Digital Payment Infrastructure Market Report Scope & Overview:

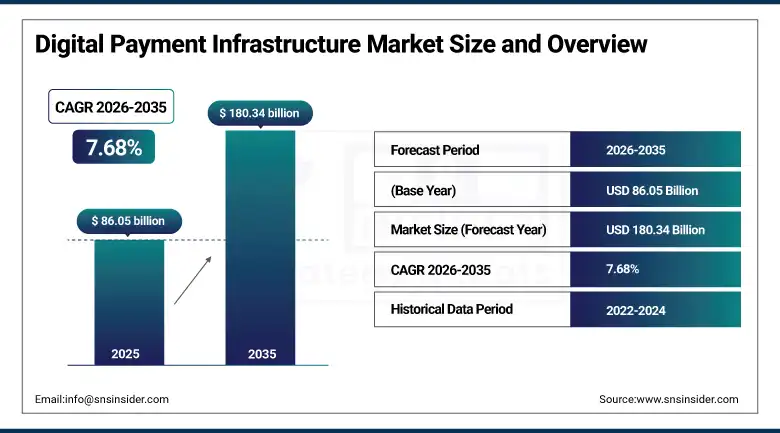

The Digital Payment Infrastructure Market was valued at USD 86.05 Billion in 2025 and is expected to reach USD 180.34 Billion by 2035, growing at a CAGR of 7.68% from 2026 to 2035.

The digital payment infrastructure refers to the complex of technological infrastructures, standards, protocols, and platforms for initiating, authenticating, routing, clearing, and settling electronic payments by payers and payees and their financial institutions. The importance of this market from a business perspective is due to the unstoppable global transition from traditional cash payment means to digital payments, accelerated after the outbreak of the COVID-19 crisis and its associated adoption of digital and contactless payment technologies among billions of users and merchants who used cash before. Open banking mandates including PSD2 in Europe, the Consumer Financial Protection Bureau's 1033 rule in the United States, and analogous requirements across Australia, Brazil, India, and the United Kingdom are compelling financial institutions to build and expose standardized API infrastructure that enables authorized third-party access to account and payment data. The U.S. Federal Reserve's FedNow service launched in 2023,

Visa launched its Visa Flexible Credential capability globally in 2025, enabling a single physical or digital card to access multiple payment funding. The product represented a significant infrastructure advancement in payment credential management that enables multi-rail payment routing from a single consumer-facing payment instrument, addressing the growing complexity of modern consumer payment portfolio management.

Market Size and Forecast

-

Market Size in 2026E: USD 92.66 Billion

-

Market Size by 2035: USD 180.34 Billion

-

CAGR: 7.68% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Digital Payment Infrastructure Market - Request Free Sample Report

Digital Payment Infrastructure Market Trends

-

Real-time payment rail adoption is accelerating globally as instant payment systems drive migration from legacy transaction infrastructure.

-

AI and machine learning integration is improving fraud detection accuracy while reducing false transaction declines significantly.

-

Open banking APIs are enabling direct account-to-account payments, increasing competition for traditional card network transaction volumes.

-

Central bank digital currency development is creating new infrastructure requirements for future digital payment settlement integration.

-

Embedded finance platforms are enabling businesses to offer payment and banking services through API-based infrastructure solutions.

