Mobile App Development Market Report Scope & Overview:

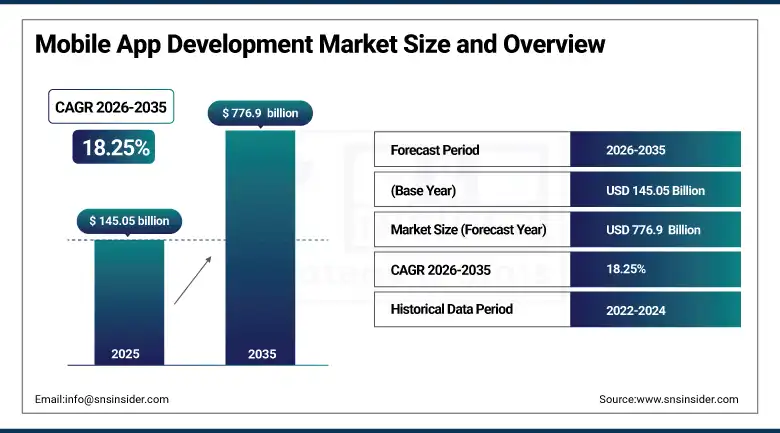

The Mobile App Development Market was valued at USD 145.05 billion in 2025 and is expected to reach USD 776.9 billion by 2035, growing at a CAGR of 18.25% from 2026–2035.

Mobile app development encompasses the full technical and creative process of designing, building, testing, deploying, and maintaining software applications that run on smartphone and tablet operating systems. Over 7 billion smartphones are in active global use as of 2025, each representing a potential distribution endpoint for mobile applications and a platform for mobile commerce, digital services, and connected experiences that mobile app developers are competing to provide across every consumer and enterprise need category. The market encompasses the commercial ecosystem of mobile app development services including custom enterprise mobile application development by professional software development firms and internal development teams, consumer app development by the independent developers and small studios, the no-code and low-code mobile app development platform market that enables non-technical users to create functional mobile applications through visual development interfaces, the mobile backend-as-a-service infrastructure that powers the server-side functionality of mobile apps, and the testing, deployment, and analytics platform ecosystem that supports mobile app quality assurance and post-launch performance optimization. The rapid advancement of AI-assisted development tools including GitHub Copilot, Anthropic Claude, and specialized mobile development AI assistants is accelerating the pace at which individual developers and small teams can create sophisticated mobile applications, simultaneously expand the developer community and compressing the time-to-market for new applications.

Statista's 2025 Global Mobile Economy Report documented that global mobile commerce revenue exceeded USD 2.2 trillion in 2024, representing over 70% of total e-commerce transactions globally, confirming that the smartphone has become the primary commercial transaction device for the majority of global consumers and establishing mobile app development investment as a commercial necessity rather than an enhancement for any business with consumer-facing digital revenue ambitions.

Market Size and Forecast

-

Market Size in 2026E: USD 171.50 Billion

-

Market Size by 2035: USD 776.9 Billion

-

CAGR (2026-2035): 18.25%

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Mobile App Development Market - Request Free Sample Report

Mobile App Development Market Trends

-

Accelerating integration of artificial intelligence and machine learning capabilities directly into mobile application features, including on-device AI models that perform image recognition, natural language processing, and personalization inference without requiring cloud round-trip latency, enabling privacy-preserving AI features that process sensitive user data locally on the device rather than transmitting it to remote servers.

-

Rapid growth of cross-platform mobile development frameworks including Flutter, React Native, and Kotlin Multiplatform that enable development teams to write application code once and deploy across both Android and iOS platforms simultaneously, reducing development cost and timeline by 30 to 50% compared with maintaining separate native codebases for each platform while achieving performance characteristics approaching native application quality.

