Counter Drone System Market Report Scope & Overview:

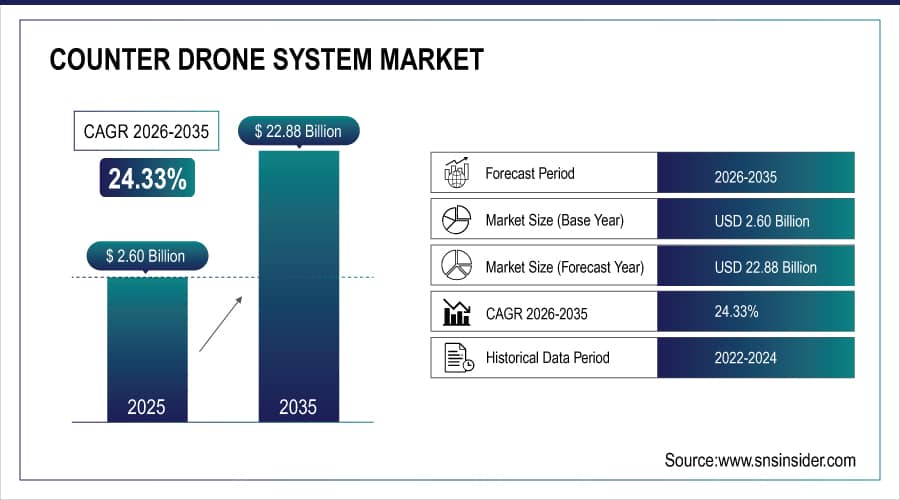

The Counter Drone System Market size is estimated at USD 2.60 billion in 2025 and is expected to reach 22.88 billion by 2035 and grow at a CAGR of 24.33% over the forecast period of 2026-2035.

The rapid growth of the Counter Drone System Market reflects the growing threat from unauthorized and hostile drone activities as they are proliferating rapidly across military, commercial and critical infrastructure sectors. Rising fears of security breaches, terrorism, and airspace violations are also spurring demand for sophisticated detection, tracking, and neutralization technologies. The combination of radio and radar frequency with AI-based oriented solutions facilitates better accuracy in threat identification and response. In addition, increasing utilization of drones in urban areas, government regulations controlling drone mitigation and increasing investment on defense and homeland security will further develop the market globally.

89% of global security agencies deployed integrated counter-drone systems combining radar, RF detection, and AI to address escalating unauthorized UAV threats and comply with new airspace regulations.

Market Size and Forecast

-

Market Size in 2025: USD 2.60 Billion

-

Market Size by 2035: USD 22.88 Billion

-

CAGR: 24.33 % from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get More Information On Counter Drone System Market - Request Free Sample Report

Counter Drone System Market Trends

-

Rising defense and homeland security investments to counter increasing threats from unauthorized and hostile unmanned aerial systems

-

Growing adoption of integrated detection and mitigation solutions combining radar RF electro-optical and AI technologies

-

Increasing deployment of counter-drone systems at airports critical infrastructure military bases and public venues

-

Advancements in electronic warfare and directed energy technologies enhancing neutralization accuracy and response speed

-

Rising demand for portable and vehicle-mounted counter-drone systems supporting tactical and rapid-response operations

-

Expansion of counter-drone applications driven by asymmetric warfare border security and urban airspace protection needs

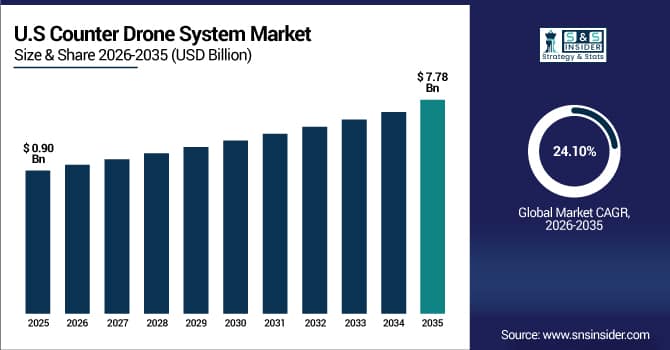

U.S. Counter Drone System Market Size Outlook:

The U.S. Counter Drone System Market is valued at USD 0.90 billion in 2025 and is expected to reach USD 7.78 billion by 2035, growing at a CAGR of 24.10 % from 2026-2035.

The proliferation of unauthorized and hostile drones has made around the military, critical infrastructure, and commercial sectors of the U.S. Counter Drone System Market expansive. Increasing security concerns and instituting government regulations, along with the increasing deployment of AI- and radar-based detection and neutralization technologies, which are primarily adoption-based and supported by investments in homeland security and defense solutions, are driving demand and enabling modest growth in the market.

