Pantograph Charger Market Report Scope & Overview:

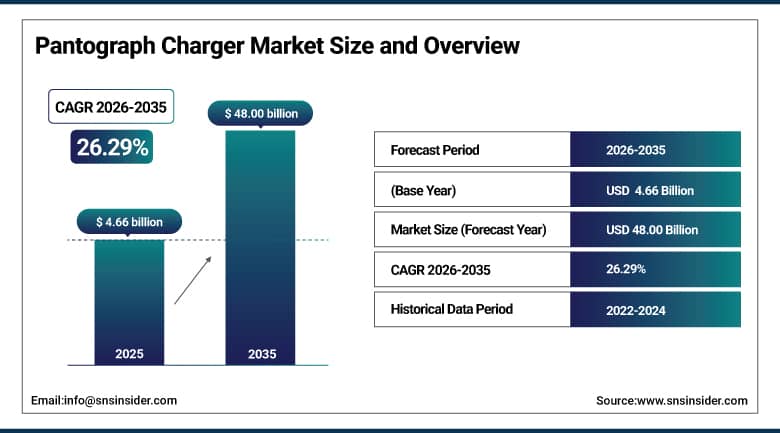

The Pantograph Charger Market size was valued at USD 4.66 Billion in 2025 and is projected to reach USD 48.00 Billion by 2035, growing at a CAGR of 26.29% during 2026-2035.

The Pantograph Charger Market is among the highest-growth segments within the broader electric vehicle charging infrastructure landscape, driven by the large-scale electrification of public transit bus fleets, tram networks, and rail systems across Europe, Asia Pacific, and North America where governments and transit authorities are committing to zero-emission public transport timelines that require depot and on-route charging infrastructure investment at a scale without historical precedent.

Market Size and Forecast:

-

Market Size in 2025 - USD 4.66 Billion

-

Market Size by 2035 - USD 48.00 Billion

-

CAGR - 26.29% From 2026 to 2035

-

Base Year - 2025

-

Forecast Period - 2026-2035

-

Historical Data - 2022-2024

To Get More Information On Pantograph Charger Market - Request Free Sample Report

Key Pantograph Charger Market Trends

-

Increasing deployment of ultra-fast pantograph chargers supporting rapid charging for electric buses in urban transit networks.

-

Growing integration of automated overhead charging systems improving operational efficiency and reducing manual intervention in fleet operations.

-

Rising adoption of high-power charging infrastructure exceeding 350 kW to support heavy-duty electric vehicle fleets.

-

Expansion of smart charging technologies enabling real-time monitoring, load management, and energy optimization across charging networks.

-

Increasing investments in sustainable public transport infrastructure driving widespread installation of pantograph charging systems globally.

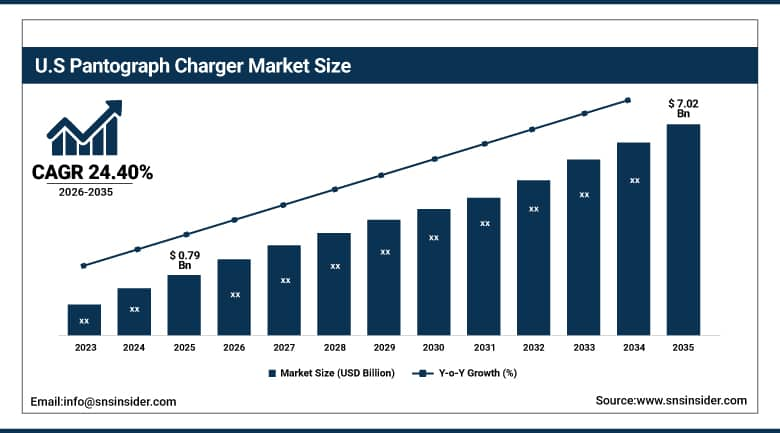

The U.S. Pantograph Charger Market size was valued at USD 0.79 Billion in 2025 and is projected to reach USD 7.02 Billion by 2035, growing at a CAGR of 24.40% during 2026-2035. The U.S. market is the dominant national market within North America, with demand generated by urban transit authority electric bus fleet procurement programs in cities including Los Angeles, New York, Chicago, and Seattle, supported by Federal Transit Administration grant programs that subsidize zero-emission bus and associated charging infrastructure investment.

Pantograph Charger Market Growth Drivers:

-

Rapid Electrification of Public Transport Systems Driving Strong Demand for High Power Automated Charging Infrastructure Globally

The market is mainly powered by the increasing electrification of mass transit networks, especially electric buses and transit systems. There have been strict emission standards and financial incentives by governments all around the world in favor of clean mobility solutions, thereby increasing the need for effective charging equipment. The pantograph charger allows quick charging and automation of charging processes, which leads to less time being spent on these activities, improving fleet operations. The rising investments in smart cities and green transportation infrastructure will drive market growth as well.

Pantograph Charger Market Restraints:

-

High Infrastructure Costs and Grid Integration Challenges Limiting Large Scale Deployment of Pantograph Charging Systems Globally

Some of the main constraints include the substantial capital that needs to be invested upfront for setting up the charging system using pantographs, including investments in grid infrastructures and installation expenses. Installation of such systems requires considerable capital, and therefore, small cities and companies find it difficult to invest in them. Besides, it is not easy for companies or utilities to integrate such systems with their existing power grids, particularly in those areas where there is inadequate electrical grid infrastructure.

