Network Encryption Market Report Scope & Overview:

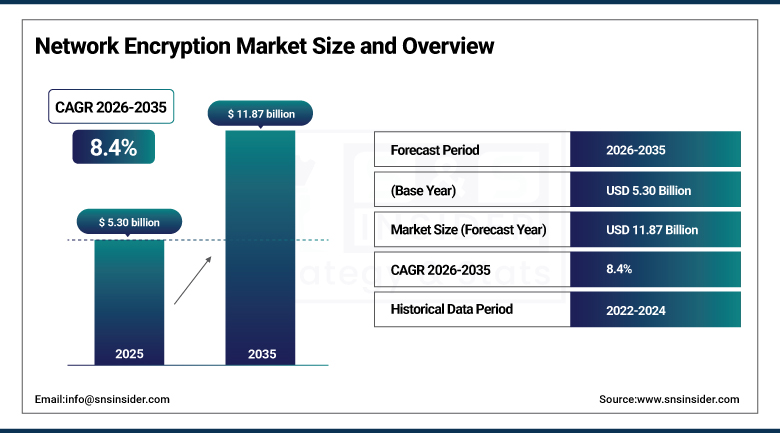

The Network Encryption Market was valued at USD 5.30 billion in 2025 and is expected to reach USD 11.87 billion by 2035, growing at a CAGR of 8.4% from 2026-2035.

The development of the Network Encryption Market is influenced by several factors such as increased cybersecurity threats, data breach incidents, and the increasing demand for encrypted communication among other things. Adoption of cloud computing, internet of things (IoT), and remote working has also been contributing towards the rising demand for encryption solutions. Strict data security laws and regulations have also been motivating enterprises to enhance their security posture. Moreover, digitalization is gaining momentum within various sectors such as BFSI, telecommunication, government, and information technology sectors.

Network Encryption Market Size and Forecast

-

Network Encryption Market Size in 2025: USD 5.30 Billion

-

Network Encryption Market Size by 2035: USD 11.87 Billion

-

CAGR: 8.4% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Network Encryption Market - Request Free Sample Report

Network Encryption Market Trends

-

Rising concerns over cyber threats, data breaches, and interception of sensitive information are driving the network encryption market.

-

Growing adoption across BFSI, government, healthcare, and enterprise IT networks is boosting market growth.

-

Expansion of cloud computing, remote work, and digital transformation initiatives is fueling encryption deployment.

-

Increasing focus on securing data in transit across wired, wireless, and hybrid networks is shaping adoption trends.

-

Advancements in quantum-resistant encryption, VPN technologies, and end-to-end encryption solutions are enhancing security strength.

-

Rising regulatory compliance requirements and data privacy laws are supporting market expansion.

-

Collaborations between cybersecurity providers, telecom operators, and enterprises are accelerating innovation and global adoption.

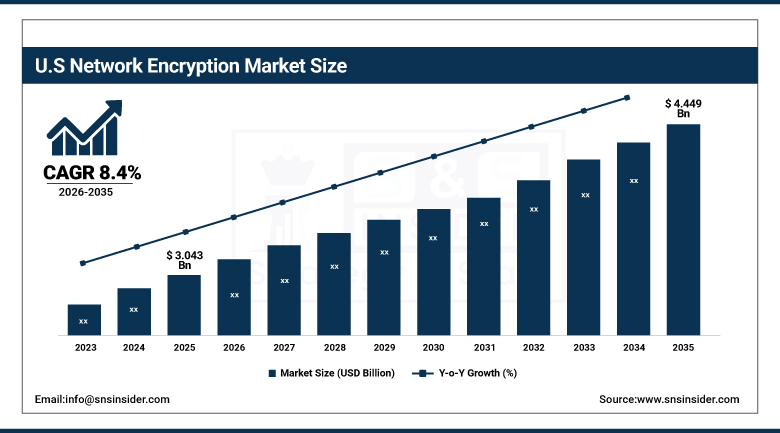

U.S. Network Encryption Market was valued at USD 1.30 billion in 2025 and is expected to reach USD 3.18 billion by 2035, growing at a CAGR of 9.34% from 2026-2035.

The growth of the U.S. Network Encryption Market can be attributed to rising cyberattacks, cloud computing, and increased need for secure data transmission. Increasing digital transformation, stringent data protection measures, and rising trend of remote working in the BFSI sector, government organizations, and IT companies are expected to fuel the growth of the market.