Counter Drone System Market Growth Drivers:

-

Rising security threats from unauthorized drones near military bases, airports, and critical infrastructure are driving strong demand for advanced counter-drone detection and mitigation systems

The illegal use of drones for spying, smuggling, or terrorism has led to growing security concerns in the military, civilian and commercial fields. Unauthorized drone incursions, especially around critical infrastructure such as airports, power plants and government facilities, are particularly dangerous. This has led the governments to spend a lot of money on detection, tracking and neutralization of drones through counter-drone technologies that can respond in real time. These concerns are dealt with using advanced systems that work through radar, radio frequency and laser, which prevent these incursions and ensure safety and compliance. Booming knowledge of drone hazards keeps boosting growth of drone detection systems market globally.

87% of military and civilian security agencies deployed advanced counter-drone systems to counter rising threats from unauthorized UAVs near bases, airports, and critical infrastructure.

Counter Drone System Market Restraints:

-

High system costs, complex integration requirements, and limited interoperability with existing defense infrastructure restrict widespread adoption, especially among smaller security organizations and civilian operators

Counter-drone measures require expensive gear, such as radar, radio frequency jammers, and detection sensors, representing a major up-front cost. Fitting in with native security systems is mostly complicated because of the need for specialized systems and integration points. Costs and technical requirements could be prohibitive for smaller organizations, private facilities and civilian operators, which may limit market penetration. Moreover, inter-system lock-in due to lack of interoperability between systems from different vendors can limit the flexibility deployment options. This slows down overall market growth as it limits adoption among organizations with tighter budgets. Although these technologies are well advanced, the high initial financial and technical barrier it imposes will continue to restrain the counter drone system from being increasingly deployed in non-military sectors.

79% of smaller security and civilian operators avoided counter-drone systems due to high costs, complex integration, and poor interoperability with existing infrastructure.

Counter Drone System Market Opportunities:

-

Rapid technological advancements in AI-based detection, radar systems, and multi-sensor fusion create opportunities for more accurate, scalable, and cost-effective counter-drone solutions

Technological innovation taking over the counter-drone market to detect and neutralize drones in a quicker and more accurate manner. AI algorithms improve threat detection, while Fusion radar and multi sensor fusion offer real time tracking in a variety of environments. This improvement helps to make lower false positives and make large-scale deployment in case of use both in military and commercial applications. Cost-savings due to miniaturization, automation, and integration of several technologies are leading to more affordable solutions. Considerable opportunity to innovate, differentiate products, and identify new segments, capitalize on global expansion for market growth, through rapid detection, classification, and mitigation of threats to vendors.

86% of counter-drone systems leveraged AI, radar, and multi-sensor fusion to deliver accurate, scalable, and cost-effective protection against evolving drone threats.

Counter Drone System Market Segmentation Analysis

-

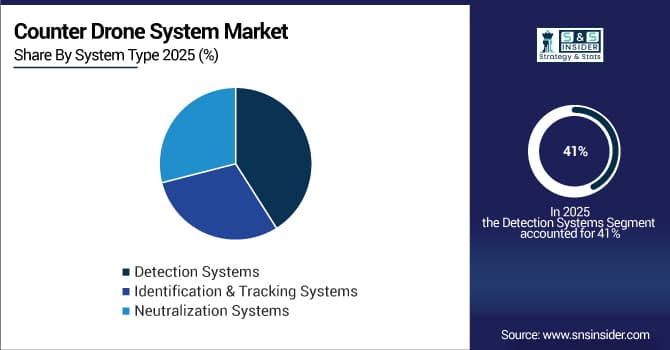

By System Type: Detection Systems led with 41% share, while Neutralization Systems is the fastest-growing segment.

-

By Technology: Radar-Based Systems led with 29% share, while Laser-Based Systems is the fastest-growing segment.

-

By Deployment Mode: Fixed Systems led with 38% share, while Man-Portable Systems is the fastest-growing segment.

-

By Application: Military & Defense led with 36% share, while Critical Infrastructure Protection is the fastest-growing segment.

-

By End-User: Defense Forces led with 34% share, while Airports & Aviation Authorities is the fastest-growing segment.

By System Type: Detection Systems led, while Neutralization Systems is the fastest-growing segment.

Detection systems dominate the counter-drone market due to their essential role in early identification of rogue or unauthorized UAVs. Equipped with radar, RF, and EO/IR sensors, these systems provide real-time situational awareness and threat alerts, forming the first line of defense. High adoption among defense, homeland security, and critical infrastructure operators ensures wide deployment.

Neutralization systems are the fastest-growing segment as militaries, airports, and critical infrastructure increasingly seek active countermeasures to disable unauthorized UAVs. The segment’s growth is further accelerated by advances in precision targeting, autonomous threat response, and integration with detection systems, making neutralization solutions a high-demand area in the counter-drone market.

