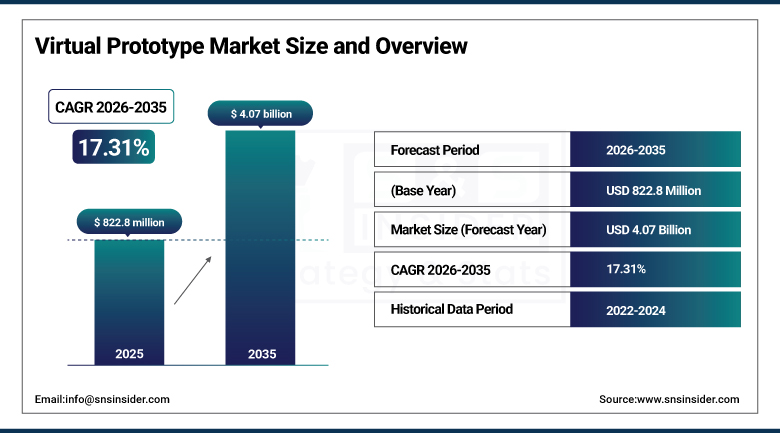

Virtual Prototype Market Report Scope & Overview:

The Virtual Prototype Market was valued at USD 822.8 Million in 2025 and is expected to reach USD 4.07 Billion by 2035, growing at a CAGR of 17.31% from 2026–2035.

The global virtual prototype market is advancing as product development organizations across automotive, aerospace, electronics, and industrial machinery increasingly replace physical prototype testing cycles with high-fidelity digital simulation environments that enable comprehensive design validation, performance analysis, and manufacturing feasibility assessment without fabricating physical parts whose iterative modification in conventional development programmes creates cost and timeline inefficiencies that virtual prototyping systematically eliminates. Virtual prototypes integrate CAD solid models with physics-based simulation engines covering structural mechanics, computational fluid dynamics, electromagnetic field analysis, and system-level behavioral modelling to create digital representations of products whose performance can be evaluated across the complete operating envelope before any physical commitment is made.

In 2024, NVIDIA expanded its Omniverse simulation platform with enhanced physics simulation capabilities for virtual prototyping. This enabling engineering teams at automotive and industrial machinery companies to evaluate product designs in photorealistic physically accurate virtual environments where sensor simulation, robotics interaction, and manufacturing process validation can occur simultaneously within a unified collaborative platform. The expansion demonstrated NVIDIA’s strategy of positioning GPU-accelerated physics simulation as the foundational infrastructure for virtual prototype workflows that integrate multiple engineering disciplines within a common digital environment.

Market Size and Forecast

-

Market Size in 2026E: USD 965.4 Million

-

Market Size by 2035: USD 4.07 Billion

-

CAGR: 17.31% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Virtual Prototype Market - Request Free Sample Report

Virtual Prototype Market Trends

-

Generative AI integration in virtual prototyping is enabling autonomous design parameter optimization that iterates thousands of design variants to identify optimal configurations faster than manual methods.

-

Cloud-based virtual prototyping SaaS platforms are democratizing high-performance simulation access for SMEs that cannot justify on-premise HPC infrastructure investment.

-

Digital twin synchronization extending virtual prototypes from design validation into manufacturing monitoring and field performance feedback creates continuous product improvement capability.

-

Multi-physics simulation integrating structural, thermal, electromagnetic, and fluid domains in unified solvers is replacing fragmented single-domain analysis workflows in complex product development.

-

Automotive EV powertrain and battery system virtual prototyping is growing as electrification complexity requires comprehensive thermal, electrical, and mechanical simulation before physical validation.

