Naphthalene Derivatives Market Report Scope & Overview

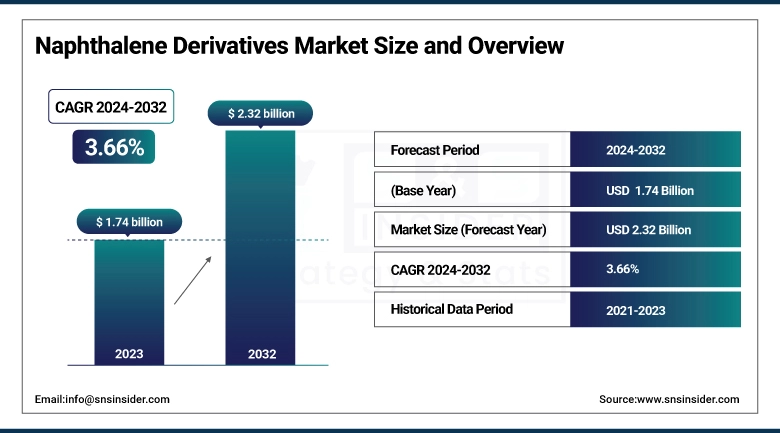

The Naphthalene Derivatives Market size was valued at USD 1.74 billion in 2024 and is expected to reach USD 2.32 billion by 2032, growing at a CAGR of 3.66% over the forecast period of 2025-2032.

Naphthalene Derivatives Market Analysis indicates that the rising utilization of agrochemicals, including pesticides and herbicides, is a key driver of market growth. The growth is driven by the use of naphthalene-based compounds is frequently employed in the fabrication of agrochemicals, especially naphthalene sulfonates, owing to their high dispersing and wetting activity. With a rapidly expanding population to feed, global agricultural requirements are continually increasing, meaning that there is a growing demand for more high-efficiency crop protection products. Such derivatives augment the performance and stability of pesticides and herbicides to control pests and crop yield.

Naphthalene Derivatives Market Size and Forecast

-

Market Size in 2024: USD 1.74 Billion

-

Market Size by 2032: USD 2.32 Billion

-

CAGR: 3.66% from 2025 to 2032

-

Base Year: 2024

-

Forecast Period: 2025–2032

-

Historical Data: 2022–2023

To Get more information on Naphthalene Derivatives Market - Request Free Sample Report

Naphthalene Derivatives Market Trends

-

Growing demand from the construction industry is driving consumption of naphthalene-based superplasticizers, with over 60% of usage linked to concrete admixtures for improved strength and durability.

-

Rising application in agrochemicals (pesticides and dispersants) is boosting market growth, contributing to around 20–25% of total demand globally.

-

Increasing use in textiles and dyes is supporting steady demand, particularly in Asia-Pacific, which accounts for over 45% of global consumption.

-

Expansion of oil & gas and chemical processing sectors is driving demand for surfactants and intermediates, growing at a CAGR of 5–6%.

-

Environmental regulations and shift toward low-toxicity alternatives are influencing product innovation, with over 30% of manufacturers investing in eco-friendly derivative formulations.

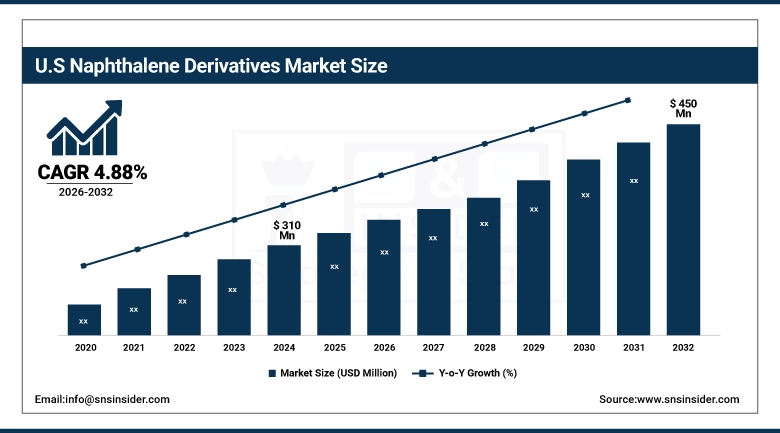

The U.S. Naphthalene Derivatives Market size was valued at USD 310 million in 2024 and is expected to reach USD 450 million by 2032, growing at a CAGR of 4.88% in the forecast period of 2025-2032. The growth is attributed to its well-established industrial base, impacting demand from key end-use industries, and its innovative market leadership in chemical manufacturing. With substantial investment toward infrastructural development, there exists a strong construction industry around the country, which spurs demand for naphthalene-based superplasticizers, such as sulphonated naphthalene formaldehyde (SNF) for better concrete performance. Moreover, the U.S. consumer agrochemicals and pharmaceuticals in the greatest areas of application of naphthalene derivatives are dispersants and intermediates. The availability of key chemical players, developed R&D facilities, and stringent regulations aids in the manufacturing of high-purity and specialty naphthalene derivatives.

