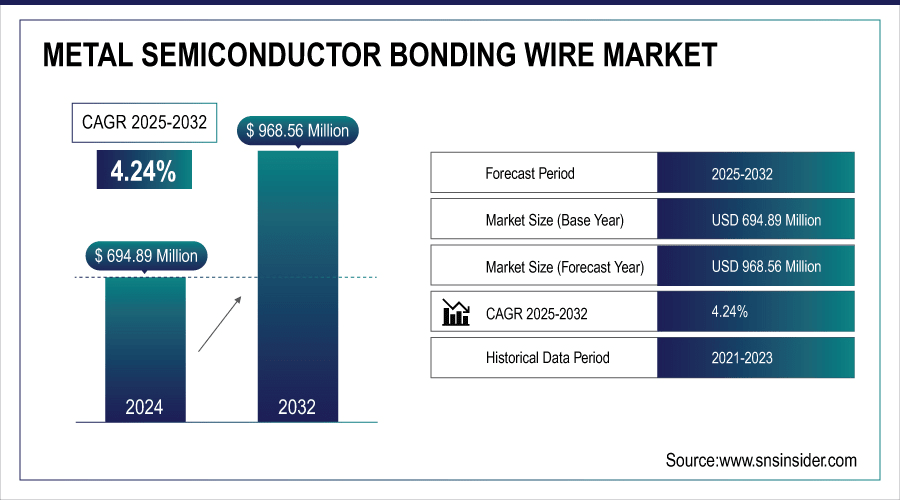

The Metal Semiconductor Bonding Wire Market size was valued at USD 694.89 Million in 2024 and is projected to reach USD 968.56 Million by 2032, growing at a CAGR of 4.24% during 2025-2032.

The Metal Semiconductor Bonding Wire market is growing at a rapid pace as electronic components drive demand for miniaturization and high performance across applications including consumer electronics, automotive, telecommunications and industrial market segments. Bonding wire continues to be a key interconnect technology as semiconductor nodes trend smaller and as packaging becomes more multi-dimensional, thanks to its low cost and versatility.

Metal Semiconductor Bonding Wire Market Size and Forecast

-

Market Size in 2024: USD 694.89 Million

-

Market Size by 2032: USD 968.56 Million

-

CAGR: 4.24% from 2025 to 2032

-

Base Year: 2024

-

Forecast Period: 2025–2032

-

Historical Data: 2022–2024

To Get more information on Metal Semiconductor Bonding Wire Market - Request Free Sample Report

Metal Semiconductor Bonding Wire Market Trends:

-

Rising demand for advanced packaging in consumer electronics and automotive semiconductors is driving bonding wire consumption, with automotive semiconductor demand growing over 12% annually.

-

Increasing shift toward copper bonding wires due to cost efficiency and higher conductivity, now accounting for over 65% of total bonding wire usage globally.

-

Expansion of power electronics and EV applications is boosting demand for high-reliability bonding wires, with the EV semiconductor market projected to grow above 20% CAGR.

-

Growth in 5G and high-performance computing is increasing adoption of fine-pitch and high-purity gold and silver wires, supporting 15–18% growth in advanced packaging segments.

-

Strong focus on miniaturization and thermal performance is accelerating R&D in alloy and coated bonding wires, improving reliability by 25–30% in high-temperature environments.

Although we retain the advantage of course as gold wires are more conductive and corrosion resistant, copper and silver variants are entering the market with greater cost benefits and thermal benefits. In addition, ultra-thin wires [4] have been enabled by packaging technology advances, such as fine-pitch architectures and stacked die architectures. Besides, IoT device, 5G infrastructure and AI chip are growing rapidly which makes adoption easier and faster.

Keysight Technologies Introduced its Electrical Structural Tester (EST)— A High - Throughput Wire Bond Inspection Solution for Semiconductors, which is capable of detecting minute wire defect such as bowl shape wire sag and stray wires by advanced nVTEP capacitive testing— equipped with up to 72,000 units/hour.

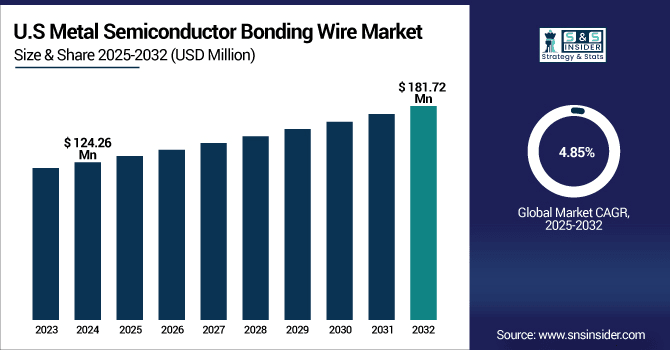

U.S Metal Semiconductor Bonding Wire Market Size Outlook

The U.S Metal Semiconductor Bonding Wire Market size was valued at USD 124.26 Million in 2024 and is projected to reach USD 181.72 Million by 2032, growing at a CAGR of 4.85% during 2025-2032. The growth of Metal Semiconductor Bonding Wire is driven by the growing U.S. semiconductor industry, the growing macrotrend towards microelectronic components integration and increased demand for durable, high performance packaging materials for logic, memory and analog devices.

