Online Education Market Report Scope & Overview:

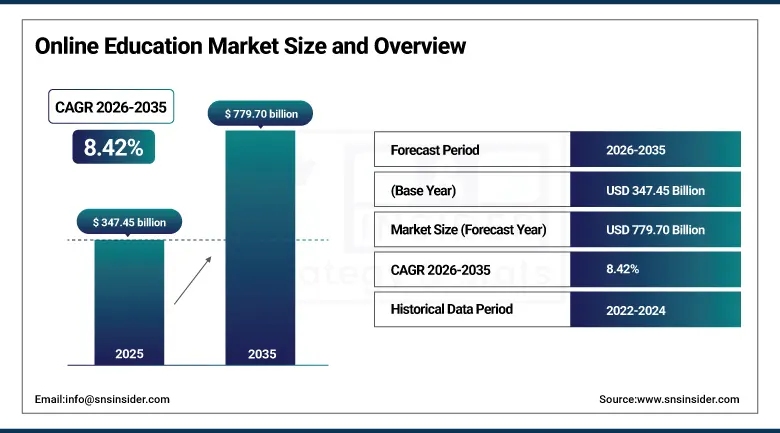

The Online Education Market was valued at USD 347.45 billion in 2025 and is expected to reach USD 779.70 billion by 2035, growing at a CAGR of 8.42% from 2026–2035.

Online education encompasses the full spectrum of technology-mediated learning experiences through which knowledge, skills, and credentials are transferred to learners across geographic and temporal distances without requiring physical co-presence of instructor and student in a dedicated educational facility, ranging from self-paced video-based courses on consumer platforms through synchronous virtual classroom sessions replicating the real-time interaction of physical classroom instruction, from corporate learning management system-delivered compliance training to doctoral-level university programmes offering accredited degrees entirely online. The market's extraordinary scale reflects the progressive recognition across every learning context from K-12 education through adult professional development that digital delivery of educational content provides access, flexibility, cost, and personalization advantages that physical classroom instruction cannot replicate at comparable scale, and that the technology platforms, pedagogical methodologies, and learner experience design capabilities required to deliver effective online education have matured sufficiently to support learning outcomes comparable to or in many contexts superior to equivalent in-person instruction.

The World Economic Forum's estimate that over 1 billion workers will need reskilling by 2030 as AI automation transforms job requirements across every industry sector, combined with the collapse of geographic barriers to education delivery enabled by internet connectivity expansion, creates the most compelling structural growth driver for online education that any market segment could possess, as the scale of the workforce upskilling requirement exceeds the capacity of any physically constrained educational system to address.

Market Size and Forecast

-

Market Size in 2026E: USD 376.72 Billion

-

Market Size by 2035: USD 779.70 Billion

-

CAGR: 8.42% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get more information on Online Education Market - Request Free Sample Report

Online Education Market Trends

-

Rapid commercialization of AI-powered personalized tutoring systems including large language model-based tutoring assistants that can explain concepts in multiple ways calibrated to individual learner comprehension levels, generate unlimited practice problems, provide immediate feedback on written work, and adapt the pacing and depth of instruction dynamically based on demonstrated learner mastery, delivering the personalized instruction that human tutors provide at scale economics impossible through human-delivered tutoring.

-

Growing adoption of micro-credential and digital badge frameworks by employers and accreditation bodies that are beginning to treat skill-specific online learning certifications as valid proxies for traditional degree-based qualification verification in hiring decisions, reducing the traditional credential disadvantage of online learning relative to residential university programmes and expanding the commercial viability of specialized short-form online credentials.

-

Accelerating corporate learning management system adoption and enterprise learning platform investment as organizations recognize that continuous employee upskilling is a strategic competitive requirement rather than a discretionary HR benefit, with AI-powered learning path recommendation and skills gap analysis tools enabling personalized employee development programmes that align individual learning investment with business strategic workforce capability requirements.

-

Rising demand for immersive virtual reality and augmented reality educational experiences that replicate physical hands-on learning in contexts including surgical skills training, industrial equipment operation, architectural visualization, and scientific laboratory experiments that previously could only be delivered through expensive physical facility access and are now accessible through affordable consumer VR headsets paired with professionally developed educational content.

