Omnichannel Retail Commerce Market Report Scope & Overview:

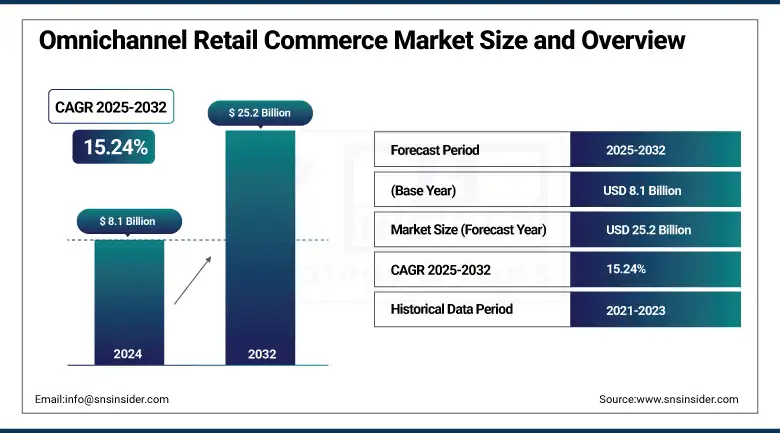

The Omnichannel Retail Commerce Market size was valued at USD 8.1 billion in 2024 and is expected to reach USD 25.2 billion by 2032, growing at a CAGR of 15.24% during 2025-2032.

The omnichannel retail commerce market growth is driven by retailers integrating physical and virtual interaction points to provide seamless customer experiences. This transformation is fueled by uncertainty and increasing expectations for attractive, personalized, and seamless online, mobile, and in-store experiences among consumers. Mobile solutions address key growth fundamentals, with smartphone adoption accelerating, cloud-based solutions advancing, and a need for real-time inventory and customer data more pronounced.

To Get more information On Omnichannel Retail Commerce Market - Request Free Sample Report

E-commerce and mobile commerce are transforming market growth. The transition toward e-business and versatile commerce is persistent and empowering market development. Omnichannel retail commerce market analysis suggests that the use of AI, CRM, and order management platforms is boosting customer engagement by TechCircle. Expected growth till 2032 will rely on the drivers of technology advancements and shifting consumer preferences. Some of the major Omnichannel Retail Commerce Market trends are mobile-first strategies, Artificial Intelligence (AI)-driven personalization, and cloud-based retail infrastructure adoption.

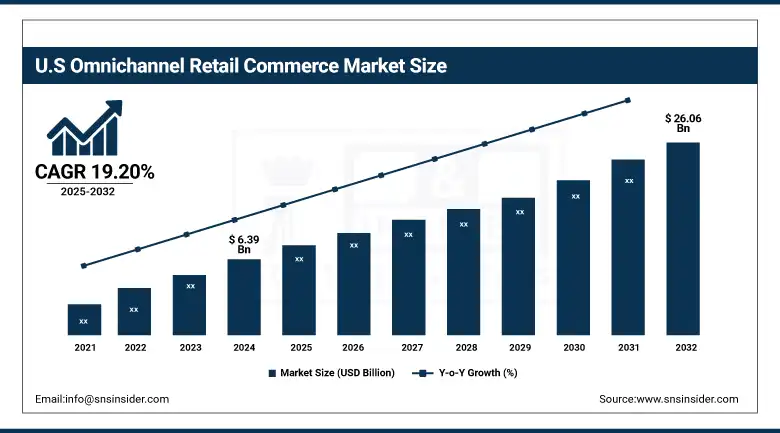

The omnichannel retail commerce market in the U.S. is estimated to reach USD 6.39 billion in 2024 and USD 26.06 billion by 2032, growing at a CAGR of 19.20% during the forecast period. Growth is fueled by the adoption of mobile commerce, the need for a frictionless customer journey, and the emergence of integrated cloud-based retail platforms. The market sees more investment in personalization, AI, and real-time data integration across platforms throughout the period.

