Military Rotorcraft Market Report Scope & Overview:

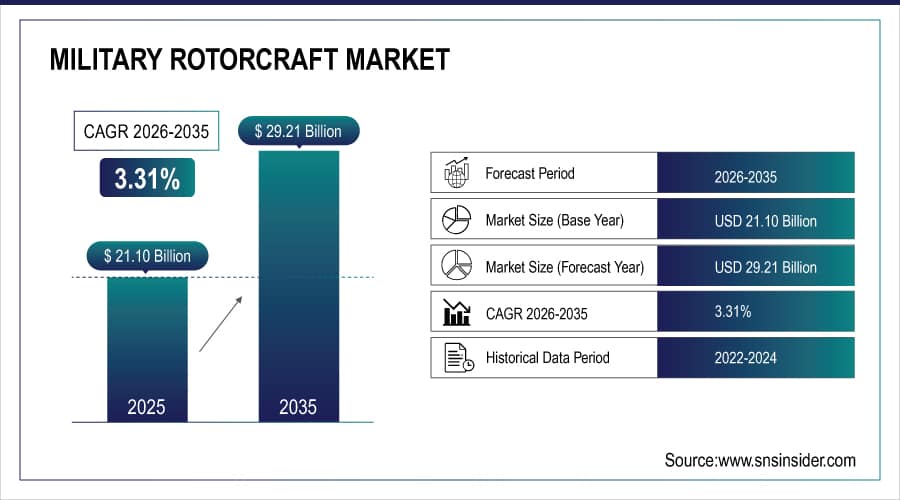

The Military Rotorcraft Market size is estimated at USD 21.10 billion in 2025 and is expected to reach USD 29.21 billion by 2035 and grow at a CAGR of 3.31% over the forecast period of 2026-2035.

The global military rotorcraft industry sector continues to grow, due to higher defense modernization programs and the demand for adaptable air platforms. military services around the world depend on rotorcraft for combat, troop transport, reconnaissance, search and rescue, and outreach missions. as more than 60% of the global fleet of military helicopters face mid-life or retirement, interest in upgrades, replacements and lifecycle support has grown. mobile avionics, flight controls, mission systems and survivability technologies are dramatically enhancing operating efficiency and readiness.

Market Size and Forecast:

-

Market Size in 2025: USD 21.10 Billion

-

Market Size by 2035: USD 29.21 Billion

-

CAGR: 3.31% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get More Information On Military Rotorcraft Market - Request Free Sample Report

Key Military Rotorcraft Market Trends:

-

Increasing fleet modernization initiatives to replace aging rotorcraft across major defense forces.

-

Rising demand for multi-role and heavy-lift helicopters to support complex combat and logistics missions.

-

Growing integration of advanced avionics, ISR systems, and electronic warfare capabilities.

-

Expansion of upgrade, retrofit, and MRO programs to extend rotorcraft service life and reduce costs.

-

Increased focus on interoperability and joint-force operations across allied defense organizations.

-

Growing investment in next-generation rotorcraft programs emphasizing speed, range, and survivability.

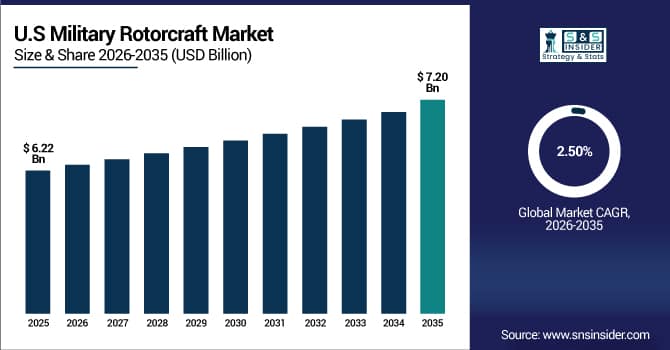

The size of the U.S. Military Rotorcraft Market is estimated to be USD 6.22 billion in 2025 and is projected to reach USD 7.20 billion by 2035, at a CAGR of 2.50% between 2025 to 2035 due to long-term commitments for modernizations, ongoing fleet recapitalization initiatives as well as new procurement programs coupled with an enhanced focus on increasing mission capable rates amidst combat operations and evolving requirements. Furthermore, modernization efforts as well as increased investments in avionics upgrades, survivability improvements and support services are some of the factors which keep bolstering the U.S. market outlook.

