Industrial Catalyst Market Size & Overview:

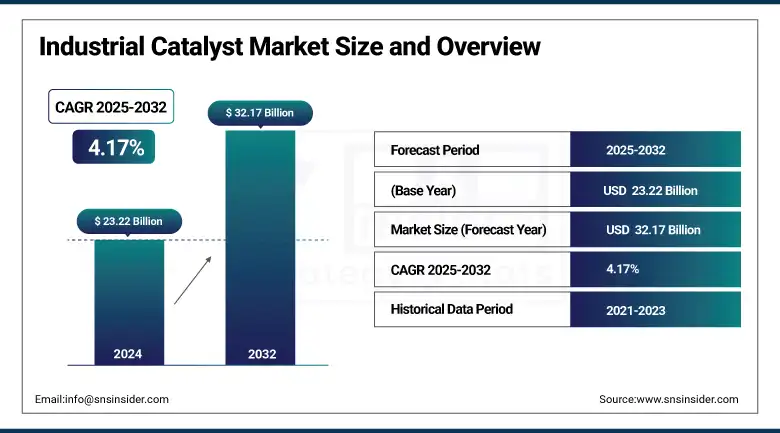

The Industrial Catalyst Market size was valued at USD 23.22 billion in 2024 and is expected to reach USD 32.17 billion by 2032, growing at a CAGR of 4.17% over the forecast period of 2025-2032.

The industrial catalyst market is transforming at a fast pace with respect to sustainability targets and technology advancements. Industrial catalyst players such as BASF are leading this growth through partnership, as it did with Plug Power to create sophisticated deoxo catalysts for clean hydrogen liquefaction plants, showcasing major industrial catalyst market trends. Pilot-scale synthesis facility investments, such as BASF's Catalyst Development and Solids Processing Center, are increasing access to new chemical catalysts, fueling the chemical catalyst market and refinery catalyst market segments. Artificial intelligence and digital tools are revolutionizing industrial catalyst market analysis, and technologies such as BASF's Fourtiva catalytic cracking catalyst enhance refinery performance. Current information indicates U.S. crude inventories dropped by 11.5 million barrels, reducing refinery utilization to 93.2%, and EIA predicts a 20% reduction in U.S. net crude oil imports by 2025. Such factors form a positive industrial catalyst industry scenario with a growing industrial catalyst market share and size.

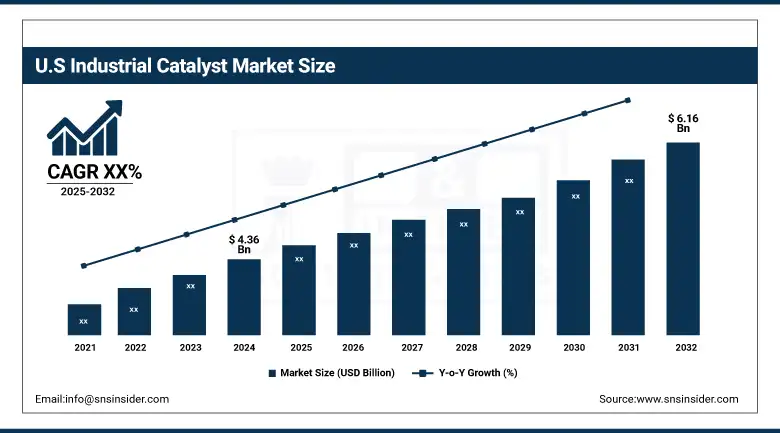

In the region, the U.S. is adopting commercial catalysts on a large scale in the refining and chemical industries. The value of their market size is approximately USD 4.36 billion and is projected to be USD 6.16 billion by 2032. Global corporations like BASF and Honeywell are collaborating with national labs to advance hydro processing and cracking catalysts. The Clean Energy Catalysis initiatives funded by the U.S. DOE help underpin this ecosystem, while government environmental agencies will be mandating significant cuts in emissions across industrial locations, resulting in increased urgency. These activities have collectively reinforced the U.S. as the leader in the deployment of industrial catalysts while helping to channel future growth in the innovation related to catalytic efficiency and sustainability.

Industrial Catalyst Market Dynamics:

Drivers:

-

Government funding for industrial decarbonization accelerates catalyst innovation and adoption

The U.S. Department of Energy has funded a $156 million opportunity for applied research, development, and demonstration projects aimed at emissions reduction in the industrial sector. This investment supports the industrial catalyst market growth by facilitating pilot-scale synthesis of new chemical processing catalysts and promoting collaboration between government labs and industrial catalyst firms. By funding projects that incorporate advanced catalyst materials into current processes, this effort supports industrial catalyst market trends towards sustainable production and enhances the industrial catalyst industry outlook for lower-carbon operations.