Omnichannel Retail Commerce Market Dynamics:

Drivers:

-

Growing Consumer Expectations Drive Need for Seamless Shopping Experiences

Increasing expectation for a seamless and personalized shopping experience between online and offline channels drives the growth of the omnichannel retail commerce market. Brands that provide shoppers with the same product allocation and pricing whenever sought, with or without a customer service touchpoint in the brand's mobile app, web store, or brick-and-mortar location, are becoming the preferred choice for shoppers. To bridge these gaps, retailers are investing in holistic systems, CRM, order management, and real-time inventory tools that allow them to respond to customer expectations while fostering loyalty. The seamless approach not only enhances customer satisfaction but also increases conversion rates and repeat purchases, and is an essential element driving market growth all across subsectors, such as apparel, electronics, and FMCG.

A 2024 Bazaarvoice survey shows that 88% of shoppers expect a consistent experience across online, mobile, and in-store channels, pushing retailers to ensure seamless transitions between platforms.

Restraints:

-

High Integration Costs Limit Adoption Among Smaller Retailers

The biggest restraint that ails the omnichannel retail commerce market is the high cost and complexity of integrating and implementing these omnichannel platforms. For small and mid-sized retailers, it can be difficult to break the budget for an upgrade of legacy systems, training staff, or managing a cross-channel data flow. Furthermore, harmonizing inventory, order fulfillment, and customer service across different platforms requires massive investments in technology and process reengineering. Such high costs can delay adoption and confine market growth, especially in developing economies or independent retail chains with poor access to advanced digital infrastructure or financial resources.

A 2024 GoDaddy survey revealed that only 34% of small retailers offer Buy Online, Pickup In-Store, despite 73% of Gen Z and 83% of Millennials considering it important.

Opportunities:

-

Advancements In AI Create New Avenues for Personalization

The omnichannel retail commerce market has a huge opportunity in technological innovation, especially artificial intelligence and advanced data analytics technology, which drives this transformation. AI-driven tools for tailored recommendations, automated inventory forecasting, and flexibility in pricing are just a few of the constructs now available for retailers. With real-time data, companies can obtain visibility on customer tastes, supply chain optimization, and multi-channel marketing management. These capabilities not only enhance customer experience but also enhance operational efficiency and profitability. The move to the cloud has enabled the best analytical and operational systems to be economically available even to the smallest retailers, thus making AI one of the most important growth and competitive advantage enablers in the omnichannel space.

Challenges:

-

Rising Cybersecurity Risks Threaten Data Integrity Across Channels

Another major challenge faced in the omnichannel retail commerce market is data privacy and cybersecurity. As the customer data is collected over websites, mobile apps, social platforms, and physical stores, the risk of data breaches and cyberattacks increases. Retailers face challenges when it comes to high volumes of sensitive information as they need to comply with strict regulations, such as GDPR and CCPA, enforce strong data protection, and keep customers' trust. Neglecting that search can lead to legal penalties and financial loss, and harm to the brand. With the growing digital integration of retail, preserving cybersecurity evolution and protecting the omnichannel foundation will be a pivotal element in building sustainable growth.

Omnichannel Retail Commerce Market Segmentation Analysis:

By product:

