Organoids and Spheroids Market Report Scope & Overview:

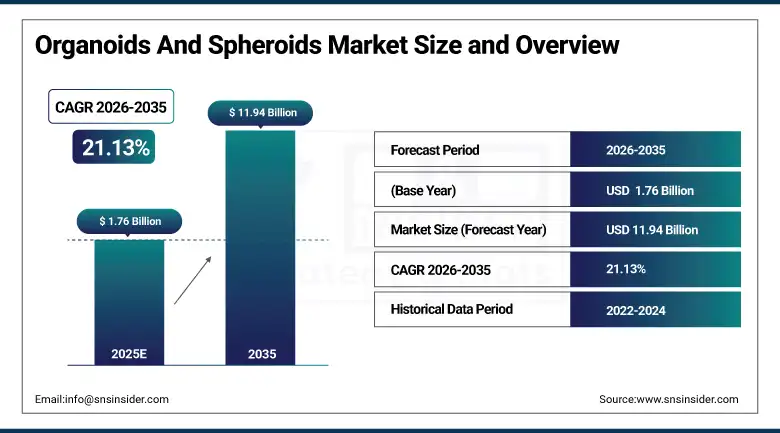

The Organoids and Spheroids Market size was valued at USD 1.76 billion in 2025 and is expected to reach USD 11.94 billion by 2035, growing at a CAGR of 21.13% over the forecast period of 2026-2035.

The global organoids and spheroids market is expanding due to the rising demand for advanced three-dimensional (3D) cell cultures. The two-dimensional cell cultures are not able to show the complex interactions between the cells. This has led to the adoption of organoid and spheroid technologies to conduct research. The rise of precision medicine, regenerative medicine, and stem cell research is also contributing to the growing adoption of these models in biotechnology companies, pharmaceutical companies, and research institutions.

Increased investments in life science research, advances in translational medicine, and the prevalence of chronic diseases such as cancer, neurological diseases, and liver diseases are also contributing factors. Organoids and spheroids allow for the development of in vitro organ-like structures. They help in understanding diseases and therapeutic responses. The integration of technologies such as CRISPR gene editing, high-content imaging, and AI-based analysis is also helping in the adoption of these technologies in life science research.

In March 2025, several leading pharmaceutical companies reported that organoid-based screening platforms reduced early-stage drug development timelines by nearly 30%, demonstrating the growing importance of 3D cell culture models in accelerating therapeutic discovery and reducing research costs.

Organoids and Spheroids Market Size and Forecast:

-

Market Size in 2025: USD 1.76 Billion

-

Market Size by 2035: USD 11.94 Billion

-

CAGR: 21.13% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Organoids And Spheroids Market - Request Free Sample Report

Organoids and Spheroids Market Trends:

-

Increasing adoption of organoid models for cancer research and personalized oncology treatment strategies.

-

Integration of stem cell technologies and CRISPR gene editing to create more physiologically accurate organoid systems.

-

Growing use of spheroid culture models for high-throughput drug screening and toxicity testing in pharmaceutical R&D.

-

Rising collaborations between biotechnology companies and academic institutes to develop patient-derived organoid biobanks.

-

Expansion of microfluidic organ-on-chip platforms combining organoids with advanced tissue engineering technologies.

-

Growing investment in regenerative medicine research using organoid systems to study tissue repair and organ development.

-

Advancements in imaging and automated cell culture technologies enabling large-scale production of spheroids and organoids.