In 2023, Dow introduced a high-performance solvent for industrial use. This addition provides Dow with an improved portfolio to produce solvents, offering lower toxicity, increased efficiency, and superior performance for a wide range of industrial applications.

Market Dynamics:

Drivers:

-

Rising Demand from the Construction Industry Drives the Market Growth

One of the most important drivers for naphthalene derivatives is the increasing demand from the construction sector. Naphthalene sulfonates are one of the most widely used superplasticizers in concrete based on naphthalene-derived compounds. The resulting superplasticizers, which are used in the production of concrete components, improve the workability, strength, and durability of concrete and are essential for many contemporary construction applications, including high-rise buildings, bridges, tunnels, and infrastructure projects. The global boom in urbanization and growing expenditure by governments on infrastructure development, particularly in developing countries, is driving demand for superior construction materials, fuelling the naphthalene derivatives market growth over the assessment period.

Total construction spending in the U.S. was at a seasonally adjusted annual rate of USD 2.196 trillion in March 2025, up 2.8% from the level of March 2024, according to a release from the U.S. Census Bureau. Residential construction spending was USD 937.7 billion. The rise is in line with the continual growth in private and public construction sectors, indicating high consumption of construction materials and additives such as naphthalene-based.

Restraints:

-

High Manufacturing and Processing Costs may hamper the Market Growth.

The large manufacturing and processing costs associated with naphthalene derivatives are a major restraint on the growth of the market. The synthesis of these substances is complex and energy-intensive, utilizing advanced technology and high standards in the manufacture (purity and performance). Moreover, raw materials, such as coal tar or petroleum-based feedstocks that need to be collected can be costly and are also exposed to price fluctuations that escalate production costs. Such expensive costs usually lead to higher prices of final products, which results in difficulty for manufacturers to compete with other chemicals or solvents that can perform similar functions at a lower price. Additionally, extra cost burdens from investments in environmentally compliant and safer production methods compound the cost.

Opportunities:

-

Increasing Adoption of Specialty Chemical Formulations is Creating Opportunities for Market Growth

The rising use of specialty chemical formulations in naphthalene market is expected to provide an essential growth opportunity for the naphthalene derivatives market. Quality of naphthalene derivatives not only bears marks of their functionality for disposable chemicals like dispersants, plasticizers, and superplasticizers, but also offers significant chemical properties, such as better dispersing ability, superior water solubility, along with compatibility with a variety of industrial processes. Naphthalene, over the years, has emerged as a basic ingredient needed to develop products that provide innovation and functionality as well as sustainability for new formulations, as these industries develop new formulations that enhance performance, durability, and productivity. This is especially prominent in the construction sector, where naphthalene-based superplasticizers enhance the strength and durability of concrete and reduce the overall water demand, which drives the naphthalene derivatives market trends.

The U.S. International Trade Administration, in mid-2024, the U.S. chemical manufacturing industry employed 902,300 employees direct count and the industry had total foreign direct investment lodged at USD 766.7 billion in 2023. Almost all are national in scope, and approximately 550,000 workers nationwide are employed in 14,000 establishments producing more than 70,000 products and specialty chemicals, including adhesives, sealants, water treatment chemicals, plastic additives, catalysts, and coatings. These performance chemicals are frequently bundled with customer and technical servicing as part of the sale, indicating the degree of innovation and specialized application to engineering thought and application in this area.

Segmentation Analysis:

