Nutraceuticals Market Report Scope & Overview:

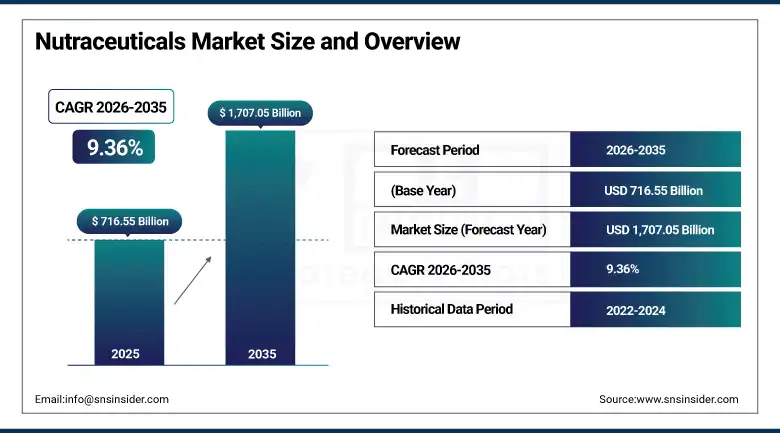

The Nutraceuticals Market was valued at USD 716.55 Billion in 2025 and is expected to reach USD 1,707.05 Billion by 2035, growing at a CAGR of 9.36% from 2026–2035.

The global nutraceuticals market is experiencing exceptional growth, driven by rising health consciousness, increasing chronic disease prevalence, growing consumer interest in preventive healthcare, and expanding scientific evidence supporting nutraceutical efficacy. Nutraceuticals are food-derived products providing health benefits beyond basic nutrition, encompassing dietary supplements, functional foods, and functional beverages that deliver vitamins, minerals, probiotics, omega-3 fatty acids, botanical extracts, and bioactive compounds targeting specific health outcomes. The market is propelled by consumer shifts toward self-managed health maintenance, the food-as-medicine movement whose dietary intervention evidence base is expanding, and the supplement industry’s e-commerce distribution channel growth that creates unprecedented product accessibility across geographies previously underserved by brick-and-mortar health retail infrastructure.

In 2024, Nestlé Health Science expanded its nutraceutical portfolio through acquisition of Orgain, a leading organic protein supplement and functional nutrition brand, strengthening its position in the premium plant-based protein supplement segment. The acquisition reflects the commercial momentum of the premium nutraceutical category whose clean-label, plant-based, and organic positioning creates above-commodity pricing that sustains premium brand equity investment in an increasingly competitive dietary supplement market.

Market Size and Forecast

-

Market Size in 2026E: USD 783.63 Billion

-

Market Size by 2035: USD 1,707.05 Billion

-

CAGR: 9.36% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Nutraceuticals Market - Request Free Sample Report

Nutraceuticals Market Trends

-

Personalized nutrition is growing through genetic testing and biomarker analysis, enabling customized supplement formulations with premium pricing models.

-

Probiotic and gut microbiome products are expanding rapidly due to clinical evidence supporting immunity, metabolism, and mental health benefits.

-

Sports nutrition demand is increasing beyond athletes, driven by mainstream fitness participation and rising protein and recovery supplement consumption.

-

Plant-based nutraceuticals are gaining traction as consumers shift toward vegan, clean-label, and environmentally sustainable supplement formulations.

-

Functional beverages are emerging strongly in energy, cognition, sleep, and immunity segments due to convenience-driven consumption demand.

The U.S. Nutraceuticals Market Outlook

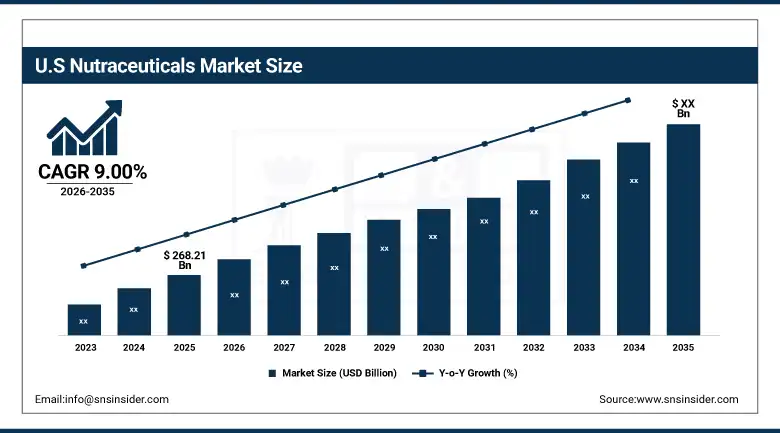

The U.S. nutraceuticals market is the world’s most commercially sophisticated nutraceutical market, valued at approximately USD 268.21 Billion in 2025 and expected to grow at a CAGR of approximately 9.00% through 2035.