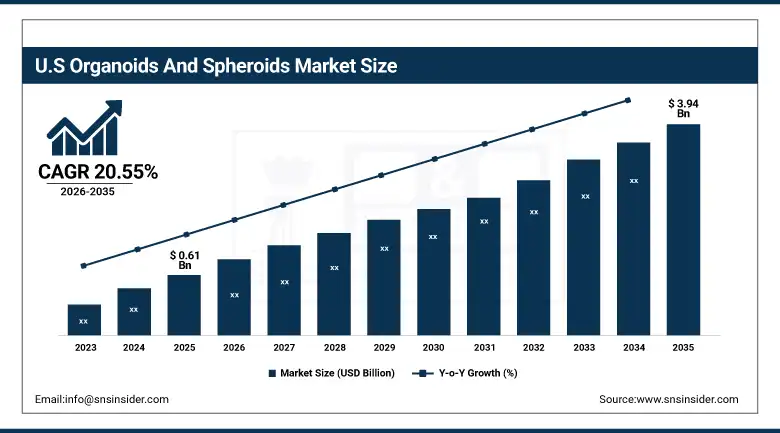

The U.S. Organoids and Spheroids market was valued at 0.61 billion in 2025 and is expected to grow at a CAGR of 20.55% from 2026-2035 to reach 3.94 billion by 2035. The U.S. market maintains a strong position in the overall market due to the strong presence of biotechnology infrastructure, high research funding, and the presence of key pharmaceutical and life science organizations. The U.S. market is witnessing increased federal funding for stem cell research activities. The country is also witnessing high collaboration between academic centers and biotech startups. The adoption of latest 3D cell culture technology is also high in the U.S. The U.S. market is witnessing increased clinical research activities for personalized medicine and precision oncology, which is further contributing to the adoption of organoids and other 3D cell cultures for studying diseases.

Organoids and Spheroids Market Growth Drivers:

-

Rising Demand for Advanced 3D Cell Culture Models Driving Market Growth

The growing demand for advanced three-dimensional cell culture systems is a major driver of the organoids and spheroids market. Conventional two-dimensional cell culture models have limitations in replicating complex human tissue architecture, making them less effective for disease modeling and drug screening. Organoids and spheroids provide a more physiologically relevant environment where cells interact and develop structures similar to human organs.

These models are increasingly used by pharmaceutical companies in early drug discovery to evaluate drug toxicity, efficacy, and biological activity in environments that mimic human physiology. As companies work to reduce drug failure rates in clinical trials, the adoption of organoid and spheroid platforms has become an important part of preclinical research. Growth in cancer research, along with increasing investment in stem cell research and regenerative medicine, continues to expand the use of these advanced cell culture technologies.

For example, in February 2025, a multinational pharmaceutical company reported that patient-derived tumor organoids enabled researchers to identify the most effective chemotherapy combinations for specific cancer types with nearly 80% predictive accuracy compared with traditional cell models.

Organoids and Spheroids Market Restraints:

-

High Development Costs and Technical Complexity Limiting Market Adoption

In addition to this, the cost factor associated with the maintenance of organoids and spheroids is also considered to be one of the challenges for their implementation. The need for specialized equipment and researchers to develop organoid cultures is also considered to be one of the challenges for their implementation. The results may not be consistent due to the conditions for organoid cultures.

Regulatory uncertainty regarding the use of organoid-based models in clinical decision-making and therapeutic development further limits market expansion. Regulatory authorities are still evaluating their reliability and reproducibility compared with conventional testing systems. Addressing these challenges through improved standardization, automation, and technological innovation will be essential to expand the accessibility and adoption of organoid and spheroid technologies.

Organoids and Spheroids Market Opportunities:

-

Expansion of Personalized Medicine and Precision Oncology Creating Major Market Opportunities

The increasing trend of personalized medicine and precision oncology is also helping this market grow. Patient-derived organoids can be used for understanding the biology of cancer and developing personalized medicine approaches based on the patient’s genetic profile and condition.

The pharmaceutical industry is also using organoid technology for drug testing on a patient-specific basis before clinical trials are carried out. This helps in selecting candidates for clinical trials, resulting in cost savings for drug development. The integration of genomic sequencing into organoid technology is also useful for identifying mutations that are specific to disease types. In addition, organoid technology in conjunction with other technologies, including AI-based drug screening technology, is also expected to contribute to market growth.

For example, in April 2025, researchers developed patient-derived intestinal organoids that successfully predicted treatment responses in inflammatory bowel disease patients, highlighting the transformative role of organoid models in advancing precision medicine.

Organoids and Spheroids Market Segment Analysis:

-

By type, organoids accounted for the largest share of approximately 57.42% in 2025, while the spheroids segment is anticipated to register the fastest growth at a CAGR of 22.16% during the forecast period.