-

Growing adoption of super-app architectures in Asian markets, where single applications serve as comprehensive digital lifestyle platforms encompassing payments, messaging, commerce, transportation, food delivery, financial services, and entertainment within a single application ecosystem that users rarely need to leave, creating platform consolidation dynamics that are being studied and progressively adopted by Western mobile platform providers.

-

Increasing enterprise investment in mobile-first internal productivity applications replacing legacy desktop software for field service, logistics management, warehouse operations, healthcare clinical documentation, and financial services advisory workflows where the smartphone's camera, location, biometrics, and offline capability provide field utility advantages that desktop applications cannot match.

-

Rising demand for augmented reality mobile application development across retail, real estate, interior design, fashion, and industrial maintenance sectors where AR overlay capability that projects digital information onto camera-captured real-world environments enables product visualization, spatial planning, and guided maintenance task execution experiences whose commercial value is demonstrably superior to conventional photograph or diagram-based equivalents.

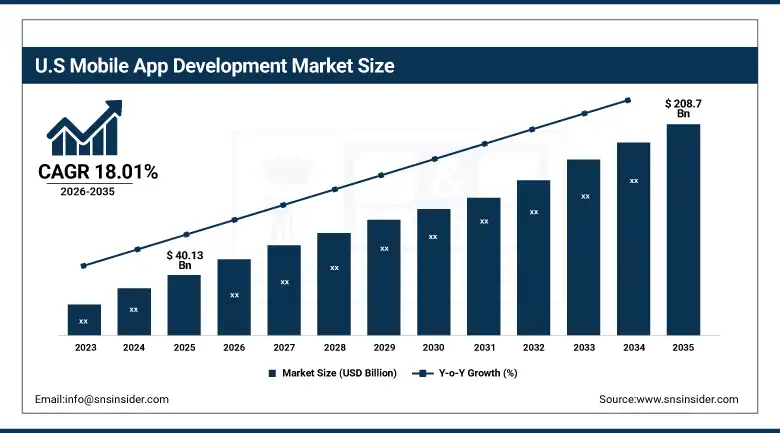

The U.S. Mobile App Development Market Outlook

The U.S. Mobile App Development Market was valued at approximately USD 40.13 billion in 2025 and is expected to reach approximately USD 208.7 billion by 2035, growing at a CAGR of 18.01%.

The United States is the world's most commercially valuable mobile app development market, where the combination of the highest mobile app consumer spending per capita globally, the headquarters concentration of the world's leading technology companies including Apple, Google, Meta, Amazon, and Microsoft whose platform and developer ecosystem investment sets global mobile development standards, and the most active enterprise mobile application investment market create a development services and platform revenue base of extraordinary commercial scale. Silicon Valley, New York, Austin, and Seattle host the world's most innovative mobile app development companies, from the independent developer studios that generate billion-dollar applications through viral consumer product innovation to the enterprise mobility solutions companies. The Apple App Store's generation of over USD 100 billion in annual developer revenue from U.S.-headquartered platform operations confirms the commercial scale of the consumer mobile application market that U.S.-based developers primarily serve.

The Federal Trade Commission's ongoing scrutiny of Apple's App Store commission structure and Google's Play Store billing practices reflects the extraordinary commercial significance of mobile app distribution platform economics, where 15 to 30% commission rates on hundreds of billions of dollars in annual in-app consumer spending represent one of the largest single taxes on digital commerce and the most commercially consequential mobile app market regulation debate of the current decade.

Mobile App Development Market Segment Analysis

-

By Type, native mobile apps dominated with approximately 52.30% in 2025; hybrid mobile apps are the fastest-growing at a CAGR of 18.20%.

-

By Platform, android led with approximately 72.40% in 2025; iOS is the fastest-growing platform at a CAGR of 15.80%.

-

By Application, e-commerce led the application segment in 2025; BFSI and healthcare are among the fastest-growing applications.

-

By End User, enterprises dominated the market; SMEs are the fastest-growing end-user category.

