Mobile Device Management Market Report Scope & Overview:

Get more information on Mobile Device Management Market - Request Sample Report

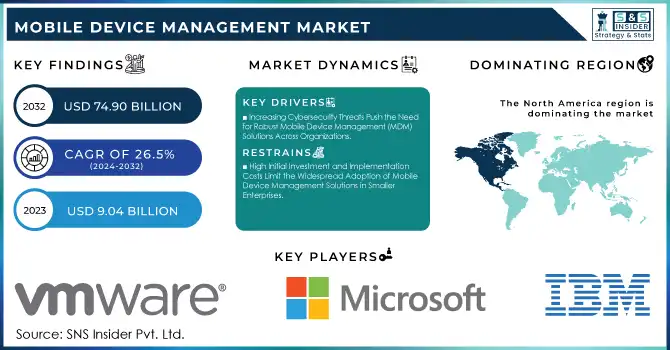

The Mobile Device Management Market Size was valued at USD 9.04 Billion in 2023 and is expected to reach USD 74.90 Billion by 2032 and grow at a CAGR of 26.5% over the forecast period 2024-2032.

The Mobile Device Management (MDM) market refers to solutions and services designed to monitor, manage, and secure mobile devices such as smartphones, tablets, and laptops in enterprise environments. MDM solutions help organizations ensure that their devices are secure, compliant with internal policies, and can be remotely managed and configured. As mobile technology evolves and is integrated into the most varied business processes, MDM solutions are necessary for enterprises in their pursuit to protect sensitive data and ensure smooth operation across a wide range of mobile platforms.

The average cost of financial loss from a data breach is approximately USD 3.86 million. This signifies the importance of Mobile Device Management (MDM) solutions for businesses to safeguard mobile devices from breaches that may have devastating financial effects. In addition, the cost of downtime in a breach is around USD 88,000 per hour, which further makes the efficiency of MDM systems inevitable to avoid any loss of time. Regulatory compliance also plays a vital role in this regard as under GDPR, businesses can face a fine of up to 4% of their annual global turnover. These statistics underscore the requirement for MDM solutions, which secure mobile devices while ensuring business continuity and reducing the associated financial risks and compliance violations.

Mobile Device Management Market Dynamics

KEY DRIVERS:

-

Increasing Cybersecurity Threats Push the Need for Robust Mobile Device Management (MDM) Solutions Across Organizations

As cyber threats increase, especially in mobile devices, organizations are put under pressure to implement comprehensive security solutions to protect sensitive data. Mobile devices are more vulnerable to cyberattacks because of their portability and frequent access to corporate networks, which make them prime targets for hackers. MDM solutions offer powerful features like remote wipe and encryption of devices and threat detection, which form the foundation of protecting data against unauthorized access, malware, and ransomware attacks.

The increasing cybersecurity risks associated with mobile device use in organizations amplify the need for robust Mobile Device Management (MDM) solutions. Research shows that 48% of companies using Bring Your Device (BYOD) policies have experienced malware through employee personal devices. However, only 40% of BYOD companies use MDM solutions, while 90% of businesses that issue devices do so. Such statistics only amplify the urgent need for MDM solutions that can help protect mobile devices and, consequently, organizations from increased cybersecurity risks.

-

Growing Adoption of BYOD and Remote Work Policies Drives the Need for Mobile Device Management Solutions in Enterprises

The adoption of BYOD policies and the rise of remote work has contributed significantly to the growth of the MDM market. With employees using personal mobile devices for work purposes, businesses face a challenge in maintaining security, managing data, and ensuring compliance across a wide range of devices. MDM solutions enable organizations to secure personal and company-issued devices alike, enforce policies, and monitor access to corporate networks and data.

Remote work and Bring Your Own Device (BYOD) policies are gaining immense popularity and are leading to huge demand for Mobile Device Management (MDM) solutions. With employees increasingly working from home or using personal devices for business, organizations find it difficult to secure and manage these devices. According to a study, 77% of remote workers experience higher productivity at home than in the traditional office setting.

