Submarine Market Report Scope & Overview:

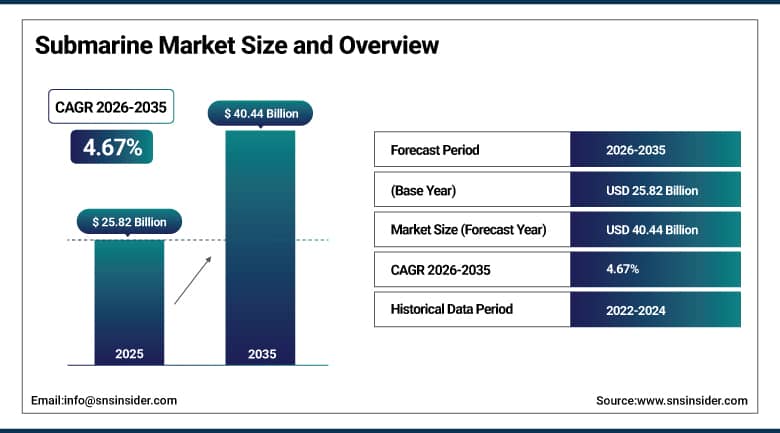

The Submarine Market was valued at USD 25.82 billion in 2025 and is expected to reach USD 40.44 billion by 2035, growing at a CAGR of 4.67% from 2026–2035.

The global submarine market is experiencing consistent growth due to increasing geopolitical uncertainties, modernization initiatives in navies, and the need for advanced capabilities in sub-marine warfare technologies. The increased importance of strategic deterrence, ISR, and ASW operations, together with the adoption of future propulsion technologies like nuclear, diesel-electric, and AIP propulsion, is expected to drive market growth.

Government defense initiatives such as the U.S. Columbia-class and Virginia-class submarine programs, China’s naval expansion strategy, India’s Project-75 and indigenous submarine development programs, Russia’s Borei and Yasen-class modernization efforts, and Europe’s NATO-aligned naval upgrade initiatives have created strong procurement pipelines globally.

Market Size and Forecast

- Market Size 2026E: USD 26.81 Billion

- Market Size 2035: USD 40.44 Billion

- CAGR (2026 - 2035): 4.67%

- Fastest Growing Region: Asia Pacific

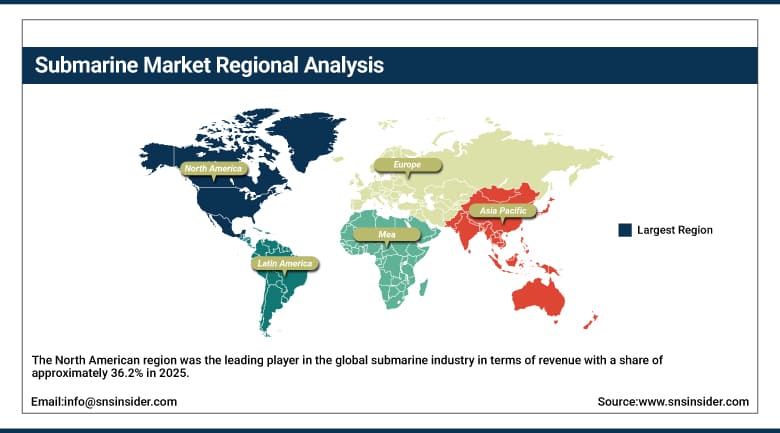

- Largest Region: North America

To Get More Information On Submarine Market - Request Free Sample Report

Submarine Market Trends

- Growing integration of AI-based sonar and combat systems is improving underwater mission accuracy.

- Expanding focus on ISR and ASW operations is boosting demand for multi-role submarines.

- Rising investment in indigenous submarine programs is strengthening domestic defense manufacturing.

- Increasing deployment of missile-equipped submarines is reinforcing strategic deterrence capability.

- Growing use of SATCOM and network-centric systems is improving real-time underwater connectivity.