Abbott Nutrition, Amway, Herbalife, Nature’s Sunshine Products, Nestlé Health Science, and Glanbia collectively define the domestic commercial landscape. The FDA’s Dietary Supplement Health and Education Act framework creates a commercially accessible regulatory environment whose structure-function claim provisions enable product marketing without the pre-market approval investment that pharmaceutical development requires, sustaining the market’s extraordinary new product introduction velocity.

In 2023, Abbott Laboratories expanded its Ensure Plus Advance nutritional supplement line with new high-protein formulations targeting elderly sarcopenia prevention and rehabilitation nutrition markets whose ageing population demographic growth creates above-average institutional procurement from hospital nutrition departments and geriatric care facilities. The expansion demonstrates the commercial opportunity in clinical nutrition adjacent supplement categories whose healthcare institution procurement creates structured demand channels complementing consumer retail sales.

Nutraceuticals Market Segment Analysis

-

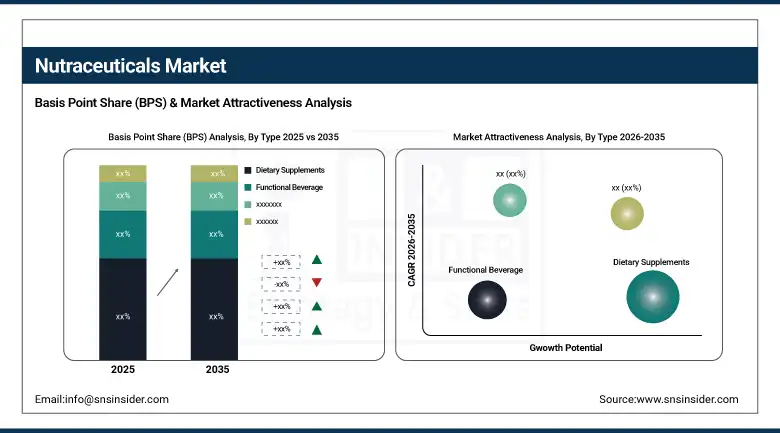

By Type, the Dietary Supplements segment dominated the Nutraceuticals Market with approximately 46% share in 2025, while the Functional Beverages segment is the fastest growing.

-

By Form, the Capsules & Tablets segment dominated the Nutraceuticals Market with approximately 44% share in 2025, while the Liquid segment is the fastest growing.

-

By Sales Channel, the Hypermarkets/Supermarkets segment dominated the Nutraceuticals Market with approximately 38% share in 2025, while the Online Channels segment is the fastest growing.

-

By End Use, the fitness and wellness segment dominated the market with approximately 41% share in 2025, while the medical sector is the fastest growing.

By Type, dietary supplements dominate, functional beverages grow fastest

Dietary supplements retained the dominant type position with approximately 46% of the market in 2025. The dietary supplement category’s commercial primacy reflects its broad product spectrum encompassing vitamin and mineral supplements, omega-3 fatty acid softgels, probiotic capsules, herbal and botanical extracts, protein powders, and specialty health supplements whose combined procurement creates the largest aggregate nutraceutical type revenue. The consumer’s established familiarity with supplementation behavior, pharmacy and retail channel accessibility, and the category’s extraordinary product innovation velocity collectively sustain dietary supplements’ dominant commercial position.

Functional beverages are the fastest-growing type because the beverage format’s consumption occasion accessibility, flavor enjoyment advantage over capsule alternatives, and premiumization opportunity in the functional ingredient delivery channel create above-average market expansion. Each new functional beverage launch that delivers adaptogens, nootropics, probiotics, or collagen in a palatable and convenient format creates consumer adoption beyond the traditional supplement consumer demographic whose capsule compliance limitation creates market barrier. The RTD protein shake, prebiotic soda, and adaptogenic tea categories collectively demonstrate the extraordinary innovation velocity that sustains functional beverage’s fastest-growing type status.

By Sales Channel, hypermarkets dominate, online grows fastest

Hypermarkets and supermarkets retained the dominant sales channel position with approximately 38% of the market in 2025. The grocery and mass retail channel’s positioning of private label and national brand nutraceuticals in dedicated supplement aisles creates high-impulse visibility procurement that supplements specialty store and pharmacy channel purchasing. Each major grocery chain’s private label supplement programme creates competitive pricing that captures value-segment consumers whose price sensitivity favors above-commodity quality at below-specialty store pricing.

