Multiprotocol Storage Market Report Scope & Overview:

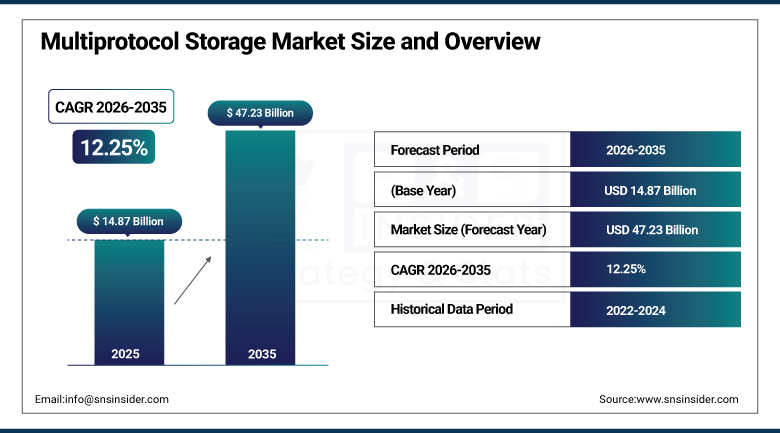

The Multiprotocol Storage Market was valued at USD 14.87 Billion in 2025 and is expected to reach USD 47.23 Billion by 2035, growing at a CAGR of 12.25% from 2026 to 2035.

The Multiprotocol Storage Market is witnessing significant growth owing to the increasing demand for flexible, scalable, and interoperable storage solutions that can effectively support various types of data and protocols. The rise in the amount of data from cloud computing, artificial intelligence, Internet of Things, and big data analytics, with 2.5 quintillion bytes of data generated every day and 90% of the total data in the world being produced in just the past two years, according to the Telecommunications Industry Association, has led companies to opt for multiprotocol storage solutions in order to ensure better performance and interoperability. In light of increasing adoption of hybrid clouds among companies, efficient management and transfer of data have truly become essential, and multiprotocol storage systems allow easy access to the data irrespective of the protocol used.

In 2025, IBM enhanced its multiprotocol storage portfolio with improved AI-driven data management and hybrid-cloud optimization features, aimed at supporting complex enterprise workloads that increasingly span on-premises, private cloud, and public cloud environments simultaneously.

Market Size and Forecast

-

Market Size in 2026E: USD 16.69 Billion

-

Market Size by 2035: USD 47.23 Billion

-

CAGR: 12.25% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Multiprotocol Storage Market - Request Free Sample Report

Multiprotocol Storage Market Trends

-

Accelerating adoption of hybrid cloud environments is propelling market expansion globally, as organizations need to manage data efficiently across mixed infrastructure.

-

Technological advancements in storage virtualization, AI-driven optimization, and NVMe integration are reshaping the multiprotocol storage market landscape.

-

Growing convergence of compute and storage capability is enabling reduced latency and real-time data processing closer to the source for AI and analytics workloads.

-

Enterprises with heterogeneous IT environments are increasingly prioritizing unified storage platforms that reduce complexity and administrative overhead.

-

Rising integration with AI, IoT, and big data applications continues expanding the practical use cases multiprotocol storage systems are asked to support.

U.S. Multiprotocol Storage Market Outlook

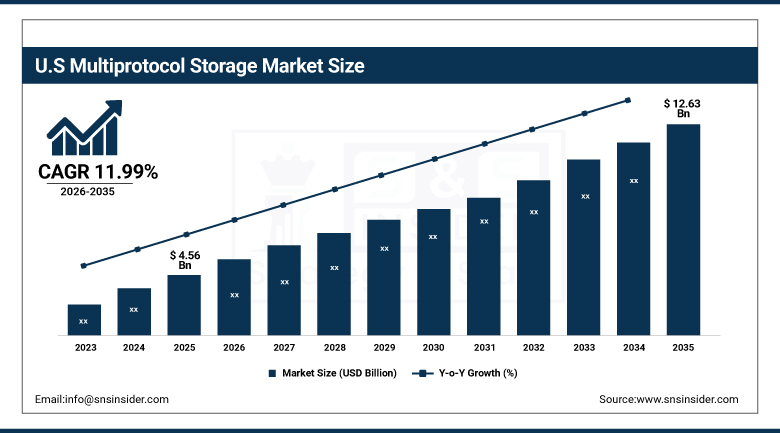

The U.S. Multiprotocol Storage Market was valued at approximately USD 4.56 Billion in 2026 and is expected to reach approximately USD 12.63 Billion by 2035, growing at a CAGR of approximately 11.99%.