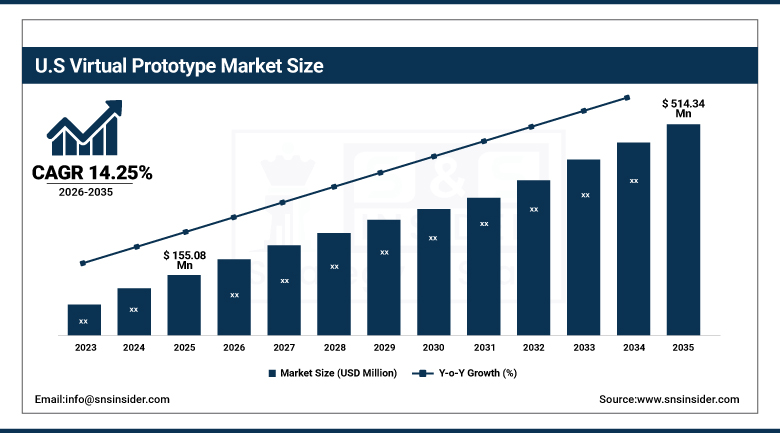

The U.S. Virtual Prototype Market Outlook

The U.S. Virtual Prototype Market was valued at approximately USD 155.08 Million in 2025 and is expected to reach approximately USD 514.34 Million by 2035, growing at a CAGR of approximately 14.25%.

North America continues to lead the Virtual Prototype Market through its strong technological infrastructure, early adoption of advanced simulation tools, and the concentration of automotive, aerospace, and electronics OEMs whose complex product development requirements create the most commercially significant virtual prototyping demand globally. Ansys, Synopsys, Cadence Design Systems, and Dassault Systèmes’ U.S. operations sustain North American simulation software market leadership whose product innovation pace defines global virtual prototyping capability standards.

In January 2024, NVIDIA launched the GeForce RTX 40 SUPER Series GPU providing substantially improved performance for AI and simulation workloads that underpin virtual prototype rendering and physics computation. This enabling engineering workstation users to run more complex multi-physics simulations at faster iteration rates than prior-generation GPU hardware could support. The launch reflected NVIDIA’s recognition that GPU-accelerated simulation has become a primary workload driving professional graphics hardware procurement above conventional visualization applications.

Virtual Prototype Market Segment Analysis

-

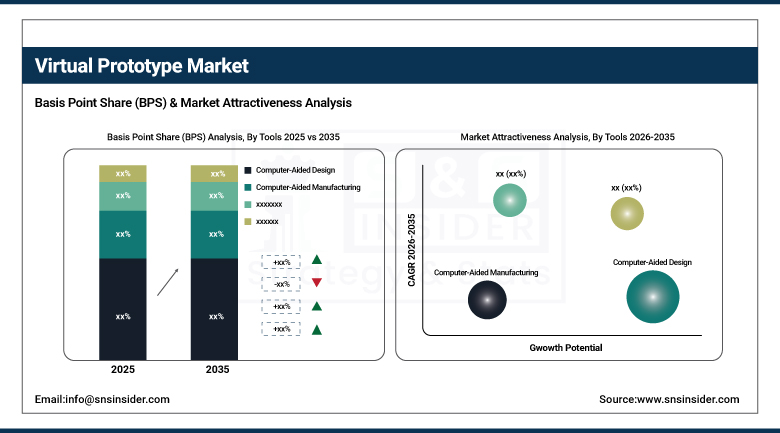

By Tools, computer-aided design segment dominated the virtual prototype market with approximately 34% share in 2025, while the computer-aided manufacturing segment is the fastest growing with a CAGR of approximately 16.08% driven by digital manufacturing process simulation adoption.

-

By Deployment, cloud-based segment dominated the virtual prototype market with approximately 66% share in 2025 and is also the fastest growing, driven by scalable HPC access without capital infrastructure investment enabling SME adoption.

-

By Industry, automotive segment dominated the virtual prototype market with the largest share in 2025 through its complex product design validation requirements, while the electronics & semiconductors segment is the fastest growing driven by chip design virtual prototyping and SoC validation demand.

By Tools, CAD dominates, CAM grows fastest

Computer-Aided Design retained the dominant tools position with approximately 34% of the virtual prototype market in 2025. CAD’s foundational role reflects its status as the upstream geometry creation environment whose 3D solid model representation of product geometry is the essential input for all downstream simulation, analysis, and manufacturing planning activities in the virtual prototyping workflow. Every virtual prototype begins with a parametric CAD model whose feature-based geometry definition enables rapid design modification for iterative simulation studies where dimensional changes propagate automatically to all dependent analyses without requiring geometry rebuilding. The extensive installed base of CAD software in engineering organizations, where Dassault Systèmes CATIA and SolidWorks, Siemens NX, PTC Creo, and Autodesk Fusion 360 collectively serve hundreds of thousands of engineering users.

