Offshore Helicopter Services Market Report Scope & Overview:

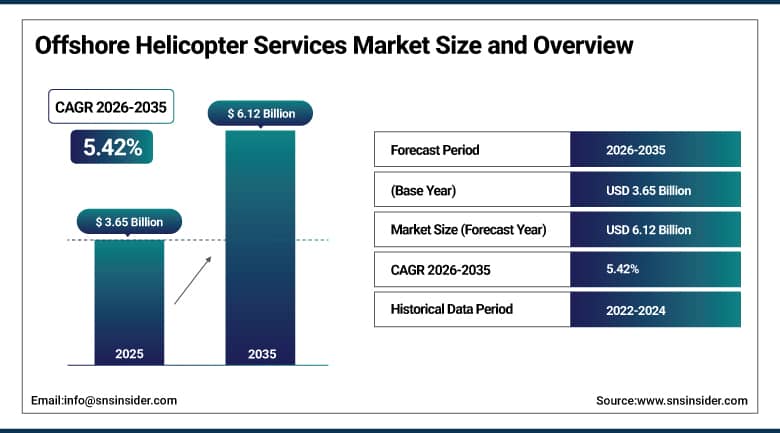

The Offshore Helicopter Services Market was valued at USD 3.65 billion in 2025 and is expected to reach USD 6.12 billion by 2035, growing at a CAGR of 5.42% from 2026–2035.

Offshore Helicopter Services Market is experiencing high growth on a global basis because of an increase in the need for regulatory compliance and privacy management systems. Enterprises are now increasingly implementing tools related to data discovery, data classification, consent management, and risk monitoring solutions. The growth in the market is being driven by AI based privacy management automation and cloud-based cybersecurity management system. The offshore helicopter services market is being fueled by the growing implementation of enterprise-wide governance solutions as well as cybersecurity solutions. Sectors including BFSI, healthcare, retail, IT, and government sectors are increasingly implementing privacy management solutions. Growing concern for data security and digital trust management solutions is driving market growth.

Bristow Group Inc., which is among the leading offshore helicopter transport operators globally, reported a revenue of about USD 1.47 Billion in its fiscal year 2024 due to the continued demand by major producers for crew change flights to their platforms in locations such as the Gulf of Mexico, North Sea, Brazil, and West Africa. The services provided by Bristow include flight operations using medium-sized helicopters, such as the Sikorsky S-92, and heavy helicopters, such as the Leonardo AW189, within the framework of long-term service contracts with producers including BP, Shell, Equinor, and TotalEnergies.

Market Size and Forecast

-

Market Size 2026E: USD 3.81 Billion

-

Market Size 2035: USD 6.12 Billion

-

CAGR (2026 - 2035): 5.42%

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Offshore Helicopter Services Market - Request Free Sample Report

Offshore Helicopter Services Market Trends

-

The increasing number of offshore wind farm facilities will increase structural demand for helicopter-based O&M services.

-

The growing use of modern technology and health usage and monitoring system implementation will improve fleet reliability and decrease O&M time.

-

The increasing use of EMS contracts in the offshore environment will allow companies to diversify service types and increase their revenues.

-

The increase in regulations that require ensuring offshore workers’ safety and provide emergency evacuation options will help maintain minimum levels of service across all basins.

-

Digital mission management and the integration of real-time weather monitoring will minimize risks during operation through optimized dispatch.

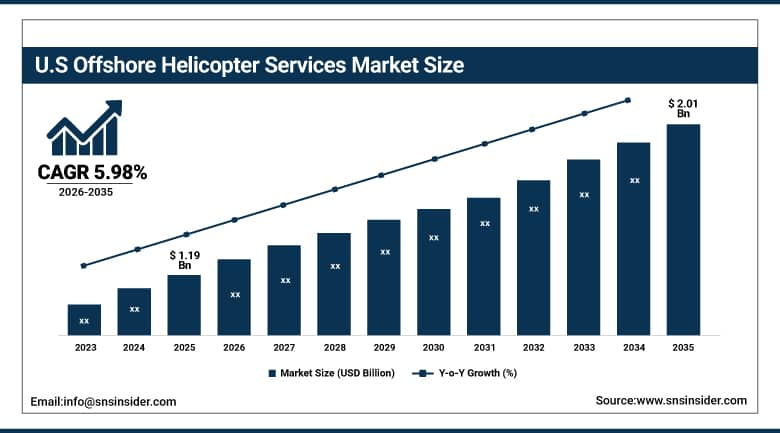

U.S. Offshore Helicopter Services Market Size Outlook.