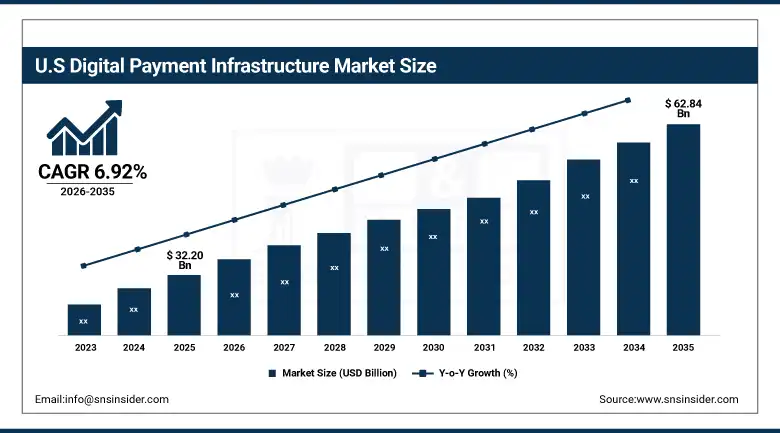

The U.S. Digital Payment Infrastructure Market Outlook

The U.S. digital payment infrastructure market was valued at approximately USD 32.20 Billion in 2025 and is expected to reach approximately USD 62.84 Billion by 2035, growing at a CAGR of approximately 6.92%.

The United States hosts the world's most commercially mature digital payment infrastructure ecosystem, anchored by the card network duopoly of Visa and Mastercard whose interchange-based business model monetizes the majority of U.S. retail payment transaction volume, the ACH network operated by The Clearing House and managed by NACHA whose debit-pull batch processing underpins payroll, bill payment, and government transfer disbursement, and the newly launched FedNow real-time gross settlement service that extends central bank instant payment access to all U.S. depository institutions. Regulatory developments including the CFPB's open banking rule implementation are creating infrastructure investment requirements across U.S. banks and credit unions whose account data API obligations will require significant technology platform upgrades. The U.S. market is also the primary commercial environment for the world's leading payment infrastructure technology companies including Fiserv, FIS, Jack Henry, and ACI Worldwide.

According to the Federal Reserve’s FedNow service, more than 1,000 American financial firms were part of the FedNow system by mid-2025, making up an adoption rate for domestic financial institutions that surpassed projections made by the Federal Reserve and indicating widespread acceptance of the instant payment system within the industry. The growth of the FedNow service provided same-day payment options and directly challenged The Clearing House’s RTP system.

Digital Payment Infrastructure Market Segment Analysis

-

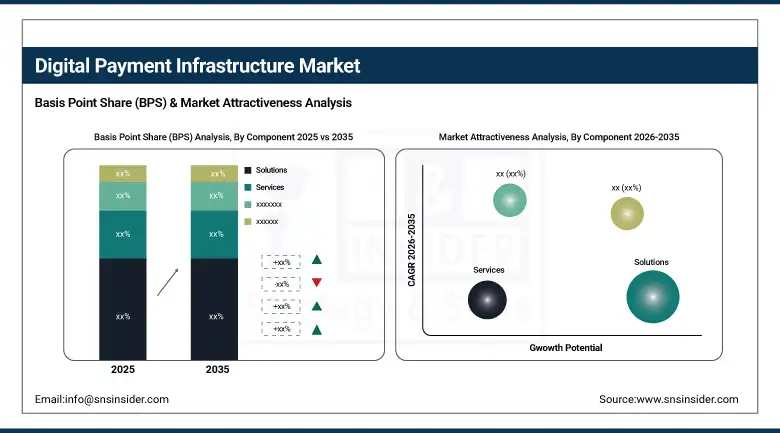

By Component, the solutions segment dominated the market with 67.82% share in 2025, while the services segment is the fastest growing component during 2026 to 2035.

-

By Payment Method, the credit & debit cards segment dominated the market with 42.84% share in 2025, while the digital wallets segment is the fastest growing payment method during 2026 to 2035.

-

By Mode of Payment, the point-of-sale segment dominated the market with 53.00% share in 2025, while online and remote payments are the fastest growing mode during 2026 to 2035.

-

By Deployment Mode, the cloud-based segment dominated the market with 58.47% share in 2025, while the on-premise segment retains regulatory-driven adoption in high-compliance environments.

-

By Industry Vertical, the BFSI segment dominated the market with 34.82% share in 2025, while the retail & e-commerce segment is the fastest growing vertical during 2026 to 2035.