-

By application, drug toxicity and efficacy testing dominated the market with a share of about 28.37% in 2025, whereas personalized medicine is projected to grow at the highest CAGR of 23.41%.

-

By end use, biotechnology and pharmaceutical industries held the largest revenue share of nearly 52.64% in 2025, while academic and research institutes are expected to expand at the fastest CAGR of 21.95%.

By Type, Organoids Dominate the Market, While Spheroids Exhibit Strong Growth Potential

The organoids segment held the largest market share in 2025. The organoids segment is expected to grow at a high rate in the near future. Organoids mimic complex tissue architecture and cellular processes observed in human organs. Organoids are useful in biomedical research and drug development. Neural organoids, hepatic organoids, and intestinal organoids are commonly used in neuroscience research, liver research, and gastrointestinal diseases. The organoids segment allows for the study of organ development, genetic diseases, and cancer.

Spheroids are expected to grow rapidly during the forecast period, owing to their increasing use in high-throughput drug screening tests and cancer research. The multicellular tumor spheroids mimic the tumor microenvironment, which makes them a more realistic system for drug response studies than the conventional cell culture system. The development of microfabrication techniques, automated cell culture systems, and microplate spheroid formation techniques are helping to develop consistent spheroid systems for drug testing.

By Application, Drug Toxicity & Efficacy Testing Leads the Market

The drug toxicity and efficacy testing segment accounted for the largest market share in 2025. This is because the market for organoid and spheroid systems is increasing due to the need for pre-clinical testing models in pharmaceutical research. This is because organoid and spheroid systems enable pharmaceutical companies to study the interactions between drug candidates and human tissue before conducting clinical trials. This helps in ensuring the safety and efficacy of drugs.

Personalized medicine is expected to grow the fastest during the forecast period. This is because the focus is on individualized treatment plans. Patient-derived organoids help clinicians determine the response of a patient to a drug, especially in oncology and rare genetic disorders. This helps in the development of targeted treatment plans, thus improving clinical outcomes while eliminating ineffective treatment plans.

By End Use, Biotechnology and Pharmaceutical Industries Dominate the Market

Biotechnology and pharmaceutical industries accounted for the highest share of the organoids and spheroids market in 2025 due to research activities carried out for drug discovery, toxicology studies, and identification of biomarkers. The industries require cutting-edge cell culture technology to speed up their R&D process while minimizing drug development expenses. The competitive environment of pharmaceutical industries to introduce novel drugs also contributed to the increased adoption of organoid and spheroid technology.

Academic and research institutes are expected to register the fastest growth rate during the forecast period, owing to the increasing research and studies related to stem cell research and tissue engineering within academic institutions. Various government funding programs, research collaborations, and interactions with biotechnology firms are supporting the development of novel organoid systems for the study of complex diseases and biological processes.

Organoids and Spheroids Market Regional Highlights:

North America Organoids and Spheroids Market Insights:

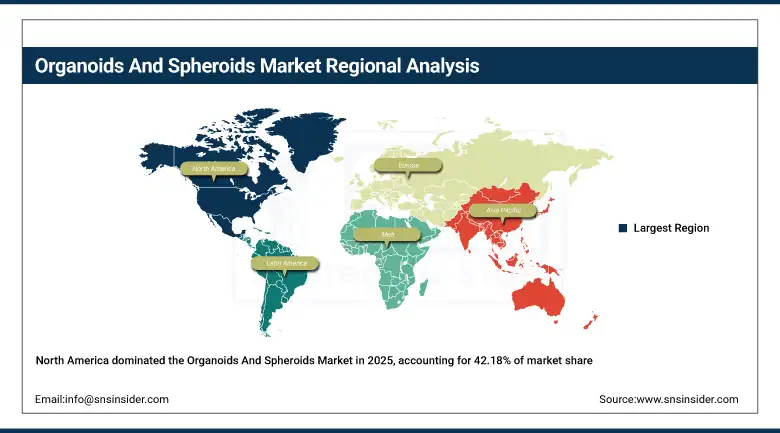

North America dominated the world market for organoids and spheroids in 2025, contributing 42.18% to the overall revenue. The region offers a robust biotech environment and high research funding. Pharmaceutical giants are investing in cutting-edge cell culture technology. The US is at the forefront of the North American market for organoids and spheroids due to high biomedical research infrastructure and a surge in clinical research activities. There is a high level of cooperation between academic centers and biotech start-ups.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Organoids and Spheroids Market Insights:

