On-Device AI Market Report Scope & Overview:

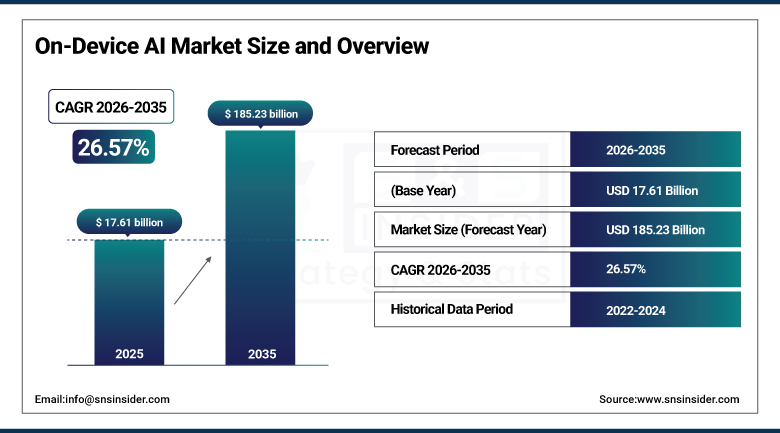

The On-Device AI Market was valued at USD 17.61 Billion in 2025 and is expected to reach USD 185.23 Billion by 2035, growing at a CAGR of 26.57% from 2026–2035.

The global on-device AI market is at the epicentre of the most significant architectural shift in artificial intelligence deployment since the cloud computing era began, as the fundamental limitations of cloud-dependent AI processing in terms of latency, bandwidth consumption, data privacy vulnerability, and connectivity dependency are driving the technology ecosystem’s progressive rebalancing toward intelligent processing capabilities that reside on the endpoint device itself rather than in remote data centres. On-device AI, which encompasses the hardware processors, software frameworks, and model optimisation techniques that enable AI inference to be performed locally on smartphones, wearables, automotive systems, IoT devices, and edge computing infrastructure without requiring real-time cloud connectivity, addresses these limitations by delivering the millisecond-response times that self-driving vehicle safety systems require, the offline functionality that healthcare diagnostic applications in connectivity-limited environments need, and the categorical privacy assurance that sensitive personal data never leaves the device that an increasing proportion of consumers and regulatory frameworks demand as a prerequisite for comfortable AI adoption.

Apple’s September 2025 introduction of the Foundation Models framework, enabling iOS, iPadOS, and macOS developers to create intelligent, privacy-focused applications using on-device AI processing without routing user data through Apple’s servers, represents the most commercially significant platform development in the on-device AI market to date, as Apple’s 2.3 billion active device installed base creates an unprecedented distribution channel for on-device AI application experiences whose scale of consumer exposure will normalise on-device AI capability across the global smartphone user population in a way that no previous technical announcement has achieved.

Market Size and Forecast

-

Market Size in 2026E: USD 22.29 Billion

-

Market Size by 2035: USD 185.23 Billion

-

CAGR: 26.57% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on On-Device AI Market - Request Free Sample Report

On-Device AI Market Trends

-

Accelerating integration of dedicated neural processing units and AI accelerators into every tier of the smartphone processor market, from flagship Snapdragon 8 Elite and Apple A18 Pro chips whose NPU compute density rivals discrete GPU performance for specific AI workloads through mid-range MediaTek Dimensity and Qualcomm Snapdragon 7 series processors that are democratising on-device AI capability beyond the premium segment into the high-volume mid-range device category that constitutes the majority of global smartphone shipments.

-

Growing deployment of on-device generative AI capabilities including real-time text generation, image synthesis, voice cloning, and multimodal reasoning on consumer devices, transitioning generative AI from a cloud-API-dependent technology requiring constant internet connectivity into a local inference capability that users can access in aeroplane mode, in remote environments, and in data-sensitive contexts where routing creative AI requests through third-party cloud servers raises intellectual property and privacy concerns.

-

Rising importance of on-device AI in automotive systems where the safety-critical real-time processing requirements of advanced driver assistance systems, automated emergency braking, lane-keep assist, and occupant monitoring cannot tolerate the latency variability of cloud-dependent AI inference and where the connectivity interruptions of tunnels, underground parking, and rural driving would create unacceptable safety gaps if ADAS intelligence depended on continuous network access.

