Online Book Services Market Report Scope & Overview:

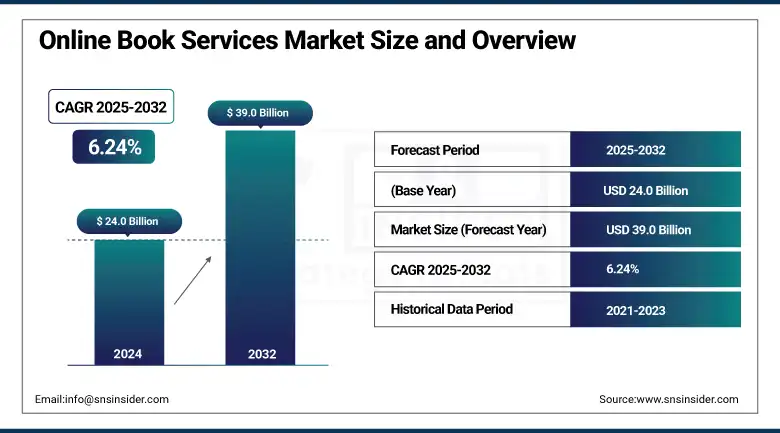

The Online Book Services Market size was valued at USD 24.0 billion in 2024 and is expected to reach USD 39.0 billion by 2032, growing at a CAGR of 6.24% during 2025-2032.

The online book services market growth is driven by factors, such as growing digitalization in the reading habits of consumers, along with increasing smartphone ownership and increasing acceptance of more portable forms of reading on the go. The rise of e-books, audiobooks, and subscription models is changing how readers and students are consuming literary and textbook content. The growth of internet access is beneficial to the market, along with cloud storage or AI-driven recommendation systems.

To Get more information On Online Book Services Market - Request Free Sample Report

Major players including Amazon Kindle, Audible, and Scribd are changing design and content. The online book services market analysis shows that emerging markets show a promising potential as digital infrastructure improves. Furthermore, the growing penetration of digital libraries by educational institutions also continues to fuel the demand. The online book services market trends include reading through voice, multilingual book content, and personalized book recommendations. It is a pivotal sector of the digital content economy and is projected to maintain progress, moving toward top-tier CAGR leading up to 2032.

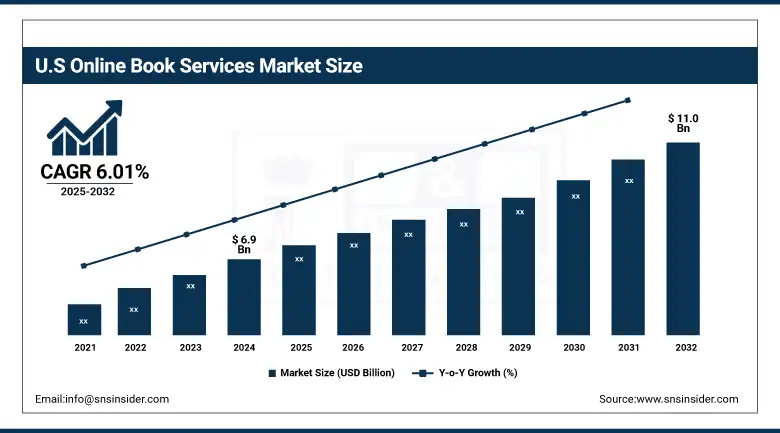

The U.S. online book services market was worth USD 6.9 billion in 2024 and is anticipated to be USD 11.0 billion by 2032, growing at a 6.01% CAGR over 2025-2032. The growth is attributable to increase in digital content consumption, the proliferation of subscription-based models, and accelerated AI-driven recommendation engines to personalize content. The market is further driven by rising mobile device use and the transition to digital learning.

Market Dynamics:

Drivers:

-

Increased Demand for On-the-Go Reading Drives the Growth of Online Book Platforms by Enhancing User Convenience

The online book services market is primarily driven by the growing preference for digital platforms owing to the convenience, portability, and quick access they offer. With the growing use of smartphones, tablets, and e-readers, readers are transitioning from the feeling of physical books to e-books and audiobooks. The capacity to carry thousands of books in a single device and read whenever has accelerated digital consumption immensely. The recent launch of subscription services that give access to large libraries for a monthly fee is also becoming more prevalent. Cloud storage and custom-made AI recommendations also improve customer experience and assist in retention and frequency of use in the market.