-

Advances in artificial intelligence and autonomous labs expedite catalyst discovery processes

With initial funding of $35 million, the ARPA‑E CATALCHEM‑E program is using artificial intelligence and autonomous laboratories to shorten the catalyst-development timeline from years to months. High-throughput experimentation platforms and machine- learning models are being used to predict and screen optimal catalyst compositions for various refinery and chemical processing applications and are definitively accelerating industrial catalyst market trends toward digital design. These technological advancements are improving industrial catalyst market assessments as they relate closely to organometallic and biocatalyst candidates' rapid screening, while simultaneously ensuring sustainable industrial catalyst market share increases and advancing the chemical processing catalysts market.

Restraints:

-

Capital expenditure requirements for advanced emission control systems burden industrial operators

In order to comply with the EPA's final rules on toxic air pollutants, facilities need to install selective or non-selective catalytic reduction systems, which involve large capital and operating costs. The EPA fact sheet on decreasing toxic emissions indicates that overall, there are potential reductions in harmful pollutants by 56,000 tons in the fifth year post-promulgation; however, there are still high upfront costs for advanced emission-control equipment. This reality of significant upfront costs means refineries and industrial facilities are limited in their budgets, which similarly limits the size of the industrial catalyst market and curtails the growth of the refinery catalyst market.

Industrial Catalyst Market Segmentation Analysis:

By Type

Heterogeneous catalysts dominated the industrial catalyst market in 2024 with a market share of 48.2%, primarily from solid catalysts utilized in fluid catalytic cracking (FCC) in refinery processes. Heterogeneous catalysts are widely employed in petroleum refineries where they yield enhancements in conversion efficiency and selectivity toward products. The U.S. Department of Energy in 2023 was funding projects that aimed to improve FCC catalyst formulations (like BASF's innovation with Fourtiva catalysts), which corroborates the trends we are observing in the industrial catalyst market, favoring heterogeneous catalysts for sustainable refining operations.

Biocatalysts are the fastest-growing segment, expected to expand with a CAGR of 4.6% through 2032. This growth is fueled by an increasing demand for sustainable chemical processing and bio-based product development. For example, the launch of the ARPA-E CATALCHEM-E program will be in 2024 and will support the acceleration of the development of biocatalysts using AI-generated tools and autonomous labs, indicating a change in the industrial catalyst industry to a greener and more efficient catalytic process.

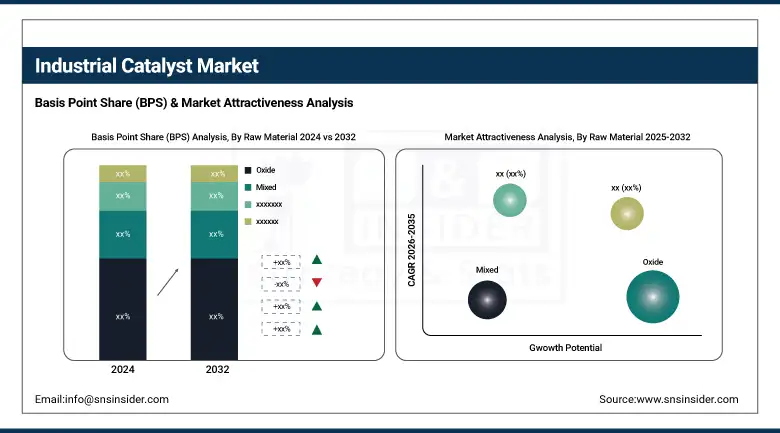

By Raw Material

Oxide catalysts held the highest industrial catalyst market share of 41.7% in 2024, largely due to their significant role in oxidation reactions in the petrochemical and refining industries. Commercial catalysts are primarily metal-oxides, such as alumina and silica-alumina are strong contenders due to thermal stability and catalytic activity. The American Chemical Society noted recently in their 2023 findings that oxide catalysts are at the center of sulfur emission reductions and improving the catalytic cracking process, which has benefited them for the industrial catalyst market assessment.

Organometallic catalysts are expected to be the fastest growing, with a projected CAGR of 5.48%, because they are increasingly being used in pharmaceutical manufacturing and precision chemical synthesis. The National Science Foundation noted that there is active R&D funding for the development of organometallic catalysts for sustainable and low-emission production as of 2024, further strengthening the chemical catalyst market and establishing multiple targeted molecular transformations with low byproducts.

By Application

The petroleum refinery segment dominated the industrial catalyst market in 2024 with an estimated market share of 43.5%, aided by continuing demand for clean fuels and newer, catalytic technologies. In 2024, the U.S. Energy Information Administration indicated that refinery utilization rates were approximately 93%. Given the trends and consolidating emissions regulations reducing global emissions, large oil companies such as Chevron and ExxonMobil are continuing to invest in new refinery catalysts, ensuring good results in the refinery catalyst market.

Chemical manufacturing is the fastest-growing segment, expected to witness a CAGR of 4.83% through 2032. This is largely due to the increased global demand for specialty and performance chemicals. In 2024, the U.S. Department of Energy's Advanced Manufacturing Office funded catalytic innovations directed toward emission reductions and energy efficiencies, which illustrates that the landscape of industrial catalyst market growth is moving to greener chemical production. These developments are helping this space to re-shape the chemical processing catalysts market with a new focus on sustainability and operational enhancements.

