Multimodal AI Market Report Scope & Overview:

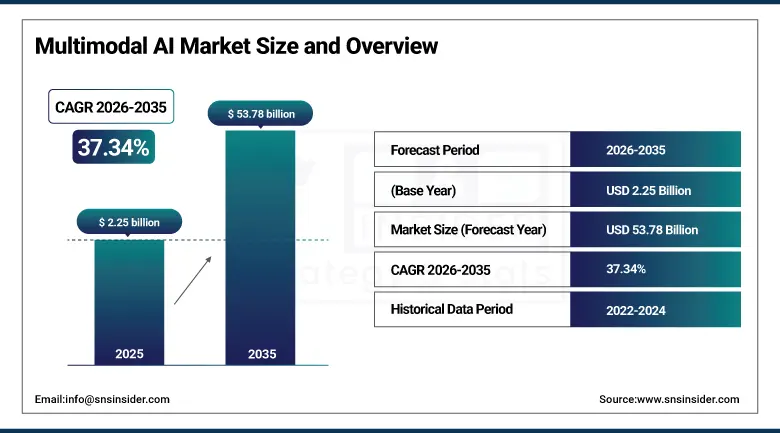

The Multimodal AI Market was valued at USD 2.25 billion in 2025 and is expected to reach USD 53.78 billion by 2035, growing at a CAGR of 37.34% from 2026-2035.

The market is witnessing swift growth, fueled by the coming together of various technology trends that are revolutionary in nature. One such factor driving the growth of the market is the increasing demand for a natural and smooth interface between human beings and machines, where businesses require the help of AI solutions that have the capability of processing input in the form of text, voice, images, and even videos in real time. In March 2025, Google has introduced AI Mode in Search driven by Gemini 2.0, giving its users the freedom to use complex multimodal inputs that include text, images, and voice all at once in a single search query. In addition, a joint venture involving OpenAI, SoftBank, and Oracle is working towards investing up to USD 500 billion in the infrastructure of AI.

According to industry data, the software segment dominated the market with approximately 68% revenue share in 2025, driven by the foundational need for model development, integration, and real-time analytics platforms — while the speech and voice data modality is projected to grow at the fastest CAGR of 40.46%, fueled by the rise of conversational AI and voice-first enterprise solutions across customer service, accessibility, and industrial control applications.

Market Size and Forecast

• Market Size in 2025: USD 2.25 Billion

• Market Size by 2035: USD 53.78 Billion

• CAGR: 37.34% from 2026 to 2035

• Base Year: 2025

• Forecast Period: 2026-2035

• Historical Data: 2022-2024

To Get more information on Multimodal AI Market - Request Free Sample Report

Multimodal AI Market Trends

-

The rapid emergence of basic multimodal models such as Google Gemini 2.0, OpenAI GPT-4o, and Anthropic Claude 3, which have the capability to analyze text, pictures, audio, and videos alongside human comprehension in the business setting.

-

The increasing integration of multimodal artificial intelligence in autonomous vehicles, which enables immediate fusion of images collected by cameras, point clouds collected by LiDARs, radar data, and verbal directions to make informed driving decisions.

-

The growing application of multimodal artificial intelligence in the medical industry, where medical images, electronic patient records, doctors' voice, and genetics information are all analyzed.

-

Rising adoption of multimodal AI in retail and e-commerce for visual search, voice shopping, automated product description generation, and personalized recommendation engines that process text queries, product images, and behavioral data.

-

Increasing adoption of multimodal AI in manufacturing to create quality control solutions that will analyze machine vision images, sensor readings, and human observations written in natural language for intelligent defect analysis and predictive maintenance.

-

Increasing application of multimodal AI-based assistants within enterprise productivity applications, where employees are able to communicate using voice, images, and text to automate multi-stage tasks on CRM, ERP, and collaboration applications.

-

Increased funding for AI-as-a-service providers, who are building multimodal models that can be accessed via cloud-based APIs, allowing SMEs to incorporate sophisticated multimodal functionality without significant infrastructure investment.