Military Rotorcraft Market Drivers:

-

Rising Defense Modernization and Fleet Replacement Programs Across Global Armed Forces

Growing defence modernization programs and the need to replace existing fleets of ageing helicopters are some of the key factors that would bolster military rotorcraft market. large numbers of military rotorcrafts in use today are 30 or more years old, resulting in excessive repair costs, lower mission readiness and unacceptable obsolescence relative to modern warfare needs. With the growing geopolitical complexity and increasing mission demands, militaries are focusing their procurement strategy on next-generation rotorcraft which can provide enhanced mobility, survivability, payload capability and multi-mission flexibility. Troop transport, ISR and combat support along with search and rescue/disaster response accounted for a single airframe in today’s modern day of warfare. As a result, the governments are investing more on their defense budgets to purchase modern platforms with smarter avionic systems and sensors that can perform network-centric operations.

In March 2025, a major defense ministry approved funding to accelerate replacement of legacy transport and attack helicopters with next-generation multi-role rotorcraft, strengthening procurement pipelines and driving market demand.

Military Rotorcraft Market Restraints:

-

High Procurement Costs and Complex Lifecycle Maintenance Limit Adoption of Advanced Platforms

Military Rotorcraft Market Restraint High purchase costs and complicated lifecycle maintenance add to the restraint factor for the Military Rotorcraft Market. Military rotorcraft including advanced avionics, composites, electronic warfare systems and mission-oriented payloads that contribute to the high costs of acquisition. These platforms also need special maintenance tools, trained folk and costly spare parts for their maintenance which will lead to high cost of operation throughout its life. A lack of funds may leave constraints on hard-pressed military budgets and this can lead to awkward decisions, delaying the purchase or using more obsolete equipment. This encourages some militaries to focus on more incremental upgrades rather than replacing their complete fleets, thereby slowing uptake of new-generation rotorcraft.

In October 2024, several defense agencies postponed new rotorcraft acquisition programs due to rising platform costs and sustainment challenges, opting instead for life-extension upgrades of existing fleets.

Military Rotorcraft Market Opportunities:

-

Development of Next-Generation Multi-Role and High-Speed Rotorcraft Unlocks Long-Term Growth Potential

Rising next-generation multirole and high-speed rotorcraft programs is a significant opportunity for the Military Rotorcraft Market. Nowadays, armed forces are tending more and more towards having a platform that can perform multiple mission profiles with the same adaptable aircraft to cut costs on complexity of fleets. Progress in propulsion systems, digital flight controls, lightweight materials and autonomous vehicles is paving the way for faster, longer-range and more survivable rotorcraft. Furthermore, increasing requirement for interoperability, quick deployment, and network-centric operations are also boosting the investments in emerging rotorcraft technologies. OEMs providing scalable, modular and future-proof designs stand to gain from long-term procurement programs and the global refresh trend in defense.

In June 2025, a leading defense contractor announced progress in high-speed military rotorcraft development, demonstrating extended range and enhanced mission flexibility, strengthening future procurement opportunities.

Military Rotorcraft Market Segmentation Analysis

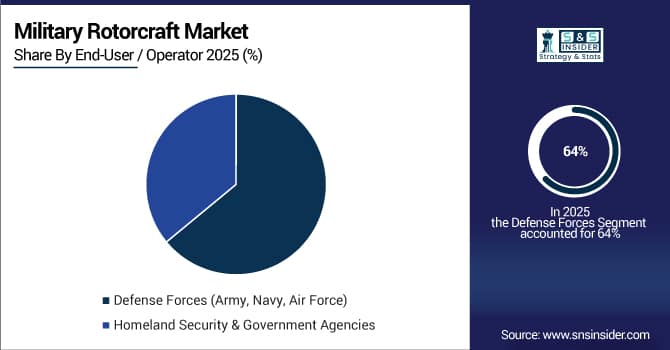

By End User, Defense Forces Segment Dominates Market with 64% Share in 2025, Homeland Security & Government Agencies Segment to Record Fastest Growth with 4.28% CAGR

The Defense Forces (Army, Navy, Air Force) segment dominated the Military Rotorcraft Market with a 64% revenue share in 2025, driven by sustained defense spending, fleet modernization programs, and increasing operational requirements across land, sea, and air domains. Armed forces all over the world are putting much money in highly capable rotorcraft to back up their combat, logistics and maritimes missions as well as quick reaction needs. Continued improvements in the areas of survivability, weapon integration, and mission systems only serve to bolster this segment’s leadership.