- Expanding fleet modernization and retrofit programs is extending submarine lifecycle performance.

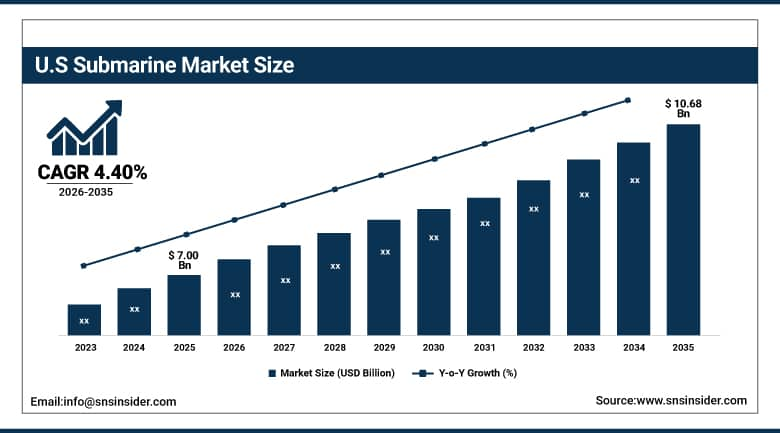

The US Submarine Market Size Outlook

The U.S. Submarine Market was valued at USD 7.00 billion in 2025 and is expected to reach around USD 10.68 billion by 2035, growing at a CAGR of 4.40% from 2026–2035.

Market is experiencing a robust growth pattern due to increased expenditures on defense modernization initiatives, nuclear deterrence needs, and efforts to maintain undersea supremacy in the Atlantic and Indo-Pacific regions. This is mainly attributed to the constant development by the U.S. Navy in next generation submarines through the acquisition of nuclear attack submarines and ballistic missile submarines alongside other cutting-edge shipbuilding technologies. The need for blue water supremacy, second strike capability, and effective maritime surveillance operations has contributed to the fast growth trend through enhanced deployment of submarines that possess optimal stealth and low acoustic signatures.

Recent developments include accelerated procurement of Virginia-class and Columbia-class submarines in the U.S., expansion of China’s nuclear and AIP submarine fleet, and India’s indigenous submarine programs under Project-75 and Project-75(I), along with increased integration of AI-enabled sonar systems, advanced stealth coatings, and next-generation missile launch systems across modern submarine platforms globally.

Submarine Market Segment Analysis

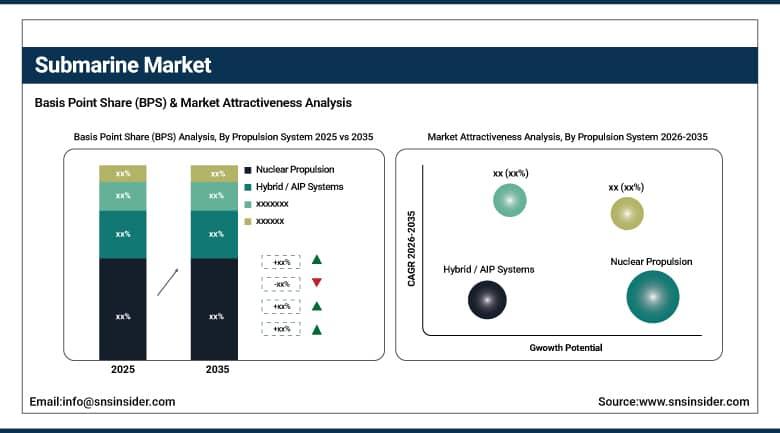

- By Propulsion System, nuclear propulsion dominated the submarine market with the 44.51% share in 2025; hybrid / AIP systems is the fastest-growing segment.

- By Type, nuclear-powered submarines (SSN/SSBN/SSGN) dominated the submarine market with the 42.15% share in 2025; air-independent propulsion (AIP) submarines recorded the fastest growth CAGR.