Computer-Aided manufacturing is growing fastest at approximately 16.08% CAGR because the digital manufacturing trend of simulating production processes, machine tool paths, assembly sequences, and factory line configurations in virtual environments before physical line commissioning creates CAM software investment that progressively becomes standard practice in advanced manufacturing companies whose cost of physical line errors substantially exceeds virtual simulation investment. Each automotive assembly plant, electronics factory, and aerospace manufacturing facility that deploys CAM virtual commissioning reduces line installation time, eliminates collision risk from invalidated robot programmes, and enables worker training on virtual line models before physical equipment installation.

By Industry, automotive dominates, electronics grows fastest

Automotive retained the dominant industry position with the largest share of the virtual prototype market in 2025. The automotive industry’s product complexity, regulatory safety validation requirements, competitive development timeline pressure, and the electrification transition’s battery system, power electronics, and software-defined vehicle architecture complexity collectively create the most commercially significant virtual prototyping investment of any single industry sector. Each new vehicle programme whose typical 3 to 4 year development cycle encompasses thousands of virtual prototype simulations covering crashworthiness, NVH, aerodynamics, thermal management, and electromagnetic compatibility creates sustained CAE software procurement and cloud HPC subscription investment across automotive OEMs and their tier-1 supplier networks.

Electronics and semiconductors is growing fastest because the semiconductor SoC design verification challenge, where a modern chip design contains billions of transistors whose interaction under all operating conditions must be validated before tape-out at USD 10 million to USD 100 million mask set cost, creates the most financially compelling virtual prototyping investment case of any engineering application. Electronic Design Automation’s virtual prototype capability enabling full-chip software execution on virtual hardware models before silicon fabrication is available for testing creates a simulation investment whose financial return through avoided re-spin cost creates measurable ROI documentation that sustains above-market EDA virtual prototype procurement growth.

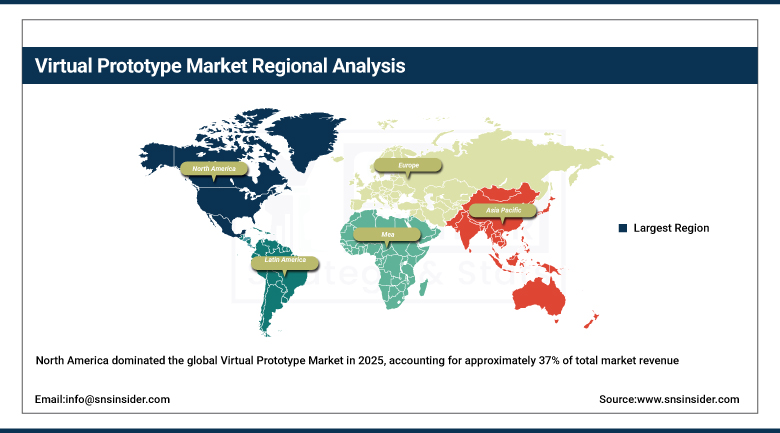

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

24.6% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Israel |

22.8% |

|

Latin America |

Brazil |

43.8% |

North America Virtual Prototype Market Insights

North America dominated the global Virtual Prototype Market in 2025, accounting for approximately 37% of total market revenue. Through its early adoption of advanced simulation technology, the concentration of aerospace and defence OEMs whose performance validation requirements drove simulation software to its performance frontier, and the commercial leadership of Ansys, Synopsys, Cadence, and Dassault Systèmes whose North American development centres define global virtual prototyping capability. The United States accounts for approximately 82.5% of North American revenues through Boeing, Lockheed Martin, and GM’s virtual prototype investment programmes.

Canada contributes supplementary North American revenues through its aerospace manufacturing sector’s simulation investment at Bombardier and Pratt & Whitney Canada, the automotive parts industry’s growing virtual prototyping adoption in Ontario manufacturing clusters, and the growing technology sector’s consumer electronics and robotics virtual prototype development programmes whose simulation software procurement creates above-baseline Canadian market growth.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Virtual Prototype Market Insights

Europe is a technically sophisticated virtual prototype market where the automotive industry’s world-leading product development investment, aerospace’s Airbus and Rolls-Royce simulation programmes, and the advanced industrial machinery sector’s digital twin adoption collectively create consistent and high-value virtual prototyping demand. Germany accounts for approximately 24.6% of European revenues through Volkswagen, BMW, Daimler, and Porsche’s extensive CAE simulation programmes, the Fraunhofer Institute’s applied simulation research, and Siemens Digital Industries Software’s European headquarters sustaining regional simulation platform development.