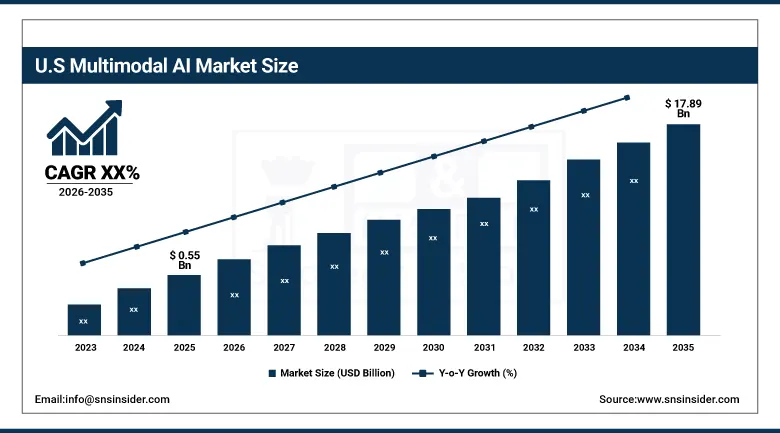

U.S. Multimodal AI Market was valued at USD 0.55 billion in 2025 and is expected to reach USD 17.89 billion by 2035, registering strong growth during the forecast period driven by healthcare, defense, and enterprise adoption.

The United States was the leader in the market due to the advanced AI research ecosystem in the country, cloud ecosystem, and because of having companies such as Google, Microsoft, OpenAI, Amazon, Meta, and NVIDIA. The United States is still experiencing fast enterprise adoption of multimodal AI for healthcare, finance, retail, autonomy, cybersecurity, and customer experience. Increased investment in infrastructure of generative AI, AI accelerators, and foundation models has helped the United States become the market leader.

As we head towards 2025, important tech vendors were seen to have intensified their efforts in developing sophisticated multimodal AI solutions that could process text, images, sound, videos, and even live conversations simultaneously. The fast deployment of AI co-pilots, conversation-based AI, intelligent search engines, and automation applications in large numbers is pushing adoption across all industries. As the focus shifts to innovations in AI, cross-modal reasoning, and investments in large AI systems, the USA continues to dominate the field of multimodal AI systems globally.

Multimodal AI Market Segment Insights

-

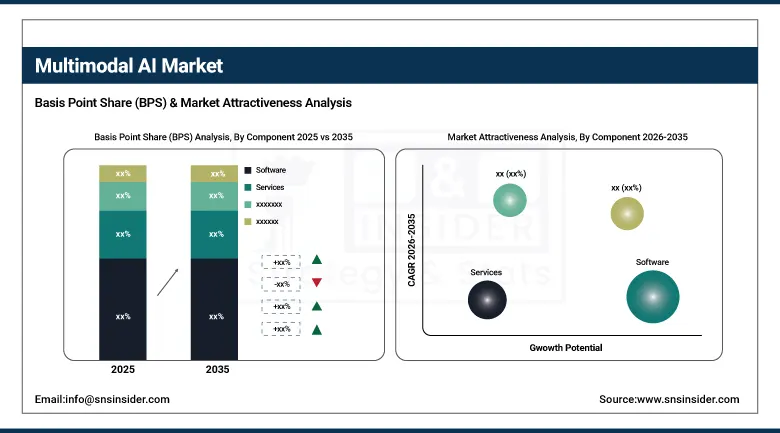

Based on Component, Software accounted for the largest market share (~68%) in 2025; Services expected to be the fastest-growing segment (CAGR of 39.19%).

-

Based on Enterprise Size, Large Enterprises accounted for the largest market share (~69%) in 2025; SMEs expected to be the fastest-growing segment (CAGR of 39.22%).

-

Based on End-Use Industry, Media & Entertainment accounted for the largest market share (~23%) in 2025; BFSI expected to be the fastest-growing segment (CAGR of 38.93%).

Multimodal AI Market Segment Analysis

By Component, Software dominates, Services expected to grow fastest

Software held a dominant position within the market with an approximate revenue share of 68% in 2025 due to the significance of model development platforms, integration middleware, and real-time analytics engines in supporting cross-modal operations on an organizational level. There was a high emphasis on software-based platforms that would help achieve the scalability of multimodal artificial intelligence capabilities through all types of data, including textual, imagery, audio, and video content.

The services segment is expected to grow at the fastest CAGR of 39.19% during 2026-2032, driven by rising demand for implementation, customization, lifecycle management, and domain-specific model training services. With organizations adopting multimodal AI technology in specialized fields such as healthcare, law, and finance, it is essential to have an advisory role, integration, and management services for safe and effective deployment.

By Enterprise Size, Large Enterprises dominate, SMEs expected to grow fastest

As far as the market share is concerned, enterprises hold an approximate market share of around 69%, thanks to the strong finances and existing IT infrastructure, and willingness to adopt new multimodal technologies. Enterprises are capable of sustaining the high amount of computation needed by these technologies in addition to the existing IT infrastructure, and can spend on sophisticated AI.