-

Increasing government investment in national online education infrastructure across developing economies, where digital learning platforms are being deployed to supplement chronically under-resourced physical school systems, extend quality educational content access to rural and remote populations, and accelerate workforce reskilling programmes in economies transitioning from manufacturing-dependent to services and technology-oriented employment structures.

The U.S. Online Education Market Outlook

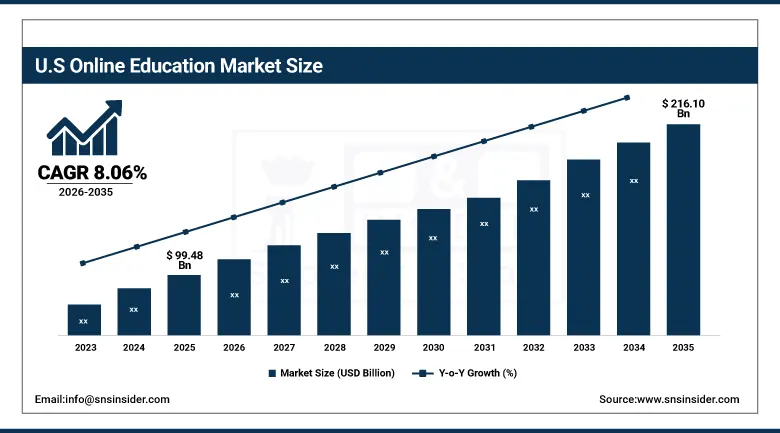

The U.S. Online Education Market was valued at approximately USD 99.48 billion in 2025 and is expected to reach approximately USD 216.10 billion by 2035, growing at a CAGR of 8.06%.

The United States is the world's most commercially developed online education market and the headquarter location of the majority of leading global online education platforms including Coursera, edX (2U), Udemy, Khan Academy, Chegg, and the online programme management divisions of major higher education institutions, collectively making the U.S. the primary innovation Centre for online education business model, technology, and pedagogical development that influences global online education market evolution. The U.S. higher education online programme market has reached a maturity where approximately 37% of graduate students and 20% of undergraduate students were enrolled in exclusively online programmes in 2025, representing a structural shift in how American higher education is delivered that creates sustained demand for learning management system infrastructure, online programme management services, and digital content development.

The U.S. Department of Education's FAFSA financial aid applicability to online degree programmes from accredited institutions, and the progressive acceptance by major employers including Google, IBM, and Apple of skills-based hiring criteria that validate online learning credentials alongside traditional university degrees, are collectively dismantling the institutional barriers that had previously disadvantaged online learners in the credential marketplace.

Online Education Market Segment Analysis

-

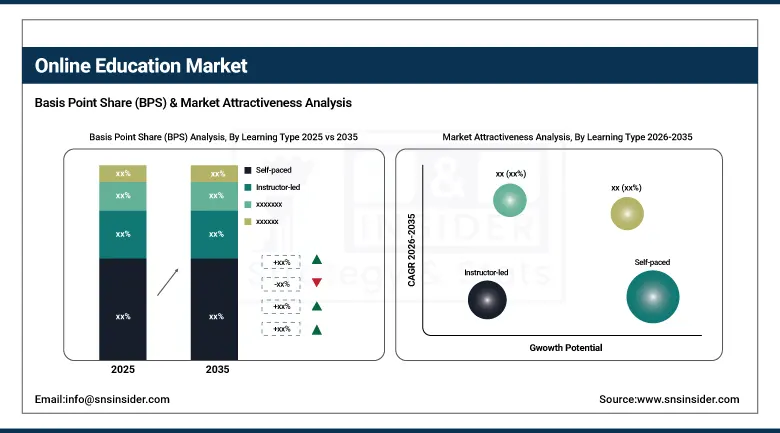

By learning type, Self-paced learning dominated with approximately 42.75% of revenues in 2025 through its alignment with working professionals' schedule flexibility requirements and the massive consumer MOOC market; Hybrid learning is the fastest-growing type at a CAGR of 9.68% as institutions and corporate learning programmes combine the flexibility of asynchronous digital content with the social learning and instructor interaction benefits of scheduled live sessions.

-

By Technology, Learning Management Systems contributed the highest share at approximately 28.43% in 2025 as the foundational infrastructure layer of corporate, higher education, and K-12 online learning programme delivery; AI-powered personalized learning platforms are the fastest-growing technology as adaptive tutoring, content recommendation, and automated assessment systems achieve commercial deployment at scale.

