Home Insurance Market Report Scope & Overview:

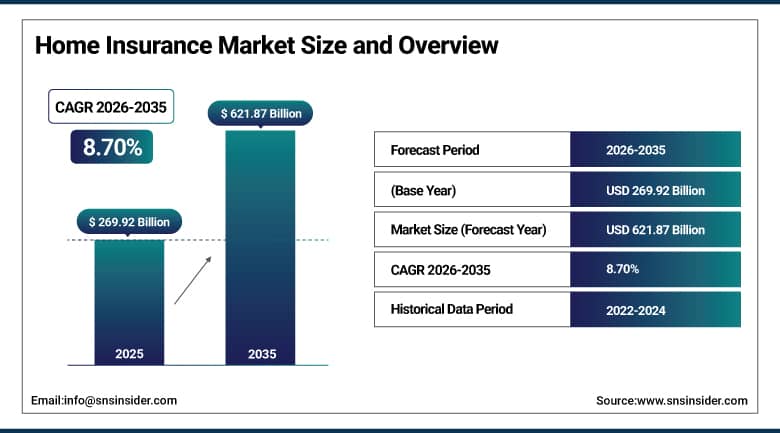

The Home Insurance Market was valued at USD 269.92 Billion in 2025 and is expected to reach USD 621.87 Billion by 2035, growing at a CAGR of 8.70% from 2026 to 2035.

The Home Insurance Market is growing steadily owing to an increase in property value, greater awareness regarding financial protection from any damages caused due to natural calamities, theft, and fires, and urbanization. Rising demand is driven by stringent mortgage regulations, which usually require insurance cover, and increased concerns about climate uncertainties that need complete insurance cover. Furthermore, technological developments within the insurance sector, such as insurtech and other digital platforms for insurance distribution, are making customers more accessible and engaged, driving the adoption process.

According to the World Bank, global urban population reached 56% in 2023 and is projected to approach 70% by 2050, increasing residential property concentration and insurance penetration potential. According to the Swiss Re Institute, global insured losses from natural catastrophes reached about USD 100 billion in 2023, highlighting growing demand for property protection products such as home insurance.

Market Size and Forecast

-

Market Size in 2026E: USD 293.72 Billion

-

Market Size by 2035: USD 621.87 Billion

-

CAGR: 8.70% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Home Insurance Market - Request Free Sample Report

Home Insurance Market Trends

-

Rising frequency of natural disasters and climate-related risks driving increased demand for comprehensive home insurance coverage and risk protection

-

Growing adoption of digital insurance platforms enabling online policy purchase, automated claims processing, and enhanced customer experience

-

Increasing integration of smart home technologies and IoT devices supporting usage-based insurance models and proactive risk assessment

-

Expanding demand for customized insurance policies covering property damage, theft, liability, and additional living expenses to meet diverse homeowner needs

-

Continuous use of AI, predictive analytics, and data-driven underwriting improving fraud detection, pricing accuracy, and claims management efficiency

The U.S. Home Insurance Market Outlook

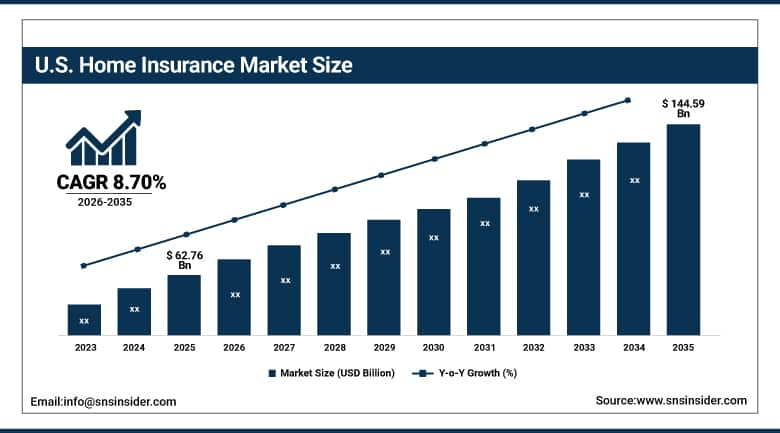

The U.S. Home Insurance Market was valued at approximately USD 62.76 Billion in 2025 and is expected to reach approximately USD 144.59 Billion by 2035, growing at a CAGR of approximately 8.70%.

The United States is the world's largest single national home insurance market, sustained by the combination of the world's largest residential property ownership market by aggregate insured value, mortgage-contingent insurance requirements that make home insurance functionally mandatory for approximately 65 percent of U.S. homeowners who carry a mortgage, and the highest exposure to natural catastrophe loss of any major economy whose combined hurricane, wildfire, tornado, and winter storm risk creates both insurance market necessity and premium rate escalation pressure.