The SME segment is expected to witness the highest growth at a CAGR of 39.22% during 2026-2032, due to increased democratization by the means of AI-as-a-Service and widespread multimodal offerings in the cloud. Such platforms allow startups and smaller businesses to make use of existing multimodal models and compete effectively without requiring costly infrastructure investments.

By End-Use, Media & Entertainment leads, BFSI grows fastest

The Media & Entertainment industry led in revenues with about 23%, owing to heavy reliance on multimodal AI to provide personalized experiences, automate content production, personalize advertising, and conduct real-time content moderation. The platforms leverage multimodal AI systems to simultaneously assess text, video, and audio data for content filtering and insights into user behaviours, which is made easier in the highly data-driven, highly personal digital media landscape.

The BFSI sector will be witnessing the highest CAGR of 38.93% over 2026-2032 due to increasing requirements of AI in the BFSI sector for efficient fraud detection, intelligent customer service, and assessing risks through an integrated process involving voice and biometric analysis along with transactional patterns. Banks and financial institutes will be using multilingual and multimodal AI for providing customers with seamless customer experience through document, speech, and behavioral analytics.

Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

49% |

|

Europe |

United Kingdom |

29% |

|

Asia Pacific |

China |

43% |

|

Middle East & Africa |

UAE |

31% |

|

Latin America |

Brazil |

42% |

North America Multimodal AI Market Insights

North America dominated with approximately 47% revenue share in 2025, supported by advanced R&D ecosystems, major AI players including Google, Microsoft, Meta, Amazon, and OpenAI, and strong regulatory backing. The U.S. leads global multimodal AI adoption across healthcare diagnostics, autonomous systems, defense, and enterprise applications. Substantial private and government investment in AI infrastructure ensures continued North American leadership through the forecast period.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Multimodal AI Market Insights

The Asia Pacific region is set to have the highest CAGR growth rate of 39.11% up until 2035. This is driven by extensive digital transformation initiatives, government-driven artificial intelligence projects, and sophisticated infrastructure in countries like China, Japan, and South Korea. China is the key player in the region, having benefitted from huge government and private funding in artificial intelligence research as well as robust multimodal models by tech giants such as Baidu, Alibaba, and Tencent.

Europe Multimodal AI Market Insights

Growth in Europe will be driven by GDPR data privacy compliance, excellent automotive and healthcare industries that benefit from multimodal AI applications, and collaborations between academia and industry. The UK leads the way in the adoption of multimodal AI technology in Europe due to its adoption of the AI Opportunities Action Plan and investment in enterprise AI startups in the financial services and healthcare industries.

Middle East & Africa and Latin America Multimodal AI Market Insights

Multimodal AI adoption in emerging economies in the Middle East, Africa, and Latin America is being hastened by government-sponsored technology schemes, increased investments in financial services, health care, and telecommunication sectors in AI customer service, as well as smart city developments implementing multimodal surveillance systems.

Multimodal AI Market Growth Drivers:

Rising demand for human-like AI interaction and rapid advancement in generative AI accelerating market growth: The current market is experiencing a significant rise in 2025 owing to the increasing demand for smart systems capable of analyzing text, images, audio, video, and sensors simultaneously. The business organizations have readily adopted multimodal artificial intelligence technology with the aim of engaging customers effectively, improving processes, facilitating decision making, and creating a personalized digital experience.

The developments made in the domain of generative artificial intelligence, large language models, and cross-modal reasoning have facilitated better contextual intelligence during human-machine interactions. Moreover, the technological companies' investments in artificial intelligence infrastructure, cloud computing, and artificial intelligence as a service have helped the enterprises implement multimodal AI solutions. Furthermore, the growing need for multimodal AI applications in industries like healthcare, retail, automotive, media, education, and enterprise automation is contributing to the growth of the market.

Multimodal AI Market Restraints

High infrastructure costs, data complexity, and AI governance challenges limiting market adoption: However, the marketplace faces several difficulties when it comes to training and deploying the AI models in 2025 because of the high demands of processing capacity and infrastructure. The processing of text, images, voice, and video in one model at once is not only resource-intensive but also demands high energy usage.