-

By Application, Corporate Training & Professional Development represented the largest revenue segment in 2025 through enterprise learning platform investment across global organizations; K-12 online supplemental education and higher education online degree programmes represent substantial and growing segments, while Skill Development & Certification is the fastest-growing application driven by workforce reskilling urgency.

-

By End User, Working Professionals and Enterprises collectively dominated through corporate learning investment and adult upskilling platform subscriptions; Students represent the largest individual end-user category through K-12 online tutoring, test preparation, and higher education online enrolment.

By Learning Type, Self-paced dominates, hybrid is expected to grow fastest

Self-paced learning retained the dominant position with approximately 42.75% of the online education market in 2025, reflecting its perfect alignment with the primary motivations driving online education adoption among the working professional segment that represents the highest-value paying customer for online learning platforms, where schedule flexibility to complete coursework during commute times, lunch breaks, evenings, and weekends without fixed class time commitments is the single most cited reason for choosing online over in-person learning alternatives.

Hybrid learning is the fastest-growing type at a CAGR of 9.68% through 2035, as both academic institutions and corporate learning departments are discovering that pure asynchronous self-paced delivery optimizes convenience but compromises completion rates, social learning, and the complex collaborative skill development that scheduled instructor-led interaction provides, creating demand for hybrid models that blend recorded instructional content delivery with regular live session check-ins, peer collaboration projects, and instructor office hours that preserve the flexibility advantages of digital delivery while restoring the social and accountability dimensions of learning that improve completion and outcome quality.

By Application, Corporate training dominates, skill development & certification is expected to grow fastest

Corporate Training and Professional Development retained the dominant application position in 2025, as the global enterprise learning management system market combined with the online professional development platform subscriptions that major corporations maintain for their workforces collectively represent the largest single spending category within the online education ecosystem. The convergence of AI-powered skills assessment, personalized learning path recommendation, and continuous microlearning content delivery is transforming corporate learning from a scheduled event-based activity into a continuous embedded workflow capability where employees receive targeted learning recommendations based on their current role requirements, demonstrated skill gaps, and career development objectives without requiring deliberate schedule allocation to formal learning activities.

Skill Development and Certification is the fastest-growing application as the structural labor market disruption driven by AI automation, green energy transition, and digital technology adoption across all industries is creating an urgent and commercially visible reskilling requirement that online learning platforms are uniquely positioned to address at the speed, scale, and cost point that the magnitude of the transition demands. Professional certification programmes in cloud computing, cybersecurity, data science, AI development, project management, and digital marketing delivered by platforms including AWS Training, Google Career Certificates, Coursera Professional Certificates, and Udemy Business are achieving commercial scale as employers accept these credentials as valid evidence of job-relevant skills alongside traditional academic qualifications.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

86.2% |

|

Europe |

United Kingdom |

22.4% |

|

Asia Pacific |

China |

43.7% |

|

Middle East & Africa |

Saudi Arabia |

28.3% |

|

Latin America |

Brazil |

42.8% |

North America Online Education Market Insights

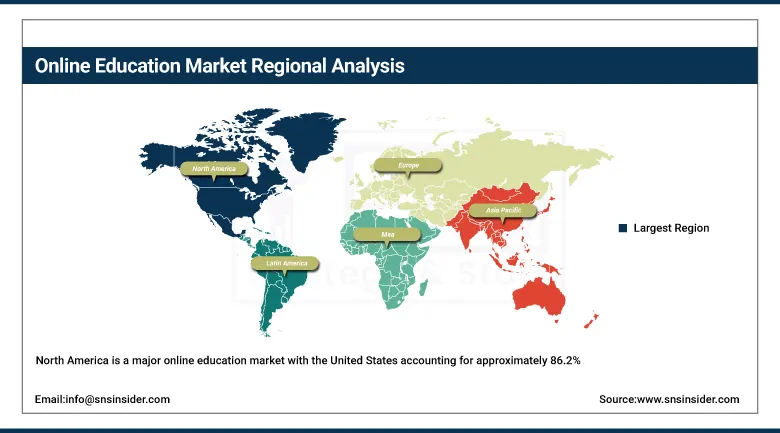

North America is a major online education market with the United States accounting for approximately 86.2% of North American revenues as the world's most commercially developed online learning ecosystem. The region's market characteristics reflect extremely high broadband penetration enabling seamless video-based learning, the world's largest population of employer-funded corporate learners creating substantial enterprise learning platform investment, an established online higher education market where accredited online degree programmes from state and private universities serve millions of enrolled students, and the concentration of global online education platform headquarters creating innovation advantages in AI tutoring, adaptive learning, and content personalization technology.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Online Education Market Insights