For instance, the number of e-book consumers worldwide is projected to reach 1 billion in 2024, up from 900 million in 2022. This growth is driven by factors, such as increased convenience, greater accessibility, and the availability of subscription models that encourage e-book reading.

Restraints:

-

Widespread Illegal Downloads Reduce Revenue and Deter Publishers from Fully Embracing Digital Formats

The online book services market faces a key restraint owing to digital piracy. Piracy of e-books and audiobooks results in huge revenue loss for publishers and authors. Since the rise of digital rights management technologies, access to pirated media content is far too easy online. As a result, it pushes content creators from fully migrating to online, with damage to market growth. Another factor is questions about originality when it comes to copyright laws and inconsistent enforcement by certain regions. This leads to trust and ethical challenges for both consumers and providers which resulting in not being able to unlock the full potential of the online book market.

In 2023, there were over 63.6 billion visits to piracy websites, indicating the massive scale of unauthorized access to digital content.

Opportunities:

-

Adoption of AI and Voice Tools Enhances Personalization and Accessibility, Attracting More Users

Pairing AI and voice technology presents a real growth market. The use of AI makes it a great tool for improving the range of engagement with users, as the AI provides book recommendations to the users that suit their reading history and preferences. On the other hand, audiobook platforms are integrating with voice assistants such as Alexa, Siri, and Google Assistant for hands-free, interactive reading. Such techs not only help visually impaired users to access the content but also provide more ways for multitasking readers. The increased adoption of smart home devices will offer companies the opportunity to capitalize on AI and voice interfaces to create unique and compelling experiences that will appeal to wider audiences in education and entertainment.

A significant 70% of users now expect personalized responses from AI-driven assistants, reflecting a growing demand for tailored content and interactions.

Challenges:

-

Difficult Content Licensing Limits Platform Offerings and Slows Global Market Expansion

Online book providers struggle with not only securing licenses for content but also adhering to publisher restrictions. Global rights can be hard to negotiate and expensive, particularly with dozens of publishers and territories. Many publishers remain cautious in licensing any premium or high-value content to digital platforms due to the fear of revenue cannibalization or piracy. With a restrictive licensing model, it limits usage, sharing, or even storage, which severely reduces the willingness for users to use it. And they are also what slow content expansion and innovation from the players who face these barriers, policing the competitiveness of the landscape by deterring smaller players trying to enter or grow in the market.

Segmentation Analysis:

By Product:

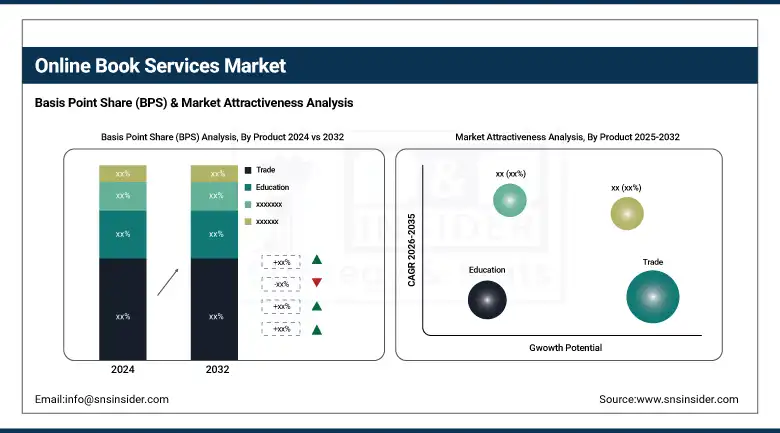

The Trade segment dominated the market and accounted for 65% of the online book services market share in 2024. High consumer demand for fiction, non-fiction, and bestsellers via digital formats made the largest contribution to the market. Smartphone usage, the flexi-subscription model, and AI-based personalized content are the booster pump for the growth. This category, which covers expanding digital libraries and the global reach of authors, is likely to continue robust engagement and steady growth right through 2032 among leisure and casual digital consumers.

For instance, companies including Pearson have reported a 6% revenue growth in their higher education division in Q1 2025, benefiting from the rising demand for AI-embedded learning resources.

Due to the growing trend of e-learning platforms and digital curricula, the education segment is estimated to record the fastest growth rate during the forecast period. The demand can be attributed to the trend of remote learning, government initiatives focusing on digital education, and AI-based adaptive learning tools. As more tablets and e-readers become integrated into classrooms, this segment is anticipated to register strong growth, especially in emerging markets and K–12 and higher education.