- By Application, defense & naval warfare dominated the submarine market with the 34.54% share in 2025; intelligence, surveillance & reconnaissance (ISR) is the fastest-growing segment.

- By Combat System, torpedo systems dominated the submarine market with the 38.46% share in 2025; sonar & detection systems are the fastest-growing segment due to increasing underwater engagement modernization.

By Propulsion System, nuclear propulsion dominates the submarine market, while hybrid / air-independent propulsion (AIP) systems are the fastest-growing segment.

Nuclear Propulsion segment dominated the submarine market with the highest revenue share of about 44.51% in 2025 owing to the greater efficiency of operation and endurance offered. Nuclear-powered propulsion continues to be the most favorable form of propulsion due to its ability to enable uninterrupted global operations without limitations on fueling.

Hybrid / AIP Systems segment is projected to register the fastest CAGR during the period 2026–2035 owing to rising demands for subs with low acoustic signature and improved stealth and fuel efficiency. The increased use in coastal defense applications and emphasis on stealthy underwater maneuverability are leading to rapid advancements in AIP technologies.

By Type, nuclear-powered submarines dominate the submarine market, while air-independent propulsion (aip) submarines are the fastest-growing segment.

Nuclear-Powered Submarines (SSN/SSBN/SSGN) segment dominated the submarine market with the highest revenue share of about 42.15% in 2025 this is because of their superior endurance capacity, strategic deterrence capabilities, and ability to conduct operations around the world without needing to resurface. Their supremacy is clearly backed up by increased naval modernization programs being adopted in powerful defense nations like the U.S., Russia, China, and India, where nuclear submarines are critical for dominance at sea.

AIP Submarines segment is projected to register the fastest CAGR during the period 2026–2035 as a result of the increased demand for stealthier, economically viable conventional submarines that can spend longer periods at sea. As more nations develop their defense capabilities, invest in coastal defense systems and asymmetrical warfare, and upgrade their diesel-electric submarine fleets, AIP technology is becoming more common.

By Application, defense & naval warfare dominates the submarine market, while intelligence, surveillance & reconnaissance (ISR) is the fastest-growing segment.

Defense & Naval Warfare segment dominated the submarine market with the highest revenue share of about 34.54% in 2025 as a consequence of rising geopolitical tensions, requirements for maritime border security, and large-scale naval fleet growth. Submarines continue to be a key element for power projection, strategic deterrence, and dominance in underwater combat, with the defense function being central in their use.

ISR segment is projected to register the fastest CAGR during the period 2026–2035 as a result of increasing needs for continuous underwater surveillance, intelligence gathering, and real-time maritime domain awareness. Enhanced use of sonars, sensor fusion technology, and automated tracking is greatly improving the capabilities of submarine-based reconnaissance in contemporary naval warfare.

By Combat System, torpedo systems dominate the submarine market, while sonar & detection systems are the fastest-growing segment.

Torpedo Systems segment dominated the submarine market with the highest revenue share of about 38.46% in 2025 due to extensive use as the primary offensive weapon system underwater. Modernization efforts for heavy weight and light weight torpedoes as well as incorporation of highly sophisticated guidance and targeting systems have further consolidated their dominant position within submarines.

The Sonar & Detection Systems market is expected to experience the highest CAGR from 2026 to 2035 owing to growing focus on situational awareness under water, stealth detection, and threat recognition.

Submarine Market Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025(%) |

|---|---|---|

|

North America |

United States |

83.36% |

|

Europe |

Germany |

27.90% |

|

Asia Pacific |

China |

44.39% |

|

Middle East & Africa |

UAE |

22.39% |

|

Latin America |

Brazil |

31.79% |

North America Submarine Market Insights

The North American region was the leading player in the global submarine industry in terms of revenue with a share of approximately 36.2% in 2025, owing to the robust naval modernization program, high defense budgets, and continuous investment in advanced submarine warfare systems of the U.S. and Canada. The region is blessed with an advanced submarine fleet including nuclear submarines for strategic deterrence and attack submarines, which can also be attributed to the advancements in stealth technology, sonar and combat management systems.