Online channels are the fastest-growing sales channel because direct-to-consumer e-commerce’s subscription model creates above-average consumer lifetime value through automatic replenishment that removes re-purchase friction. Amazon’s supplement marketplace, brand direct websites, and subscription wellness platforms collectively create digital procurement channels whose growth compounds with e-commerce adoption and health-conscious consumer segment’s digital engagement. The digital channel’s product discovery, consumer review accessibility, and clinical evidence communication capability create conversion advantages for premium nutraceutical brands whose evidence-based positioning requires consumer education beyond what retail shelf space can efficiently deliver.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Nutraceuticals Market Insights

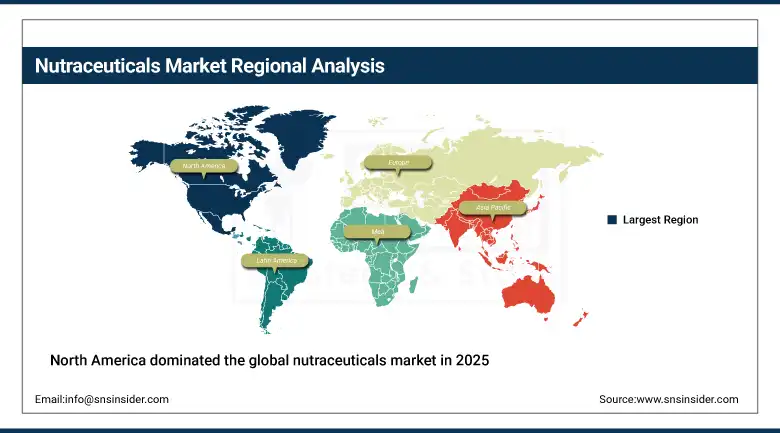

North America dominated the global nutraceuticals market in 2025, driven by highest per-capita nutraceutical expenditure, well-established consumer supplement culture, and the commercial presence of Abbott, Amway, Herbalife, Nestlé Health Science, and Glanbia. The United States accounts for approximately 87.4% of North American revenues through its mature supplement market, above-average consumer health investment, and direct-selling and e-commerce channel sophistication.

Canada contributes approximately 12.6% of North American revenues through its Natural Health Products directorate-regulated supplement market, growing plant-based supplement preference, and health-conscious consumer demographic.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Nutraceuticals Market Insights

Europe is a technically sophisticated market where EU health claim regulation, EFSA scientific opinion requirements, and the premium health food retail environment create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through its pharmacy channel supplement dominance, the health-conscious consumer demographic, and DSM-Firmenich and BASF’s nutritional ingredient manufacturing.

The United Kingdom, France, and the Netherlands are significant secondary markets where health retailer Holland & Barrett’s network, France’s pharmacy supplement channel, and the Netherlands’ DSM nutritional ingredient manufacturing create consistent commercial demand.

Asia Pacific Nutraceuticals Market Insights

Asia Pacific is the fastest-growing regional nutraceuticals market, driven by China’s extraordinary supplement market growth, Japan’s Foods for Specified Health Uses regulatory framework, India’s Ayurveda-integrated supplement market, and Southeast Asia’s growing health consciousness. China accounts for approximately 44.8% of Asia Pacific revenues through its domestic supplement market’s extraordinary expansion, the traditional Chinese medicine ingredient integration with modern supplement formats, and the e-commerce channel’s supplement distribution penetration.

India represents the most commercially dynamic emerging market within Asia Pacific where Dabur, Himalaya Drug Company, and the Ayurvedic supplement tradition create a large domestic market whose modern supplement format adoption creates above-average growth that compounds with India’s growing middle class health investment.

MEA & Latin America Nutraceuticals Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through its health-conscious Muslim consumer demographic’s halal supplement specification, the growing private healthcare sector’s clinical nutrition procurement investment, and Vision 2030’s preventive health programme creating supplement awareness.

Brazil leads Latin American revenues at approximately 44.2% through its large dietary supplement retail market, the pharmacy channel’s established supplement procurement dominance, and the fitness culture’s protein and sports nutrition demand. UAE’s premium wellness consumers and South Africa’s growing health supplement market collectively sustain regional development through 2035.

Market Dynamics

Growth Drivers: Health consciousness and preventive healthcare adoption creating systematic nutraceutical procurement

Rising global health consciousness accelerated by COVID-19 pandemic awareness is the market’s most commercially durable structural growth driver. The pandemic’s demonstration of immune vulnerability creating lasting consumer motivation for immune support supplementation, combined with chronic disease management’s growing acceptance of dietary intervention as a complementary treatment approach, creates structural demand growth whose demographic momentum compounds with ageing population growth and emerging market middle class expansion. Each consumer who initiates a nutraceutical supplementation routine creates a recurring procurement relationship whose annual repurchase creates above-transactional commercial value for brand investment.