By Component, solutions dominate, services grow fastest

Solutions generated 67.82% of digital payment infrastructure market revenue in 2025, encompassing the authorization and switching platforms, fraud management systems, payment gateway technology, tokenization engines, clearing and settlement systems, and regulatory compliance monitoring platforms that constitute the core functional layer of digital payment infrastructure whose technical architecture determines the speed, security, and scalability of every payment transaction processed through it. The solutions category's commercial dominance reflects the high software license and transaction fee revenue generated by payment processing platform vendors whose per-transaction and per-account billing models create recurring revenue that scales directly with payment volume growth.

Services are growing fastest as payment infrastructure modernisation programmes at financial institutions, the migration from legacy mainframe-based core banking to cloud-native architectures, and the implementation of open banking API platforms each require substantial professional services investment in system integration, testing, regulatory compliance documentation, and change management.

By Industry Vertical, BFSI dominates, retail & e-commerce grows fastest

BFSI generated 34.82% of digital payment infrastructure market revenue in 2025, reflecting financial institutions' role as both the primary operators of payment infrastructure and the heaviest investors in its modernisation. Banks, credit unions, payment processors, and fintech companies collectively account for the overwhelming majority of payment infrastructure capital expenditure as they simultaneously upgrade legacy systems, build open banking API platforms, integrate real-time payment connectivity, and invest in AI-powered fraud management capabilities.

Retail and e-commerce is growing fastest as the continued global expansion of online commerce, the proliferation of social commerce payment integration within Instagram, TikTok, and WeChat, and the growing adoption of embedded one-click payment experiences within retail mobile applications collectively drive payment infrastructure investment across the merchants, payment facilitators, independent software vendors, and platform technology companies that serve the online retail ecosystem whose transaction volume and payment complexity is growing simultaneously.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

84.73% |

|

Europe |

United Kingdom |

32.84% |

|

Asia Pacific |

China |

38.47% |

|

Middle East & Africa |

UAE |

24.73% |

|

Latin America |

Brazil |

43.84% |

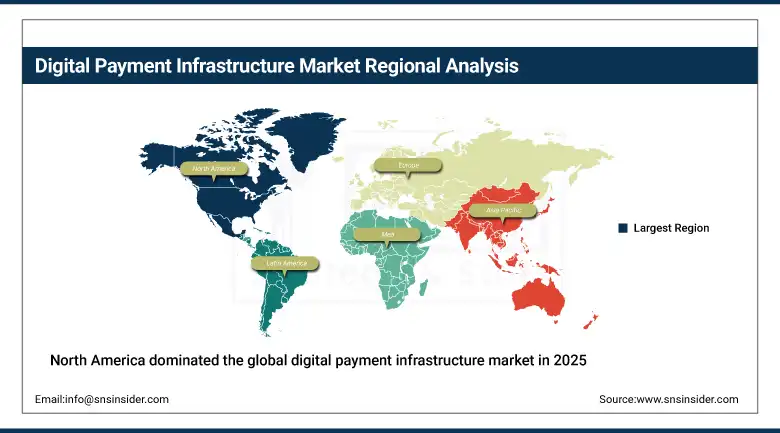

North America Digital Payment Infrastructure Market Insights

North America dominated the global digital payment infrastructure market in 2025, holding approximately 36.00% of global revenues. The United States accounts for approximately 84.73% of regional revenue through the commercial scale of its card network operations, the revenue generated by major payment processors and banking technology vendors, and the compliance-driven infrastructure investment of U.S. financial institutions responding to open banking, real-time payment, and fraud management regulatory expectations. Canada contributes supplementary demand through Interac's domestic real-time payment infrastructure and the growing adoption of digital wallet and contactless payment among Canadian consumers whose mobile payment penetration rates are comparable to U.S. averages.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Digital Payment Infrastructure Market Insights

Europe held approximately 24.84% of global Digital Payment Infrastructure revenues in 2025. The EU's PSD2 open banking directive, PSD3 proposal advancing the regulatory framework further, and the European Payments Initiative's push to build a pan-European instant payment network independent of U.S. card network rails collectively create a regulatory-driven infrastructure investment cycle of significant commercial scale. The United Kingdom accounts for approximately 32.84% of European revenues through its Faster Payments System, the New Payments Architecture modernisation programme, and its post-Brexit open banking regulatory leadership whose implementation has stimulated substantial third-party payment provider ecosystem investment and consumer adoption of account-to-account payment alternatives.