In support of this supremacy, the U.S. Navy’s Virginia-class and Columbia-class submarine programs continue to drive large-scale investments in nuclear-powered platforms, while the AUKUS security partnership is further accelerating submarine technology collaboration, shipbuilding expansion, and long-term fleet modernization initiatives across the United States defense ecosystem.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Submarine Market Insights

Europe has a prominent presence in the submarine industry due to its capability in submarines in nations like the UK, France, Germany, and Russia and its growing emphasis on maritime security and monitoring in the Arctic regions. There has been considerable investment in submarine technology in Europe, especially in the domain of nuclear submarines and modern AIP submarines. Growing tension in the Baltic and Black Sea regions have only increased the significance of submarine-based defense capabilities.

Asia Pacific Submarine Market Insights

Asia Pacific region is projected to have the highest CAGR of around 5.39% during the forecast period due to growing navy expansion, increased defense expenditure, and emphasis on achieving maritime dominance in China, India, Japan, South Korea, and Australia. The growing requirement for nuclear and AIP submarines is propelling the growth of this market in the Asia Pacific region, owing to the rising demand for maritime security by the nations due to increasing regional threats.

Middle East & Africa and Latin America Submarine Market Insights

MEA region and the Latin American region are observing consistent growth in the submarine market due to a growing emphasis on marine security and safeguarding marine assets along with gradual modernization of naval fleet capabilities. Some of the major countries within the MEA region that include Israel, Egypt, and Saudi Arabia are investing in state-of-the-art diesel-electric submarines and Air Independent Propulsion systems, whereas, the major country in the Latin American region is Brazil with its Scorpène class and nuclear submarines.

Market Dynamics:

Growth Drivers: Rising naval modernization programs and increasing demand for stealth, endurance, and multi-mission submarine capabilities are accelerating market expansion

The increasing levels of geopolitical tensions, disputes related to the maritime borders, and competition among the leading nations when it comes to the capabilities of their navies are all responsible for an increase in spending on next generation submarines. Nations like the US, China, India, and Russia have embarked on programs aimed at modernizing their fleets, with a focus on developing nuclear deterrence submarines, AIP-powered submarines, and multirole attack submarines. The increasing importance of stealth operations and long-duration missions has contributed significantly to the increase in spending on submarines. Furthermore, advances in AI-driven sonar technology, combat management, and better propulsion systems are playing a role in increasing efficiency in operations.

Restraints: Extremely high procurement costs, long development cycles, and technological complexity are limiting faster adoption of advanced submarine programs globally

There are various obstacles faced by the sub-marine industry since it requires huge amounts of investment in addition to complicated production processes that take much time to build both nuclear and advanced conventional submarines. It is important to note that the use of complicated mechanisms like nuclear propulsion, stealth technology, sonar equipment, and weapons makes the cost of production higher. Consequently, there are only some few countries that have the capability of investing in this industry and buying submarines. In addition, strict regulations regarding safety issues make the development of projects difficult.

Opportunities: Rising demand for autonomous underwater systems, digital submarine platforms, and next-generation stealth technologies is creating strong growth potential

Significant innovations in autonomous underwater vehicle (AUV), artificial intelligence-driven navigation systems, and digital twin-driven submarine life cycle management technologies are making way for emerging trends in the submarine market. Navies are turning their attention towards developing hybrid crews/uncrewed fleets of submarines to improve surveillance, reconnaissance, and offensive operations as well as reduce risk. Research and development efforts for next-generation stealth coatings, sound dampening technologies, and undetectable powertrain technologies are also leading to innovations in submarine design. The increased focus on investments in smart naval infrastructure and communication networks, as well as command and control networks, is also aiding adoption. Besides, increased spending on procurement and upgrading of submarine platforms in the Asia Pacific region, along with high demand for upgradeable/submarine platforms, offers significant commercial potential.