Preventive healthcare adoption’s systematic shift from reactive illness treatment toward proactive wellness maintenance creates the foundational commercial motivation for nutraceutical investment that sustains market growth independent of economic cycles. Each consumer wellness programme, corporate employee health initiative, and government preventive health campaign that incorporates nutraceutical supplementation creates commercial procurement whose structural motivation is independent of acute health event triggers.

Restraints: Regulatory fragmentation and efficacy claim substantiation requirements

Regulatory fragmentation across global markets creates product reformulation, labelling adaptation, and claim substantiation investment whose compliance cost moderates the pace of international market expansion for nutraceutical brands. Each major market’s different health claim substantiation standard, ingredient permitted list, and labelling requirement creates regulatory compliance investment that sustains market entry barriers for smaller brand operators.

Scientific efficacy claim substantiation requirements whose randomized controlled trial evidence standard creates above-commodity clinical investment for novel health claims moderates the introduction pace of new nutraceutical categories whose evidence base requires investment ahead of commercial launch.

Opportunities: Personalized nutrition and probiotic microbiome innovation

Personalized nutrition represents the most commercially premium near-term opportunity whose genetic testing, microbiome assessment, and biomarker profiling create individualized supplement formulation services commanding premium pricing above commodity supplement alternatives. Each personalized nutrition platform that converts biomarker testing into targeted supplement recommendation creates recurring subscription revenue whose customer retention economics sustain investment in the testing and formulation technology.

Probiotic and microbiome innovation represents the most commercially dynamic ingredient category whose clinical evidence expansion across immunity, mental health, metabolic syndrome, and skin health creates new commercial application breadth that compounds with each published clinical trial demonstrating microbiome intervention efficacy.

Recent Developments:

-

2026: Nestle Health Science is reshaping the global nutraceutical landscape, with the company strengthening premium science-backed supplement lines while divesting lower-growth mass-market vitamin assets to focus on high-evidence wellness products.

-

2026: DSM-Firmenich AG is accelerating development of bioactive compounds, probiotics, and personalized nutrition solutions aligned with microbiome and metabolic health applications in clinical-grade nutraceutical formulations.

-

2026: Abbott Laboratories is expanding clinical nutrition portfolios, particularly in diabetes management, sarcopenia prevention, and age-related muscle health support products.

Nutraceuticals Market key players are:

-

Nestle Health Science SA

-

Abbott Laboratories

-

Amway Corporation

-

Herbalife Nutrition Ltd.

-

Glanbia plc

-

DSM-Firmenich AG

-

Archer Daniels Midland Company (ADM)

-

DuPont de Nemours Inc.

-

Nu Skin Enterprises Inc.

-

Nature’s Sunshine Products Inc.

-

NBTY Inc. (The Nature’s Bounty Co.)

-

Bayer AG (One A Day/Berocca)

-

Haleon plc

-

Reckitt Benckiser Group plc

-

Danone SA

-

Unilever plc

-

Kerry Group plc

-

GNC Holdings LLC

-

Swisse Wellness Pty Ltd.

-

Blackmores Ltd.

Nutraceuticals Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 716.55 Billion |

| Market Size by 2035 | USD 1,707.05 Billion |

| CAGR | CAGR of 9.36% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Functional Beverage, Functional Food, Dietary Supplements) • By Form (Capsules & Tablets, Liquid, Powder, Others) • By Sales Channel (Hypermarkets/Supermarkets, Specialty Stores, Pharmacies, Online Channels) • By End Use (Fitness and Wellness, Medical, Food and Beverage, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Nestle Health Science SA, Abbott Laboratories, Amway Corporation, Herbalife Nutrition Ltd., Glanbia plc, DSM-Firmenich AG, Archer Daniels Midland Company (ADM), DuPont de Nemours Inc., Nu Skin Enterprises Inc., Nature’s Sunshine Products Inc., NBTY Inc. (The Nature’s Bounty Co.), Bayer AG (One A Day/Berocca), Haleon plc, Reckitt Benckiser Group plc, Danone SA, Unilever plc, Kerry Group plc, GNC Holdings LLC, Swisse Wellness Pty Ltd., Blackmores Ltd. |

Frequently Asked Questions

The Nutraceuticals Market is expected to grow at a CAGR of 9.36% from 2026 to 2035.

The Nutraceuticals Market was valued at USD 716.55 Billion in 2025.

Rising global health consciousness and preventive healthcare adoption creating systematic supplement procurement.

Dietary Supplements dominated the Nutraceuticals Market with approximately 46% share in 2025.

North America dominated the Nutraceuticals Market in 2025.

Get in Touch