France’s Airbus and Safran aerospace virtual prototype investment, the United Kingdom’s Rolls-Royce engine simulation programmes, and Sweden’s Volvo and Scania commercial vehicle virtual development collectively sustain European virtual prototype market development. The EU’s Horizon Europe research programme’s virtual testing and digital twin investment creates academic and industrial co-funded simulation capability development that progressively creates commercial adoption momentum.

Asia Pacific Virtual Prototype Market Insights

Asia Pacific is the fastest-growing regional virtual prototype market, driven by the rapidly expanding automotive, electronics, and semiconductor industries’ adoption of simulation-driven development methodologies to compete with established Western OEMs’ development efficiency. China accounts for approximately 44.8% of Asia Pacific revenues through its world’s largest automotive market’s domestic OEM virtual prototype investment, the semiconductor chip design industry’s EDA virtual prototype adoption, and domestic simulation software development companies progressively challenging Western platform incumbents in specific application domains.

Japan’s Toyota, Honda, and Sony’s world-leading simulation programme maturity, South Korea’s Samsung and Hyundai’s virtual prototype investment, and Taiwan’s TSMC and MediaTek’s EDA virtual prototype adoption collectively create premium Asia Pacific market demand whose technical sophistication approaches North American and European standards. India’s growing automotive and aerospace engineering services sector’s simulation software adoption and domestic OEM development programme investment create above-regional-average growth momentum.

MEA & Latin America Virtual Prototype Market Insights

Israel leads MEA revenues through its world-class high-technology industry’s semiconductor and system design virtual prototype adoption, the defense electronics sector’s simulation investment at Elbit Systems and Rafael Advanced Defense Systems, and the growing medical device and autonomous vehicle technology sectors’ virtual prototype investment. The UAE’s aviation and advanced manufacturing sectors contribute growing regional demand.

Brazil leads Latin American revenues at approximately 43.8% through its automotive manufacturing sector’s growing virtual prototype adoption at Fiat Chrysler Brazil and Volkswagen do Brasil, the aerospace sector’s Embraer virtual prototype programme whose global aircraft development standards require comprehensive simulation investment, and the growing Brazilian engineering software development and simulation services sector.

Market Dynamics

Growth Drivers: Accelerating product development cycle pressure and EV powertrain complexity creating non-discretionary virtual prototype investment across automotive and electronics industries

The virtual prototype market’s growth is powered by the structural alignment between competitive product development cycle compression requirements and the rising product complexity that makes physical prototype testing economically and temporally infeasible as the primary validation method. Each year of reduction in automotive programme development time from the historical 4 to 5 years toward the current competitive benchmark of 2.5 to 3 years requires proportional expansion of virtual prototype validation scope to replace physical testing that no longer fits within the compressed timeline. The electric vehicle transition’s introduction of battery system, power electronics, thermal management, and software-defined vehicle complexity substantially above equivalent ICE vehicle design creates a virtual prototype investment mandate whose commercial scale is progressive as electrification penetrates from premium to mass-market vehicle categories.

Restraints: High software license cost and simulation expertise scarcity limiting adoption among smaller engineering organizations and in resource-constrained markets

Premium virtual prototype software platforms including Ansys Mechanical, Dassault CATIA, and Synopsys Virtualizer each carry annual licence costs of USD 20,000 to USD 200,000 per seat that create adoption barriers for engineering organizations whose project scale, software utilization frequency, and budget constraints make per-seat licence economics unfavorable relative to outsourcing simulation to service bureaus or continuing physical prototype validation. Simulation expertise scarcity, where the combination of deep physics domain knowledge, software operational proficiency, and engineering design context understanding that skilled simulation engineers require takes years of specialized education and project experience to develop, creates a talent gap whose manifestation as extended time-to-results and suboptimal simulation setup quality reduces the ROI that organizations without established simulation competencies achieve from software investment.