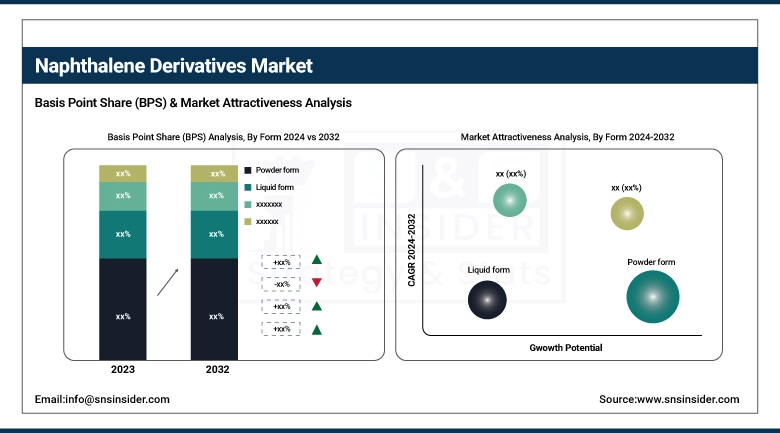

By Form

Powder held the largest Naphthalene Derivatives market share, around 66%, in 2024. It is due to its widespread use, ease of handling, and superior performance characteristics within industries. Particularly, powdered naphthalene derivatives (naphthalene sulfonate formaldehyde condensates, NSFC) are most suitable for construction applications (in the formulation of concrete superplasticizers) owing to their superior solubility, long shelf life, and reproducible dispersing behavior. Moreover, it is chemically and physically more stable in powder form than in liquid form, which keeps the powder value for industrial usage at a low cost. It is also applied in agrochemicals where powdered derivatives are utilized to produce dispersants in pesticides and herbicides, likewise in textile and dye, with strict dosing and mixing homogeneity.

Liquid held a significant market share and was the fastest-growing segment over the forecast period owing to its wide range of applications and availability of naphthalene derivatives in the liquid state enables easy integration in different industrial processes. Liquid derivatives of naphthalene are especially appealing in agrochemical, textile, and pharmaceutical industries as they can dissolve and blend quickly with other components and take little to no time to process, as there is no extra dissolution step. As a result of their application in liquid dispersants and surfactants, such as for herbicides or dyes, they are widely used in contemporary agriculture and textile production.

By Derivative

The sulphonated naphthalene formaldehyde segment held the largest market share, around 32.44%, in 2024. It is due to its widespread application as a high-performance dispersing agent, in particular, in the construction industry. SNF is used in the manufacture of superplasticizers for concrete, offering greatly improved workability, strength, and durability with no added water. It is, therefore, a highly sought-after material for use in infrastructure projects, such as bridges, highways, and high-rise buildings, where access to raw materials that could provide better concrete properties is of utmost importance. SNF is stable thermally and chemically, thus making it ideal to be deployed across climatic and operational conditions. It is used in various applications in addition to construction, such as agrochemicals and dyes, to disperse active ingredients to mix uniformly.

The Naphthalene Sulphonic Acid segment held a significant market share and was the fastest-growing segment in the forecast period owing to its importance as a chemical intermediate and to ensuring its use in different industrial applications. NSA has extensive application in the textile and leather industries for the manufacturing of dyes, pigments, and artificial tanning agents. With good solubility and strong sulfonating, it can be applied to improve dyeing processes and enhance color fastness. NSA is also an important ingredient in the production of dispersants and wetting agents, especially for the application in the manufacturing of agrochemicals and construction.

By End-use Industry

The construction segment held the largest market share, around 28%, in 2024. The segment’s expansion is driven by the high application of naphthalene-based compounds, especially Sulphonated Naphthalene Formaldehyde (SNF), as concrete admixtures. SNF is a high-efficiency superplasticizer that increases workability, strength, and durability of concrete through severe water content reduction without loss of performance. This means that it is a key part of modern construction practice, particularly large infrastructure jobs including freeways, bridges, tunnels, and skyscrapers. The global demand for high-performance construction materials has increased due to swift urbanization, a growing population, and rising investment in infrastructure development in developed and emerging economies.

Pharmaceuticals held a significant market share due to the vital importance of these compounds as an intermediate in drug synthesis and formulation. Naphthalene derivatives are utilized in the production of certain medicaments, such as antiseptics, antifungal agents, and other non-high potency therapeutic agents. Owing to their unique chemical structure, they can easily be modified to generate novel molecules with desired biological activity. The high purity and stability of these derivatives are also appreciated by the pharmaceutical industry and are important factors for ensuring a product that is both safe and effective. The increasing need for drugs globally, supported by an aging population, greater healthcare access, and the growing burden of chronic diseases, has also been favorable for using naphthalene derivatives in this sector.

