Aerospace Titanium Machining Market Size & Trends:

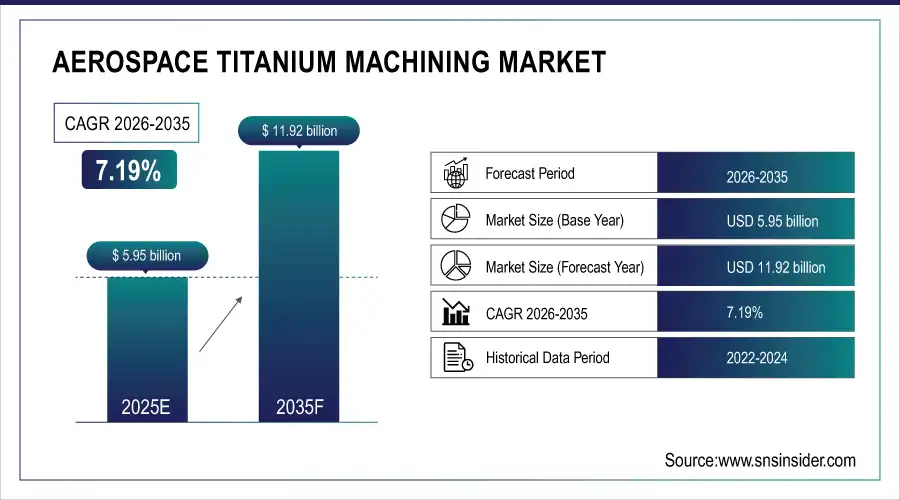

The Aerospace Titanium Machining Market size was valued at USD 5.95 billion in 2025 and is projected to reach USD 11.92 billion by 2035, growing at a CAGR of 7.19% during 2026–2035.

The market is experiencing substantial growth due to the increasing demand for light-weight and high-strength aerospace components. The corrosion-resistant, strong, and fuel-efficient characteristics of titanium alloys are critical in the commercial aviation, defense, and space industries. Advances in CNC machining, precision, and additive manufacturing are making it feasible to produce complex components. Increasing aircraft production, defense contracts, and the need for fuel-efficient and high-performance materials are driving the growth of the market.

Aerospace Titanium Machining Market Size and Forecast:

-

Market Size in 2025: USD 5.95 billion

-

Market Size by 2035: USD 11.92 billion

-

CAGR: 7.19% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Aerospace Titanium Machining Market - Request Free Sample Report

Key trends in the Aerospace Titanium Machining Market:

-

Rising demand for lightweight and fuel-efficient aircraft is increasing titanium adoption.

-

Growth in defense and space exploration programs is driving precision machining requirements.

-

Advancements in CNC, additive, and hybrid machining technologies are enabling complex, high-performance parts.

-

Focus on corrosion-resistant and high-strength materials is extending aircraft and component service life.

-

Increasing commercial and private aircraft production is broadening market opportunities.

-

Integration of smart manufacturing and automation is improving machining accuracy, productivity, and cost efficiency.

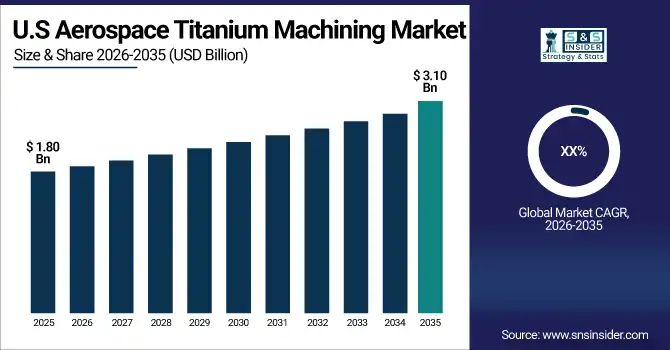

U.S. Aerospace Titanium Machining Market:

The U.S. Aerospace Titanium Machining Market was valued at USD 1.80 billion in 2025 and is projected to reach USD 3.10 billion by 2035, due to the escalating demand for high performance titanium parts used in commercial and military aircraft. Introduction of innovative machining technology, implementation of fuel efficient programs and establishment of aerospace manufacturing facilities are also supporting the market expansion.