-

Expanding application of on-device AI in healthcare wearables and medical IoT devices where continuous monitoring of electrocardiogram signals, blood glucose trends, respiratory patterns, and sleep quality data at the device level enables persistent health intelligence that would generate overwhelming data volumes if transmitted raw to cloud processing infrastructure, while the medical data privacy requirements of HIPAA, GDPR, and equivalent regulations create strong compliance motivation for on-device processing that keeps sensitive patient health data on the individual’s device.

-

Growing commercial ecosystem of on-device AI developer tools, model repositories, and hardware-software co-design services as chip manufacturers including Qualcomm, MediaTek, and Apple provide vendor-specific AI development frameworks, pre-optimised model libraries, and performance profiling tools that reduce the engineering investment required to port AI workloads from cloud to device while maintaining the accuracy levels that end-user applications require.

U.S. On-Device AI Market Outlook

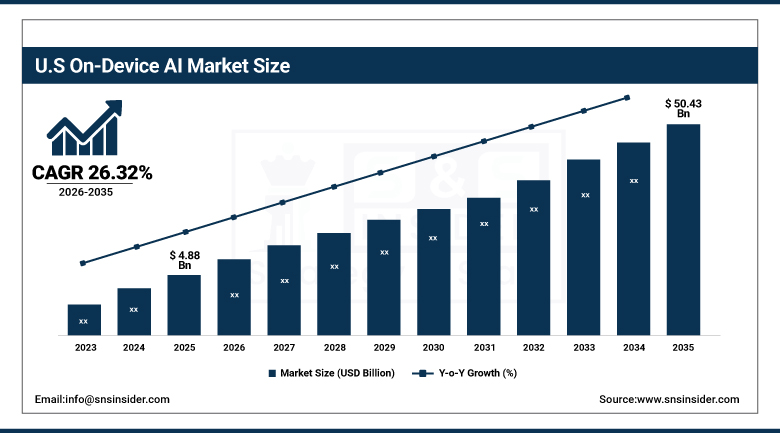

The U.S. on-device AI market was valued at approximately USD 4.88 Billion in 2025 and is expected to reach approximately USD 50.43 Billion by 2035, growing at a CAGR of approximately 26.32%.

The United States represents the world’s leading on-device AI market by both technological innovation output and commercial adoption depth, anchored by the presence of the market’s defining platform companies whose silicon engineering, software development, and device ecosystem control creates on-device AI capabilities that the entire global smartphone, automotive, and IoT industry progressively builds upon. Apple’s vertically integrated silicon-software-hardware ecosystem, whose Apple Intelligence privacy-by-design AI system processes language, image, and voice AI workloads on-device by default with selective cloud routing only for more complex tasks, represents the world’s most commercially impactful on-device AI deployment whose user base of over 200 million U.S. iPhone users creates the largest single national market for on-device AI consumer experiences.

OpenAI’s April 2026 announcement of plans to co-develop specialised AI processors with Qualcomm and MediaTek for an AI-native smartphone platform, aiming for 300 to 400 million annual units and targeting mass-market consumer adoption of deeply integrated on-device AI capabilities, represents the most commercially ambitious on-device AI platform initiative yet announced and, if executed, would create a new category of AI-first smartphone whose on-device processing architecture is optimised for AI agent capability rather than treating AI as an additive feature layer on top of a conventional smartphone operating model.