Regional Analysis:

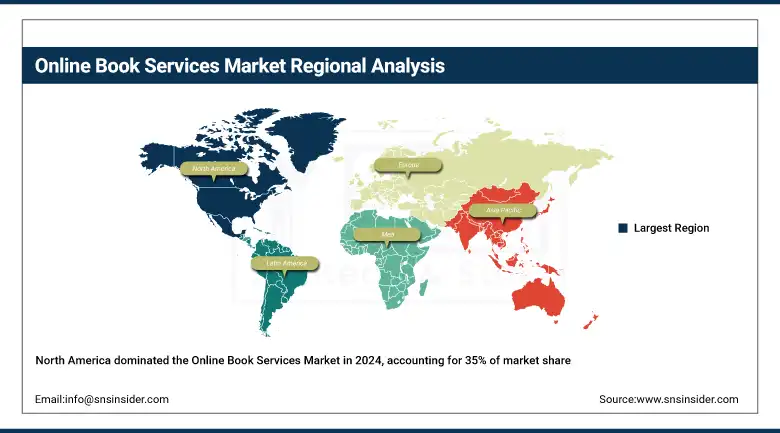

North America dominated the online book services market in 2024 and accounted for 35% of the revenue share due to their high level of digital literacy, prevalence of smartphones, and a strong infrastructure for e-commerce and e-publishing. Availability of content and innovation is further boosted by the presence of leading players, such as Amazon and Apple. Their commercial development will continuously have a dominant factor in the region, along with the factors of the continued demand for audiobooks, integration with educational platforms, and AI-driven personalization for the younger age groups and professional learners from 2032.

Get Customized Report as per Your Business Requirement - Enquiry Now

The fastest CAGR is anticipated in Asia Pacific, which is owing to the rapid penetration of the internet, along with the rapidly increasing use of smartphones and the increasing number of digital learning initiatives. Online book consumption is increasing due to government-led educational reforms, rapid expansion of middle-class populations through economic development, and growing demand for multilingual digital content among consumers. Mobile first platforms as well as AI-fueled language tools will be establishing in user entry in most of the countries, particularly India and China, where they are likely to stay as the most symbolic place for the growth regions until 2032.

China is leading the Asia Pacific online book services market owing to high digital penetration, government support for e-learning, and mobile payment adoption. From now through 2032, growth will ramp up as AI-enabled platforms come online, literacy rates rise, and demand for Mandarin web content increases.

For instance, in 2023, China's digital publishing industry generated revenues nearing 1.6 trillion yuan, highlighting the substantial scale and growth of digital content consumption in the country.

Expanding use of e-readers, coupled with a steady demand for multilingual content and a focus on sustainable publishing practices, are all factors driving growth in Europe's online book services market. Expansion by 2032 is also expected to be driven by increased investments into digital education and AI-powered platforms, particularly across Western and Northern European areas with a solid digital foundation.

High rates of digital literacy coupled with widespread consumption of audiobooks and the presence of strong major publishers make the United Kingdom the most important country for the European market. Mobile-first reading trends, coupled with voice-assisted technologies, and the continuous rise in use of online book services within schools and universities, ought to see growth continue through 2032.

Key Players:

The major online book services market companies are Amazon Kindle, Apple Books, Google Play Books, Scribd, Kobo, Audible, Barnes & Noble Nook, OverDrive, Bookmate, Hoopla, and others

Recent Developments:

-

In May 2025, Audible announced plans to implement AI-generated voices for audiobook narration, aiming to broaden global access and streamline production processes.

-

In April 2025, Amazon introduced the “Recaps” feature on Kindle devices, offering readers concise summaries of previous book installments to refresh their memory before continuing a series.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | US$ 24.0 Billion |

| Market Size by 2032 | US$ 39.0 Billion |

| CAGR | CAGR of 6.24 % From 2024 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2024-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Trade, STM, Education) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Amazon Kindle, Apple Books, Google Play Books, Scribd, Kobo, Audible, Barnes & Noble Nook, OverDrive, Bookmate, Hoopla and others in the report |

Frequently Asked Questions

Ans- North America region dominated the Online Book Services Market with 35% of revenue share in 2024.

Ans- The Trade segment dominated the market and accounted for 65% of the online book services market share in 2024.

Ans- Increased Demand for On-the-Go Reading Drives the Growth of Online Book Platforms by Enhancing User Convenience.

Ans- The Online Book Services Market size was valued at USD 24.0 billion in 2024 and is expected to reach USD 39.0 billion by 2032.

Ans- The CAGR of the Online Book Services Market during the forecast period is 6.24% over 2025-2032.

Get in Touch