Opportunities: AI-powered automated simulation setup and cloud HPC democratization enabling non-specialist virtual prototype access creating market expansion beyond CAE expert user populations

AI-powered simulation automation that intelligently meshes CAD geometry, selects appropriate physics solver settings, assigns material properties from component databases, and interprets results against design criteria without requiring expert engineer configuration represents the most commercially transformative capability development in virtual prototyping history. Each simulation software platform that successfully deploys AI-automated setup reduces the specialist expertise barrier that has historically confined virtual prototype adoption to engineering organizations with dedicated CAE teams, enabling design engineers without simulation specialist training to run meaningful virtual prototype validations as an integrated part of their design workflow. Cloud HPC’s transformation of simulation economics from capital infrastructure investment toward per-job compute consumption enables SMEs and engineering service companies without on-premise cluster infrastructure to access simulation capacity.

Recent Developments:

-

2024: NVIDIA expanded its Omniverse platform with enhanced physics simulation for virtual prototyping, enabling engineering teams to validate product designs in photorealistic physically accurate virtual environments covering sensor simulation, robotics interaction, and manufacturing process validation within a unified collaborative platform.

-

2024: Ansys launched its SimAI artificial intelligence platform providing AI-powered simulation result prediction that reduces solver runtime from hours to seconds for trained model inference, enabling rapid design space exploration across thousands of design variants at a fraction of the conventional simulation compute cost.

-

2023: Siemens Digital Industries Software launched Simcenter X, a cloud-native simulation and test platform providing browser-accessible structural, thermal, and fluid simulation for engineering teams without on-premise HPC infrastructure, extending virtual prototyping access to SME engineering organisations through per-project cloud compute subscription.

Virtual Prototype Market Key Players are:

-

Synopsys Inc.

-

Cadence Design Systems Inc.

-

Dassault Systèmes SE

-

Ansys Inc.

-

Altair Engineering Inc.

-

Autodesk Inc.

-

Siemens Digital Industries Software (Siemens AG)

-

PTC Inc.

-

MathWorks Inc.

-

COMSOL Inc.

-

ESI Group SA

-

National Instruments Corp. (NI/Emerson)

-

Arm Limited (SoftBank Group)

-

Imperas Software Ltd.

-

Magillem SA

-

Carbon Design Systems Inc.

-

Agilent Technologies Inc. (Keysight Technologies)

-

NVIDIA Corporation

-

Hexagon AB (MSC Software)

-

Mentor Graphics Corp. (Siemens)

Virtual Prototype Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 822.8 Million |

| Market Size by 2035 | USD 4.07 Billion |

| CAGR | CAGR of 17.31% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Tools (Computer-Aided Design, Computer-Aided Manufacturing, Computer-Aided Engineering, Electronic Design Automation, Others) • By Deployment (Cloud-Based, On-Premise) • By Industry (Automotive, Aerospace & Defense, Electronics & Semiconductors, Industrial Machinery, Consumer Goods, Healthcare & Medical Devices, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Synopsys Inc., Cadence Design Systems Inc., Dassault Systèmes SE, Ansys Inc., Altair Engineering Inc., Autodesk Inc., Siemens Digital Industries Software (Siemens AG), PTC Inc., MathWorks Inc., COMSOL Inc., ESI Group SA, National Instruments Corp. (NI/Emerson), Arm Limited (SoftBank Group), Imperas Software Ltd., Magillem SA, Carbon Design Systems Inc., Agilent Technologies Inc. (Keysight Technologies), NVIDIA Corporation, Hexagon AB (MSC Software), and Mentor Graphics Corp. (Siemens) |

Frequently Asked Questions

The Virtual Prototype Market is expected to grow at a CAGR of 17.31% from 2026 to 2035.

The Virtual Prototype Market was valued at USD 822.8 Million in 2025.

Competitive product development cycle compression requiring virtual replacement of physical testing, EV powertrain complexity mandating comprehensive simulation before physical validation are the primary growth factors.

The computer-aided design segment dominated the Virtual Prototype Market with approximately 34% share in 2023, while the Computer-Aided Manufacturing segment is the fastest growing at approximately 16.08% CAGR.

North America dominated the Virtual Prototype Market in 2025.

Get in Touch