By Type, native Apps dominate, hybrid is expected to grow fastest

Native mobile apps retained the dominant type position with approximately 52.30% of the mobile app development market in 2025. Native iOS applications written in Swift and native Android applications written in Kotlin can access the full capability surface of their respective platforms including advanced camera processing APIs, biometric authentication frameworks, health and fitness sensor integration, real-time augmented reality rendering through ARKit and ARCore, and platform-specific accessibility and input method support, providing the comprehensive device capability access and the consistent performance characteristic that distinguish premium native mobile experiences from cross-platform alternatives. The App Store and Google Play Store quality review processes that validate native application performance before distribution also provide a competitive advantage for native applications in consumer discovery, as platform curation favors applications that demonstrate the performance and reliability characteristics that native development enables.

Hybrid mobile apps are the fastest-growing type at a CAGR of 18.20% through 2035, driven by the combination of dramatic performance improvements in cross-platform development frameworks that have narrowed the user experience gap with native applications, and the compelling economic advantages of maintaining a single codebase that delivers consistent functionality across both major mobile platforms rather than the doubled development and maintenance investment that separate native codebases require.

By Platform, android dominates, iOS is expected to grow fastest

Android retained the dominant platform position with approximately 72.40% of mobile app development market revenues in 2025. Android's open ecosystem that accommodates device manufacturers from Samsung, Xiaomi, Oppo, and Vivo through hundreds of smaller device makers serving specific national markets creates extraordinary global device diversity at price points from sub-USD-50 entry-level devices through USD 2,000 premium flagships, collectively serving the full global income spectrum in ways that enable mobile applications to reach users across developing and developed markets without the income ceiling that Apple's premium device pricing creates for iOS adoption.

iOS is the fastest-growing platform at a CAGR of 15.80% through 2035, driven by the disproportionate commercial value that iOS users represent relative to their device market share, as iPhone owners demonstrate consistently higher app download frequency, in-app purchase conversion rates, subscription renewal rates, and per-session spending than Apple's consistent hardware performance improvements, the annual iOS update adoption rate that significantly exceeds Android OS update adoption across the installed base, and the introduction of advanced developer technologies including Vision Pro spatial computing development, CoreML on-device machine learning, and ARKit augmented reality frameworks are continuously expanding the capability frontier for iOS application development.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

84.9% |

|

Europe |

United Kingdom |

23.8% |

|

Asia Pacific |

China |

41.5% |

|

Middle East & Africa |

UAE |

28.7% |

|

Latin America |

Brazil |

43.4% |

North America Mobile App Development Market Insights

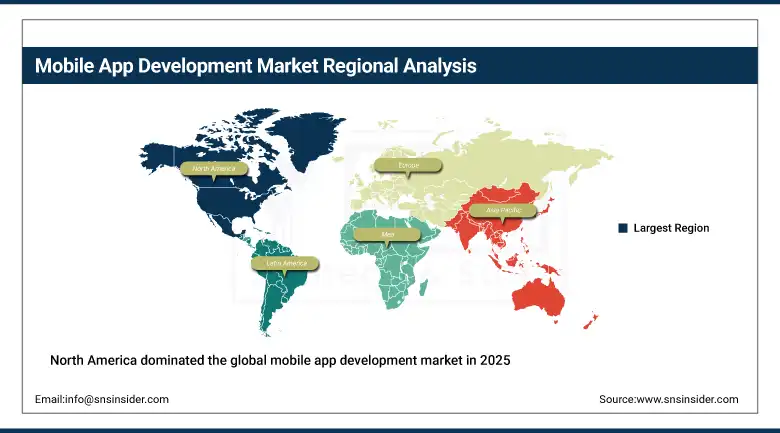

North America dominated the global mobile app development market in 2025, with the United States accounting for approximately 84.9% of North American revenues as the world's largest mobile app economy by commercial value. The region's market leadership reflects the co-location of the world's leading mobile platform providers Apple and Google whose App Store and Google Play revenue flows are concentrated in U.S.-headquartered developer operations, the highest per-capita mobile app consumer spending among major economies, and the concentration of enterprise technology investment that makes North American corporations the highest-value enterprise mobile development clients globally. The U.S. mobile gaming market's leadership position and the extraordinary revenue concentration of top-grossing U.S.-published games creates a premium commercial segment within mobile app development that sustains high-margin development investment from both independent studios and established game publishers.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Mobile App Development Market Insights