The Homeland Security & Government Agencies segment is expected to grow at the fastest pace, registering a CAGR of 4.28% during the forecast period, supported by rising border surveillance, disaster response, and internal security operations. Product developments emphasizing surveillance payloads, endurance, and rapid deployment capabilities are increasing rotorcraft adoption among non-military government agencies. This expanding operational scope is accelerating growth and enhancing the segment’s role within the Military Rotorcraft Market.

By Type, Attack Helicopters Segment Dominates Market with 43% Share in 2025, Transport Helicopters Segment to Record Fastest Growth with 5.37% CAGR

The Attack Helicopters segment occupied the major share at 43% of the total Military Rotorcraft sector in 2025 on account of growing geopolitical tension, asymmetric warfare and focus to carry out more close air support missions. The focus is on well-armed rotorcraft with precision guided weapons, advanced targeting systems and increased survivability. Uninterrupted product advancement by attackers aimed to deliver enhanced lethality, sensor fusion and electronic warfare capabilities have increased the operational effectiveness of attack helicopters, boosting its status as a market leader in terms of revenue share.

The Transport Helicopters segment is expected to register the fastest growth at a CAGR of 5.37% during 2026–2035, supported by growing demand for rapid troop deployment, transportation support, disaster relief and aeromedical evacuation. New designs for rotorcraft will become the backbone for modern military transport fleets due to their increased payload, range and multiple mission architectures. These developments enhance operational flexibility & multi-mission readiness, further pushing their faster induction cycle processes and extensively bolstering the Military Rotorcraft Market.

By Application, Combat / Attack Operations Segment Dominates Market with 42% Share in 2025, Surveillance & Reconnaissance Segment to Record Fastest Growth with 6.33% CAGR

The Combat / Attack Operations segment held the largest revenue share of 42% in 2025, leverages growth in the use of rotorcraft in front-line applications including combat, counter-terrorism, and border security. Armies meanwhile are modernising their combat helicopters with new fire-control systems, precision weapons and better armoured protection. These advances are directly contributing to mission effectiveness and survivability, helping maintain strong demand for procurement and upgrades, thereby reinforcing the dominance of this segment in the Military Rotorcraft Market.

The Surveillance & Reconnaissance segment is projected to grow at the fastest rate, with a CAGR of 6.33% from 2026–2035, driven by the increasing importance of intelligence, surveillance, and reconnaissance in modern warfare. System advancements utilizing the latest in EO sensors, real-time data flow and battlefield networking are providing around-the-clock situational awareness. This trend toward intelligence driven military operations is driving the demand for such products and boosts the contributions made by this segment to market growth.

By Weight / Size Class, Medium Military Helicopters Segment Dominates Market with 45% Share in 2025, Light Military Helicopters Segment to Record Fastest Growth with 5.08% CAGR

The Medium Military Helicopters segment accounted for the largest revenue share of 45% in 2025, driven by their balanced capability across transport, combat support, surveillance, and humanitarian missions. Medium-class helicopters also provide the best combination of payload, range, and endurance for a wide variety of multi-role military missions. Evolving products concentrating on advanced avionics, fuel efficiency and mission adaptability has led to fleet replacement programs around the world which is making it as the dominant segment in Military Rotorcraft Market.

The Light Military Helicopters segment is projected to grow at the fastest rate with a CAGR of 5.08% during 2026–2035, supported by rising demand for cost-effective platforms for training, reconnaissance, and light combat roles. Trending Defense News The trends in the defense industry show an increasing use of lightweight helicopters integrated with sophisticated sensors, digital cockpits, and create new modular weapons. The Updated supply chain provides greater operating flexibility and lifecycle savings faster time to revenue and overall market growth.