Progressive Corporation achieved 40 percent growth in its homeowners insurance premium volume in 2025, driven by geographic expansion into markets vacated by competitors retreating from catastrophe-exposed states and its usage of telematics and smart home data integration to achieve more precise risk selection than traditional actuarial approaches allow.

Home Insurance Market Segment Analysis

-

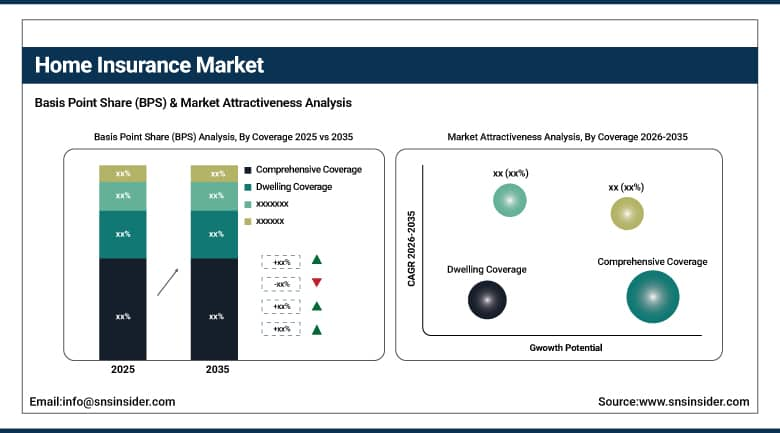

By Coverage, Comprehensive Coverage segment dominated the Home Insurance Market in 2025 with 46% share; Dwelling Coverage segment is the fastest growing segment.

-

By Distribution Channel, Tied Agents & Branches segment dominated the market in 2025 with 52% share; Brokers segment is the fastest growing segment.

-

By End Use, Landlords segment dominated the market in 2025 with 57% share; Tenants segment is the fastest growing segment.

By Coverage, Comprehensive Coverage segment dominates the Home Insurance Market, Dwelling Coverage segment expected to grow fastest

The Comprehensive Coverage segment dominated the Home Insurance Market in 2025 owing to its wide protection against diverse risks such as fire, theft, natural calamities, and other forms of damage. Customers are more inclined towards comprehensive coverage as it provides higher security and reduces the burden of maintaining various separate insurance policies. The increasing consciousness about property coverage and the growth in the value of assets are the additional factors contributing to the growth of this segment.

The Dwelling Coverage segment is the fastest growing in the Home Insurance Market due to increasing demand for basic structural protection at low premiums. Customers are choosing dwelling coverage as it provides basic coverage for the safety of the structure of the property from core risks. Increasing housing construction, mandatory insurance requirement on mortgages, and consciousness about the risks of damage to property are some of the factors driving this segment.

By Distribution Channel, Tied Agents & Branches segment dominates the Home Insurance Market, Brokers segment expected to grow fastest

The Tied Agents & Branches segment dominated the Home Insurance Market in 2025 owing to high level of consumer trust, customized advisory services, and pre-existing insurer networks. Most consumers find it convenient to interact in person while learning about insurance coverage, policies, claim process, etc. In addition, the advantages of this sales channel include pre-existing relations with clients and penetration in urban as well as semi-urban areas. The reliability and advisory nature of this sales channel continues to make it the most preferred one.

The Brokers segment is the fastest growing in the Home Insurance Market owing to the increased need for unbiased advice, comparison of different policies, and customization of insurance policies. The presence of different insurers makes it possible for consumers to choose from a wide range of competitive and flexible policies. Increased digitalization, cost optimization, and growth of online insurance brokers are helping the segment grow rapidly.

By End Use, Landlords segment dominates the Home Insurance Market, Tenants segment expected to grow fastest

The Landlords segment dominated the Home Insurance Market in 2025 because of the increasing concern by landlords of protecting their rental properties from any form of damage or liability claims or income loss. Increased investment in real estate and rentals has resulted in an increased insurance uptake among landlords. Insurance can be used to protect the value of the property and secure the owner financially in case there are any forms of damage or liabilities by tenants. The increasing need for risk management has resulted in landlords being the dominant end-users of home insurance in the market.