By Technology: Radar-Based Systems led, while Laser-Based Systems is the fastest-growing segment.

Radar-based systems dominate due to their long-range detection capabilities and reliability under diverse weather and terrain conditions. These systems form the backbone of counter-UAV operations, enabling early warning and tracking of drones. High adoption rates and proven performance ensure radar remains the primary technology for drone threat mitigation in defense and civil applications globally.

Laser-based counter-drone systems are the fastest-growing technology segment due to their precision, speed, and effectiveness in neutralizing drones without collateral damage. Adoption is increasing in military, critical infrastructure, and airport security applications where active drone threats are high. Regulatory support for safe airspace and the need for rapid-response countermeasures drive strong growth, positioning laser systems as a high-potential technology in the counter-drone market.

By Deployment Mode: Fixed Systems led, while Man-Portable Systems is the fastest-growing segment.

Fixed systems dominate as they provide continuous, high-coverage monitoring and defense for sensitive sites such as military bases, airports, and power plants. High reliability, scalability, and automation make fixed installations the preferred choice for large-scale, high-priority operations. Widespread adoption in defense and government sectors ensures this segment remains the largest contributor to revenue and security coverage.

Man-portable systems are the fastest-growing segment, offering flexibility, rapid deployment, and mobility for defense personnel and law enforcement. Their growth is fueled by operational versatility, ease of transport, and ability to neutralize drones in dynamic or high-threat environments. Expanding demand from military, law enforcement, and security service providers positions man-portable systems as a high-growth segment in the counter-drone market.

By Application: Military & Defense led, while Critical Infrastructure Protection is the fastest-growing segment.

Military and defense applications dominate counter-drone system adoption as armed forces prioritize airspace control, threat detection, and neutralization. Detection and neutralization technologies form critical components of modern defense strategies, making military and defense the largest application segment by revenue and deployment globally.

Critical infrastructure protection is the fastest-growing application segment due to increasing drone threats targeting power plants, data centers, transport hubs, and industrial facilities. The segment is expanding as governments and private operators implement advanced counter-UAV systems to mitigate growing airborne threats to essential infrastructure.

By End-User: Defense Forces led, while Airports & Aviation Authorities is the fastest-growing segment.

Defense forces dominate the market as primary end-users of counter-drone systems, leveraging detection, tracking, and neutralization technologies to secure military bases, operational zones, and borders. Integration with existing military surveillance and command systems enhances operational readiness, reinforcing their dominant position in the counter-drone market.

Airports and aviation authorities are the fastest-growing end-user segment as drones pose increasing safety risks to air traffic. Growth is driven by regulatory mandates, rising commercial air traffic, and the need for operational continuity. The segment’s expansion reflects increasing adoption of integrated drone defense solutions to ensure safe airspace management and protect passengers, aircraft, and ground operations

Regional Insights

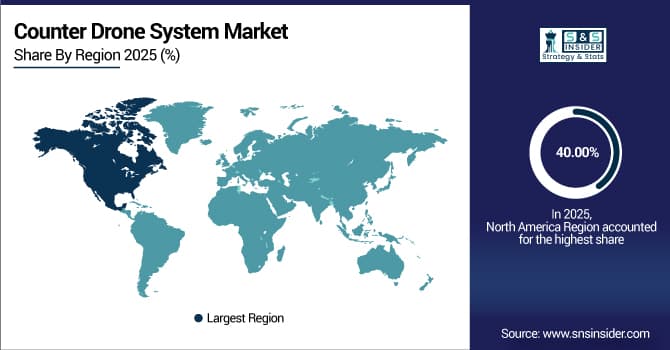

North America Counter Drone System Market Insights:

North America held 40.00% share of counter drone system in 2025 owing to high defense spending, and presence of leading drone detection and neutralization technology providers as well as high military and homeland security expenditure. Strict regulatory frameworks and growing concern over rogue drone operations kept this region as the market leader.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Asia Pacific Counter Drone System Market Insights

Asia Pacific is predicted to register the fastest CAGR of approximately 26.25% between 2026 and 2035 due to increasing defense modernization initiatives, improving border security capital expenditures, and quickly increasing adoption of counter-drone solutions. The demand for systems that can detect and neutralize drones is being driven in the region by the increase in the number of drones for commercial use, fast-developing urbanization, as well as government initiatives aimed to enhance public safety.

Europe Counter Drone System Market Insights

In 2025, a significant share of Counter Drone System Market is held by Europe due to strong defense and security infrastructure, increasing illegal ant-drone awareness due to drones, and presence of matured, technologically advanced countering drone system providers. In Europe, the growth is mainly attributed to rising investments to protect critical infrastructure coupled with strict aviation regulations, and growing adoption of combined detection & neutralization systems.