Growing enterprise data, the use of hybrid cloud solutions, the need for scalable and high-performance storage, and integration with AI, IoT, and big data applications to guarantee effective, safe, and adaptable data management are the main factors propelling expansion of the U.S. multiprotocol storage market. U.S. enterprises invest heavily in digital modernization, AI workloads, and multi-cloud strategies, driving sustained demand across virtually every major industry. Regulatory compliance needs, strong cybersecurity focus, and rapid expansion of AI-enabled storage infrastructure further reinforce the country's leadership in the North American multiprotocol storage landscape.

In 2025, Cisco introduced strengthened interoperability offerings for hybrid and multi-cloud storage environments, enhancing performance and simplifying storage-network operations for U.S. enterprises managing increasingly complex, multi-vendor infrastructure.

Multiprotocol Storage Market Segment Analysis

-

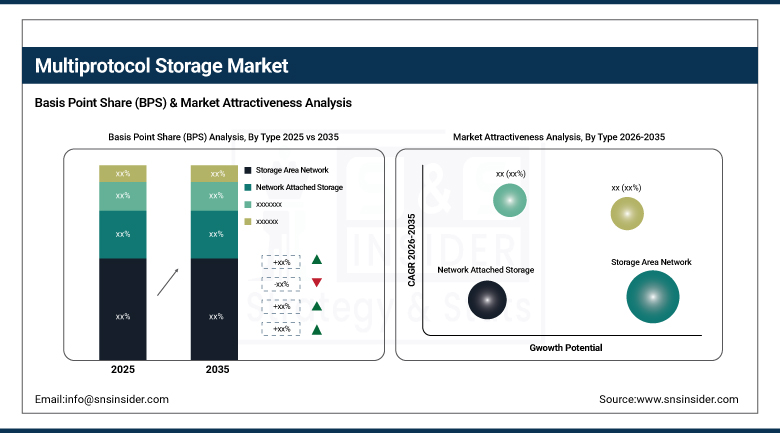

By Type, Storage Area Network segment dominated the Multiprotocol Storage Market in 2025 with 41% share; Network Attached Storage segment is the fastest-growing segment.

-

By Deployment, Hybrid Cloud segment dominated the market in 2025 with 46% share; Public Cloud segment is the fastest-growing segment.

-

By Enterprise Size, Large Enterprises segment dominated the market in 2025 with 68% share; Small and Medium Enterprises segment is the fastest-growing segment.

-

By Application, BFSI segment dominated the market in 2025 with 24% share; Healthcare segment is the fastest-growing segment.

By Type, Storage Area Network (SAN) Dominates the Multiprotocol Storage Market While Network Attached Storage (NAS) Registers the Fastest Growth

The Storage Area Network (SAN) segment dominated the Multiprotocol Storage Market in 2025 with a 41% share due to its high-performance storage solutions, reduced latency, and capability to deliver mission-critical enterprise workloads. Larger enterprises use SAN technologies for data management, virtualization, database processing, and large transactions. The growing requirement for advanced storage infrastructure, high availability of data, and performance of the enterprise has increased the usage of SAN solutions.

The Network Attached Storage (NAS) segment is the fastest-growing because companies require storage solutions which will be cost-effective and scalable and at the same time easy to access. The technology enables centralized file sharing and easy collaboration of the company's employees. The growth in data creation, adoption of remote working, edge storage requirements, and flexibility of storage environment have contributed to the adoption of NAS solutions.

By Deployment, Hybrid Cloud Dominates the Multiprotocol Storage Market While Public Cloud Emerges as the Fastest-Growing Deployment Model

The Hybrid Cloud segment dominated the Multiprotocol Storage Market in 2025 with a 46% share owing to its ability to offer companies a combination of both the scalability and flexibility of public clouds as well as the private infrastructure management. More and more companies opt for hybrid storage architecture in order to achieve better cost savings, increased security of their data and efficient management of their workloads.

The Public Cloud segment is the fastest-growing due to high demand for flexible and scalable storage infrastructure. Companies start transferring their workloads to the cloud platforms in order to minimize capital expenses, ensure better accessibility and support their digital transformation efforts. Increased adoption of cloud-native workloads and artificial intelligence services is driving the demand for public cloud multiprotocol storage solutions.

By Enterprise Size, Large Enterprises Dominate the Multiprotocol Storage Market While SMEs Witness the Fastest Growth

The Large Enterprises segment dominated the Multiprotocol Storage Market in 2025 with a 68% share because of their huge data needs, complex information technology environment, and greater spending on storage infrastructure. Large companies need multiprotocol storage technology in order to facilitate enterprise-level applications, analytics, virtualization, and cyber security initiatives. The increase in the size of data and the need for robust storage architecture has promoted its adoption by large companies.

The Small and Medium Enterprises segment is the fastest-growing due to availability of low-cost storage solutions as well as cloud computing services which have made advanced data management technologies more affordable. SMEs are embracing multiprotocol storage technology in order to boost collaboration, increase efficiency, and transform their processes digitally without any major investment in infrastructure.