The U.S. Offshore Helicopter Services Market was valued at USD 1.19 billion in 2025 and is expected to reach around USD 2.01 billion by 2035, growing at a CAGR of 5.98% from 2026–2035.

The expansion of the U.S. Offshore Helicopter Services Market has been fueled by increasing offshore exploration for oil and natural gas, especially deepwater exploration in the Gulf of Mexico, and an increase in offshore wind power installations. The growing need for safer and faster transportation of crews, old fleet replacement, and increasing offshore safety standards have also added to market growth.

Era Group Inc., the strategic acquisitions and training of crews for the Sikorsky S-92 helicopter at Era puts the company in a position to generate more revenue from the mature oil and gas crew transportation market as well as the new offshore wind market along the Atlantic coast.

Offshore Helicopter Services Market Segment Analysis

-

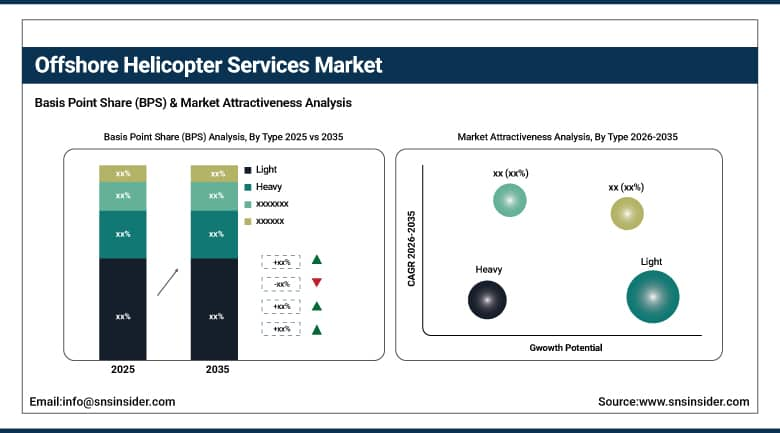

By Type, the Light helicopter segment dominated the offshore helicopter services market with 42.74% share in 2025, while the heavy helicopter segment represents the fastest growing type with CAGR of 6.54 through 2026 to 2035.

-

By Application, the crew transport segment dominated the offshore helicopter services market with 28.61% share in 2025, while the inspection segment is the fastest growing application with CAGR of 6.44% during 2026 to 2035.

-

By End User, the oil & gas industry segment dominated the offshore helicopter services market with 30.59% share in 2025, while the offshore wind industry segment is the fastest growing end user with CAGR of 6.53% during 2026 to 2035.

-

By Service Type, the scheduled services segment dominated the offshore helicopter services market with 38.45% share in 2025, while emergency medical services are the fastest growing service type with CAGR of 6.44% during 2026 to 2035.

By Type, Light helicopters segment dominate, heavy helicopters segment grows fastest

The light helicopter category remained the largest contributor to the offshore helicopter services market, contributing around 42.74% share of market revenue in 2025. The light helicopter category covers one of the widest ranges of usage within the scope of the offshore services market as these helicopter types find use in transporting passengers for near-shore platforms, surveys and inspections, personnel retrieval, and coastal search & rescue. The diversity of models available from manufacturers such as Airbus with its H145, Leonardo with its AW109, and Bell with its 407 contributes to this segment’s wide revenue range.

Among all helicopter categories considered in this report, heavy helicopters represent the fastest-growing type category driven by the increasing activities for ultra-deepwater exploration in regions such as the Gulf of Mexico, West Africa, and Brazil pre-salt basins, which require long-distance flights to transport workers to offshore platforms that can be positioned up to 200 NM offshore.

By Application, crew transport segment dominates, inspection segment grows fastest

The crew transport application segment generated 28.61% of offshore helicopter services application revenue in 2025. The absolute need to rotate offshore personnel between production platforms, drilling rigs, and construction vessels following crew change cycles makes crew transport the most lucrative and contractually robust application segment in the offshore helicopter services market space. Crew transport contracts generally come with minimum hours of flying commitment as well as aircraft availability commitments, allowing offshore helicopter operators to have very good revenue visibility.

The fastest-growing application in the market is inspection services due to the continuous growth of offshore wind farm structures, which require periodic turbine and foundation inspection, aging oil and gas structures that need intense structural integrity assessments, and helicopter laser scanning technologies that enable complete asset assessment and eliminate the need for marine vessel deployment for underwater and above-water infrastructure inspection.