The Tenants segment is the fastest growing in the Home Insurance Market owing to factors like growing urbanization, increased presence of rental housing, and the awareness regarding the protection of their personal possessions. It is being observed that tenants prefer insurance plans that provide coverage for their contents, liability, and costs of alternative accommodation. Premium rates affordability, ease of buying insurance online, and mobility of the younger generation are some of the factors contributing towards this trend.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

84.73% |

|

Europe |

Germany |

22.84% |

|

Asia Pacific |

China |

32.84% |

|

Middle East & Africa |

UAE |

22.84% |

|

Latin America |

Brazil |

43.84% |

North America Home Insurance Market Insights

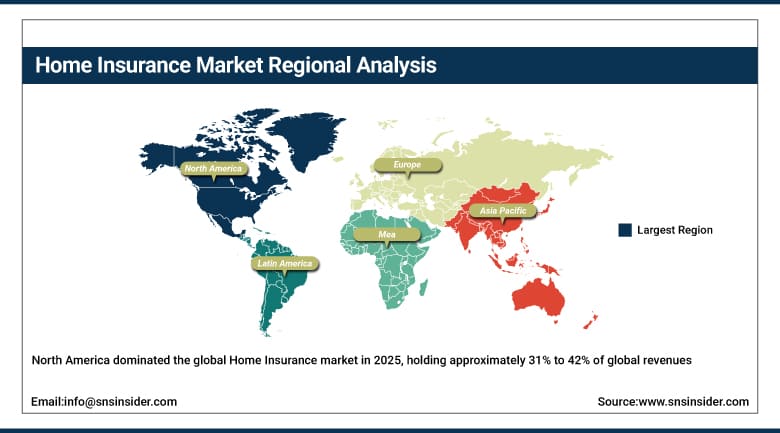

North America dominated the global Home Insurance market in 2025, holding approximately 31% to 42% of global revenues depending on market scope definition. The United States accounts for approximately 84.73% of regional revenue through its combination of the world's largest residential property market by aggregate insured value, mortgage-contingent coverage requirements affecting approximately 65 percent of homeowners, and the highest natural catastrophe exposure of any major economy.

State Farm, Allstate, USAA, Liberty Mutual, and Farmers Insurance each maintain substantial market positions through their underwriting scale, claims infrastructure, and distribution network breadth. Canada contributes supplementary North American demand through its growing residential property market, whose major urban markets in Toronto and Vancouver have experienced substantial property value appreciation creating growing insured values per policy.

According to the Federal Emergency Management Agency (FEMA), the United States experiences billions of dollars in annual disaster-related property losses, particularly from hurricanes, floods, and wildfires, highlighting the increasing exposure of residential assets to climate-related risks.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Home Insurance Market Insights

Europe held approximately 26.84% of global Home Insurance revenues in 2025. Germany accounts for approximately 22.84% of European revenues through its large established residential insurance market, the domestic presence of Allianz, Munich Re's primary insurance operations, and the German property market's high average property values and strong homeownership culture.

The UK represents Europe's most developed and competitively structured home insurance market, where price comparison websites including Comparethemarket and GoCompare have driven digital distribution adoption that is the highest nationally within Europe. France, Italy, and the Netherlands each contribute meaningful European demand through their residential property markets and mandatory or near-mandatory home insurance requirements under mortgage lending standards.

Asia Pacific Home Insurance Market Insights

Asia Pacific is the fastest-growing regional Home Insurance market, projected to expand at a CAGR exceeding 10% through 2035, driven by rising homeownership rates as expanding middle-class populations across China, India, Southeast Asia, and South Korea increasingly purchase residential property whose value protection against natural disaster and theft risk motivates growing insurance adoption.

China accounts for approximately 32.84% of Asia Pacific revenues through its massive residential property market, growing consumer awareness of financial risk protection, and the domestic home insurance market's progressive development from near-zero penetration in the 1990s toward meaningful coverage rates in major urban markets. India is growing rapidly through mortgage market expansion whose lender-imposed insurance requirements are creating first-time home insurance purchase demand among the growing cohort of urban first-time homebuyers.

MEA & Latin America Home Insurance Market Insights

Middle East and Latin America are growing Home Insurance markets where urbanisation, increasing homeownership, and rising awareness of financial risk protection are creating expanding demand. The UAE leads MEA revenues at approximately 22.84% of the regional total through its high-value residential property market, expatriate resident property ownership, and regulatory frameworks that encourage home insurance adoption. Saudi Arabia's growing residential property market and Vision 2030 programme supporting financial services sector development contribute secondary MEA demand.

Brazil leads Latin American revenues at approximately 43.84% of the regional total through its large urban residential market, growing middle class homeownership rate, and domestic insurance company distribution networks providing home insurance access across major Brazilian metropolitan markets.

Market Dynamics

Growth Drivers: Rising climate disasters and property values increase demand and insured exposure

The progressive increase in global natural catastrophe loss frequency and severity is creating sustained upward pressure on home insurance premium rates and demand for coverage breadth that simultaneously expands market revenue. Swiss Re estimates that global insured natural catastrophe losses have exceeded USD 100 billion annually in four of the five years from 2020 to 2024, and Munich Re's analysis of climate trend attribution in catastrophe loss data indicates that extreme precipitation, wildfire risk, and storm intensity will continue increasing through the forecast period in ways that compound both the frequency and severity of insured events.

