Tactical Communication Market Report Scope & Overview:

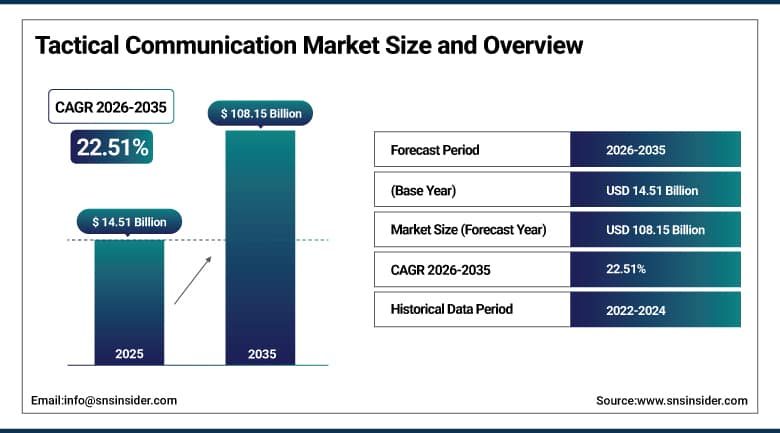

The Tactical Communication Market was valued at USD 14.51 billion in 2025 and is projected to reach USD 108.15 billion by 2035, expanding at a CAGR of 22.51% during 2026–2035.

The tactical communication market is experiencing steady expansion driven by the rapid transformation of modern warfare into a fully network-centric and multi-domain operational environment. Armed forces across major economies are increasingly prioritizing secure, real-time, and interoperable communication systems that integrate land, air, sea, and space-based platforms. Rising demand for Software-Defined Radios (SDR), SATCOM-enabled battlefield connectivity, and LTE/5G-based tactical networks is significantly enhancing command, control, and situational awareness capabilities across defense operations.

Furthermore, in 2024, multiple defense technology providers expanded partnerships with armed forces to deploy advanced MANET-based battlefield communication networks and SATCOM-integrated mobile command systems, supporting enhanced mobility, survivability, and mission-critical coordination in contested and electronically degraded environments.

Market Size and Forecast

-

Market Size in 2026E: USD 17.40 Billion

-

Market Size by 2035: USD 108.15 Billion

-

CAGR Rate (2026-2035): 22.51%

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Tactical Communication Market - Request Free Sample Report

Tactical Communication Market Trends

-

Rising adoption of SDR and advanced waveform technologies is improving interoperability across defense networks.

-

Increasing deployment of SATCOM systems is enhancing long-range battlefield connectivity.

-

Rapid growth of LTE/5G tactical networks is enabling high-speed real-time data exchange.

-

Expanding use of MANET is strengthening resilient communication in contested environments.

-

Rising focus on encrypted and cyber-secure systems is improving protection against electronic warfare.

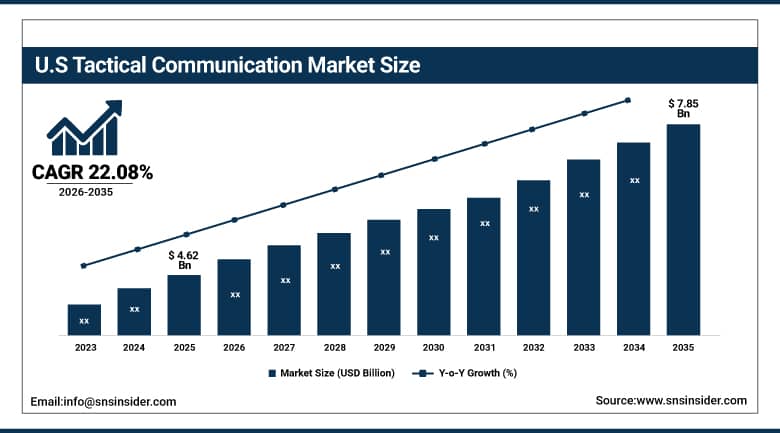

The U.S. Tactical Communication Market Outlook

The U.S. Tactical Communication Market was valued at USD 4.62 billion in 2025 and is projected to reach USD 7.85 billion by 2035, growing at a CAGR of 22.08% from 2026-2035.