By End User, oil & gas industry segment dominates, offshore wind industry segment grows fastest

Oil & Gas Industry held a share of 30.59% of the offshore helicopter services end-user revenue in 2025. The oil and gas industry's structural need for helicopter services, from crew rotations through logistics, medevac, and asset inspections, ensures that it is the bedrock of demand for offshore helicopter services around the world. Leading producers like BP, Shell, Equinor, TotalEnergies, and Chevron have contracted service providers for their assets, providing a revenue base for the operators' future investment.

Offshore wind is the fastest-growing end user for helicopter services because the accelerated programme of global offshore wind energy generation creates structurally new and growing demand for helicopter-based maintenance visits, personnel transport, and construction and logistical assistance. By 2050, the International Energy Agency projects that there will be 2,000 GW of installed offshore wind capacity, meaning that thousands of turbines will be installed per year for several decades, and each turbine will require numerous helicopter services over a 25 to 30-year lifespan.

By Service Type, scheduled services segment dominate, emergency medical services segment grows fastest

Scheduled services made up 38.45% of offshore helicopter services revenue in 2025. The scheduled crew change rotation strategy, wherein helicopters operated by companies perform crew change missions on set routes between onshore bases and offshore locations in a regular fashion in line with producer manning schedules, is by far the most capital-efficient service delivery mode for offshore helicopter services operations. Contractual predictability of revenue generated through scheduled operations drives the decision-making of major operators to invest in new aircraft and expand capacity.

Emergency medical services constitute the segment growing fastest among offshore helicopter services, as offshore helicopter operations have been steadily venturing into basins further removed from mainland facilities while stricter worker safety legislation has been introduced for these workers, creating demand for dedicated offshore EMS helicopter services capable of performing medical evacuations as well as in-flight critical care treatment.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025(%) |

|---|---|---|

|

North America |

United States |

82.41% |

|

Europe |

Germany |

36.74% |

|

Asia Pacific |

China |

41.82% |

|

Middle East & Africa |

UAE |

11.30% |

|

Latin America |

Brazil |

8.97% |

North America Offshore Helicopter Services Market Insights

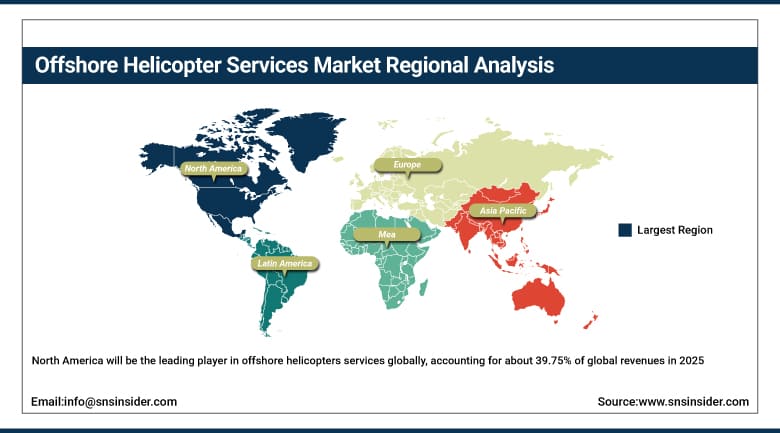

North America will be the leading player in offshore helicopters services globally, accounting for about 39.75% of global revenues in 2025. The United States will account for about 82.41% of North American revenue. The leadership of the North America region in offshore helicopters market is attributed to its exceptional operational capacity, due to the presence of the Gulf of Mexico oil and gas basin, which boasts the densest offshore helicopter facility infrastructure in the world as well as daily flights between onshore bases like Houma, Lafayette, and New Orleans and about 1,800 oil platforms in the region.

In addition, the Bureau of Safety and Environmental Enforcement (BSEE), US has strengthened offshore aviation safety through updated helideck operational standards, emergency response training frameworks, and aviation fuel handling guidelines across 2,000+ offshore facilities, supporting improved compliance rates estimated at 90%+ across regulated offshore installations in 2025, thereby reducing aviation-related offshore incident risks and improving mission reliability.