RESTRAIN:

-

High Initial Investment and Implementation Costs Limit the Widespread Adoption of Mobile Device Management Solutions in Smaller Enterprises

The Mobile Device Management (MDM) market is the significant upfront investment and implementation costs associated with implementing these solutions, especially for SMEs. MDM solutions require significant capital outlays for software, infrastructure, and ongoing maintenance and may be a barrier to organizations with limited IT budgets. Besides the financial cost, the time and effort needed to integrate MDM solutions with existing IT infrastructure can be overwhelming for smaller businesses that do not have dedicated resources.

High initial investment and the running implementation costs of MDM solutions are still a big challenge for smaller enterprises. Research shows that the average cost of MDM implementation for small businesses falls between USD 10,000 and USD 50,000, which covers the cost of software, infrastructure, and support. Moreover, SMEs may incur annual maintenance costs of up to 20% of the original investment. These statistics present a challenging task for MDM adoption among small organizations with thin budgets, possibly limiting them from securing their mobile devices and data effectively.

Mobile Device Management Market Segmentation Analysis

BY ORGANISATION SIZE

In 2023, the large Enterprises segment dominated the Mobile Device Management (MDM) market, capturing 52.00% of the total market share. These organizations focus on advanced MDM solutions to secure the variety of mobile devices in their global operations. Companies like Microsoft and VMware have come out with improved MDM solutions that leverage AI and machine learning to detect threats and automate processes. Moreover, organizations are also adopting MDM solutions for BYOD policies and remote working environments. With more than 58% of companies in the U.S. adopting remote work at least part-time, large organizations have embraced advanced MDM solutions to streamline device management, improve cybersecurity, and support a hybrid workforce.

The Small and Medium Enterprises (SMEs) segment in the Mobile Device Management (MDM) market is projected to grow at the largest CAGR of 27.3% during the forecast period 2024-2032. This growth is mainly attributed to the growing need for SMEs to improve their cybersecurity, simplify operations, and adhere to industry regulations. With the savings BYOD programs offer, businesses are realizing the growing security and management issues it presents. According to research, only 40% of BYOD organizations have implemented MDM solutions, while those that issue devices to employees have a much higher rate of implementation, at 93%.

BY VERTICAL

The Healthcare sector dominates the Mobile Device Management (MDM) market, holding a significant 22 % revenue share in 2023. This is because the care of patients, communication, and efficiency in running healthcare organizations increasingly rely on mobile devices. MDM solutions are critical in the health industry for managing mobile devices for doctors, and nurses, among other staff, and patient data privacy compliance in strict regulations such as HIPAA. Healthcare providers increasingly resort to MDM in management and securing sensitive medical information to access and communicate with safe mobile devices.

The IT and Telecommunications segment is projected to experience the fastest CAGR of 29.7% during the forecasted period in the Mobile Device Management (MDM) market. This growth is primarily driven by increasing mobile device integration in telecom operations, remote management, and the need for higher security with the expansion of mobile services. Telecom companies and IT service providers are making use of MDM solutions for managing and securing mobile devices, especially in an environment where remote work and mobile communications are critical.

Mobile Device Management Market Regional Overview

In 2023, North America dominated the Mobile Device Management (MDM) market, holding a significant market share of approximately 37%. This is attributed to several factors that include the high rate of technology adoption, a high number of businesses implementing Bring Your Own Device (BYOD) policies, and an increase in mobile-first strategies across the industries. A huge population of businesses in North America already embraces mobile-first strategies and 75% of organizations leverage mobile devices in their workforce. Additionally, over 50% of North American organizations have been found to implement BYOD policies, and this is one of the reasons why MDM solutions are growing.

The Asia Pacific region is experiencing the fastest growth in the Mobile Device Management (MDM) market, with an expected CAGR of 28.12% from 2024 to 2032. This growth is mainly caused by the increasing adoption of cloud-based MDM solutions in businesses. These are cost-effective, flexible, and scalable options for businesses. China, India, and Japan are leading countries in this regard. In Singapore, 73% of firms have adopted BYOD. This will further push the adoption of mobile device management in the region. Cloud adoption is rising rapidly across Asia, with 84% of firms planning to expand their use of cloud services. This can foster the growing adoption of Mobile Device Management solutions.