On-Device AI Market Segment Analysis

-

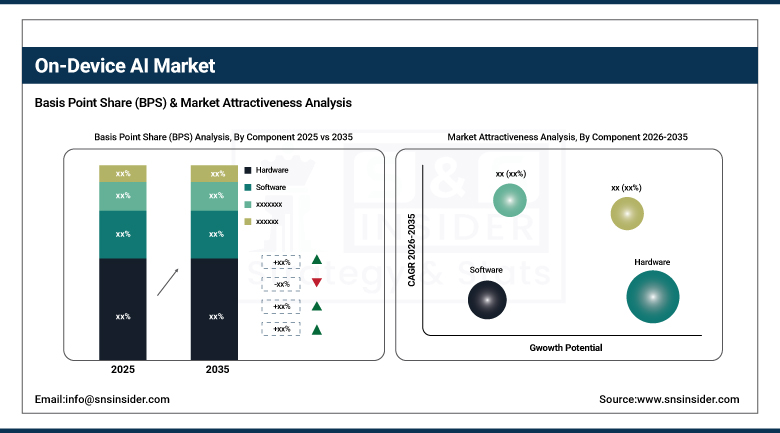

By Component, hardware dominated with approximately 60.40% share in 2025 driven by the increasing penetration of dedicated AI processors, neural processing units, and AI-optimised chipsets in smartphones, wearables, automotive systems, and industrial IoT devices; software is the fastest-growing segment at a CAGR of approximately 31.04% driven by rising demand for AI frameworks, model compression tools, and intelligent applications that can operate efficiently on resource-constrained edge hardware.

-

By Type, smartphones & tablets led with approximately 56.70% share in 2025 driven by the high adoption rate of AI-integrated chips across global smartphone shipments exceeding 1.3 billion units annually; wearables are the fastest-growing type at a CAGR of approximately 25.24% driven by the proliferation of health monitoring applications requiring continuous on-device AI inference for ECG analysis, blood oxygen monitoring, sleep staging, and fall detection.

-

By Technology, machine learning led the on-device AI market in 2025 as the foundational AI technique enabling image recognition, speech processing, predictive text, and anomaly detection across the broadest range of device and application categories; natural language processing is the fastest-growing technology driven by the expansion of on-device voice assistant capability, real-time translation, and generative text features that are progressively replacing cloud-dependent NLP with local inference for privacy-sensitive language tasks.

-

By Vertical, consumer electronics held the largest share at approximately 41.06% in 2025 driven by mass-market AI smartphone adoption across global device shipments; automotive is the fastest-growing vertical at a CAGR of approximately 25.30% driven by increasing integration of on-device AI in ADAS systems, in-vehicle voice assistants, driver monitoring, and real-time navigation intelligence across the rapidly electrifying and autonomy-advancing global vehicle market.

By Component, hardware dominates, software grows fastest

Hardware retained the dominant component position with approximately 60.40% of the on-device AI market in 2025, a dominance reflecting the fundamental commercial reality that on-device AI capability is enabled by and limited by the dedicated silicon processing infrastructure embedded in each device, whose performance characteristics in terms of neural network inference throughput, memory bandwidth, and power efficiency per TOPS determine the AI application experiences that device manufacturers can deliver and that consumers can access. The hardware segment encompasses the neural processing units embedded in application processors from Apple, Qualcomm, MediaTek, Samsung Exynos, and HiSilicon, the dedicated AI accelerators in automotive system-on-chip from NVIDIA, Qualcomm, and Mobileye, the micro-NPUs in ultra-low-power IoT edge processors from Arm Cortex-M NPU and NXP eIQ, and the specialised AI inference accelerators in industrial edge computing platforms. Each silicon generation cycle delivers substantial NPU performance per watt improvement whose commercial impact is to expand the range of AI model complexities that can run on-device within battery and thermal constraints, progressively bringing workloads that previously required cloud processing infrastructure within the capability envelope of mobile and edge device hardware.

Software is the fastest-growing component at a CAGR of approximately 31.04% through 2035, propelled by the extraordinary developer ecosystem activity around on-device AI frameworks, model optimisation tools, and AI-powered application development whose commercial momentum reflects both the technology’s rapid maturation and the enormous application opportunity that on-device AI processing opens for developers who can now build private, low-latency, offline-capable AI experiences that cloud-dependent alternatives cannot provide. Apple’s Foundation Models framework announced in September 2025 enabling developers to access on-device language model capabilities through standard API calls, Google’s MediaPipe on-device ML solution library, Qualcomm’s AI Model Efficiency Toolkit, and the TensorFlow Lite and PyTorch Mobile deployment frameworks collectively define the software infrastructure on which on-device AI application development is built at scale, and whose continuous capability expansion is progressively reducing the engineering effort required to deploy sophisticated AI models on resource-constrained device hardware.