Furthermore, recent US legislative actions mandating broader adoption of ADS-B surveillance technology across military and civilian aircraft by 2031, combined with FAA modernization programs for offshore and low-altitude operations, are expected to improve offshore helicopter situational awareness and operational safety coverage by 15%–20% over the next decade.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Offshore Helicopter Services Market Insights

Europe offshore helicopter services revenues represented about 25.64% of worldwide revenues in 2025. Europe is considered to be the market characterized by the North Sea region which consists of the UK Continental Shelf, Norwegian Continental Shelf, Denmark, Holland, and Germany offshore regions where the oil and gas activities ensure the highest development of the offshore helicopter services business globally except for the Gulf of Mexico. Norway and the United Kingdom represent the main offshore helicopter flight time users in Europe due to high level platform/FPSO facilities operations requiring daily personnel transportation from Aberdeen, Stavanger, Bergen, and Esbjerg airports.

Strengthening offshore aviation safety regulations under the European Union Aviation Safety Agency (EASA), including compliance with CAP 437 helideck design and operational standards across North Sea offshore platforms, has improved offshore helicopter landing safety compliance to an estimated 92%–96% across regulated installations, while reducing helideck-related operational incidents by approximately 15%.

In addition, the expansion of North Sea offshore wind energy zones under EU Green Deal initiatives and national energy transition programs in the UK, Germany, and the Netherlands, covering more than 30 GW+ of installed and under-construction offshore wind capacity, is driving a sharp increase in crew transfer helicopter operations, contributing to an estimated 11.80% rise in offshore flight activity in wind-focused corridors.

Asia Pacific Offshore Helicopter Services Market Insights

The Asia Pacific is the fastest-growing regional market for offshore helicopter services, recording an approximate CAGR of 6.41% until 2035. Asia Pacific's offshore helicopter revenues include contributions from the country of Australia, owing to the presence of offshore oil and gas production operations in the North West Shelf and Browse Basin regions in the country, requiring long-range missions using heavy helicopters to transport personnel to remote offshore FPSOs and installations. The offshore helicopter market in Asia Pacific is also boosted by the offshore developments in countries such as Malaysia, Indonesia, Vietnam, and Thailand, where there are active offshore operations conducted by national oil companies and foreign oil & gas companies, requiring frequent use of helicopters to transport offshore personnel.

In China, accelerated offshore oil & gas exploration in the South China Sea combined with national civil aviation authority upgrades in offshore flight monitoring and low-altitude airspace reforms is driving a 16.41% increase in offshore helicopter flight activity, supported by improved navigation systems and expanding offshore infrastructure networks.

MEA & Latin America Offshore Helicopter Services Market Insights

The Middle East and Africa region is emerging as an important market for offshore helicopter services, with the growth in the offshore drilling of oil and gas exploration and production activities, the adoption of modern practices by state oil companies, and greater regulations regarding offshore personnel safety standards increasing the demand for helicopter services in hitherto underserved regions. Saudi Arabia dominates the MEA region in terms of helicopter revenues due to the wide scope of offshore field operations by Saudi Aramco, with helicopters facilitating worker transportation to and from offshore platforms, pipelines, and emergency services throughout Saudi Aramco's offshore oil and gas facilities.

The deepwater oil reserves of West Africa (Nigeria, Angola, and Equatorial Guinea) are the main contributors to helicopter services revenues in the region through the helicopter services provided by Shell, TotalEnergies, and ExxonMobil as crew transporters for their FPSO assets in West Africa. In Latin America, helicopters generate around 46% of revenue in the region through Brazil's extensive pre-salt program run by Petrobras.

Market Dynamics:

Growth Drivers: Accelerating offshore energy development and expanding offshore wind sector

The continued investment by international and national oil companies in deepwater and ultra-deepwater production development, supported by oil price levels that maintain the commercial viability of high-cost offshore projects, is sustaining and in key basins expanding the crew transport and logistics demand that forms the foundational revenue base for the offshore helicopter services industry. Regulatory requirements for offshore emergency medical capability and search and rescue coverage across all offshore operating jurisdictions globally are creating mandatory demand floors that persist irrespective of commodity price variability, providing operators with structural revenue resilience that supports long-term fleet investment commitments.

Expansion of offshore oil & gas exploration and accelerating offshore wind energy projects in Europe and North America are expected to drive steady growth in offshore helicopter service demand, contributing to an overall market expansion of 5.9% through 2035.

Restraints: High operating costs, regulatory compliance burden, and weather dependency

The offshore helicopter services industry operates with a cost structure characterized by high capital expenditure for modern helicopter acquisition, intensive maintenance requirements driven by regulatory airworthiness standards, substantial crew training and certification costs, and significant insurance premiums reflecting the inherent operational risks of offshore flight operations in challenging maritime environments. These structural cost characteristics create barriers to profitability improvement and limit the ability of operators to reduce pricing in response to customer cost reduction initiatives during periods of oil and gas industry austerity, creating contractual tension that has resulted in market consolidation and operator rationalization across the industry's history.