Aerospace Titanium Machining Market Drivers:

-

Rising Demand for Lightweight and High-Strength Titanium Components in Commercial and Defense Aircraft

The increasing requirement for light-weight and high-strength titanium components in commercial and military aircraft is a major driver for the aerospace titanium machining market. Titanium alloys have better corrosion resistance, strength, and fuel efficiency compared to traditional aluminum and steel materials, thereby directly contributing to their demand in aircraft components and parts. The increasing aircraft production of models such as Boeing 737 MAX, Airbus A320neo, and defense modernization programs is also adding to the demand for precision machined titanium components. In addition, advancements in CNC machining, additive machining, and hybrid machining processes make it possible to produce complex shapes with high precision, thereby fueling the aerospace titanium machining market growth. Unwavering R&D investments in advanced titanium machining technology by OEMs and Tier-1 suppliers ensure that the industry is ready to meet the rising demands of aerospace production.

In March 2025, Boeing partnered with Spirit AeroSystems to co-develop and manufacture titanium machined components for next-generation commercial aircraft, demonstrating how rising aircraft production directly drives aerospace titanium machining demand.

Aerospace Titanium Machining Market Restraints:

-

High Production Costs and Complex Machining Challenges Limiting Titanium Adoption in Aerospace Manufacturing

Higher production costs and the machining process of titanium are major key constraints for the aerospace titanium machining market. Titanium mining, smelting, and billet preparation are energy and cost-intensive processes, and machining titanium alloys is a process that requires specialized tools, sophisticated cooling systems, and skilled operators. This results in higher production time, tool wear, and material scrap rates, thus making it unfeasible in terms of cost. Moreover, raw material availability and cost fluctuations are also major constraints for aerospace manufacturers, thus hindering the growth of the aerospace titanium machining market.

Aerospace Titanium Machining Market Opportunities:

-

Growth of Hypersonic and Space Launch Programs Driving Demand for Advanced Titanium Machined Components

The aerospace titanium machining market provides a vast opportunity, as the demand for hypersonic aircraft and space launch missions is increasing. Hypersonic aircraft and space launch missions demand materials that are lightweight, high-strength, and heat-resistant. This leads to an increase in the demand for titanium machining. As governments and aerospace companies invest in reusable launch vehicles and hypersonic aircraft, the demand for machined titanium components rises. The application of additive and hybrid manufacturing technology enhances the ability to machine large titanium components. This provides manufacturers with an opportunity to develop the capability to meet the high-performance requirements of specialized applications.

In August 2025, scientists were able to 3D-print a titanium fuel tank that could pass durability tests, showing the capabilities of additive machining in producing complex titanium parts that are lightweight and suitable for extreme aerospace conditions

Aerospace Titanium Machining Market Segmentation Analysis:

By Titanium Type, Titanium Alloys Segment Dominates with 47% Share in 2025, High-Temperature Titanium Alloys to Record Fastest Growth with 9.69% CAGR

The Titanium Alloys segment had a leading aerospace titanium machining market share of around 47% in 2025. The increasing requirement for lightweight and corrosion-resistant parts in commercial and military aircraft is fueling the market. Titanium alloys are in high demand for wing components, fuselage reinforcement, and engine mounting due to their high strength-to-weight ratio. Improvements in CNC machining and additive manufacturing are allowing for the accurate production of complex titanium parts.

The High-Temperature Titanium Alloys market is projected to register the highest growth rate during the forecast period of 2026-2035, with a CAGR of 9.69%. Rising demands for extreme environment components in jet engines, hypersonic aircraft, and space launch vehicles are driving the market. The machining technology provides an opportunity to manufacture high-strength and heat-resistant components such as turbine discs and exhaust systems, which are essential for aerospace applications.