The United States remains the dominant country in the tactical communication market due to its extensive defense modernization programs, strong focus on network-centric warfare, and the presence of leading defense communication providers such as RTX Corporation (Collins Aerospace), L3Harris Technologies, Northrop Grumman, General Dynamics, and Honeywell. Growing investments in Joint All-Domain Command and Control (JADC2), next-generation SATCOM integration, and encrypted battlefield communication systems are significantly strengthening operational connectivity and real-time decision-making capabilities across U.S. armed forces.

In 2025, the U.S. Department of Defense expanded next-generation tactical network modernization programs focused on integrating AI-enabled communication routing and resilient SATCOM-based battlefield connectivity across joint forces.

Tactical Communication Market Segment Analysis

-

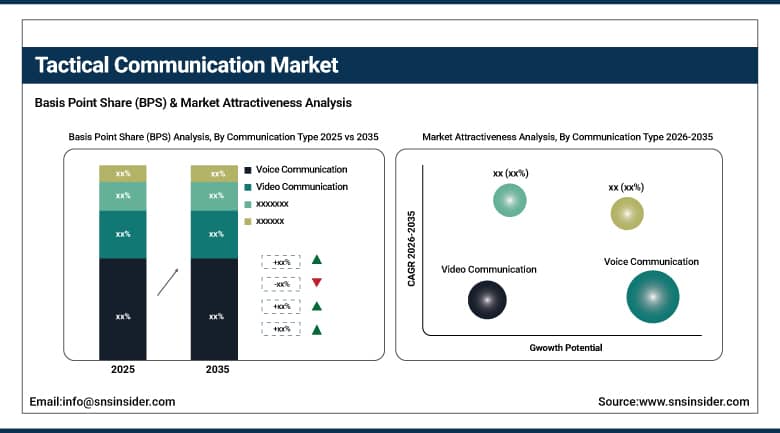

By Communication Type: Voice Communication dominated the market with 34.45% share in 2025; Video Communication showed the fastest growing CAGR.

-

By Platform: Ground (soldier systems, command centers) dominated the market with 42.56% share in 2025; Naval platforms registered the fastest growing CAGR of 25.35%.

-

By Component: Hardware (radios, antennas, terminals) dominated the market with 38.29% share in 2025; Software (network management, encryption, waveform software) posted the fastest growing CAGR.

-

By Technology: Software-Defined Radio (SDR) dominated the market with 38.46% share in 2025; SATCOM recorded the fastest growing CAGR.

By Communication Type, voice communication segment dominated the tactical communication market, video communication showed the fastest growing CAGR.

Voice communication segment maintained its dominant position in the tactical communication market, accounting for 34.45% of total revenue in 2025. It is largely because of the importance of this category in executing commands, coordinating operations, and communicating on the ground that this category continues to dominate. The highly reliable and universal character of this category continues to make it the most extensively used communication category in military operations.

Video communication segment is projected to record the highest CAGR from 2026 to 2035. The fast-paced growth is fueled by rising demands for real-time visualizations on battlefields, live video feeds from UAVs, and improved situational awareness functions. Another factor that has spurred the use of video intelligence in warfare is its increasing application in network-centric warfare platforms.

By Platform, ground (soldier systems, command centers) segment dominates the tactical communication market, naval platforms registered the fastest growing CAGR.

Ground (soldier systems, command centers) segment maintained its dominant position in the tactical communication market, accounting for 42.56% of total revenue in 2025. This particular market’s dominance is mainly attributed to the extensive use of soldier-mounted communications equipment, massive investments in modernizing the command-and-control infrastructure, and the rising need for secure and reliable battlefield communications systems.

Naval segment is projected to record the highest CAGR from 2026 to 2035. This rapid growth is driven by increasing naval modernization programs, rising investments in maritime domain awareness, and expanding adoption of secure ship-to-ship and ship-to-shore communication systems.

By Component, hardware (radios, antennas, terminals) segment dominated the tactical communication market, software (network management, encryption, waveform software) posted the fastest growing CAGR.

Hardware (radios, antennas, terminals) segment maintained its dominant position in the tactical communication market, accounting for 38.29% of total revenue in 2025. This domination is generally reinforced through extensive procurement of rugged communication equipment, swift upgrading of older analog communication equipment with newer SDR-based equipment, and constant modernization of battlefield communication infrastructure.

Software segment is projected to record the highest CAGR from 2026 to 2035. This growth can be attributed to the increasing implementation of AI-driven networking management technologies, encryption software for waveforms, and sophisticated spectrum optimization systems. The growing use of software-defined battlefield communications infrastructures and real-time data routing functionalities is making the military operations more efficient and reliable.