Each major catastrophe event in a new or underinsured geographic area creates a demonstration effect where previously uninsured or underinsured homeowners in affected and adjacent communities recognise their exposure and acquire or upgrade coverage, expanding the insured property base.

Restraints: High-risk market withdrawals and affordability issues create coverage gaps and regulatory pressure

The structural challenge confronting the home insurance industry in the highest-risk markets including coastal Florida, wildfire-exposed California counties, and coastal Louisiana is the fundamental economic incompatibility between the actuarially adequate premium levels that insurers require to cover expected loss costs plus expenses with a reasonable profit margin, and the consumer affordability and political acceptability of premium rates that reflect full catastrophe risk pricing.

California's Proposition 103 insurance rate regulation framework, which requires prior regulatory approval for rate increases and prohibits the use of forward-looking catastrophe models in rate justification, created a regulatory environment in which major insurers could not achieve approval for premium rates adequate to cover California wildfire risk at 2020 and 2021 wildfire loss levels, precipitating the withdrawal of multiple major carriers from new business and non-renewal of existing policies.

Opportunities: InsurTech platforms and parametric insurance expand access and improve underserved market reach

InsurTech platforms including Lemonade, Hippo, Root, and Kin are demonstrating that digital-native home insurance distribution and claims processing can reduce customer acquisition cost, accelerate policy issuance, and improve claims experience to levels that create customer satisfaction and retention advantages over traditional channel alternatives. Lemonade's AI-powered claims processing, which resolves simple property loss claims in seconds through automated damage assessment and payment approval, represents the experiential benchmark that traditional insurers must approach to remain competitive for digital-native consumer segments whose service expectations are set by fintech and e-commerce rather than insurance historical norms.

Parametric home insurance products whose predetermined payment amounts trigger automatically on verified meteorological events provide immediate financial support that enables homeowners to begin recovery without waiting for claims adjustment, addressing the most common consumer complaint about traditional insurance whose adjustment-dependent payment timelines create financial hardship during the period when recovery investment is most urgently needed.

Recent Developments:

-

2025: State Farm announced the non-renewal of approximately 30,000 California home insurance policies in wildfire-exposed counties, reflecting the industry-wide structural challenge of achieving actuarially adequate premium rates under California's rate regulation framework and triggering regulatory reform discussions regarding California's insurance market sustainability.

-

2025: Progressive Corporation achieved 40 percent growth in homeowners insurance premium volume driven by geographic expansion into markets vacated by competitors and its Snapshot Home smart device integration programme providing premium discounts for policyholders installing water, fire, and intrusion monitoring devices.

-

2024: Lemonade Insurance announced expansion of its AI-powered homeowners insurance platform to additional U.S. states and European markets, with its automated claims processing system demonstrated to resolve eligible claims within minutes of submission using AI photo assessment and fraud detection that reduced claims adjustment cost and payment timeline simultaneously.

Home Insurance Market Key Players are:

-

Amica Mutual Insurance Company

-

State Farm

-

Allstate Corporation

-

Travelers Companies

-

Nationwide Mutual Insurance Company

-

Farmers Insurance Group

-

Progressive Corporation

-

USAA

-

Chubb Limited

-

The Hartford

-

Liberty Mutual Insurance

-

American Family Insurance

-

Erie Insurance Group

-

Auto-Owners Insurance

-

MetLife

-

Zurich Insurance Group

-

AXA

-

Aviva

-

Berkshire Hathaway

-

Reliance General Insurance

Home Insurance Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 269.92 Billion |

| Market Size by 2035 | USD 269.92 Billion |

| CAGR | CAGR of 8.70% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Coverage (Comprehensive Coverage, Dwelling Coverage, Content Coverage, Other Optional Coverage) • By Distribution Channel (Tied Agents & Branches, Brokers, Others) • By End Use (Landlords, Tenants) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Amica Mutual Insurance Company, State Farm, Allstate Corporation, Travelers Companies, Nationwide Mutual Insurance Company, Farmers Insurance Group, Progressive Corporation, USAA, Chubb Limited, The Hartford, Liberty Mutual Insurance, American Family Insurance, Erie Insurance Group, Auto-Owners Insurance, MetLife, Zurich Insurance Group, AXA, Aviva, Berkshire Hathaway, Reliance General Insurance. |

Frequently Asked Questions

The comprehensive coverage segment dominated the Home Insurance Market.

North America dominated the Home Insurance Market in 2025.

The Home Insurance Market was valued at USD 269.92 Billion in 2025.

Rising disasters, higher property values, homeownership growth, mortgage mandates, InsurTech adoption, and expanding middle-class demand drive market growth.

The Home Insurance Market is expected to grow at a CAGR of 8.70% from 2026 to 2035.

Get in Touch