By Type, smartphones & tablets dominate, wearables grow fastest

Smartphones and tablets retained the dominant type position with approximately 56.70% of the on-device AI market in 2025, reflecting their status as both the world’s highest-volume consumer device category and the platform on which on-device AI capability is most immediately commercially relevant for the broadest consumer audience. Every major smartphone processor released since 2021 incorporates dedicated neural processing hardware as standard, meaning that on-device AI capability has been delivered to over 3 billion device users globally through the natural upgrade cycle of smartphone hardware replacement without requiring any additional consumer purchasing decision or application download. The smartphone’s role as the primary personal computing and communications device creates an extraordinary breadth of on-device AI use case relevance spanning camera scene recognition and portrait mode, real-time language translation in messaging, predictive keyboard personalisation, voice assistant wake-word detection and command processing, face ID biometric authentication, battery usage optimisation, and the emerging generative AI features including on-device summarisation, writing assistance, and image generation that Apple Intelligence and Google Gemini Nano are bringing to mass consumer device experience.

Wearables are the fastest-growing type segment at a CAGR of approximately 25.24% through 2035, driven by the extraordinary commercial expansion of health and fitness wearable devices including smartwatches, fitness trackers, continuous glucose monitors, and smart earbuds whose core value proposition increasingly depends on sophisticated on-device AI processing that can analyse biometric data streams continuously throughout the day and night without requiring cloud connectivity or draining device batteries through continuous wireless data transmission. Apple Watch’s cardiac monitoring capabilities including ECG analysis, atrial fibrillation detection, and irregular heart rhythm notification are enabled by on-device neural network inference that processes electrocardiogram data locally in real time, exemplifying the category-defining health monitoring capability that is driving both consumer demand for premium health-focused wearables and competitive investment by Garmin, Samsung, Fitbit, and Chinese wearable manufacturers in equivalent on-device health AI capabilities.

By Vertical, consumer electronics dominates, automotive grows fastest

Consumer electronics retained the dominant vertical position with approximately 41.06% of the on-device AI market in 2025, reflecting the extraordinary volume of AI-capable consumer devices entering the global market annually through smartphone refresh cycles, smart speaker upgrades, smart television purchases, and wireless earphone replacements that each incorporate progressively more capable on-device AI processing as a differentiating feature rather than a premium option. The consumer electronics vertical’s AI capability density is increasing with each product generation cycle as device manufacturers compete on AI experience quality in categories including real-time noise cancellation in wireless earbuds, scene and subject recognition in digital cameras, smart home device responsiveness and local control reliability, and the emerging personal AI assistant experiences that smartphone manufacturers are competing to define as the next-generation consumer electronics value proposition beyond hardware specification improvement. The consumer electronics vertical’s on-device AI commercial development is particularly advanced in the premium segment where Apple’s iPhone, Galaxy S, and Pixel device lines have established on-device AI as a primary marketing differentiator whose capabilities are demonstrated through flagship consumer experience showcases that generate media attention and purchase consideration among the broader premium smartphone consumer audience.

Automotive is the fastest-growing vertical at a CAGR of approximately 25.30% through 2035, propelled by the accelerating integration of on-device AI across the full spectrum of automotive intelligence functions that directly determine driver safety, vehicle efficiency, and the premium in-cabin experience that differentiate modern vehicles in an increasingly competitive and electrifying global automotive market. The automotive on-device AI requirement is uniquely demanding in its combination of real-time processing latency requirements measured in microseconds for collision avoidance decisions, functional safety certification standards under ISO 26262 that mandate rigorous validation of AI model behaviour across all driving conditions including adversarial weather, night, and occlusion scenarios, and the extended product lifetime requirement of automotive electronics whose 10 to 15 year vehicle service life far exceeds the 2 to 3 year AI capability improvement cycles that consumer electronics device categories follow. Tesla’s continued development of its proprietary FSD chip for full self-driving neural network inference, Mobileye’s EyeQ automotive AI processor line, and Qualcomm’s Snapdragon Ride automotive platform collectively define the leading edge of automotive on-device AI hardware whose capability roadmaps are closely tracked by every vehicle manufacturer evaluating their autonomous driving technology development strategy.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

61.7% |

|

Middle East & Africa |

Saudi Arabia |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America On-Device AI Market Insights