By Technology, software-defined radio (sdr) segment dominated the tactical communication market, satcom recorded the fastest growing CAGR.

Software-defined radio (sdr) segment maintained its dominant position in the tactical communication market, accounting for 38.46% of total revenue in 2025. This domination is caused by wide-spread adoption of SDR solutions in Favor of existing communications technologies, enabling multiband, multifunctional, and extremely compatible features. The increasing trend towards flexible and secure communication structures adds to the popularity of SDR in military communication systems.

Satcom segment is projected to record the highest CAGR from 2026 to 2035. This growth is driven by rising demand for beyond-line-of-sight communication, expansion of multi-domain operations, and increasing integration of space-based communication networks into modern defense communication infrastructure.

Regional Insights:

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

84.54% |

|

Europe |

Germany |

31.56% |

|

Asia Pacific |

China |

45.21% |

|

Middle East & Africa |

UAE |

29.38% |

|

Latin America |

Brazil |

40.17% |

North America Tactical Communication Market Insights

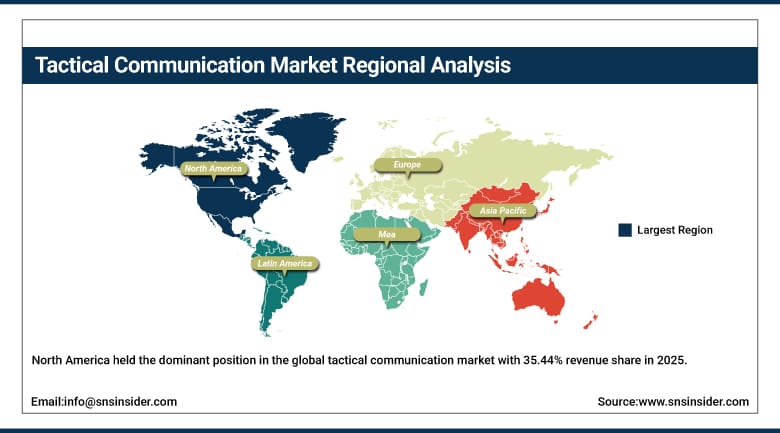

North America held the dominant position in the global tactical communication market with 35.44% revenue share in 2025, motivated by significant efforts at military modernization, high levels of defense spending, and widespread use of advanced communication technology on battlefields. This region is advantaged by having many providers of defense communications, a well-established ecosystem for defense technology, and large expenditures on network-centric warfare. North America’s lead is held by the United States because of increasing expenditures on battlefield digitalization, Software-Defined Radios (SDR), and Joint All-Domain Command and Control (JADC2).

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Tactical Communication Market Insights

Europe is one of the largest markets in the world for tactical communications, owing to the increased efforts towards defense preparedness, high political tensions, and increased emphasis on improving the security of communications within the allied militaries. There is an increased procurement of communication equipment in countries such as Germany, France, the UK, Italy, and Poland. The defense establishments of Europe have become increasingly concerned about improving network centric warfare and communication capabilities.

Asia Pacific Tactical Communication Market Insights

Asia Pacific region is projected to register the highest Cagr with 23.45% growth during 2026–2035, fuelled by the need for defense modernization programs, border security issues, and investments in military communications infrastructure in emerging economies. The growing demand for reliable communication equipment such as tactical radios and battlefield communication solutions is being witnessed from countries like China, India, Japan, South Korea, and Australia. The emergence of locally-made communication technology systems that increase readiness levels is evident in the region.

Latin America, Middle East & Africa (LAMEA) Tactical Communication Market Insights

LAMEA is experiencing consistent growth in the tactical communications market on account of growing modernization trends in the military, growing border security needs, and the growing development in defense communications infrastructure. Countries like Brazil, Mexico, Saudi Arabia, UAE, and South Africa are contributing towards this growth by developing their tactical mobility programs, defense equipment modernization, and acquiring advanced communication solutions. In the Middle Eastern region, there has been an increase in spending on communication infrastructure by the defense department.

Growth Drivers: Rising network-centric warfare initiatives and increasing deployment of secure multi-domain battlefield communication systems creating strong modernization momentum globally.

Some of the main drivers fuelling the market for tactical communications comprise military modernization initiatives which seek to modernize existing battlefields communications networks by equipping them with advanced and real-time tactical communication systems that are secure and interoperable. Demand for Software-Defined Radios (SDR), satellite communication technology (SATCOM), and overall communication systems is growing rapidly and is resulting in increased procurement activity in defense forces globally.