Opportunities: Offshore wind expansion and emerging basin development represent high-value growth frontiers

The offshore wind energy sector's trajectory toward large-scale far-offshore development in the North Sea, U.S. Atlantic Coast, Taiwan Strait, and Australian continental shelf creates helicopter services demand that is structurally additive to existing oil and gas driven demand, expanding the total addressable market for established operators whose oil and gas expertise is directly applicable to offshore wind operations and maintenance requirements. The application of advanced helicopter types featuring improved range, payload, and all-weather capability, combined with digital mission management and predictive maintenance platforms, is enabling operators to improve service reliability and reduce operating costs in ways that strengthen competitive positioning in contract renewal situations.

Applications of advanced avionics, AI-based flight management systems, and digital twin technologies in offshore helicopter operations are expected to improve mission efficiency rates by 11.80%, while reducing unplanned flight disruptions by 9.12%.

Recent Developments

-

2025:Bristow Group Inc. announced a fleet expansion programme involving the acquisition of six additional Leonardo AW189 heavy helicopters for deployment in North Sea and Gulf of Mexico operations, reflecting the company's confidence in sustained deepwater crew rotation demand and growing offshore wind service requirements across both operating regions.

-

2026:Babcock International Group secured a long-term offshore helicopter services contract with a major North Sea operator for emergency medical evacuation and search and rescue services, incorporating new contractual provisions for offshore wind installation coverage that reflects the growing integration of wind sector requirements into traditional oil and gas operator service frameworks.

-

2025:Airbus Helicopters delivered its 300th H175 medium helicopter to offshore operators globally, marking a commercial milestone for the type that has become a leading platform for offshore crew transport in the North Sea and Asia Pacific markets, with its combination of range, passenger capacity, and operational economics enabling operators to optimize fleet deployment across multiple customer contracts from shared terminal bases.

Offshore Helicopter Services Market Key Players are:

-

Bristow Group Inc.

-

PHI Inc. (Petroleum Helicopters)

-

Babcock International Group

-

Milestone Aviation Group

-

Omniflight LLC

-

Gama Aviation

-

Offshore Logistics Inc.

-

Airbus Helicopters

-

Leonardo S.p.A.

-

Sikorsky Aircraft Corporation (Lockheed Martin)

-

Bell Textron Inc.

-

Air Methods Corporation

-

CHC Helicopter

-

Era Group Inc.

-

Norsk Helikopter AS

-

Lobo Leasing Ltd.

-

Offshore Helicopter Services Ltd.

-

Starspeed Ltd.

-

PTC Helicopter Inc.

-

Titan Helicopter Group

Offshore Helicopter Services Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.65 Billion |

| Market Size by 2035 | USD 6.12 Billion |

| CAGR | CAGR of 5.42% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Light, Medium, Heavy), • By Application (Crew Transport, Cargo Transport, Inspection, Others) • By End User (Oil & Gas Industry, Offshore Wind Industry, Government & Defense Agencies, Commercial Shipping & Marine Logistics, Others) • By Service Type (Scheduled Services, Charter / On-demand Services, Emergency Medical Services (EMS), Search & Rescue Operations, Inspection & Survey Services, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Bristow Group Inc., PHI Inc. (Petroleum Helicopters), Babcock International Group, Milestone Aviation Group, Omniflight LLC, Gama Aviation, Offshore Logistics Inc., Airbus Helicopters, Leonardo S.p.A., Sikorsky Aircraft Corporation (Lockheed Martin), Bell Textron Inc., Air Methods Corporation, CHC Helicopter, Era Group Inc., Norsk Helikopter AS, Lobo Leasing Ltd., Offshore Helicopter Services Ltd., Starspeed Ltd., PTC Helicopter Inc., Titan Helicopter Group. |

Frequently Asked Questions

The offshore helicopter services market is expected to grow at a CAGR of 5.42% from 2026 to 2035.

The offshore helicopter services market was valued at USD 3.65 billion in 2025.

The primary growth factors include sustained offshore oil and gas development activity requiring mandatory crew transport and emergency services, the accelerating expansion of offshore wind energy infrastructure creating structurally new helicopter services demand.

Crew transport segment dominated the market in 2025 due to scalable deployment and centralized data governance.

North America dominated the market in 2025 due to strong adoption of privacy software and strict regulatory frameworks.

Get in Touch