Europe is a large and technically sophisticated mobile app development market characterized by strong enterprise mobile transformation investment, a vibrant fintech mobile application sector centered in London, Amsterdam, and Berlin, and a regulatory environment under GDPR that has shaped privacy-first mobile application architecture across the region in ways that are increasingly influencing global mobile development standards as other jurisdictions adopt similar data protection frameworks. The United Kingdom accounts for approximately 23.8% of European mobile app development revenues as the region's most commercially active national market, combining the concentration of fintech mobile application development in London's financial technology ecosystem with strong enterprise mobility investment from the UK's substantial financial services, retail, and professional services corporate sectors.

Asia Pacific Mobile App Development Market Insights

Asia Pacific is the fastest-growing mobile app development market, driven by the world's largest active smartphone user population providing the addressable market scale that makes Asian mobile app development commercially attractive at local pricing levels, the extraordinary innovation of Chinese and Indian mobile app ecosystems that have pioneered super-app architectures, short video social commerce integration, and mobile payment ubiquity that are influencing global mobile application design, and the rapid growth of mobile-first digital services across healthcare, education, financial inclusion, and agriculture in markets where smartphone access preceded desktop computing penetration in the majority of the population. China accounts for approximately 41.5% of Asia Pacific revenues through the world's largest national mobile app market by usage intensity where WeChat, Alipay, TikTok, and Taobao have created the most commercially sophisticated mobile application ecosystems globally.

MEA & Latin America Mobile App Development Market Insights

The Middle East and Africa and Latin America are rapidly growing mobile app development markets where the combination of young digital-native demographics, accelerating smartphone penetration, and the leapfrogging of desktop computing toward mobile-first internet access creates large addressable markets for mobile applications across fintech, e-commerce, healthcare, and education. UAE leads MEA mobile app development revenues at approximately 28.7% of regional revenues through its high smartphone penetration, technology-forward population, and government smart services investment that has created comprehensive mobile government service platforms. Brazil leads Latin American revenues at approximately 43.4% of regional revenues as the home of Nubank, one of the world's most commercially successful fintech mobile applications, and a vibrant domestic mobile startup ecosystem serving Brazil's 180 million smartphone users.

Market Dynamics

Growth Drivers: 5G network rollout unlocking new mobile application capability categories

The primary structural growth drivers for the mobile app development market are the global rollout of 5G networks whose combination of dramatically higher data throughput, lower latency, and greater connection density is unlocking new mobile application categories including cloud gaming with console-quality graphics streamed to mobile devices, real-time augmented reality applications requiring the sustained high-bandwidth low-latency connectivity that 4G cannot reliably provide, industrial IoT management applications where mobile interfaces must process high-frequency sensor data in real time, and telemedicine platforms where high-definition video consultation quality requires reliable mobile broadband performance. The integration of AI assistance into mobile development workflows through tools including GitHub Copilot, Claude, and specialized mobile development AI assistants is simultaneously accelerating development velocity, improving code quality, and reducing the expertise barrier for mobile application creation in ways that are expanding the developer community and enabling smaller organizations to build more sophisticated mobile applications than their team size would previously have supported.