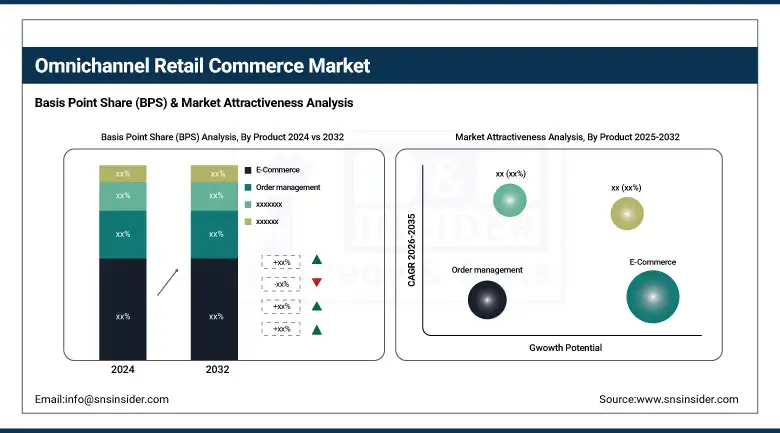

The E-Commerce segment dominated the omnichannel retail commerce market in 2024 and accounted for a significant revenue share, owing to the growing popularity of online stores due to the rising internet accessibility and smartphone uptake globally. The need of consumers to shop whenever they want has forced retailers to improve their online shopping presence. Technologies, such as AI that are effective in providing customized recommendations and AR/VR that assist in enabling virtual try-on have further added to the experience of shopping online. The D2C model, advancements in digital payment systems, and other factors will help ensure this segment's dominant ownership continues.

The order management is expected to grow with the fastest CAGR during the forecast period, owing to the requirement of managing complex order processes across various channels from a single tool. With the omnichannel trend, the need for a strong order management system with real-time inventory visibility and frictionless coordination of online and offline channels has skyrocketed. In addition, the need for better order management solutions is fueled by the quick commerce and same-day delivery wave.

By Deployment:

the on-premise segment dominated the market in 2024 and accounted for 72% of the omnichannel retail commerce market share, as it provides better control of data and better security and customization, which large retailers with complicated IT setups appreciate greatly. However, on-premise systems are still the go-to for many businesses in regulated industries for compliance and internal auditing, even though they are expensive both to set up and maintain. This market segment still contains a good market share as long as full control of the infrastructure is more preferred.

Due to factors, such as scalability, lower initial expenditures, and ease of deployment, SaaS is poised to register the fastest CAGR during 2025-2032. Perfect for all SMEs and growing retailers, cloud-based platforms provide real-time updates, access from anywhere, and seamless integration. SaaS adoption is witnessing a surge across the retail industry due to rising digital transformation and the need for agile commerce solutions.

By End-Use

The Apparel & Footwear segment dominated the omnichannel retail commerce market in 2024 and accounted for 34% of revenue share, due to the rising demand from the younger population for luxury apparel and footwear. Retailers have started using omnichannel retail solutions as this tech-savvy demographic appreciates the convenience of shopping through multiple channels. This segment has further grown due to the integration of both the online and offline experience, such as virtual try-ons and personalized recommendations.

Consumer Electronics segment is expected to be the fastest growing, mostly due to increased penetration of smartphones and rapid uptake of electronic gadgets. From a consumer perspective, retailers are beefing up the features of their offerings in various ways. Such solutions are anticipated to escalate the overall growth of the segment during the forecast period.

Omnichannel Retail Commerce Market Regional Outlook:

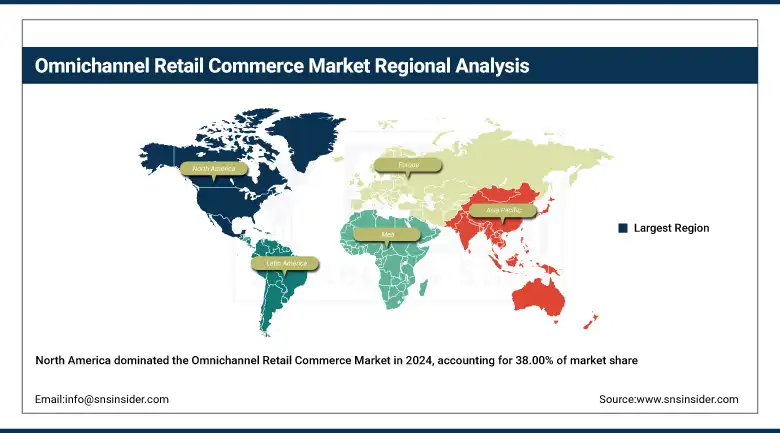

North America dominated the omnichannel retail commerce market and accounted for 38% of revenue share in 2024, due to the regional advanced digital infrastructure, high smartphone penetration, and mature e-commerce ecosystem. Big players including Amazon and Walmart have made substantial investments in omnichannel, covering BOPIS and mobile commerce. Tech-native shoppers in the region keep demand steady for integrated in-store and online shopping experiences.