Recent Developments:

- 2026: General Dynamics Electric Boat expanded its U.S. submarine manufacturing capacity by accelerating construction of Columbia-class ballistic missile submarines and Virginia-class attack submarines, integrating next-generation nuclear propulsion systems and advanced acoustic stealth technologies to support long-term strategic deterrence requirements of the U.S. Navy.

- 2026: Huntington Ingalls Industries (Newport News Shipbuilding) enhanced its submarine modernization programs by upgrading digital shipbuilding infrastructure and integrating advanced modular construction techniques, improving production efficiency and lifecycle maintenance of nuclear-powered submarines for the U.S. fleet, while supporting increased demand for faster delivery timelines.

- 2025: BAE Systems strengthened its submarine combat systems portfolio through upgrades to sonar processing, combat management software, and stealth optimization technologies for Royal Navy Astute and Dreadnought-class submarines, improving underwater detection accuracy and operational survivability in high-threat maritime environments.

- 2025: ThyssenKrupp Marine Systems advanced its diesel-electric and AIP submarine capabilities by enhancing hydrogen fuel cell-based propulsion systems and integrating improved low-noise signature technologies in its Type 212CD platform, supporting growing demand for next-generation stealth conventional submarines in Europe and Asia-Pacific markets.

Submarine Market Key Players are:

-

General Dynamics Electric Boat

-

Huntington Ingalls Industries

-

BAE Systems

-

Naval Group

-

ThyssenKrupp Marine Systems

-

Fincantieri

-

Saab Kockums

-

Mitsubishi Heavy Industries

-

Kawasaki Heavy Industries

-

Hyundai Heavy Industries

-

Hanwha Ocean

-

United Shipbuilding Corporation

-

Admiralty Shipyards

-

Sevmash

-

Mazagon Dock Shipbuilders

-

Larsen & Toubro

-

Lockheed Martin

-

Northrop Grumman

-

Thales Group

-

Leonardo S.p.A.

Submarine Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 25.82 Billion |

| Market Size by 2035 | USD 40.44 Billion |

| CAGR | CAGR of 4.67% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Type (Nuclear-Powered Submarines SSN/SSBN/SSGN, Diesel-Electric Submarines SSK, Air-Independent Propulsion AIP Submarines) •By Application (Defense & Naval Warfare, ISR, Strategic Nuclear Deterrence, ASW) •By Propulsion System (Nuclear Propulsion, Diesel-Electric Propulsion, Hybrid/AIP Systems) •By Combat System (Torpedo Systems, Missile Systems Cruise/Ballistic, Countermeasure Systems, Sonar & Detection Systems) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | General Dynamics Electric Boat, Huntington Ingalls Industries, BAE Systems, Naval Group, ThyssenKrupp Marine Systems, Fincantieri, Saab Kockums, Mitsubishi Heavy Industries, Kawasaki Heavy Industries, Hyundai Heavy Industries, Hanwha Ocean, United Shipbuilding Corporation, Admiralty Shipyards, Sevmash, Mazagon Dock Shipbuilders, Larsen & Toubro, Lockheed Martin, Northrop Grumman, Thales Group, Leonardo S.p.A. |

Frequently Asked Questions

The Submarine market is expected to grow at a CAGR of 4.67% from 2026 to 2035.

The Submarine market was valued at USD 25.82 billion in 2025.

Rising geopolitical tensions, increasing naval modernization programs, and growing investments in stealth, endurance, and multi-mission underwater warfare capabilities are driving demand for advanced submarine platforms globally.

The nuclear-powered submarines (SSN, SSBN, SSGN) segment dominated the submarine market in 2025.

North America dominated the submarine market in 2025

Get in Touch