Europe is a sophisticated online education market characterised by strong government investment in national digital education infrastructure through programmes including the European Education Area initiative, high employer participation in workplace learning programmes driven by skills shortage responses across the EU's manufacturing, technology, and healthcare sectors, and mature consumer online learning adoption across professional upskilling, language learning, and hobby education categories that sustain large individual subscription revenue bases for platforms including Babbel, Duolingo, and LinkedIn Learning's European user community. The United Kingdom accounts for approximately 22.4% of European online education revenues through its combination of a world-renowned distance learning heritage anchored by the Open University, strong EdTech startup ecosystem in London, and high corporate learning investment across the financial services, professional services, and technology sectors that represent the UK's largest employment categories.

Asia Pacific Online Education Market Insights

Asia Pacific is simultaneously the largest and fastest-growing regional online education market, driven by the extraordinary demographic advantage of the world's largest school-age and working-age populations in China, India, Indonesia, and the ASEAN nations, combined with extraordinarily high cultural prioritization of educational achievement and professional credential acquisition that makes educational spending a relatively recession-resistant consumer investment category across Asian markets. China accounts for approximately 43.7% of Asia Pacific online education revenues through its combination of a 1.4 billion population with deep cultural investment in educational advancement, the world's most competitive corporate environment creating intense demand for professional skill differentiation, and the most active online education investment ecosystem globally that has produced companies including VIPKID, Yuanfudao, and Zuoyebang with valuations exceeding multiple billions of dollars despite the Chinese government's 2021 regulations on for-profit K-12 tutoring that restructured but did not eliminate the massive demand for supplemental educational support.

MEA & Latin America Online Education Market Insights

The Middle East and Africa and Latin America represent high-growth online education markets where the combination of young demographics with the world's largest proportions of school-age and early-career populations, rapidly expanding smartphone and internet penetration enabling mobile-first learning access, and chronic undersupply of quality physical educational infrastructure creating strong demand for digital alternatives collectively create the structural conditions for above-average online education adoption growth. Saudi Arabia leads MEA online education revenues at approximately 28.3% of regional revenues through Vision 2030's explicit commitment to human capital development through digital education, the National Center for e-Learning's government-funded online learning platform infrastructure, and the high female labor force participation growth aspiration that online professional development learning supports. Brazil leads Latin American revenues at approximately 42.8% through its large population, the established consumer culture of EaD (Edu cacao a distance) distance learning that predates digital platforms, and the active Brazilian EdTech ecosystem including Duolingo's large Brazilian user base and local platforms including Decomplicate, Empirics, and Gran Crusos.

Market Dynamics

Growth Drivers: Rising AI-driven workforce reskilling needs, growing online learning adoption, and AI-powered personalized education are driving market growth.

The primary structural growth drivers for the online education market are the extraordinary scale of the workforce reskilling requirement created by AI automation's transformation of job requirements across every industry sector, where the World Economic Forum's estimate that over 1 billion workers will need reskilling by 2030 creates a commercially addressable learning demand that vastly exceeds the capacity of any physically constrained educational delivery system and that online platforms are uniquely positioned to address at the necessary speed, geographic reach, and cost point. Simultaneously, the integration of generative AI tutoring systems into online learning platforms is resolving the historically most significant quality limitation of self-paced online learning, where learners encountering conceptual difficulties had no access to responsive expert guidance between scheduled instructor contact points, by providing always-available AI tutors that can explain, re-explain, and adapt explanations to individual learner comprehension levels with infinite patience and at zero marginal cost per interaction.

Restraints: Low course completion rates, limited digital access, and employer skepticism toward some online certifications are restraining market growth.