Asia Pacific Digital Payment Infrastructure Market Insights

Asia Pacific is the fastest-growing regional digital payment infrastructure market, projected to expand at a CAGR of approximately 18.00% through 2035, driven by the extraordinary scale of digital payment adoption in China and India, the rapid deployment of QR code and mobile wallet payment infrastructure across Southeast Asia, and government-mandated payment system modernisation programmes across the region's developing economies. China accounts for approximately 38.47% of Asia Pacific revenues through the infrastructure investments of Alipay's Ant Group and WeChat Pay's Tencent Financial Technology whose combined payment infrastructure serves over one billion active users. India's UPI has become one of the world's most impressive payment infrastructure success stories, processing 15 billion monthly transactions by late 2025 at zero merchant discount rate, demonstrating the extraordinary transaction scale achievable through government-supported open payment rails.

MEA & Latin America Digital Payment Infrastructure Market Insights

Middle East and Latin America are high-growth digital payment infrastructure markets where financial inclusion mandates, expanding smartphone penetration, and deliberate government payment system modernisation investments are driving rapid adoption of digital payment rails across populations with historically low banking penetration. Brazil's PIX instant payment system, launched in November 2020, had accumulated over 150 million registered keys by 2025 and demonstrated that central bank-operated zero-fee instant rails can achieve transformative payment system penetration within years rather than decades. The UAE leads MEA revenues at approximately 24.73% of the regional total through its advanced financial services infrastructure, high consumer digital payment adoption rates, and the regulatory innovation of DIFC and ADGM financial frameworks that attract global payment technology companies.

Market Dynamics

Growth Drivers: Real-time payment rail adoption and open banking regulatory mandates are creating sustained infrastructure investment cycles across global financial systems.

The commercial momentum of digital payment infrastructure investment is powered by two simultaneously operating forces. Regulatory mandates including open banking requirements, real-time payment system participation obligations, and fraud liability frameworks create non-discretionary capital investment requirements for financial institutions whose non-compliance carries regulatory sanction rather than merely competitive disadvantage. Simultaneously, commercial competitive pressure from fintech challengers, card network scheme competition, and the consumer experience expectations established by leading digital payment applications create investment urgency beyond regulatory minimum compliance. Together these forces generate a payment infrastructure investment cycle that is simultaneously compliance-driven and market-driven, making it more commercially durable than either force alone would sustain.

Restraints: Cybersecurity risk and the complexity of legacy payment system modernisation constrain the pace of digital payment infrastructure transformation.

Global financial services cybersecurity incidents involving payment infrastructure have increased substantially over the past five years, with sophisticated attack campaigns targeting authorization systems, card data environments, and real-time payment rails whose speed and irreversibility make fraud recovery more difficult than in slower legacy systems. The technical and regulatory complexity of migrating payment infrastructure from legacy mainframe-based systems to cloud-native architectures while maintaining the 99.999% availability standards that payment regulators require creates implementation risk that causes financial institutions to extend modernisation timelines beyond initial programme plans. These extended timelines increase total programme cost and delay the commercial benefit realization that justifies the initial investment case.

Opportunities: Central bank digital currency infrastructure development and embedded finance platform expansion represent transformative payment infrastructure growth.