Europe is the second-largest market for organoids and spheroids, where well-funded research activities are carried out in regenerative medicine and stem cell biology. Countries such as Germany, the UK, and the Netherlands are spending significantly on organoid-based disease modeling and drug discovery research. The government is also taking initiatives to fund innovations in biotechnology and other scientific collaborations in this region.

Asia Pacific Organoids and Spheroids Market Insights:

The Asia Pacific market is expected to grow at the fastest rate during the forecast period with a CAGR of 22.87%. The growth of biotechnology industries is one of the key drivers for the growth of the market. The demand for advanced drug discovery technologies is also driving the growth of the market. Countries like China, Japan, Korea, and India are improving their life sciences research infrastructure. Additionally, investments are also being made in stem cell research activities.

Latin America and Middle East & Africa Organoids and Spheroids Market Insights:

The markets in Latin America and the Middle East & Africa are gradually expanding due to increasing investment in biomedical research infrastructure and growing collaboration with international biotechnology companies. The adoption of advanced research technologies in universities and clinical laboratories is expected to contribute to steady market growth in these regions over the coming decade.

Organoids and Spheroids Market Competitive Landscape:

Thermo Fisher Scientific (founded in 2006) is a global leader in life sciences tools and services and provides a wide range of organoid culture systems, reagents, and 3D cell culture platforms designed to support advanced biomedical research and drug discovery applications.

-

In January 2025, the company introduced a new organoid culture kit designed to accelerate patient-derived tumor organoid development for oncology drug screening.

Corning Incorporated (founded in 1851) is a leading provider of laboratory consumables and 3D cell culture technologies, offering specialized microplates and scaffolds for spheroid and organoid research applications.

-

In October 2024, the company expanded its 3D cell culture portfolio with advanced spheroid microplates designed for high-throughput screening workflows.

STEMCELL Technologies (founded in 1993) develops specialized cell culture media and reagents for organoid research, supporting scientists worldwide in stem cell biology and regenerative medicine studies.

-

In March 2025, the company launched a new intestinal organoid culture system designed to improve long-term organoid growth and reproducibility.

Organoids and Spheroids Market Key Players:

-

Thermo Fisher Scientific

-

Corning Incorporated

-

STEMCELL Technologies

-

Merck KGaA

-

Lonza Group

-

PromoCell GmbH

-

Greiner Bio-One International

-

3D Biotek

-

InSphero AG

-

HUB Organoids

-

DefiniGEN

-

AMS Biotechnology

-

PeproTech

-

Takara Bio

-

Cellesce Ltd

-

Axol Bioscience

-

Reprocell Inc.

-

ScienCell Research Laboratories

-

TissUse GmbH

-

CN Bio Innovations

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.76 Billion |

| Market Size by 2035 | USD 11.94 Billion |

| CAGR | CAGR of 21.13% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Organoids, Spheroids) • By Application (Developmental Biology, Personalized Medicine, Regenerative Medicine, Disease Pathology Studies, Drug Toxicity & Efficacy Testing) • By End-use (Biotechnology and Pharmaceutical Industries, Academic & Research Institutes, Hospitals and Diagnostic Centers) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Thermo Fisher Scientific, Corning Incorporated, STEMCELL Technologies, Merck KGaA, Lonza Group, PromoCell GmbH, Greiner Bio-One International, 3D Biotek, InSphero AG, HUB Organoids, DefiniGEN, AMS Biotechnology, PeproTech, Takara Bio, Cellesce Ltd, Axol Bioscience, Reprocell Inc., ScienCell Research Laboratories, TissUse GmbH, CN Bio Innovations |

Get in Touch