A significant restraint on the online education market is the well-documented completion rate disadvantage of self-paced online learning relative to structure in-person or synchronous online instruction, where industry-wide completion rates for free MOOC courses consistently fall below 10% and even for paid professional development courses frequently remain below 50%, reflecting the motivational, accountability, and social learning dimensions of educational engagement that digital platforms have historically struggled to replicate at the quality of physical classroom environments. The digital divide representing persistent gaps in broadband connectivity quality, device access, and digital literacy skills across lower-income, older, and rural populations limits the online education market's ability to serve the most educationally underserved populations who could benefit most from flexible digital learning access but whose technological constraints and digital capability gaps prevent full participation in online learning environments.

Opportunities: AI-powered tutoring, customized corporate learning programs, and government workforce reskilling initiatives are creating significant market opportunities.

The commercialization of AI tutoring systems that provide genuinely responsive, personalized instructional support at the quality of expert human tutoring for any learner at any time without the cost constraints that limit human tutoring access to affluent consumer segments represents the most transformative educational equity and market expansion opportunity in the online education landscape, as demonstrated AI tutoring effectiveness can convert the massive informal interest in online learning evident in platform registration statistics into genuine learning completion and credential attainment outcomes that justify both individual and enterprise investment in online programme subscription. Government workforce reskilling programme procurement, where national governments are increasingly commissioning large-scale online learning platform deployments to address structural unemployment resulting from industrial transitions, represents a new high-volume institutional procurement channel that is expanding online education market revenue beyond the commercial enterprise and individual consumer segments that have historically dominated platform revenue.

Recent Developments:

-

2025: Coursera announced expanded AI-powered learning assistant capabilities across its platform, deploying a large language model-based course guide that provides personalized explanation, practice problem generation, and progress feedback within course learning interfaces, reporting early user engagement data showing 40% improvement in weekly active learning time among users who engaged with the AI assistant compared with non-assisted peers.

-

2025: LinkedIn Learning expanded its AI-powered skills assessment and learning path recommendation system to enterprise clients, enabling HR managers to identify company-wide skills gaps relative to strategic business objectives and automatically generate personalized learning plans for each employee that align their individual development priorities with organizational capability requirements.

-

2025: Google expanded its Google Career Certificates programme with new AI, cybersecurity, and data analytics credentials designed in direct collaboration with major employer partners who commit to considering certificate holders as qualified candidates, demonstrating the employer partnership model that is progressively legitimising online skill credentials in corporate hiring processes.

Online Education Market Key Players are:

-

Coursera Inc.

-

edX (2U Inc.)

-

Udemy Inc.

-

LinkedIn Learning (Microsoft)

-

Khan Academy

-

Chegg Inc.

-

Pluralsight

-

Skillshare

-

MasterClass

-

Duolingo Inc.

-

Byju's

-

Simplilearn

-

Udacity Inc.

-

FutureLearn

-

Articulate Global LLC

-

D2L Corporation

-

Blackboard Inc.

-

Instructure (Canvas)

-

Cornerstone OnDemand

-

SAP SuccessFactors Learning

Online Education Market Report Scope

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 347.45 Billion |

| Market Size by 2035 | USD 779.70 Billion |

| CAGR | CAGR of 8.42% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Learning Type (Self-paced, Instructor-led, Hybrid) • By Technology (Learning Management Systems, AI-powered Platforms, Virtual Classrooms, Mobile Learning, Others) • By Application (K-12 Education, Higher Education, Corporate Training & Professional Development, Skill Development & Certification, Others) • By End User (Students, Working Professionals, Enterprises, Government) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Coursera Inc., edX (2U Inc.), Udemy Inc., LinkedIn Learning (Microsoft), Khan Academy, Chegg Inc., Pluralsight, Skillshare, MasterClass, Duolingo Inc., Byju's, Simplilearn, Udacity Inc., FutureLearn, Articulate Global LLC, D2L Corporation, Blackboard Inc., Instructure (Canvas), Cornerstone OnDemand, and SAP SuccessFactors Learning. |

Frequently Asked Questions

Asia Pacific dominated the Online Education Market in 2025, driven by the world's largest learner populations in China, India, and Southeast Asia.

Self-paced learning dominated with approximately 42.75% of revenues in 2025.

Workforce reskilling urgency created by AI automation transforming job requirements across every industry combined with AI-powered personalization improving online learning outcomes and the collapse of geographic barriers to quality educational content access through internet connectivity expansion.

The Online Education Market was valued at USD 347.45 billion in 2025.

The Online Education Market is expected to grow at a CAGR of 8.42% from 2026 to 2035.

Get in Touch