Restraints: Platform fragmentation across Android device manufacturers creating compatibility testing complexity, App Store and Google Play policy constraints limiting certain business model implementations, and mobile application security vulnerabilities creating regulatory and reputational risk

A significant restraint on the mobile app development market is the Android platform's extraordinary device fragmentation, where the combination of hundreds of device manufacturers, thousands of distinct hardware configurations, and irregular operating system update adoption across the installed base creates compatibility testing complexity that mobile development teams must address through extensive device testing programmes and defensive coding practices that add significant quality assurance cost to Android development compared with iOS's more tightly controlled hardware and software ecosystem. App Store and Google Play policy constraints limit the implementation of certain business models and functionality categories, where Apple's prohibition of third-party payment processing in iOS applications and Google's equivalent restrictions on payment system alternatives to Google Play Billing create mandatory platform commission costs that can fundamentally alter the unit economics of subscription and in-app purchase-monetized mobile applications.

Opportunities: No-code and low-code platform democratization, healthcare digital therapeutics regulatory validation, and wearable and IoT companion app development

The no-code and low-code mobile application development platform market represents the most democratizing force in mobile app development, enabling tens of millions of business users, domain experts, and entrepreneurs without traditional software engineering backgrounds to create functional mobile applications through visual development interfaces that translate user interface and business logic design intentions into deployable mobile applications without requiring code-level implementation expertise. Platforms including Bubble, Adalo, Glide, and AppSheet are enabling restaurant owners, healthcare administrators, logistics coordinators, and small business operators to build custom mobile applications tailored to their specific operational requirements at a fraction of the cost of traditional custom development, expanding the mobile application development market to customer segments that could not previously justify the investment required for professional mobile development.

Recent Developments:

-

2025: Apple introduced significant iOS 18 development framework enhancements including expanded on-device machine learning inference capability through Core ML updates, enhanced spatial computing development tools for Vision Pro, and new accessibility framework features.

-

2025: Google launched Android 15 with enhanced AI model hosting capabilities enabling on-device large language model inference at improved performance and lower battery consumption.

-

2025: Flutter 4.0 was released with significantly improved performance characteristics including compilation optimizations, expanded platform targeting beyond mobile to include mature web, desktop, and embedded Linux support.

Mobile App Development Market key players are:

-

Apple Inc.

-

Google LLC

-

Microsoft Corporation

-

IBM Corporation

-

Amazon Web Services

-

Meta Platforms Inc.

-

Infosys Limited

-

Tata Consultancy Services Ltd.

-

Wipro Limited

-

Accenture plc

-

Capgemini SE

-

HCL Technologies

-

Salesforce Inc.

-

SAP SE

-

Oracle Corporation

-

Fueled

-

Intellectsoft

-

Konstant Infosolutions

-

Savvy Apps

-

Y Media Labs

Mobile App Development Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 145.05 billion |

| Market Size by 2035 | USD 776.9 Billion |

| CAGR | CAGR of 18.25% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Native Mobile Apps, Web-based Apps, Hybrid Mobile Apps) • By Platform (Android, iOS, Others) • By Application (E-commerce, Banking Financial Services & Insurance, Healthcare, Entertainment & Media, Gaming, Education, Travel & Hospitality, Others) • By End User (Enterprises, SMEs, Individual Developers) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Apple Inc., Google LLC, Microsoft Corporation, IBM Corporation, Amazon Web Services, Meta Platforms Inc., Infosys Limited, Tata Consultancy Services Ltd., Wipro Limited, Accenture plc, Capgemini SE, HCL Technologies, Salesforce Inc., SAP SE, Oracle Corporation, Fueled, Intellectsoft, Konstant Infosolutions, Savvy Apps, Y Media Labs |

Frequently Asked Questions

North America dominated the mobile app development market in 2025.

Native Mobile Apps dominated with approximately 52.30% of revenues in 2025.

5G network rollout unlocking new mobile application capability categories combined with AI integration

The mobile app development market was valued at USD 145.05 billion in 2025.

The mobile app development market is expected to grow at a CAGR of 18.25% from 2026 to 2035.

Get in Touch