Regional Analysis:

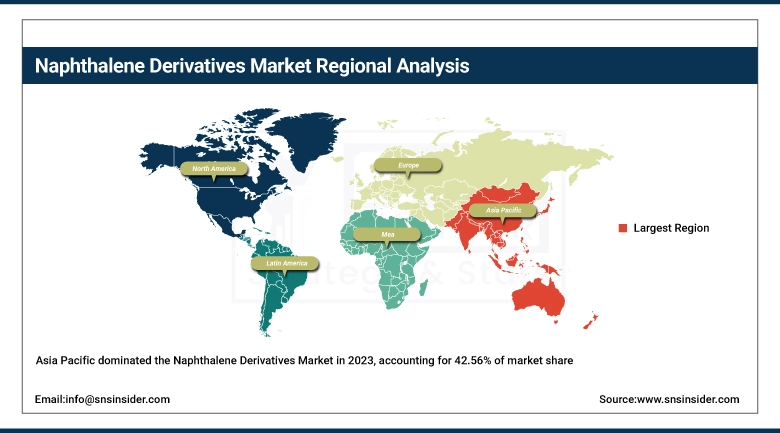

Asia Pacific held the largest market share, around 42.56%, in 2024. This growth is owing to rapid urbanization and booming infrastructure development. With the construction activities expected to gain momentum, particularly in China, India, and Southeast Asian countries, demand for naphthalene-based superplasticizers (based on concrete admixtures), naphthalene intermediates are likely to increase in the future. Furthermore, it is one of the world's largest consumer regions of naphthalene derivatives, such as dispersants and dye intermediates, which is attributable to the growing textile and agrochemical industry in the region. The availability of cheap manufacturing units, raw materials, and favourable government policies enabled large-scale chemical plants across the globe. Additionally, the continuous growth of the global population and the increase in the consumption of pharmaceuticals, dyes, and agro-products have driven the growth of the market.

Get Customized Report as per Your Business Requirement - Enquiry Now

For instance, in August 2024, BASF entered into a Memorandum of Understanding (MoU) with UPC Technology Corporation for regional cooperation on the supply of plasticizer alcohols and catalysts for phthalic anhydride and maleic anhydride production processes.

North America held a significant market share and growing region over the forecast period. It can be attributed to the well-established infrastructure of the region, the presence of key end-use industries in the region, and advanced technological developments in chemical manufacturing. The construction, pharmaceutical, textile, and agrochemical sectors are U.S. and Canada-based major industries, which will further boost the demand for naphthalene derivatives, owing to high application rates in concrete admixtures, dye intermediates, and pesticide formulations. In addition, strict quality norms and high spending on R&D also led to the usage of better specialty chemicals, such as sulphonated naphthalene formaldehyde and naphthalene sulphonic acid. The increasing investment in energy-efficient and sustainable construction practices in the region also supports demand for composition additives such as naphthalene-based superplasticizers.

Europe held a significant market share in 2024 due to a stringent regulation, a high industrial base, and a rising green chemistry and sustainability trend. It also puts pressure on manufacturers to pursue Naphthalene Derivatives with proven compliance, making those products a sound investment for the long term. Besides that, the legacy of Europe’s large pharmaceuticals, paints and coatings, and cosmetics industries commands a large fraction of solvent use there. Top naphthalene derivatives companies focus on innovation and sustainability, which are driving forces in Germany, France, and the U.K.

Key Players:

The leading players in the market are BASF SE, Arkema Group, Clariant, Huntsman Corporation, Koppers Inc., Evonik Industries AG, King Industries, Inc., Cromogenia Units, Rain Carbon Inc., and JFE Chemical Corporation.

Recent Developments:

-

In 2024, Koppers has also increased its coal tar distillation capacity 2024 to provide naphthalene-based intermediates that are used to manufacture construction chemicals and resins.

-

In 2024, Himadri Specialist Chemical Ltd launched a new range of rheology modifiers based on high-performance naphthalene derivatives, which are primarily used for textile dispersants and construction chemicals, and expanded exports to Southeast Asia.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 1.74 Billion |

| Market Size by 2032 | USD 2.32 Billion |

| CAGR | CAGR of3.66% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Form (Liquid form, Powder form) • By Derivative (Sulphonated Naphthalene Formaldehyde (SNF), Phthalic Anhydride, Naphthalene Sulphonic Acid, Alkyl Naphthalene Sulphonate Salts (ANS), Naphthols, Others) • By End-Use Industry (Paints & Coatings, Pharmaceuticals, Personal Care, Crop Protection, Lubricants, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | BASF SE, Arkema Group, Clariant, Huntsman Corporation, Koppers Inc., Evonik Industries AG, King Industries, Inc., Cromogenia Units, Rain Carbon Inc., JFE Chemical Corporation |

Frequently Asked Questions

Ans: Asia Pacific led the Naphthalene Derivatives Market in the region with the highest revenue share in 2023.

Ans: Rising Demand from the Construction Industry Drives the Market Growth.

Ans: Powder will grow rapidly in the Naphthalene Derivatives Market from 2024 to 2032.

Ans: The expected CAGR of the global Naphthalene Derivatives Market during the forecast period is 3.66%

Ans: The Naphthalene Derivatives Market was valued at USD 1.74 billion in 2024.

Get in touch