Need any customization research/data on Mobile Device Management Market - Enquiry Now

Key Players in Mobile Device Management Market

Some of the major players in the Mobile Device Management Market are:

-

VMware (VMware Workspace ONE, VMware AirWatch)

-

Microsoft (Microsoft Intune, Microsoft Endpoint Manager)

-

IBM (IBM MaaS360, IBM Security Identity Governance and Intelligence)

-

Blackberry (Blackberry UEM, Blackberry Work)

-

Citrix (Citrix Endpoint Management, Citrix Workspace)

-

Google (Google Endpoint Management, Android Enterprise)

-

Cisco (Cisco Meraki Systems Manager, Cisco Umbrella)

-

Samsung (Samsung Knox Manage, Samsung Knox Platform for Enterprise)

-

Micro Focus (Micro Focus ZENworks, Micro Focus Mobile Management)

-

ZOHO (Zoho UEM, Zoho One)

-

SolarWinds (SolarWinds Mobile Device Manager, SolarWinds Remote Monitoring and Management)

-

SAP (SAP Mobile Secure, SAP Afaria)

-

Quest Software (Quest KACE Cloud Mobile Device Management, Quest KACE Systems Management)

-

Ivanti (Ivanti Neurons for MDM, Ivanti Unified Endpoint Manager)

-

Sophos (Sophos Mobile, Sophos Intercept X for Mobile)

-

SOTI (SOTI MobiControl, SOTI XSight)

-

Jamf (Jamf Pro, Jamf Now)

-

Qualys (Qualys Mobile Security Management, Qualys Cloud Platform)

-

Snow Software (Snow Device Manager, Snow License Manager)

-

Rippling (Rippling Mobile Device Management, Rippling IT Management)

RECENT TRENDS

-

In August 2024, Microsoft implemented MFA, forcing all Azure users to sign up for the added layer of security against cyber-attacks. The move was part of its bigger efforts to protect its cloud services identity and access management.

-

In February 2024, IBM and Samsung unveiled their collaboration on Zero-Touch Mobility at MWC 2024, to transform enterprise mobility. The solution integrates AI and automation to streamline device management, reduce support burdens, and improve security, thus furthering the efficiency of mobile device deployment and maintenance within enterprises.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 9.04 Billion |

| Market Size by 2031 | US$ 74.90 Billion |

| CAGR | CAGR of 26.5% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Operating System (iOS, Android, Windows, MacOS, Other Operating systems) • By Deployment Mode (On-Premises, Cloud) • By Organisation Size (Small and Medium Enterprises, Large Enterprises) • By Vertical (Banking Financial Services and Insurance, Telecom, Retail, Healthcare, Education, Transport and Logistics, Government and Public Sector, Manufacturing and Automotive, Other Verticals) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe [Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | VMware, Microsoft, Blackberry, IBM, Citrix, Google, Cisco, Samsung, Micro Focus, ZOHO and others |

| Key Drivers | • Increasing Cybersecurity Threats Push the Need for Robust Mobile Device Management (MDM) Solutions Across Organizations. • Growing Adoption of BYOD and Remote Work Policies Drives the Need for Mobile Device Management Solutions in Enterprises. |

Frequently Asked Questions

Ans: North America dominated the Mobile Device Management Market in 2023.

Ans: Large Enterprises dominated the Mobile Device Management Market.

Ans: The major growth factor of the Mobile Device Management (MDM) Market is the increasing adoption of bring-your-own-device (BYOD) policies and the growing need for securing enterprise mobile devices.

Ans: The Mobile Device Management Market size was USD 9.04 billion in 2023 and is expected to Reach USD 74.90 billion by 2032.

Ans: The Mobile Device Management Market is expected to grow at a CAGR of 26.5% during 2024-2032.

Get in Touch