Network Encryption Market Segment Highlights

-

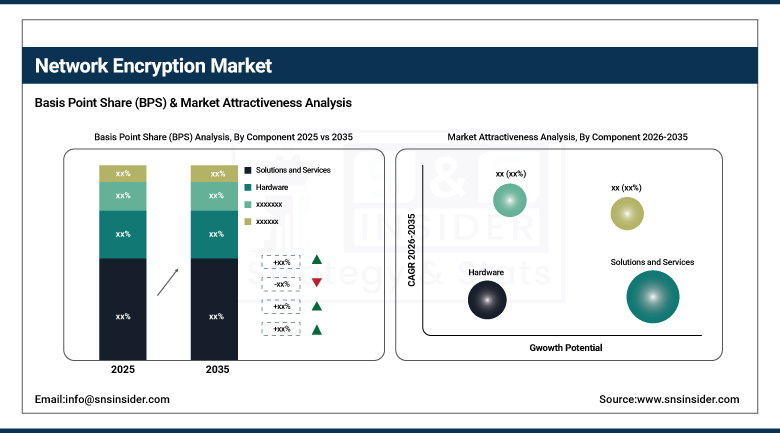

By Component, Solutions segment dominated the Network Encryption Market in 2025 with ~58% share; Services segment fastest growing during 2026–2035.

-

• By Deployment Mode, On-premises segment dominated the Network Encryption Market in 2025 with ~51% share; Cloud-based segment fastest growing during 2026–2035.

-

By Organization Size, Large Enterprises segment dominated the Network Encryption Market in 2025 with ~67% share; SMEs segment fastest growing during 2026–2035.

-

By End Use Industry, Telecom and IT segment dominated the Network Encryption Market in 2025 with ~34% share; BFSI segment fastest growing during 2026–2035.

Network Encryption Market Segment Analysis

By Component, Solutions segment dominates the Network Encryption Market, Services segment expected to grow fastest

The solutions segment dominates the network encryption market, owing to high demand for comprehensive encryption systems that can encrypt the information present in networks, endpoints, and cloud services. More enterprises today opt for end-to-end encryption systems for protecting confidential data from cyber attacks and regulations. Widespread deployment of cutting-edge encryption systems and other security hardware and software in organizational IT architectures reinforces the dominance of this category.

The services segment is registering tremendous growth due to the increasing requirement for professional services related to encryption management and compliance. There is an increasing need for organizations to engage service providers for managing encryption processes as it reduces complexity and provides compliance with changing cybersecurity regulations. Lack of sufficient in-house knowledge of cybersecurity issues and complexities in hybrid IT infrastructures are driving the demand for services in the network encryption domain.

By Deployment Mode, On-premises segment dominates the Network Encryption Market, Cloud-based segment expected to grow fastest

On-premises deployment dominates the network encryption market owing to the high preference by companies that desire to have absolute control over their critical information and security infrastructure. Companies operating in highly-regulated industries prefer on-premises installation for regulatory reasons, in order to preserve data sovereignty, and to minimize the risk of attacks from external sources. On-premises deployment enables the organization to customize encryption protocols.

Cloud-based deployment is growing rapidly because of the widespread use of cloud computing, telecommuting, and hybrid IT systems. There is an emerging trend among businesses towards implementing cloud-based encryption because of the advantages such systems provide regarding scalability, low initial investment, and simple deployment within networked environments. Another reason why cloud-based encryption is witnessing increased implementation is because of the rising popularity of SaaS software and multi-cloud ecosystems.

By Organization Size, Large Enterprises segment dominates the Network Encryption Market, SMEs segment expected to grow fastest

Large enterprises dominate the network encryption market due to their substantial IT resources and the amount of data they handle. They have to protect themselves from cyberattacks through the use of efficient encryption tools for secure communication as well as handling customer and finance data. Strict compliance rules make it mandatory for companies to implement advanced security measures. Their capability to afford expensive cyber security tools gives them a competitive edge in the market.

SMEs are the fastest-growing segment because of the awareness regarding cybersecurity threats and an increase in the number of data breaches in SMEs. The provision of affordable encryption services through clouds and subscription-based security methods has made advanced protection available to SMEs. Factors such as digital transformation and business growth on the Internet have also contributed to this phenomenon.

By End Use Industry, Telecom & IT segment dominates the Network Encryption Market, BFSI segment expected to grow fastest.