The U.S. Metal Semiconductor Bonding Wire Market trends such as a shift toward copper and palladium-coated wires driven by their cost-effectiveness and superior conductivity compared to gold. Other notable trends include rising demand for fine-pitch, low-diameter wires, AI-enabled wire bond inspection, and increasing usage in automotive and aerospace applications requiring high-reliability semiconductor packaging.

Metal Semiconductor Bonding Wire Market Drivers:

-

Rising Demand for Clean Semiconductor Packaging Drives Adoption of Advanced Separation Technologies

The push for cleaner, high-yield semiconductor packaging is accelerating the adoption of advanced separation technologies. Innovations in temporary bonding materials and residue-free release methods are replacing traditional processes like laser ablation, which often generate soot and slow production. New approaches now offer rapid, damage-free wafer and package handling while maintaining high thermal and chemical resistance. These solutions support both front-end and back-end process cleanliness, aligning with the industry’s increasing standards for purity and yield. As semiconductor packaging becomes more complex and miniaturized, efficient and contamination-free handling techniques are becoming essential to preserve fabrication quality and throughput. This shift reflects how material science is driving manufacturing improvements across the global semiconductor value chain.

Resonac releases Xe flash-based debonding process and high-resistance bonding film for advanced IC packaging The solution accelerates the dry, contaminant-free segmentation of wafers and delivers significant speed, cleanliness and efficiency advantages over conventional laser-based techniques.

Metal Semiconductor Bonding Wire Market Restraints:

-

High Material Costs and Technological Shifts Limit Growth of Bonding Wire Market

The Metal Semiconductor Bonding Wire market faces significant restraints due to rising material costs, particularly for gold and palladium, which directly impact manufacturing expenses and product pricing. Additionally, the increasing complexity of semiconductor device architectures demands tighter bonding tolerances, challenging the compatibility of traditional bonding wires. Environmental regulations concerning the use of certain metals and lead-based solders further complicate production processes. Moreover, the industry is under pressure to adopt alternative packaging methods such as flip-chip and wafer-level packaging, which reduce the reliance on conventional wire bonding. These factors collectively limit market expansion, especially among cost-sensitive manufacturers and in regions with stringent environmental policies.

Metal Semiconductor Bonding Wire Market Opportunities:

-

Miniaturization and Performance Demands Are Creating New Growth Avenues for Wire Bonding Technologies

As electronics continue to miniaturize and demand higher performance, the wire bonding market is witnessing significant growth opportunities. The shift towards compact, high-density circuits in applications like aerospace, medical devices, and defense requires ultra-precise, ultra-fine wire bonding solutions. Material innovation such as the use of copper and palladium-coated wires is addressing both cost-efficiency and performance, helping manufacturers meet rising industry standards. Moreover, advancements in automated bonding equipment with micron-level accuracy are enabling next-generation packaging. Despite emerging alternatives like flip-chip technology, wire bonding’s proven reliability, established infrastructure, and compliance with critical standards maintain its dominance. These trends position the wire bonding industry to expand into advanced and high-reliability application areas, reinforcing its relevance in the future semiconductor interconnect ecosystem.

From copper to ultra-fine wire, wire bonding continues to be an essential process in semiconductor manufacturing; new materials and methods are constantly being developed to keep pace with miniaturization demands. While flip-chip is gaining ground as an alternative packaging approach, its reliability is unmatched, allowing it to remain integral in many of the most critical sectors, including aerospace and medical electronics.

Metal Semiconductor Bonding Wire Market Challenges:

-

Miniaturization, Material Constraints, and Emerging Packaging Alternatives Are Challenging the Growth of Metal Semiconductor Bonding Wire Market

The Metal Semiconductor Bonding Wire market faces several persistent challenges impacting scalability and efficiency. Heavy raw materials cost for gold and palladium especially, creates pressure onto profit margin and supply chain predictability. Although copper wire is cheaper, bonding it is more challenging because of oxidation, and requires careful control of the surrounding atmosphere. As devices shrink continues, ultra-fine pitch requirements need to be met at high speed through advanced equipment and extreme process accuracy. In addition, new bonding techniques such as flip-chip and 3D interconnection technologies are expected to supersede conventional bonding processes for high-density applications. Another expensive aspect is the testing and certification of products because they must adhere to stringent quality and reliability standards, especially in aerospace, medical, and automotive industries.