By Application, BFSI Dominates the Multiprotocol Storage Market While Healthcare Experiences the Fastest Growth

The BFSI segment dominated the Multiprotocol Storage Market in 2025 with a 24% share owing to the heavy dependence of the BFSI industry on secure, high-performance, and reliable data storage systems. The BFSI sector produces massive amounts of transactional data which needs to be stored through advanced data storage systems for analytics purposes, compliance, risk management, and delivery of quality customer services. The BFSI segment has been seeing increasing demands for multiprotocol storage solutions because of digital banking and need for secured data storage solutions.

The Healthcare segment is the fastest-growing as healthcare companies produce a lot of medical imagery, electronic medical records, and research data. The multiprotocol storage helps to provide the data access securely, collaborate effectively, and manage healthcare information systems in a scalable manner. Increasing popularity of digital healthcare platforms, artificial intelligence diagnostics, telemedicine, and medical imaging technology pushes the growth of the healthcare segment.

Regional Insights

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

71.60% |

|

Europe |

Germany |

24.50% |

|

Asia Pacific |

China |

31.05% |

|

Middle East & Africa |

UAE |

26.65% |

|

Latin America |

Brazil |

35.80% |

North America Multiprotocol Storage Market Insights

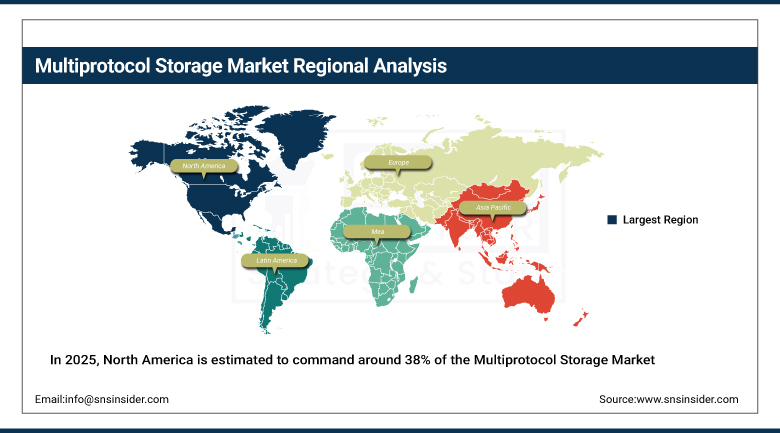

In 2025, North America is estimated to command around 38% of the Multiprotocol Storage Market, driven by its advanced cloud ecosystem, dense concentration of hyperscale data centers, and strong enterprise demand for scalable, secure, and interoperable storage solutions. That combination of infrastructure density and enterprise sophistication has kept North America the market's clear regional leader.

The United States accounts for roughly 71.60% of regional revenue, anchored by heavy enterprise investment in digital modernization, AI workloads, and multi-cloud strategies. Canada adds further regional demand through its own growing enterprise cloud adoption, and that combined regional strength should keep North America the largest addressable market for multiprotocol storage vendors through the forecast period.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Multiprotocol Storage Market Insights

Europe holds a meaningful share of the global multiprotocol storage market, driven by the region's focus on data protection and compliance with stringent regulations such as GDPR. The presence of established industries, including finance, healthcare, and manufacturing, further drives demand for advanced, compliant storage solutions across the region's major economies.

Germany leads regional demand at roughly 24.50% of European revenue, supported by its substantial industrial and financial services base. The UK and France contribute substantial additional demand, and the region's continued emphasis on innovation and digital transformation should keep regional demand for multiprotocol storage climbing steadily through the forecast period.

Asia Pacific Multiprotocol Storage Market Insights

Asia Pacific is projected to grow at an estimated CAGR of approximately 11.1%, driven by rapid digital transformation, massive cloud adoption, and accelerated data-center expansion across emerging and developed economies. Growing investments in AI, 5G, IoT, and enterprise modernization significantly raise the need for flexible, scalable multiprotocol storage, making Asia Pacific the highest-growth region tracked in this report.

China leads the region, accounting for roughly 31.05% of regional revenue, supported by large-scale cloud infrastructure development, strong government digitalization initiatives, and rapid enterprise adoption of AI and big data analytics. Japan and South Korea contribute meaningful additional demand, and that broadening base of regional data-center investment is what's keeping Asia Pacific's growth outlook well ahead of every other region tracked in this report.

MEA & Latin America Multiprotocol Storage Market Insights

The Middle East & Africa and Latin America are both showing steady growth in multiprotocol storage adoption, driven by expanding data-center investment, growing enterprise cloud adoption, and rising government focus on digital infrastructure modernization across both regions. As these markets continue building out modern IT infrastructure, multiprotocol storage is proving an efficient way to support increasingly heterogeneous enterprise data environments.