The telecom and IT vertical accounts for the largest share in the network encryption market, owing to the high volume of data transfer and the necessity to encrypt the networks to safeguard them against any intrusion. Telecommunications service providers cater to the large-scale movement of data via their mobile networks, broadband networks, and enterprise networks, and it becomes essential to secure the networks by providing adequate encryption.

The BFSI segment is the fastest-growing segment because of cyber threats aimed at financial transactions, banking platforms, and customer data. There has been a rising need to use digital banking and fintech applications to facilitate payments. In this market segment, regulatory compliance and real-time transmission of financial information make it necessary to install encryption techniques.

Network Encryption Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

91.3% |

|

Europe |

United Kingdom |

23.6% |

|

Asia Pacific |

Australia |

7.8% |

|

Middle East & Africa |

UAE |

14.2% |

|

Latin America |

Brazil |

49.1% |

North America Network Encryption Market Insights

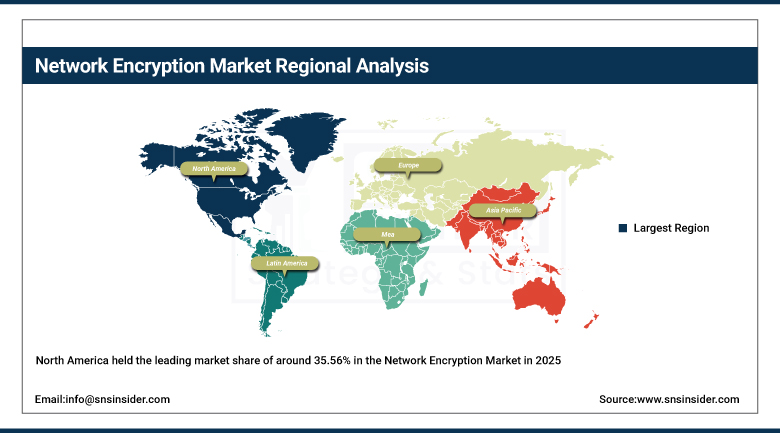

North America held the leading market share of around 35.56% in the Network Encryption Market in 2025 owing to the presence of robust cybersecurity frameworks, high penetration of cloud computing, and growing need for security of data transfers within businesses. In addition, the growth of this market can also be attributed to the availability of large technology players and developed IT ecosystems. Moreover, growing instances of cyber attacks, strict data security policies, and high investments in encryption technologies are further propelling the dominance of North America in the global market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Network Encryption Market Insights

Network Encryption Market in Asia-Pacific region will witness the highest CAGR owing to rapid digitalization and increasing concerns related to cybersecurity. The growing demand for data security owing to increased usage of cloud computing, Internet of Things, and 5G technologies is fueling the growth of the market. Investments in digitalization by governments of emerging economies coupled with growing infrastructure of IT and telecommunication sectors are aiding the growth of the market in Asia Pacific region.

Europe Network Encryption Market Insights

Europe Network Encryption Market is expected to witness strong growth owing to stringent data protection policies like GDPR and growing concern towards cybersecurity. With increased usage of cloud computing, banking applications, and industrial automation, there is an increasing need for better encryption services. Presence of strong BFSI, government, and manufacturing industries in Europe is also contributing positively to the growth of the market. European countries like Germany, the UK, and France are spending considerably on IT infrastructure security.

Middle East & Africa and Latin America Network Encryption Market Insights

Middle East & Africa and Latin America Network Encryption Market is witnessing gradual growth owing to the growing trend of digitalization and increased concern about cybersecurity. Growing telecom network infrastructure, cloud computing services, and e-commerce transactions are adding more demand for secure communication. Countries like Brazil, Mexico, UAE, and Saudi Arabia have made investments in digitalization and security framework. Limited availability of cybersecurity infrastructure and budgetary constraints act as major barriers for the growth of the market.

Network Encryption Market Growth Drivers:

-

Rapid Expansion of Cloud Computing, Remote Work, and Digital Transformation Driving Strong Demand for Network Encryption Solutions Globally

Greater usage of cloud computing systems, telecommuting, and digitization of businesses is leading to an increased demand for encrypted networking solutions around the world. Enterprises are quickly turning to encrypted communications to safeguard their sensitive data within public, private, and hybrid clouds. Growing trends in cyber attacks, data thefts, and ransomware threats are making it even more important to implement strong encryption systems. Businesses in various industries such as BFSI, healthcare, governmental organizations, and IT have been showing high spending in encrypted networking infrastructure. Digital transformations and greater internet connectivity are fueling the use of encrypted networking solutions.