Military Rotorcraft Market Regional Insights:

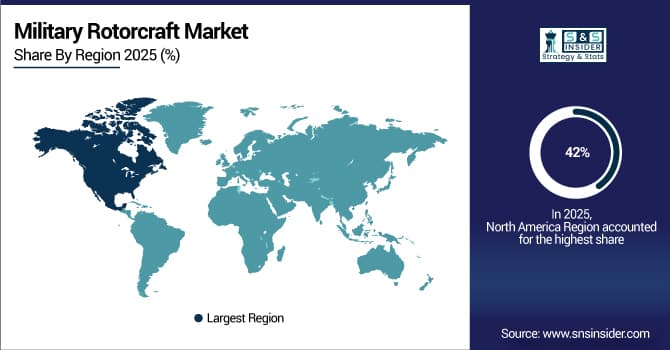

North America Dominates Military Rotorcraft Market in 2025

In 2025, North America commands an estimated 42% share of the Military Rotorcraft Market, driven by sustained defense spending, ongoing fleet modernization, and high operational demands. There are long-term procurement programs in place for attack, transport and multi-role helicopters as well as upgrade, maintenance and life extension projects. Rising investment in advanced avionics, survivability systems and mission-specific rotorcraft configurations will add growth momentum and underpin demand, making North America the leading region for military rotorcraft adoption and innovation.

The United States dominates the North American Military Rotorcraft Market due to its large-scale defense budget, global military reach and the globe’s biggest rotorcraft fleet. Regular refreshing of the fleet, as well as improvements for combat and transport logistics and naval operations, all maintain high levels of procurement. Extensive domestic manufacturing abilities, cutting-edge R&D initiatives, and decades-long defense contracts add to the U.S.'s standing in the region.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Asia-Pacific is the Fastest-Growing Region in Military Rotorcraft Market (2026–2035)

The Asia-Pacific Military Rotorcraft Market is projected to grow at an estimated CAGR of 5.49% during 2026–2035, fueled by rising geopolitical tensions, expanding defense budgets, and accelerated military modernization programs. Rising demand for attack, transport, and surveillance helicopters to support border security, naval expansion, and disaster response missions is driving rapid fleet expansion across emerging and established defense forces in the region.

China dominates the Asia-Pacific market due to its aggressive military expansion strategy and strong focus on indigenous rotorcraft development. The nation is also ramping up deployment of cutting-edge attack and transportation choppers to back land, naval and amphibious onslaughts. The procurement of military rotorcraft at a large scale, an increasingly budding domestic military helicopter development and manufacturing sector, and increased operational demands makes China the prime growth engine in the APAC market.

Europe Military Rotorcraft Market Insights, 2025

Europe held a significant share of the Military Rotorcraft Market in 2025, supported by fleet modernization programs, increased defense collaboration, and heightened readiness requirements across NATO member states. The requirement for multi-role rotorcraft capable of combat, maritime and humanitarian missions is driving the demand. France is dominating the European market as it has robust aerospace manufacturing sector and due to several ongoing military operations as well as procurement of missile-based attack helicopters & ship based anti-submarine helicopters. Stable market growth is also supported by regional defense collaboration.

Middle East & Africa and Latin America Military Rotorcraft Market Insights, 2025

In 2025, the Middle East & Africa Military Rotorcraft Market experienced steady growth supported by defense modernization efforts, counterterrorism operations, and border security requirements. Demand is on attack or transport helicopters, which have high levels of operating performances. Latin America also experienced some moderate growth, driven by domestic security, disaster response and military logistical needs. Both region's governments focus on adaptable and affordable rotorcraft programmes to maintain a steady presence in the market.

ilitary Rotorcraft Market Competitive Landscape:

Lockheed Martin Corporation

Lockheed Martin Corporation is a U.S.-based global defense and aerospace leader with a strong presence in the military rotorcraft market through advanced mission systems, avionics integration, sustainment, and lifecycle support. The company plays a critical role in enhancing the operational effectiveness of military helicopters by integrating advanced sensors, command-and-control systems, electronic warfare capabilities, and survivability solutions. Lockheed Martin supports attack, transport, and multi-role rotorcraft platforms used by defense forces worldwide, ensuring mission readiness, interoperability, and long-term fleet modernization. Its focus on digital engineering, advanced manufacturing, and sustainment services strengthens its leadership position in the military rotorcraft ecosystem.