Central bank digital currency programmes in China, the European Union, the United Kingdom, India, and approximately 130 other countries at various stages of exploration and pilot represent a potential architectural transformation of settlement infrastructure whose implementation would require substantial new technical investment in CBDC wallet management, privacy-preserving transaction processing, and CBDC-to-commercial-bank-money conversion systems. The embedded finance opportunity encompasses the growing commercial market for banking-as-a-service infrastructure that enables non-financial businesses to offer payment acceptance, account management, and lending services through their own digital product interfaces, creating a new category of payment infrastructure customer whose investment in BaaS platform connectivity generates incremental payment infrastructure revenue.

Recent Developments:

-

2025: Visa launched its Flexible Credential capability globally, enabling a single card to access multiple payment funding sources including debit, credit, buy now pay later, and cryptocurrency balances with source selection based on merchant category or consumer preference rules, advancing multi-rail payment routing from a single consumer payment credential.

-

2025: The Federal Reserve's FedNow Service surpassed 1,000 participating U.S. financial institutions less than two years after launch, establishing real-time gross settlement capabilities across the majority of the U.S. deposit account base and progressively displacing ACH same-day payment for time-sensitive disbursement use cases.

-

2024: Mastercard expanded its Multi-Rail network capabilities, enabling financial institutions and fintech companies to route payments across real-time, debit, credit, and ACH rails through a single API integration that abstracts the complexity of individual payment system participation and optimizes rail selection based on transaction type, value, and speed requirements.

Digital Payment Infrastructure Market key players are:

-

Visa Inc.

-

Mastercard Inc.

-

PayPal Holdings Inc.

-

Fiserv Inc.

-

FIS (Fidelity National Information Services)

-

Stripe Inc.

-

Adyen NV

-

Jack Henry & Associates Inc.

-

ACI Worldwide Inc.

-

Global Payments Inc.

-

Worldpay

-

SWIFT (Society for Worldwide Interbank Financial Telecommunication)

-

The Clearing House Payments Company LLC

-

Temenos AG

-

Finastra Ltd.

-

Nuvei Corporation

-

Paysign Inc.

-

Ant Group Co. Ltd. (Alipay)

-

Tencent Financial Technology (WeChat Pay)

-

PhonePe Pvt. Ltd.

Digital Payment Infrastructure Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 86.05 Billion |

| Market Size by 2035 | USD 180.34 Billion |

| CAGR | CAGR of 7.68% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Solutions, Services) • By Payment Method (Mobile Payments, Credit & Debit Cards, Net Banking, Digital Wallets, Buy Now Pay Later, Others) • By Mode of Payment (Point of Sale, Online/Remote Payments) • By Deployment Mode (Cloud-Based, On-Premise) • By Industry Vertical (BFSI, Retail & E-Commerce, Healthcare, IT & Telecommunications, Government, Travel & Hospitality, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Visa Inc., Mastercard Inc., PayPal Holdings Inc., Fiserv Inc., FIS (Fidelity National Information Services), Stripe Inc., Adyen NV, Jack Henry & Associates Inc., ACI Worldwide Inc., Global Payments Inc., Worldpay, SWIFT (Society for Worldwide Interbank Financial Telecommunication), The Clearing House Payments Company LLC, Temenos AG, Finastra Ltd., Nuvei Corporation, Paysign Inc., Ant Group Co. Ltd. (Alipay), Tencent Financial Technology (WeChat Pay), PhonePe Pvt. Ltd. |

Frequently Asked Questions

North America dominated the Digital Payment Infrastructure Market in 2025, holding approximately 36.00% of global revenues.

The credit & debit cards segment dominated the market with 42.84% share in 2025.

The primary growth factors are the global deployment of real-time payment rails creating new infrastructure investment requirements and open banking regulatory mandates compelling financial institution API platform development.

The digital payment infrastructure market was valued at USD 86.05 Billion in 2025.

The digital payment infrastructure market is expected to grow at a CAGR of 7.68% from 2026 to 2035.

Get in Touch