Middle East & Africa and Latin America Counter Drone System Market Insights

In 2025, steady growth in Counter Drone System Market is projected to shoot up at 6.29% interestingly in Middle East & Africa and Latin America due to growing defense spending, rising critical infrastructure, and increasing acceptance of drone surveillance and countermeasure systems. The regional growth of the defense smart munitions market was driven by growing security apprehensions in these areas, government agencies are trying to protect critical assets and city structures, and modernization of the defense industry in these regions.

Counter Drone System Market Competitive Landscape:

Lockheed Martin Corporation is a leading provider of aerospace and defense systems, and has developed integrated counter-drone capabilities to counter drones for military and security applications globally. It makes integrated systems employing radar, sensors and directed-energy technologies that find and chase down unauthorized aerial drones. The company makes critical infrastructure protection, defense bases, and urban security counter-UAS solutions focusing on reliability, innovation, and scalability. Lockheed Martin remains you unmanned aerial threat partner, with time- and mission-informed R&D capability and experience that spans globally.

-

April 2025, Lockheed Martin announced the field deployment of ATHENA DEFSYS, a 300-kW-class fiber laser integrated into the U.S. Army’s Directed Energy Maneuver-Short Range Air Defense (DE M-SHORAD) program.

Raytheon Technologies Corporation

As a major global defense and aerospace tech company, Raytheon Technologies Corporation supplies advanced counter-drone systems to meet the novel threat from unmanned aircraft. This is based on combining radar, electronic warfare and laser pinpointing to detect, track and eliminate drones within that time frame to find out what it is. Raytheon aims to protect bases, critical infrastructure, and cities. Drawing from years of defense innovation and frontline operational experience around the globe, the company is further honing the efficacy, reliability, and scalability of its counter-UAS solutions.

-

February 2025, RTX (via its Raytheon business) delivered the first Sentinel A4 C-UAS variant to the U.S. Marine Corps, featuring AI-driven micro-Doppler analysis for small drone identification.

Northrop Grumman Corporation is a global leader in aerospace and defense. The provide advanced military, government and commercial drone protection systems. It employs a smartly integrated operation of a combination of radar, sensors, and electronic warfare to detect, track, and mitigate UAS threats system and counter-UAS solutions. The company is all about putting new ideas together and checking the reliability of the systems operations. It supports defense forces and national critical infrastructure globally. Northrop Grumman's technologies enhance situational awareness, safety and mission success while designed to counter rapidly evolving drone threats.

-

June 2025, Northrop Grumman launched Falcon Shield, a modular, scalable C-UAS system designed for airports, power plants, and stadiums, combining RF detection, RF jamming, and cyber-takeover.

Counter Drone System Companies are:

-

Lockheed Martin Corporation

-

Raytheon Technologies Corporation

-

Northrop Grumman Corporation

-

Thales Group

-

BAE Systems plc

-

Israel Aerospace Industries Ltd.

-

Leonardo S.p.A.

-

Saab AB

-

Rheinmetall AG

-

Dedrone Holdings, Inc.

-

DroneShield Ltd.

-

Airbus Defence and Space

-

SRC, Inc.

-

Hensoldt AG

-

Liteye Systems, Inc.

-

Elbit Systems Ltd.

-

Blighter Surveillance Systems Ltd.

-

Aaronia AG

-

QinetiQ plc

-

Battelle Memorial Institute

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.60 Billion |

| Market Size by 2035 | USD 22.88 Billion |

| CAGR | CAGR of 24.33% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By System Type: Detection Systems, Identification & Tracking Systems, Neutralization Systems • By Technology: Radar-Based Systems, Radio Frequency (RF) Systems, Electro-Optical / Infrared (EO/IR) Systems, Laser-Based Systems, Kinetic Systems • By Deployment Mode: Fixed Systems, Mobile Systems, Man-Portable Systems • By Application: Military & Defense, Homeland Security, Critical Infrastructure Protection, Commercial Facilities, Public Event Security • By End User: Defense Forces, Government & Law Enforcement Agencies, Airports & Aviation Authorities, Energy & Utility Operators, Commercial & Private Organizations |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

Frequently Asked Questions

The Counter Drone System Market size was valued at USD 2.60 billion in 2025.

North America dominated the Counter Drone System Market in 2025

Rising threats from unauthorized and hostile drones, along with the adoption of advanced detection, tracking, and neutralization technologies, are driving market growth.

Radar-Based Systems dominated the Counter Drone System Market.

The Counter Drone System Market is expected to grow at a CAGR of 24.33% from 2026 to 2035.

Get in Touch