-

In March 2025, Lockheed Martin expanded its rotorcraft sustainment portfolio by introducing next-generation avionics upgrade packages designed to enhance mission survivability and network-centric warfare capabilities for allied military helicopter fleets.

Airbus Helicopters

Airbus Helicopters is a global leader in military rotorcraft manufacturing, headquartered in Europe, with a comprehensive portfolio of light, medium, and heavy military helicopters. The company serves defense forces worldwide with platforms designed for combat, transport, maritime, and multi-mission operations. Airbus Helicopters is known for integrating advanced fly-by-wire systems, mission modularity, and fuel-efficient designs to enhance operational versatility. Its strong global support network, combined with long-term service contracts and modernization programs, enables sustained fleet performance and high availability rates across diverse operational environments.

-

In June 2025, Airbus Helicopters introduced enhanced mission configuration upgrades for its military rotorcraft platforms, improving payload flexibility and multi-role adaptability for land and naval operations.

Leonardo S.p.A.

Leonardo S.p.A. is an Italy-based global aerospace and defense company with a strong specialization in military helicopters and integrated defense systems. The firm designs and produces next generation rotorcraft for assault, transport, attack and special operations. Leonardo helicopters are known for their advanced avionics and mission adaptability. Vertically integrated from design to production, training and lifecycle support. High reliability and mission ready. The company cements its role in the military rotorcraft market globally through strategic partnerships with international defence forces.

-

In April 2025, Leonardo announced the expansion of its military helicopter upgrade and sustainment programs, focusing on enhanced mission systems and extended service life for existing rotorcraft fleets.

Military Rotorcraft Market Companies are:

-

Lockheed Martin Corporation

-

The Boeing Company

-

Airbus Helicopters

-

Leonardo S.p.A.

-

Russian Helicopters

-

Bell Textron Inc.

-

Hindustan Aeronautics Limited (HAL)

-

Korea Aerospace Industries (KAI)

-

Turkish Aerospace Industries (TAI)

-

AVIC Helicopter Company

-

MD Helicopters, Inc.

-

NHIndustries

-

Kawasaki Heavy Industries, Ltd.

-

Embraer S.A.

-

PZL-Świdnik

-

Denel Aeronautics

-

Changhe Aircraft Industries Corporation

-

AgustaWestland

-

Northrop Grumman

-

Safran Helicopter Engines

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | US$ 21.10 Billion |

| Market Size by 2035 | US$ 29.21 Billion |

| CAGR | CAGR of 3.31 % From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Attack Helicopters, Transport Helicopters, Multi-Mission Helicopters, Maritime / Naval Helicopters) • By Application (Combat / Attack Operations, Transport & Logistics, Search & Rescue (SAR), Surveillance & Reconnaissance) • By Weight / Size Class (Light Military Helicopters, Medium Military Helicopters, Heavy / Heavy-Lift Helicopters) • By End-User (Defense Forces (Army, Navy, Air Force), Homeland Security & Government Agencies) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Lockheed Martin Corporation, The Boeing Company, Airbus Helicopters, Leonardo S.p.A., Russian Helicopters, Bell Textron Inc., Hindustan Aeronautics Limited (HAL), Korea Aerospace Industries (KAI), Turkish Aerospace Industries (TAI), AVIC Helicopter Company, MD Helicopters, Inc., NHIndustries, Kawasaki Heavy Industries, Ltd., Embraer S.A., PZL-Świdnik, Denel Aeronautics, Changhe Aircraft Industries Corporation, AgustaWestland, Northrop Grumman, Safran Helicopter Engines |

Frequently Asked Questions

The Military Rotorcraft Market includes helicopters and other rotor-based aircraft designed for military missions such as combat, transport, surveillance, search and rescue, and medical evacuation.

Major types include attack helicopters, transport helicopters, multi-mission helicopters, and maritime or naval helicopters.

Combat and attack operations represent the dominant application due to sustained defense spending and the need for advanced battlefield capabilities.

North America leads the market, supported by strong defense procurement programs and the presence of major rotorcraft manufacturers.

Growth is driven by military modernization programs, rising defense budgets, demand for multi-role platforms, and increasing emphasis on surveillance and reconnaissance missions.

Get in Touch