By Application, Engine Components Segment Dominates with 29% Share in 2025, Space & Launch Vehicle Components to Record Fastest Growth with 12.16% CAGR

The Engine Components business has maintained a strong market share of 29% in the aerospace titanium machining market in 2025. Increasing deliveries of commercial aircraft and defense aircraft development programs boost the demand for machined titanium components such as fan blades, cases, and discs. Technological developments in CNC and multi-axis machining enable the production of complex engine components, thereby fueling the titanium machining market.

The Space & Launch Vehicle Components market is projected to register the highest growth rate during the period from 2026 to 2035 at a CAGR of 12.16%. Rising investments in reusable launch vehicles, hypersonic vehicles, and satellite development programs fuel the demand for high-strength and lightweight titanium alloys. Latest machining and 3D printing technologies make it possible to manufacture large and complex components like fuel tanks and structural frames, opening up new avenues in aerospace titanium machining.

By Aircraft Type, Commercial Aircraft Segment Dominates with 42% Share in 2025, UAVs Segment to Record Fastest Growth with 13.28% CAGR

The Commercial Aircraft business had a leading aerospace titanium machining market share of 42% in 2025. The demand for high-strength titanium parts in aircraft structures, landing gear, and engine assemblies is driven by new aircraft deliveries and the replacement fleet. The use of advanced machining processes supports precise manufacturing, which enhances fuel efficiency, strength, and aircraft performance, thereby driving titanium machining.

The UAVs market is projected to register the highest growth rate during the period from 2026 to 2035, with a CAGR of 13.28%. The increasing demand for military, surveillance, and delivery UAVs creates a demand for the production of lightweight and high-strength titanium components. Additive and precision machining enable the production of complex small-scale titanium parts, which optimize UAV performance and endurance, thereby increasing the aerospace titanium machining market in new UAV applications.

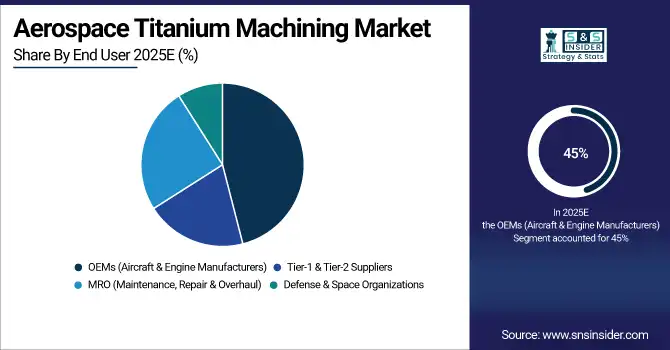

By End User, OEMs Segment Dominates with 45% Share in 2025, MRO Segment to Record Fastest Growth with 10.19% CAGR

The OEMs (Aircraft & Engine Manufacturers) segment held a prominent market share of 45% in the aerospace titanium machining market in 2025. The commercial and defense OEMs require a substantial number of machined titanium parts for engines, aircraft, and landing gear. Advancements in CNC machining and additive machining help in the rapid manufacture of complex parts, thus directly driving the market for titanium machining.

The MRO (Maintenance, Repair & Overhaul) market is expected to record the highest growth rate in the forecast period of 2026-2035, with a CAGR of 10.19%. With the increase in the age of aircraft and the maintenance cycle, the requirement for replacing titanium parts increases. The latest machining and 3D printing technology enables fast turnaround of high-strength parts for engines and structural assemblies, thus directly contributing to the growth of the aerospace titanium machining market.

Aerospace Titanium Machining Market Regional Insights:

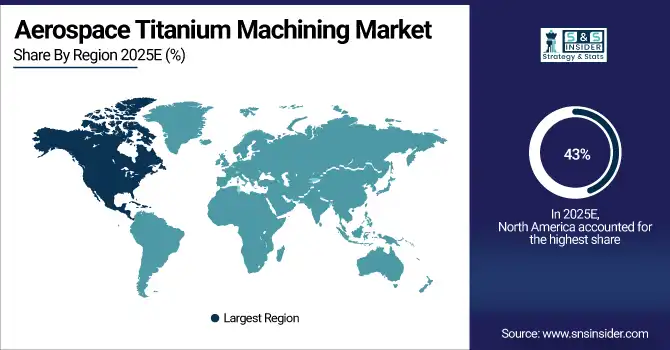

North America Dominates Aerospace Titanium Machining Market in 2025

In 2025, North America commands an estimated 43% share of the aerospace titanium machining market, due to its advanced aerospace manufacturing capabilities, high aircraft production rates, and defense modernization initiatives. The demand for high-strength, corrosion-resistant titanium components in airframes, engines, and UAVs is fueled by leading OEMs like Boeing, Lockheed Martin, and Northrop Grumman. Advances in CNC machining, additive manufacturing, and high-performance titanium alloys facilitate the production of complex geometries, thus fueling market dominance.

The market is dominated by the US with its highly developed infrastructure for aerospace industry, great number of commercial and military aircraft manufactures, and developed R&D sector. Technological advancements in machining and additive manufacturing allow U.S. manufacturers to meet difficult regulations and performance requirements. Moreover, the excessive count of government defence contracts & full- scale aircrafts development programs automatically leads to the consistent need for precision machined titanium parts which in turn maintains U.S market demand as it is credited with highest share contribution in North America market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia-Pacific is the Fastest-Growing Region in Aerospace Titanium Machining Market During 2026–2035

The Asia-Pacific region is projected to achieve a CAGR of 9.39% during the period 2026-2035, driven by the increasing demand for commercial aircraft manufacturing, the modernization of the defense industry, and the increasing production of UAVs. The establishment of aerospace infrastructure, R&D expenditure, and the use of advanced CNC and additive machining technology will have a direct positive influence on the demand for titanium components.

China holds the largest share in the Asia-Pacific aerospace titanium machining market, given its fast growing commercial aircraft industry and increasing defense programs. Such companies as COMAC and AVIC are ramping up production of regional jets and narrow-bodied planes, while UAVs and satellite programs need high-strength but lightweight titanium parts. Aggressive government investments in aerospace R&D, manufacturing capability and additive machining policy are allowing China to take the lead in market growth throughout the region.

Europe Aerospace Titanium Machining Market Insights, 2025

The aerospace titanium machining market in 2025 had a substantial presence in the European region, accounting for about 25% of the market revenue, mainly due to commercial aircraft manufacturing and defense programs. The high usage of advanced machining technology, along with regulatory compliance requirements, helps in the precise manufacturing of titanium components for engines, aircraft, and landing gear.

France dominates the European aerospace titanium machining market, as a result of key aircraft and engine production programs by Airbus and Safran. Ongoing investment in CNC machining, AM and advanced titanium alloys enables French suppliers to produce sophisticated lightweight components. Government backing of aerospace innovation and development of new large aircraft program is an added advantage that keeps France at the driver’s seat in Europe.

Middle East & Africa and Latin America Aerospace Titanium Machining Market Insights, 2025

In 2025, the Middle East & Africa market showed steady growth driven by defense modernization, regional airline expansions, and increased investments in precision titanium components. The UAE and Saudi Arabia lead the region with high adoption of aerospace technology and collaborations with global OEMs.

Latin America grew moderately in 2025, fueled mainly by Brazil and Mexico on the strength of commercial aircraft production at EMBRAER, ramped-up MRO facility growth, and defense modernization efforts. CNC and additive machining R&D investments contribute to improve the manufacturing of high-strength titanium components, while aerospace titanium machining-based solutions witness rising traction in the region.

Competitive Landscape for the Aerospace Titanium Machining Market:

Kennametal

Kennametal is a US-based company that is a leader in precision cutting tools and engineering solutions for aerospace titanium machining. The company focuses on carbide cutting inserts, drills, end mills, and reamers that are suitable for high-strength titanium alloys, which are used in engine parts, aircraft structures, and UAVs. The company has been involved in the aerospace tooling industry for several decades and is a leader in providing innovative solutions for precision CNC and additive machining. The company’s involvement in the aerospace titanium machining industry is very significant, as it provides high-performance tools that enhance efficiency and reduce wear on high-strength titanium components.