In addition, concerns regarding data privacy, model transparency, bias, copyright issues, and regulatory compliance are creating governance challenges for organizations adopting multimodal AI systems. Integration complexity across multiple data sources and the lack of standardized AI frameworks also continue to slow deployment in some industries. These technical and regulatory barriers remain key factors limiting widespread commercialization and scalability of advanced multimodal AI solutions globally.

Multimodal AI Market Opportunities

Expanding enterprise AI adoption and industry-specific multimodal applications creating major growth opportunities: There are numerous chances of growth for the Multimodal AI market up to 2035 because of the rising use of AI-driven automation, intelligent analysis, and digital experience personalization within companies. Organizations across healthcare, retail, finance, automotive, manufacturing, media, and education are increasingly deploying multimodal AI solutions to improve operational efficiency, customer engagement, and real-time decision-making capabilities.

Growing demand for AI co-pilots, AI assistant, autonomy, intelligent robot, and generation of contents using AI will fuel the growth of the market further. Apart from this, advances in technology such as edge AI, AI as a service (AIaaS), and multimodal foundation models for different industries are paving the way for technological companies to explore new opportunities. Further, investment in the infrastructure of generative AI and cross-modal reasoning is expected to help innovate these technologies.

Recent Developments:

-

2026: NVIDIA expanded its multimodal AI ecosystem through the Nemotron initiative, introducing advanced multimodal models integrating vision, audio, and language capabilities for enterprise AI, robotics, and autonomous systems applications.

-

2026: Microsoft and NVIDIA strengthened their AI infrastructure collaboration to support next-generation multimodal AI workloads, integrating advanced GPUs, AI supercomputing infrastructure, and multimodal capabilities across Microsoft Copilot and Azure AI platforms.

-

2026: OpenAI accelerated development of advanced multimodal AI models focused on faster reasoning, improved image generation, low-latency interaction, and enterprise-grade cross-modal intelligence capabilities following intensified competition in the generative AI market.

Multimodal AI Market Key Players

• Google LLC

• Microsoft Corporation

• OpenAI, L.L.C.

• Meta Platforms, Inc.

• Amazon Web Services, Inc.

• NVIDIA Corporation

• IBM Corporation

• Salesforce, Inc.

• Baidu, Inc.

• Tencent Holdings Limited

• Alibaba Group

• SenseTime Group Inc.

• Huawei Technologies Co., Ltd.

• Samsung Electronics Co., Ltd.

• Tesla, Inc.

• Twelve Labs, Inc.

• Jina AI GmbH

• Uniphore Technologies Inc.

• Aimesoft Inc.

• Cohere Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.25 Billion |

| Market Size by 2035 | USD 53.78 Billion |

| CAGR | CAGR of 37.34% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Software, Services, Hardware) • By Data Modality (Text, Image, Speech & Voice, Video, Others) • By Enterprise Size (Large Enterprises, SMEs) • By End-Use Industry (Media & Entertainment, Healthcare, BFSI, Automotive, Retail, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Google LLC, Microsoft Corporation, OpenAI, L.L.C., Meta Platforms, Inc., Amazon Web Services, Inc., NVIDIA Corporation, IBM Corporation, Salesforce, Inc., Baidu, Inc., Tencent Holdings Limited, Alibaba Group, SenseTime Group Inc., Huawei Technologies Co., Ltd., Samsung Electronics Co., Ltd., Tesla, Inc., Twelve Labs, Inc., Jina AI GmbH, Uniphore Technologies Inc., Aimesoft Inc., Cohere Inc. |

An accurate research report requires proper strategy as well as implementation. There are multiple factors involved in the completion of a good and accurate research report, and selecting the best methodology to conduct the research is the toughest part. Since the research reports we provide play a crucial role in any company's decision-making process, we at SNS Insider always believe in choosing the methodology that delivers results closest to reality. This enables us to provide our clients with the best possible investment-to-output ratio.

Each report that we prepare requires approximately 300–350 business hours for production. Beginning with title selection, followed by in-depth brainstorming sessions, comprehensive research, validation, quality assurance, and final publishing, our team follows a structured process to ensure every report meets the highest standards of accuracy and reliability.

Secondary Research

Extensive secondary research is conducted to understand the market landscape and collect existing information. Multiple trusted public and commercial sources are reviewed to establish a strong research foundation before primary validation begins.

Sources typically include:

- Company annual reports and investor presentations

- Government publications and regulatory databases

- Industry associations and trade journals

- White papers and technical publications

- Company websites and press releases

- Reputable news sources and market databases

Primary Research

Primary research validates secondary findings and gathers firsthand insights from industry participants. Our analysts conduct detailed interviews with professionals across the value chain to obtain accurate market intelligence, validate assumptions, and understand current industry trends.