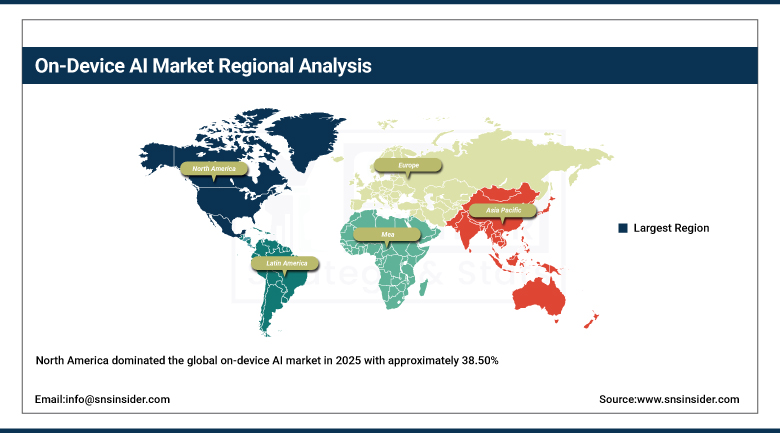

North America dominated the global on-device AI market in 2025 with approximately 38.50% of global revenues, driven by the region’s concentration of the world’s leading on-device AI technology developers including Apple, Qualcomm, Google, NVIDIA, and Intel whose silicon engineering, software platform development, and device ecosystem leadership collectively define the global on-device AI capability standard that Asian and European device manufacturers progressively adopt and build upon. The United States accounts for approximately 87.4% of North American on-device AI revenues through its combination of the world’s highest-value smartphone installed base led by the iPhone’s dominant premium market position, the most developed enterprise edge AI deployment market, and the automotive AI development programmes of Tesla, General Motors, Ford, and the North American operations of Japanese and Korean automotive manufacturers. Canada contributes approximately 12.6% of North American revenues through a technology sector with growing AI chip design capability and a consumer electronics market whose premium device adoption patterns closely mirror U.S. trends.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe On-Device AI Market Insights

Europe is a technically sophisticated on-device AI market whose distinctive characteristic is the GDPR data protection framework’s commercial pull toward on-device processing as a privacy-by-design architecture that eliminates the personal data cloud transmission that conventional cloud AI requires, creating a regulatory incentive alignment between on-device AI technology advantages and the data governance requirements that European consumers and regulators both prioritise. Germany accounts for approximately 22.3% of European on-device AI revenues as the region’s largest national market, anchored by the automotive AI development programmes of Volkswagen, BMW, Mercedes-Benz, Bosch, and Continental whose investment in on-device AI for ADAS, in-vehicle intelligence, and manufacturing automation creates the most commercially significant European on-device AI demand pool in any single national market. The European AI Act’s high-risk AI system classification requirements for automotive, healthcare, and critical infrastructure AI applications are creating additional commercial pressure toward on-device processing architectures that maintain AI decision logic within the device’s auditable computational boundary rather than distributing it across cloud infrastructure that complicates regulatory traceability and accountability.

Asia Pacific On-Device AI Market Insights

Asia Pacific is the fastest-growing regional on-device AI market at a CAGR of approximately 27.83% through 2035, driven by the region’s extraordinary dominance of global smartphone hardware manufacturing, the world’s largest consumer electronics production ecosystem, and the competitive intensity of the Chinese, South Korean, and Taiwanese smartphone markets whose leading brands including Xiaomi, OPPO, Vivo, Samsung, and Huawei are competing on AI capability as a primary device differentiation dimension. China accounts for approximately 61.7% of Asia Pacific on-device AI revenues through its combination of the world’s largest smartphone shipment volume, rapidly advancing domestic AI chip capabilities from HiSilicon’s Kirin series and emerging competitors, and government-supported AI technology development programmes that are directing research and commercial investment toward AI chip design capabilities that reduce the country’s dependence on foreign semiconductor IP in strategically important AI hardware categories. South Korea’s Samsung Electronics represents one of Asia Pacific’s most significant on-device AI contributors through its Exynos processor development programme and its Galaxy AI initiative that deploys on-device AI capabilities including real-time translation, photo editing, and generative text across its global smartphone user base of over 300 million active devices.