Get Customized Report as per Your Business Requirement - Enquiry Now

The Asia Pacific region is projected to record the fastest CAGR during the forecast period, driven by the increase in internet users, mobile shopping, expansion of e-commerce in China, India, and Southeast Asian countries. In the region, retailers are swiftly adopting AR/VR and IoT to connect offline and online chains. This is also fueled by government digitalization initiatives and an emerging middle class that supports the region’s shift toward omnichannel.

The omnichannel retail growth in Europe is largely supported by the rapid adoption of digital technologies, the growing inclination of hybrid shopping behaviours by consumers, and the conducive regulatory environment. Smart retail infrastructure is being implemented in countries. Consumer demand for personalized, smooth retail experiences wherever they might be in the region will define the future trajectory of the market, which will continue expanding at a steady pace.

The U.K. has a stronghold in the European omnichannel retail commerce market with elevated levels of e-commerce penetration, well-established logistics, and widespread omnichannel strategies. Integrated platforms are led by retailers, such as Tesco and John Lewis. As AI, mobile payments, and real-time inventory systems revolutionize customer engagement and operational efficiency, the growth will continue.

Key Players:

The major omnichannel retail commerce market companies are Salesforce, Oracle, SAP, Adobe, IBM, Shopify, Microsoft, NCR Corporation, Toshiba Global Commerce Solutions, Zebra Technologies, and others.

Recent Developments:

In January 2025, Salesforce introduced Agentforce for Retail, an AI-powered platform with pre-built skills for tasks including order management and appointment scheduling. They also launched Retail Cloud with Modern POS, integrating online and offline data to enhance personalized shopping experiences across channels.

In January 2025, SAP unveiled the SAP S/4HANA Cloud Public Edition tailored for retail, fashion, and vertical businesses, offering integrated ERP capabilities. They also announced an upcoming AI shopping assistant and a new loyalty management solution aimed at enhancing personalized customer experiences and loyalty programs.

|

Report Attributes |

Details |

|---|---|

|

Market Size in 2024 |

USD 8.1 Billion |

|

Market Size by 2032 |

USD 25.2 Billion |

|

CAGR |

CAGR of 15.24% From 2025 to 2032 |

|

Base Year |

2024 |

|

Forecast Period |

2025-2032 |

|

Historical Data |

2021-2023 |

|

Report Scope & Coverage |

Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

|

Key Segments |

• By Product (E-Commerce, Order Management, Point of Sales, Retail Order Broker Cloud, CRM, Warehouse Management, Others) |

|

Regional Analysis/Coverage |

North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

|

Company Profiles |

Salesforce, Oracle, SAP, Adobe, IBM, Shopify, Microsoft, NCR Corporation, Toshiba Global Commerce Solutions, Zebra Technologies and others in the report |

Frequently Asked Questions

North America region dominated the Omnichannel Retail Commerce Market with 38% of revenue share in 2024.

The on-premise segment dominated the market in 2024 and accounted for 72% of the omnichannel retail commerce market share.

Growing Consumer Expectations Drive Need For Seamless Shopping Experiences

The Omnichannel Retail Commerce Market size was valued at USD 8.1 billion in 2024 and is expected to reach USD 25.2 billion by 2032

The CAGR of the Omnichannel Retail Commerce Market during the forecast period is 15.24% over 2025-2032.

Get in Touch