-

In March 2025, Kennametal launched its “AeroMax Ti-Series” carbide inserts, designed specifically for high-temperature titanium alloys, improving tool life by 25% and precision in machining complex aerospace components.

Sandvik Coromant

Sandvik Coromant is a Sweden-based global leader in tooling solutions for aerospace titanium machining. The company offers precision end mills, drills, turning inserts, and milling cutters engineered for machining titanium alloys in engines, landing gear, and structural components. Sandvik Coromant combines advanced material science with cutting-edge coating technologies to enhance tool durability, reduce machining forces, and improve surface quality. Its role in the aerospace titanium machining market is central, enabling manufacturers to achieve faster cycle times and higher precision while handling difficult-to-machine titanium materials.

-

In January 2025, Sandvik Coromant introduced the “Inveio Aero Coated End Mills,” designed for high-temperature titanium machining, enabling aerospace manufacturers to achieve tighter tolerances and improved productivity in critical engine and airframe parts.

FPD Company

FPD Company is a United States-based aerospace material expert in titanium machining and the production of titanium alloys. The company provides high-quality titanium plates, sheets, and precision-made parts for aircraft structures, engines, and UAS. With experience in precision forming, cutting, and surface finishing, FPD Company helps OEMs and MROs in providing lightweight and high-strength titanium parts. The impact of FPD Company on the aerospace titanium machining industry is significant, as it provides raw materials and finished parts that meet the stringent aerospace performance and regulatory standards.

-

In February 2025, FPD Company unveiled its “Ti-6Al-4V Pre-Machined Plates” for jet engine applications, designed for improved machinability and dimensional stability in high-performance aerospace parts.

Gould Alloys

Gould Alloys is a U.S.-based manufacturer specializing in aerospace-grade titanium alloys and precision machining services. The company produces high-performance titanium sheets, bars, and custom components for engines, landing gear, and structural airframe assemblies. Gould Alloys integrates advanced CNC and additive machining processes with alloy expertise to deliver components with high strength, corrosion resistance, and tight tolerances. Its role in the aerospace titanium machining market is pivotal, enabling OEMs and MRO providers to meet growing demand for lightweight, durable titanium parts while maintaining high-quality standards.

-

In May 2025, Gould Alloys launched its “G-Alloy Ti-64 Ultra Series,” a pre-machined titanium alloy bar optimized for high-temperature aerospace engine components, enhancing production efficiency and component durability.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | US$ 5.95 Billion |

| Market Size by 2035 | US$ 11.92 Billion |

| CAGR | CAGR of 7.19 % From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Titanium Type (Titanium Alloys, Commercially Pure Titanium, High-Temperature Titanium Alloys, Specialty / Beta Titanium Alloys) • By Application (Airframe Components, Engine Components, Landing Gear Components, Fasteners & Hardware, Control & Actuation Components, Space & Launch Vehicle Components) • By Aircraft Type (Commercial Aircraft, Military Aircraft, Business Jets, Helicopters & Rotorcraft, Unmanned Aerial Vehicles (UAVs), Spacecraft & Launch Vehicles) • By End User (OEMs (Aircraft & Engine Manufacturers), Tier-1 & Tier-2 Suppliers, MRO (Maintenance, Repair & Overhaul), Defense & Space Organizations) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Kennametal, Sandvik Coromant, FPD Company, Gould Alloys, RTI International Metals, Maniko, Protolabs, Dynamic Metal, Ural Boeing Manufacturing, Universal Metal, Precision Castparts Corp., Spirit AeroSystems Holdings Inc., Triumph Group Inc., GE Aerospace, Rolls-Royce Holdings plc, Safran SA, RTX Corporation, Allegheny Technologies Incorporated (ATI), VSMPO-AVISMA Corporation, GKN Aerospace |

Frequently Asked Questions

Kennametal, Sandvik Coromant, FPD Company, and Gould Alloys.

North America leads; Asia-Pacific is the fastest-growing region.

Engine components and airframe structures drive the highest revenue.

Titanium Alloys, due to strength, corrosion resistance, and wide aerospace applications.

Demand for lightweight, high-strength titanium components and advances in CNC and additive machining.

Get in Touch