Metal Semiconductor Bonding Wire Market Segmentation Analysis:

By Material Type

In 2024, the Gold (Au) Wire segment accounted for approximately 65% of the Metal Semiconductor Bonding Wire Market share, owing to its superior conductivity, corrosion resistance, and reliability in critical applications. Despite rising material costs, gold wire remains the industry benchmark, particularly in aerospace, medical, and high-reliability semiconductor packaging where performance and precision are non-negotiable.

The Copper (Cu) Wire segment is expected to experience the fastest growth Metal Semiconductor Bonding Wire Market over 2025-2032 with a CAGR of 5.08%. This growth is driven by copper’s cost-efficiency, excellent electrical conductivity, and increasing adoption in high-volume consumer electronics. Innovations in coated copper wires further address reliability concerns, making it a compelling alternative to gold.

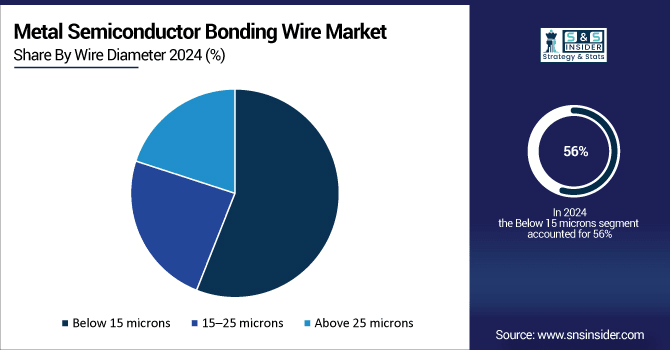

By Wire Diameter

In 2024, the Below 15 microns segment accounted for approximately 56% of the Metal Semiconductor Bonding Wire Market share, due to increased demand for miniaturized and high-density semiconductor devices. The leadership position in this segment highlights the progress being made in ultra-fine wire technologies for the precise and consistent bonding of fine wires in dense circuits being used in mobile devices, wearables, and high-performance packaging applications.

The Above 25 microns segment is expected to experience the fastest growth Metal Semiconductor Bonding Wire Market over 2025-2032 with a CAGR of 5.17%. The growth is driven by increasing demand for power devices and automotive electronics, where large wires improve current-carrying capacity, mechanical strength, and reliability for high-stress and high-temperature applications.

By Application

In 2024, the Consumer Electronics segment accounted for approximately 45% of the Metal Semiconductor Bonding Wire Market share, due to the high-volume manufacturing of smartphones, tablets and wearables. The growing need for compact, high-performance devices with greater functional capabilities is pushing the adoption of fine-pitch bonding wires worldwide for high-density semiconductor packaging in consumer technology applications.

The Automotive Electronics segment is expected to experience the fastest growth Metal Semiconductor Bonding Wire Market over 2025-2032 with a CAGR of 5.69%. The increase is propelled by the demand for EVs, ADAS and other in-vehicle infotainment systems. Models of high-performance bonding wire solutions are accelerating the demand for reliable, high-temperature interconnect in advanced automotive applications.

By End-Use Industry

In 2024, the Semiconductor Manufacturing segment accounted for approximately 50% of the Metal Semiconductor Bonding Wire Market share. This dominance is attributed to the surging global demand for advanced chips across sectors such as AI, consumer electronics, and cloud computing. Continuous investments in front-end fabrication facilities and packaging innovations are further boosting bonding wire usage in semiconductor production.

The MEMS Devices segment is expected to experience the fastest growth Metal Semiconductor Bonding Wire Market over 2025-2032 with a CAGR of 5.39%. This growth is driven by the rising need for miniaturized sensors and actuators within the automotive, healthcare, and consumer electronics industries. The increase in MEMS adoption owing to the growth of IoT and smart technologies is driving the consumption of bonding wires.

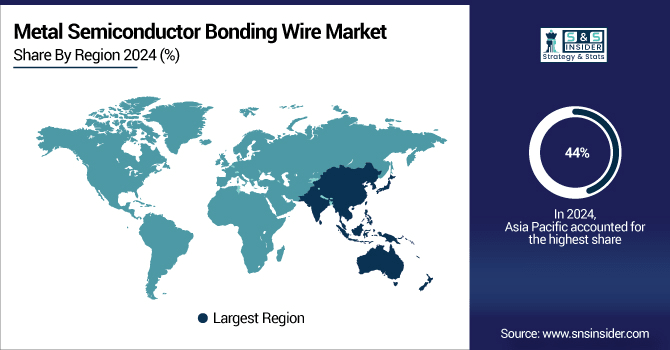

Metal Semiconductor Bonding Wire Market Regional Outlook:

In 2024, Asia Pacific dominated the Metal Semiconductor Bonding Wire Market and accounted for 44% of revenue share, owing to its strong semiconductor manufacturing infrastructure, with the most prominent fabrication leaders located in China, Taiwan, South Korea, and Japan. Persistent high demand for consumer electronics and a growth of automotive and industrial electronics are driving the region and ensuring that Asia Pacific remains the predominant area for the global wire bonding application base.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America is expected to witness the fastest growth in the Semiconductor Bonding Market over 2025-2032, with a projected CAGR of 5.87%. The fast growth is largely fueled by increasing investment in advanced semiconductor packaging, growing demand for automotive electronics, and government efforts to promote domestic chip making. The strong R&D ecosystem in the region also fuels innovation in bonding technologies.

In 2024, Europe maintained a well-sustained Metal Semiconductor Bonding Wire Market, supported by robust demand from the automotive and industrial sectors. The region's focus on electric vehicles (EVs), renewable energy systems, and precision electronics continues to drive steady consumption of high-performance bonding wires. Additionally, advancements in miniaturized electronics and MEMS devices further bolster market stability.

LATAM and MEA are experiencing steady growth in the Metal Semiconductor Bonding Wire Market, owing to the growth of electronics manufacturing in the region along with rising investment on telecommunications and automotive sectors. Figure 4: The region is driven by state-led industrialization initiatives and increasing demand for consumer electronics, and the associated adoption is sustained albeit at a moderate growth rate due to infrastructure barriers and lack of higher R&D intensity

Metal Semiconductor Bonding Wire Companies are:

The Key Players in Metal Semiconductor Bonding Wire Market are Heraeus Holding GmbH, Sumitomo Metal Mining Co., Ltd., AMETEK Inc., Tatsuta Electric Wire & Cable Co., Ltd., MKS Instruments Inc. (ESI), Tanaka Denshi Kogyo Co., Ltd., KOA Corporation, KANTO ELECTRONICS CORPORATION, TOWA Corporation, Palomar Technologies, Custom Chip Connections Inc., Microbonds Inc., Mitsui Mining & Smelting Co., Ltd., Toyo Seikan Group Holdings, Ltd., Nippon Micrometal Corporation, Wieland Group, Tungsten Corporation, Furukawa Electric Co., Ltd., Shinkawa Ltd., ASM Pacific Technology Ltd. and Others.

Recent News:

-

In Oct 2024, TANAKA Kikinzoku Kogyo launched “TK-SK”, a high-hardness palladium alloy (640HV) for probe pins in semiconductor test equipment, aiming to improve durability and reduce maintenance.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 694.89 Million |

| Market Size by 2032 | USD 968.56 Million |

| CAGR | CAGR of 4.24% From 2024 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Material Type(Gold (Au) Wire, Copper (Cu) Wire, Silver (Ag) Wire and Others (Platinum, Aluminum)) • By Wire Diameter(Below 15 microns, 15–25 microns and Above 25 microns) • By Application(Consumer Electronics, Automotive Electronics, Telecommunications and Industrial Electronics) • By End-Use Industry(Semiconductor Manufacturing, Integrated Circuit (IC) Packaging, LED Manufacturing and MEMS Devices) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | The Metal Semiconductor Bonding Wire Market companies are Heraeus Holding GmbH, Sumitomo Metal Mining Co., Ltd., AMETEK Inc., Tatsuta Electric Wire & Cable Co., Ltd., MKS Instruments Inc. (ESI), Tanaka Denshi Kogyo Co., Ltd., KOA Corporation, KANTO ELECTRONICS CORPORATION, TOWA Corporation, Palomar Technologies, Custom Chip Connections Inc., Microbonds Inc., Mitsui Mining & Smelting Co., Ltd., Toyo Seikan Group Holdings, Ltd., Nippon Micrometal Corporation, Wieland Group, Tungsten Corporation, Furukawa Electric Co., Ltd., Shinkawa Ltd., ASM Pacific Technology Ltd. and Others. |

Frequently Asked Questions

Ans: Asia-Pacific dominated the Metal Semiconductor Bonding Wire Market in 2024.

Ans: The “Gold (Au) Wire” segment dominated the Metal Semiconductor Bonding Wire Market

Ans: Rising demand for advanced semiconductor packaging and miniaturized electronic devices is driving growth in the Metal Semiconductor Bonding Wire Market.

Ans: The Metal Semiconductor Bonding Wire Market size was valued at USD 694.89 Million in 2024 and is projected to reach USD 968.56 Million by 2032

Ans: The Metal Semiconductor Bonding Wire Market is expected to grow at a CAGR of 4.24% during 2025-2032.

Get in Touch