The UAE leads Middle East & Africa demand at roughly 26.65% of regional revenue, supported by the country's substantial data-center investment and its broader push toward advanced digital infrastructure. Saudi Arabia and South Africa contribute further regional demand through their own technology modernization programs. In Latin America, Brazil accounts for approximately 35.80% of regional revenue, with growing enterprise data-center investment continuing to anchor regional demand for multiprotocol storage.

Growth Drivers: Accelerating hybrid cloud adoption and exploding data volumes

The increasing adoption of hybrid cloud environments is facilitating growth of the market worldwide owing to the fact that it has now become imperative to handle and transfer the data effectively within the different environments. The multiprotocol storage systems have offered access to data irrespective of the protocol used by offering seamless integration of on-premise and cloud based infrastructures, which has been the main factor behind consistent rise in the demand for these systems within organizations of all sizes and industries.

The increase in the volume of data from cloud computing, artificial intelligence, IoT and big data analysis has acted as another driver supporting the aforementioned driver as an estimated 2.5 quintillion bytes of data gets generated every day and 90 percent of the world's data has been produced only in the last two years as per industry reports.

Restraints: Implementation complexity and integration costs

Implementation of multiprotocol storage infrastructure that is capable of handling multiple protocols and workloads calls for complex integration and design capabilities, and such considerations are one of the reasons for slow adoption of this type of infrastructure, especially for companies that lack internal knowledge of storage technology. Transition to multiprotocol storage infrastructure from traditional storage infrastructure with a single protocol is not an easy task for most businesses.

Cost factors play an additional role in slowing down the implementation of multiprotocol storage infrastructure, especially for companies that have limited IT budgets compared to big companies. The above factors contribute to the reason why implementation of multiprotocol storage is fast for larger companies and relatively slow for smaller ones.

Opportunities: AI-Integrated storage architecture and computed storage expansion

Increasing convergence between compute and storage capabilities is a true opportunity for vendors capable of providing an architecture that cuts down on latency and supports real-time processing nearer to the data source. Given that AI, analytics, and IoT workloads require both high speed and compute capacity at once, vendors who provide efficient computed storage solutions are poised to claim a considerable share of this fast-growing segment.

Growing adoption by SMEs presents another major opportunity for vendors because the increasing adoption of digital transformation and cloud apps makes it easier for companies to obtain sophisticated multiprotocol storage solutions. With SMEs increasingly seeing the value of adopting storage solutions, vendors are poised to gain a considerable market share from the segment traditionally overlooked by others.

Recent Developments

-

2025: IBM enhanced its multiprotocol storage portfolio with improved AI-driven data management and hybrid-cloud optimization features to support complex enterprise workloads.

-

2025: Cisco introduced strengthened interoperability offerings for hybrid and multi-cloud storage environments, enhancing performance and simplifying storage-network operations.

Multiprotocol Storage Market Key Players

-

IBM Corporation

-

NetApp

-

NTT Communications Corporation

-

Dell EMC (Dell)

-

Avere

-

Hewlett-Packard (HP)

-

Zadara Storage

-

EMC Corporation

-

Huawei Technologies

-

Pure Storage

-

Fujitsu Limited

-

Western Digital Corporation

-

Oracle Corporation

-

Infinidat

-

Quantum Corporation

-

DataDirect Networks (DDN)

-

Nutanix

-

Tintri

Multiprotocol Storage Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 14.87 Billion |

| Market Size by 2035 | USD 47.23 Billion |

| CAGR | CAGR of 12.25% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Network Attached Storage, Storage Area Network, Computed Storage) • By Deployment (Public Cloud, Hybrid Cloud, Private Cloud) • By Enterprise Size (Small and Medium Enterprises, Large Enterprises) • By Application (BFSI, Healthcare, Logistics, Retail & E-Commerce, Media & Entertainment, Manufacturing, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | IBM Corporation, Cisco Systems, NetApp, NTT Communications Corporation, Dell EMC (Dell), Avere, Hewlett-Packard (HP), Zadara Storage, EMC Corporation, Huawei Technologies, Hitachi Vantara, Pure Storage, Fujitsu Limited, Western Digital Corporation, Oracle Corporation, Infinidat, Quantum Corporation, DataDirect Networks (DDN), Nutanix, Tintri |

Frequently Asked Questions

The Multiprotocol Storage Market is expected to grow at a CAGR of 12.25% from 2026 to 2035.

The Multiprotocol Storage Market was valued at USD 14.87 Billion in 2025.

The major growth factor is rising need for flexible, scalable, and interoperable storage solutions driven by exploding data volumes from cloud computing, AI, IoT, and big data analytics.

The Network Attached Storage segment dominated the Multiprotocol Storage Market by type in 2025.

North America dominated the Multiprotocol Storage Market in 2025 with an estimated 38% share of total global market revenue.

Get in Touch