MEA & Latin America On-Device AI Market Insights

The Middle East and Africa and Latin America are emerging on-device AI markets where the rapid growth of smartphone penetration, the adoption of AI-integrated mid-range devices from Asian manufacturers whose competitive pricing makes AI-capable hardware accessible to mass-market consumer demographics, and the specific advantage of on-device AI in connectivity-limited environments that characterise significant portions of these regions’ geographies are collectively creating growing commercial on-device AI deployment across applications spanning mobile photography, voice translation, agricultural monitoring IoT devices, and mobile healthcare diagnostics. Saudi Arabia leads Middle East and Africa on-device AI revenues at approximately 38.4% of the regional total through the Kingdom’s high smartphone penetration rate, above-average premium device adoption among its young, tech-forward consumer population, and the growing deployment of AI-enabled surveillance, smart city IoT, and industrial automation systems under Vision 2030’s digital transformation agenda. Brazil leads Latin American on-device AI revenues at approximately 44.2% of the regional total through its large and growing smartphone user base, the rapid adoption of Chinese on-device AI-capable mid-range devices by its cost-conscious but technology-enthusiastic consumer population, and a growing technology sector whose software development community is progressively engaging with on-device AI application development frameworks.

Market Dynamics

Growth Drivers: Real-time processing demand requiring sub-millisecond AI inference latency that cloud architecture cannot deliver, data privacy regulation and consumer concern driving on-device processing preference, and semiconductor NPU efficiency improvement enabling increasingly sophisticated AI on power-constrained devices

The primary structural growth drivers for the on-device AI market are the convergent pressures of real-time performance requirements and data privacy imperatives that collectively create compelling commercial motivation for on-device AI architecture across every major application vertical simultaneously. The latency argument for on-device AI is quantifiable and compelling: cloud AI inference round-trip times typically range from 50 to 300 milliseconds in network-connected conditions and become completely unavailable in offline scenarios, while on-device inference can deliver sub-5-millisecond response times for optimised models running on current-generation NPU hardware, a performance differential that is the difference between viable and unviable for autonomous vehicle collision avoidance, continuous health monitoring alarm, industrial anomaly detection, and augmented reality overlay use cases where response time directly determines whether the AI system adds value or creates safety risk. The privacy motivation is simultaneously strengthening as consumer awareness of AI data collection practices grows and as regulatory frameworks including GDPR’s data minimisation principle, the U.S.’ proposed federal AI privacy legislation, and China’s Personal Information Protection Law create legal incentive structures that favour AI processing architectures keeping personal data on the user’s device.

Restraints: Device compute and memory constraints limiting on-device model complexity relative to cloud equivalents, battery life impact of sustained NPU workloads, and fragmented hardware ecosystem complicating cross-device AI application development

A significant restraint on the on-device AI market is the fundamental compute resource asymmetry between edge device hardware and cloud data centre infrastructure that will persist across the forecast period despite NPU efficiency improvement, as the thermal and battery constraints of mobile devices create absolute upper bounds on sustained AI inference power consumption that cloud computing’s elastic infrastructure scale is not subject to. The practical commercial consequence is that the most sophisticated AI model capabilities including state-of-the-art large language model inference, real-time video generation, and complex multimodal reasoning require cloud processing infrastructure for their highest-capability versions even as on-device equivalents improve, creating a persistent performance gap between cloud and device AI experiences that limits on-device AI to the model complexity tiers whose accuracy and capability suffice for device-appropriate use cases without matching the frontier model performance that cloud inference can deliver with effectively unlimited compute.

Opportunities: OpenAI-Qualcomm AI-native smartphone platform creating new on-device AI device category, automotive ADAS AI hardware expansion, and healthcare wearable continuous monitoring creating high-value regulated application markets

The OpenAI-Qualcomm partnership announced in April 2026 to co-develop specialised AI processors for an AI-native smartphone platform targeting 300 to 400 million annual units represents the most commercially significant near-term opportunity in the on-device AI market, as the creation of a mass-market smartphone whose hardware and software architecture is designed from inception around on-device AI agent capability rather than retrofitting AI features onto a conventional smartphone design could accelerate on-device AI market growth by establishing a new device category standard that competitive device manufacturers must match across the global mid-range and premium smartphone market. Healthcare wearable AI represents a high-value and regulatory-protected application category whose commercial development is being driven by the convergence of medical-grade sensor miniaturisation, NPU efficiency improvement enabling continuous biometric inference within hearing aid-level power budgets, and clinical evidence accumulation that is progressively expanding the regulatory-cleared health conditions that wearable on-device AI can monitor and alert for without requiring a prescription.