Restraints: High deployment costs, interoperability challenges, and electronic warfare vulnerabilities limiting communication infrastructure scalability

The biggest limitation that restricts tactical communication market from growing further is the high cost of implementing the most advanced Tactical Communication Systems, such as SDR platforms, satellite communications integration technology, and even the communication equipment used on the battlefield. The integration into existing military systems further adds to this burden.

Opportunities: AI-enabled communication networks, next-generation SATCOM integration, and defense digitization programs across emerging military economies.

The deployment of AI-enabled communication routing solutions and implementation of space-based tactical communication solutions emerge as two critical opportunities in the tactical communication market. Advanced communication technologies possess vast opportunities to improve bandwidth efficiency and operational effectiveness in the context of the difficulties arising in the evolving battlefields. The growing trend towards autonomous systems and digital battlefields in the defense industry offers many opportunities for tactical communications.

Bottom of Form

Recent Developments:

-

2026: L3Harris Technologies expanded its next-generation tactical communication portfolio with enhanced Software-Defined Radio (SDR) systems featuring advanced multi-band interoperability and secure waveform capabilities designed for joint multi-domain military operations.

-

2026: Thales Group strengthened its battlefield communication ecosystem through deployment of upgraded tactical communication architectures integrating AI-enabled network management and resilient communication technologies for high-intensity operational environments.

-

2025: RTX Corporation (Collins Aerospace) advanced secure tactical communication solutions through enhanced SATCOM-integrated battlefield networking systems designed to improve beyond-line-of-sight connectivity and real-time operational coordination capabilities.

-

2025: Elbit Systems expanded its digital battlefield communication offerings with next-generation MANET-enabled communication technologies supporting improved situational awareness, encrypted connectivity, and integrated command-and-control operations across mobile defense platforms.

Tactical Communication Market Key Players are:

-

RTX Corporation (Collins Aerospace)

-

L3Harris Technologies Inc.

-

Thales Group

-

BAE Systems plc

-

Northrop Grumman Corporation

-

General Dynamics Corporation

-

Leonardo S.p.A.

-

Saab AB

-

Rohde & Schwarz GmbH & Co. KG

-

Elbit Systems Ltd.

-

Honeywell International Inc.

-

Leonardo DRS

-

Motorola Solutions Inc.

-

Viasat Inc.

-

Iridium Communications Inc.

-

Cobham Limited

-

Curtiss-Wright Corporation

-

Airbus Defence and Space

-

Kongsberg Gruppen ASA

-

ASELSAN A.S.

Tactical Communication Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 14.51 Billion |

| Market Size by 2035 | USD 108.15 Billion |

| CAGR | CAGR of 22.51% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Platform (Ground – Soldier Systems and Command Centers, Airborne Platforms, Naval Platforms, Space-enabled SATCOM-Integrated Systems) • By Component (Hardware – Radios, Antennas, Terminals, Software – Network Management, Encryption, Waveform Software, Services – Integration, Maintenance, Training and Support Services) • By Communication Type (Voice Communication Systems, Data Communication Systems, Video Communication Systems, Integrated Network-Centric Communication Systems) • By Technology (Software-Defined Radio (SDR), SATCOM Systems, LTE/5G Tactical Networks, MANET (Mobile Ad Hoc Networks)) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | RTX Corporation (Collins Aerospace), L3Harris Technologies Inc., Thales Group, BAE Systems plc, Northrop Grumman Corporation, General Dynamics Corporation, Leonardo S.p.A., Saab AB, Rohde & Schwarz GmbH & Co. KG, Elbit Systems Ltd., Honeywell International Inc., Leonardo DRS, Motorola Solutions Inc., Viasat Inc., Iridium Communications Inc., Cobham Limited (Adams C&T / Ultra segment legacy), Curtiss-Wright Corporation, Airbus Defence and Space, Kongsberg Gruppen ASA, ASELSAN A.S. |

Frequently Asked Questions

The tactical communication Market is expected to grow at a CAGR of 22.51% from 2026 to 2035.

The tactical communication Market was valued at USD 14.51 billion in 2025

Ground (soldier systems, command centers) dominated with 42.56% of revenues in 2025.

North America dominated with 35.44% of revenues in 2025.

Get in Touch