Industrial Catalyst Market Regional Outlook:

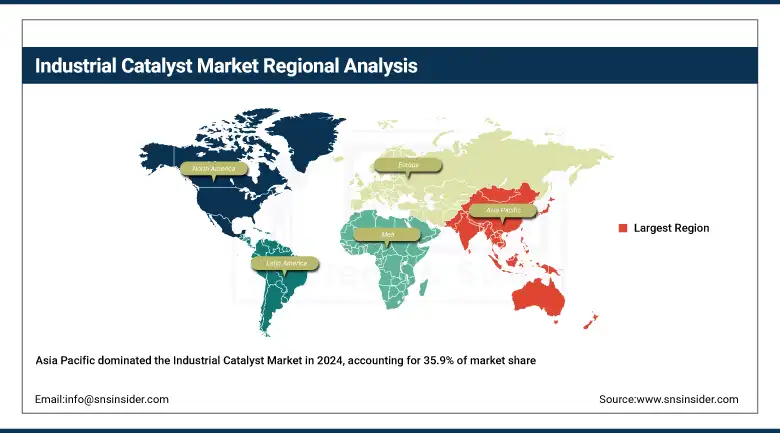

Asia Pacific dominated the industrial catalyst market in 2024 with a 35.9% market share, fueled by driven by a need for industrialization and massive refinery expansion across China, India, and Southeast Asia. The International Energy Agency indicated that regional governments were advancing refinery updates at even faster paces to respond to increasingly stringent environmental rules, with the region adding the most new catalysts, led by China and India. China's prominence as a country was evident, with PetroChina deploying ultra-low sulfur catalysts in 2023 under mandates of the Ministry of Ecology and Environment, and Sinopec advancing catalyst R&D with Tsinghua University, cementing China's role in regional market growth.

North America accounted for 27.8% of the industrial catalyst market share in 2024 and is projected to expand at the highest CAGR of 4.49% from 2025 to 2032. This solid growth is driven by innovative emissions regulations, advances in refinery catalysts, and large investments in decarbonization technology. The U.S. Department of Energy 2023 launched catalytic process innovations at $47 million. Also in 2024, Natural Resources Canada stated it had encouraged the adoption of clean catalyst technology through strategic grants using the clean catalyst strategy. Both the U.S. and Canada continue to invest substantial financial resources in low-emission chemical processing and maintain a strong role in the industrial catalyst sector.

In 2024, Europe had an industrial catalyst market share of 24.6%, ranking third in the global market. Several regulatory programs, including the Green Deal, the REPowerEU, and funding for Horizon Europe, have created a demand for sustainable catalysts. Additionally, Horizon Europe has supported R&D initiatives on green hydrogen and low-carbon synthesis. Germany has been the leader in the region, with the recent launch of advanced ammonia catalysts by BASF in 2023, while the Federal Ministry of Education and Research in Germany has put significant funding to support green chemistry innovations, solidifying the importance of Germany to European advancements in refinery and chemical catalysts.

Key Players:

The major industrial catalyst market competitors include BASF SE, Albemarle Corporation, Johnson Matthey Plc, Clariant AG, Evonik Industries AG, Haldor Topsoe A/S, W. R. Grace and Co., Sinopec Corporation, Criterion Catalysts & Technologies L.P., and LyondellBasell Industries Holdings B.V.

Recent Developments:

-

In May 2025, Umicore expanded its homogeneous catalyst production to meet rising industrial demand, aiming to strengthen its global footprint in sustainable catalytic technologies across diverse industrial applications.

-

In November 2024, BASF opened a new Asia Pacific headquarters in Singapore to boost regional operations, focusing on innovation and sustainability in industrial catalysts and chemical processing solutions.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 23.22 billion |

| Market Size by 2032 | USD 32.17 billion |

| CAGR | CAGR of 4.17% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Type (Heterogeneous, Homogeneous, Biocatalysts) •By Raw Material (Mixed, Oxide, Metallic, Sulfide, Organometallic) •By Application (Petroleum Refinery, Chemical Manufacturing, Petrochemical, Food Processing, Automotive and Transportation, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | BASF SE, Albemarle Corporation, Johnson Matthey Plc, Clariant AG, Evonik Industries AG, Haldor Topsoe A/S, W. R. Grace and Co., Sinopec Corporation, Criterion Catalysts & Technologies L.P., and LyondellBasell Industries Holdings B.V. |

Frequently Asked Questions

North America is the fastest-growing with a 4.49% CAGR, fueled by DOE decarbonization funding and advanced emission regulations across the U.S.

Asia Pacific dominates the Industrial Catalyst Market with a 35.9% share due to refinery expansions and catalyst R&D in China and India.

Germany leads Europe in the Industrial Catalyst Market, supported by BASF’s innovations and government-funded green catalyst R&D programs.

Heterogeneous catalysts led the Industrial Catalyst Market with 48.2% share due to widespread usage in refinery fluid catalytic cracking applications.

The Industrial Catalyst Market is projected to reach USD 32.17 billion by 2032, reflecting steady growth at a CAGR of 4.17% over the forecast period.

Get in Touch