Network Encryption Market Restraints:

-

High Implementation Costs and Complex Integration Processes Limiting Widespread Adoption of Network Encryption Solutions Across Small and Medium Enterprises

Expensive implementation of sophisticated encryption techniques is a hindrance to adoption by smaller companies due to the cost of hardware, software, and experienced professionals in cybersecurity. The incorporation of encryption technology into existing information technology systems can be difficult and time-consuming, demanding a great deal of technical skills and improvements to the systems. The cost involved in maintaining, updating, and adhering to regulations adds to operational costs. Moreover, performance issues related to encryption can affect network performance. All these factors hinder the extensive use of encryption technology in business organizations worldwide.

Network Encryption Market Opportunities:

-

Growing Adoption of IoT Devices, 5G Networks, and Connected Ecosystems Creating Strong Opportunities for Network Encryption Market Expansion

The rapid deployment of IoT devices, 5G technology, and other interconnected digital systems has resulted in great potential for development in network encryption services. The growing interaction among connected devices makes it necessary to ensure the availability of safe communication mediums for preventing any breaches from occurring within an ecosystem. Many different industries including smart cities, automobiles, healthcare, and industrial automation have been implementing encrypted networks in order to keep their data transmission safe. With increasing use of edge computing and AI technology, there is growing demand for safe data security services as well.

Recent Developments:

-

2026: Palo Alto Networks expanded AI-powered network security platforms with Prisma SASE upgrades, strengthening encrypted traffic inspection, secure access, and AI-driven threat prevention across enterprise networks and cloud environments.

-

2025: Cisco introduced AI-first Secure Network Architecture, improving encrypted traffic visibility, Zero Trust enforcement, and secure enterprise connectivity across hybrid environments. The update strengthens enterprise VPN and cloud encryption frameworks.

-

2025: IBM expanded hybrid cloud security and encryption services with AI-driven threat detection, improving secure network communication and enterprise-grade data encryption across distributed environments.

-

2025: Zscaler expanded Zero Trust Exchange platform with improved encrypted traffic inspection and secure access service edge (SASE) capabilities for enterprise network security.

-

2024: Palo Alto Networks launched AI-driven Prisma SASE enhancements, improving encrypted traffic inspection, secure access, and Zero Trust enforcement across cloud and enterprise networks.

Key Players

Some of the Network Encryption Market Companies

-

Cisco Systems, Inc.

-

Juniper Networks, Inc.

-

Palo Alto Networks, Inc.

-

Fortinet, Inc.

-

Check Point Software Technologies Ltd.

-

IBM Corporation

-

Thales Group

-

Micro Focus International plc

-

Broadcom Inc.

-

Huawei Technologies Co., Ltd.

-

Nokia Corporation

-

Ericsson

-

Microsoft Corporation

-

Amazon Web Services (AWS)

-

Zscaler, Inc.

-

Forcepoint LLC

-

McAfee Corp.

-

Trend Micro Incorporated

-

VMware, Inc.

-

Radware Ltd.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 5.30 Billion |

| Market Size by 2035 | USD 11.87 Billion |

| CAGR | CAGR of 8.4% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Component (Hardware, Solutions and Services) •By Deployment Mode (Cloud-based, On-premises) •By Organization Size (Small and Medium-sized Enterprises (SMEs), Large Enterprises) •By End Use Industry (Telecom and IT, BFSI, Government, Media and Entertainment, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Cisco Systems, Inc., Juniper Networks, Inc., Palo Alto Networks, Inc., Fortinet, Inc., Check Point Software Technologies Ltd., IBM Corporation, Thales Group, Micro Focus International plc, Broadcom Inc., Huawei Technologies Co., Ltd., Nokia Corporation, Ericsson, Microsoft Corporation, Amazon Web Services (AWS), Zscaler, Inc., Forcepoint LLC, McAfee Corp., Trend Micro Incorporated, VMware, Inc., Radware Ltd. |

Frequently Asked Questions

Ans: North America dominated the Network Encryption Market in 2025.

Ans: The Solutions segment dominated the Network Encryption Market in 2025.

Ans: Rapid Expansion of Cloud Computing, Remote Work, and Digital Transformation Driving Strong Demand for Network Encryption Solutions Globally.

Ans: The Network Encryption Market was valued at USD 5.30 billion in 2025.

Ans: The Network Encryption Market is expected to grow at a CAGR of 8.4% from 2026 to 2035.

Get in Touch