Interviews are conducted with:

- CEOs and Senior Executives

- Product Managers

- Sales and Marketing Professionals

- Distributors and Suppliers

- Manufacturers

- Industry Consultants

- Subject Matter Experts (SMEs)

- End Users and Customers

Market Size Estimation

The market size is estimated using multiple analytical approaches to improve accuracy:

Top-down analysis

- The analysis starts from a macro-level view, considering overall market size and industry trends.

- Large-scale data and market indicators are used to make general assumptions about the market.

- This method identifies key drivers and trends, narrowing the focus as more detailed data is explored and specific segments are examined.

- It is particularly effective for quickly evaluating market potential and regional opportunities.

Bottom-up analysis

- The process begins with gathering micro-level data, such as individual data points or small sample sets.

- This data is then aggregated and analyzed to draw broader conclusions.

- Vendor market share and contributions are assessed, providing a detailed understanding of key market players.

- This approach offers a granular view, ideal for markets with diverse segments and varied customer preferences.

Demand-side Assessment

The demand-side approach estimates market size by analyzing product consumption and purchasing patterns across various end-use industries. It focuses on understanding customer demand and market adoption.

Analyses Purchasing Behaviour of End Users

- Examines customer buying patterns, purchasing frequency, and product preferences.

- Identifies key factors influencing purchase decisions, including price, quality, and brand value.

Evaluates Demand Across Industries and Applications

- Measures product demand across different industries and application areas.

- Determines which sectors contribute the highest revenue and growth.

Estimates Consumption Volumes and Adoption Rates

- Calculates product consumption based on historical sales and usage data.

- Evaluates adoption rates of new technologies and products across industries.

Assesses Future Demand Based on Market Trends

- Forecasts future demand using economic indicators, industry developments, and statistical forecasting models.

- Considers factors such as urbanization, sustainability initiatives, and changing consumer preferences.

Supply-side Assessment

The supply-side approach estimates market size by evaluating the production capabilities and supply chain performance of manufacturers and suppliers.

Assesses Production Capacity of Manufacturers

- Evaluates manufacturing capacity, production output, and facility expansion plans.

- Identifies leading manufacturers and their production capabilities.

Evaluates Supplier Networks and Distribution Channels

- Analyses supplier relationships, distribution networks, and logistics infrastructure.

- Assesses product availability across different regions and sales channels.

Analyses Product Availability and Market Supply

- Examines inventory levels, manufacturing output, and product availability.

- Evaluates the balance between market demand and product supply.

Estimates Market Size Using Production and Shipment Data

- Calculates market size using production volumes, shipment statistics, and company revenue data.

- Validates estimates through manufacturer interviews and industry reports.

QA/QC Process

After data collection and validation, our team performs a final level of quality check and quality assurance to provide appropriate and factual data. This process includes eliminating typographical errors, removing duplicate information, validating numerical accuracy, and ensuring no important information is missing.

The QA/QC process is carried out by experienced content writers, editors, research heads, and graphics designers. Once every stage is completed successfully, the report is uploaded to our platform and made available to clients.

Report Delivery

Executive Summary

A concise overview highlighting key findings, market opportunities, competitive landscape, and future outlook to support informed decision-making.

Market Insights

Comprehensive analysis of industry dynamics, customer behaviour, technological developments, and competitive trends to identify growth opportunities.

Charts & Visualizations

Clear graphical representations of market trends, comparisons, and forecasts that simplify complex data.

Strategic Recommendations

Actionable recommendations that help organizations improve operational efficiency and strengthen their market position.

Market Forecasts

Forecasts developed using historical data, industry trends, economic indicators, and statistical models to support long-term business planning.

Frequently Asked Questions

North America dominated the Multimodal AI Market in 2025 driven by advanced R&D ecosystems and strong enterprise adoption across healthcare, defense, and technology sectors.

The Media & Entertainment segment dominated the market in 2025 with approximately 23% revenue share.

The Software segment dominated the market in 2025, accounting for approximately 68% of global revenue.

Rising demand for natural and seamless human-computer interaction combined with breakthroughs in generative AI enabling simultaneous cross-modal understanding of text, images, audio, and video.

The market was valued at USD 2.25 billion in 2025.

The market is expected to grow at a CAGR of 37.34% from 2026 to 2035.

Get in Touch