Recent Developments:

-

2025: Apple introduced the Foundation Models framework in September 2025, enabling iOS, iPadOS, and macOS developers to build intelligent, privacy-focused applications using on-device AI processing capabilities across Apple’s installed device base of 2.3 billion active devices, marking the most significant on-device AI developer platform launch in the market’s commercial history by volume of addressable devices and developer community scale.

-

2025: Apple expanded its on-device AI capabilities through Apple Intelligence in June 2025, integrating writing tools, image generation, and a substantially enhanced Siri experience powered by on-device model inference across iPhone 15 Pro and newer devices, demonstrating the consumer-facing on-device AI experience quality that Apple’s Silicon Neural Engine can deliver while maintaining the privacy-by-design architecture that Apple positions as a competitive differentiator versus cloud-dependent AI alternatives.

-

2025: Deutsche Telekom unveiled plans at Mobile World Congress 2025 for an ‘AI Phone’ developed in collaboration with Perplexity AI that replaces conventional app-centric user interfaces with AI-native interaction models minimising reliance on individual apps, demonstrating telecommunications operator interest in on-device AI as a platform-level differentiation strategy beyond network connectivity value proposition.

-

2025: Qualcomm showcased the Snapdragon X Elite at Computex 2025, emphasising the platform’s AI PC capabilities including 45 TOPS NPU performance for on-device AI workloads across Windows applications, demonstrating that on-device AI capability is extending beyond smartphone into the personal computer category whose 280 million annual unit shipment volume represents a significant new commercial frontier for on-device AI hardware and software.

-

2026: OpenAI announced in April 2026 plans to co-develop specialised AI processors with Qualcomm and MediaTek for an AI-native smartphone platform targeting 300 to 400 million annual units, representing a fundamental commitment to on-device AI as the architecture for next-generation consumer device intelligence and creating competitive pressure on Apple, Samsung, and Google to accelerate their own on-device AI hardware and software development roadmaps.

On-Device AI Market Key Players

-

Apple Inc.

-

Qualcomm Technologies Inc.

-

Samsung Electronics Co. Ltd.

-

Google LLC (Alphabet Inc.)

-

MediaTek Inc.

-

Huawei Technologies Co. Ltd. (HiSilicon)

-

NVIDIA Corporation

-

Intel Corporation

-

Arm Holdings plc

-

Baidu Inc.

-

Synaptics Inc.

-

Broadcom Inc.

-

NXP Semiconductors N.V.

-

STMicroelectronics N.V.

-

Texas Instruments Inc.

-

Rockchip Electronics Co. Ltd.

-

Ambarella Inc.

-

SiMa.ai

-

Eta Compute Inc.

-

DeGirum Corporation

On-Device AI Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 17.61 Billion |

| Market Size by 2035 | USD 185.23 Billion |

| CAGR | CAGR of 26.57% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Hardware, Software) • By Type (Smartphones & Tablets, Wearables, Automotive Systems, Smart Home Devices, Industrial IoT Devices, Others) • By Technology (Machine Learning, Natural Language Processing, Computer Vision, Others) • By Vertical (Consumer Electronics, Automotive, Healthcare, Industrial, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Apple Inc., Qualcomm Technologies Inc., Samsung Electronics Co. Ltd., Google LLC (Alphabet Inc.), MediaTek Inc., Huawei Technologies Co. Ltd. (HiSilicon), NVIDIA Corporation, Intel Corporation, Arm Holdings plc, Baidu Inc., Synaptics Inc., Broadcom Inc., NXP Semiconductors N.V., STMicroelectronics N.V., Texas Instruments Inc., Rockchip Electronics Co. Ltd., Ambarella Inc., SiMa.ai, Eta Compute Inc., DeGirum Corporation |

Frequently Asked Questions

North America dominated the On-Device AI Market in 2025, with the United States accounting for approximately 87.4% of North American revenues.

Hardware dominated with approximately 60.40% of revenues in 2025.

The rising demand for real-time sub-millisecond AI inference that cloud architecture cannot deliver for latency-critical applications combined with growing data privacy regulation and consumer concern driving preference for on-device processing that keeps personal data on the user’s device, and continuous semiconductor NPU efficiency improvement enabling increasingly sophisticated AI models to run within the power and memory constraints of mobile and edge devices.

The On-Device AI Market was valued at USD 17.61 Billion in 2025.

The On-Device AI Market is expected to grow at a CAGR of 26.57% from 2026 to 2035.

Get in Touch