Pantograph Charger Market Opportunities:

-

Expansion of Electric Bus Fleets and Smart City Initiatives Creating Significant Growth Opportunities for Advanced Charging Solutions

Many opportunities have emerged due to the fast-growing market for electric buses in urban settings around the world. There is a growing trend among governments to invest in smart city projects that involve setting up an automated charging infrastructure. Due to technological advancements in the form of large-capacity batteries and ultra-fast charging technology, the use of pantograph chargers has become more effective. In addition, the growing demand for low-emission vehicles and efforts to improve urban air quality have led to increased demand. Another opportunity involves the involvement of private companies in electric vehicle infrastructure projects.

Pantograph Charger Market Segment Analysis

-

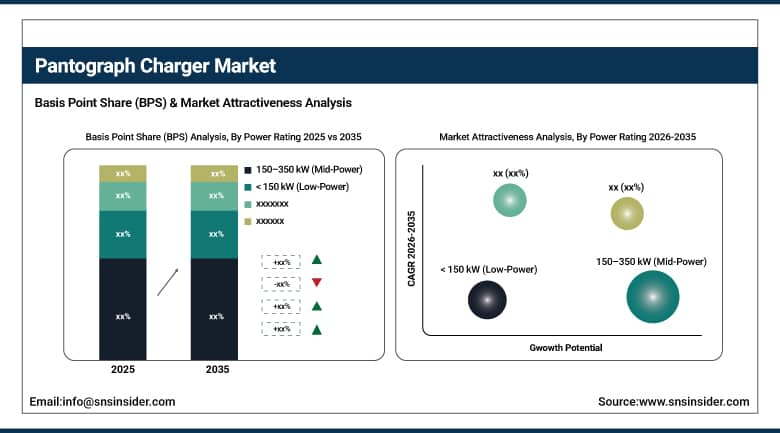

By Power Rating, 150-350 kW (Mid-Power) dominated with 38.27% in 2025, and 350-600 kW (High-Power) is expected to grow at the fastest CAGR of 27.52% from 2026 to 2035.

-

By Charger Type, Roof-Mounted Pantograph Chargers dominated with 32.18% in 2025, and Dual-Arm Pantograph Chargers are expected to grow at the fastest CAGR of 27.57% from 2026 to 2035.

-

By Application, Public Transit Vehicles (Electric Buses/Trams) dominated with 52.63% in 2025, and Commercial EV Fleets (Logistics & Delivery Vehicles) are expected to grow at the fastest CAGR of 28.32% from 2026 to 2035.

-

By End-User, Transit Authorities & Municipal Operators dominated with 57.92% in 2025, and Commercial EV Charging Infrastructure Providers are expected to grow at the fastest CAGR of 27.95% from 2026 to 2035.

By Power Rating, Mid-Power Leads Pantograph Charger Market While High-Power Shows Fastest Growth 2026 to 2035

Medium Power Pantograph Charger is leading in the segment since it offers a good compromise between fast charging, cost, and integration with the grid. It finds wide applications in the urban transport system where medium-fast charging is required during the regular operations of vehicles. In comparison to the former, the latter is growing at a much faster pace since there is a rise in the need for fast charging that ensures minimum vehicle idle time. The high-power pantograph charger is especially useful for electric buses having high passenger capacity.

By Charger Type, Roof-Mounted Pantograph Chargers Lead Pantograph Charger Market While Dual-Arm Systems Set for Fastest Growth 2026 to 2035

The roof-mounted pantograph charger holds its popularity in the global market owing to its wide usage in electric buses and transportation. Such charging system is characterized with automatic, top charging capability without requiring too much involvement from drivers. The dual arm pantograph charger is the most rapidly developing segment of the pantograph charger market thanks to its improved flexibility and better contact stability. This type of charger is mainly used in routes where electric transport operates at high frequency.

By Application, Public Transit Vehicles Lead Pantograph Charger Market While Commercial EV Fleets Show Fastest Growth 2026 to 2035

Pantograph chargers are used mostly by public transport systems, such as electric buses and trams, because of the extensive electrification efforts being done in the urban transport sector. These public transport systems need to use efficient automatic charging solutions in order to be able to function efficiently and keep up with their schedules. Meanwhile, electric fleet vehicles have been seen to be the fastest growing segment within the pantograph chargers industry, owing to the fast growth of the logistics, delivery, and e-commerce industry.

By End-User, Transit Authorities & Municipal Operators Lead and Commercial EV Charging Infrastructure Providers Show Fastest Growth in Pantograph Charger Market 2026 to 2035

Transit operators and city governments lead in the market, being the main users of pantograph charging systems for electrified public transport. Their desire to lower urban pollution levels and increase the efficiency of transit is driving major infrastructure investments. Meanwhile, commercial EV charging infrastructure providers account for the most rapidly expanding user base in the industry, with growing corporate involvement in building the overall ecosystem around EVs. They are developing high-capacity charging infrastructure that would accommodate the emergence of commercial electric vehicle fleets.

Pantograph Charger Market Regional Analysis

North America Pantograph Charger Market Insights

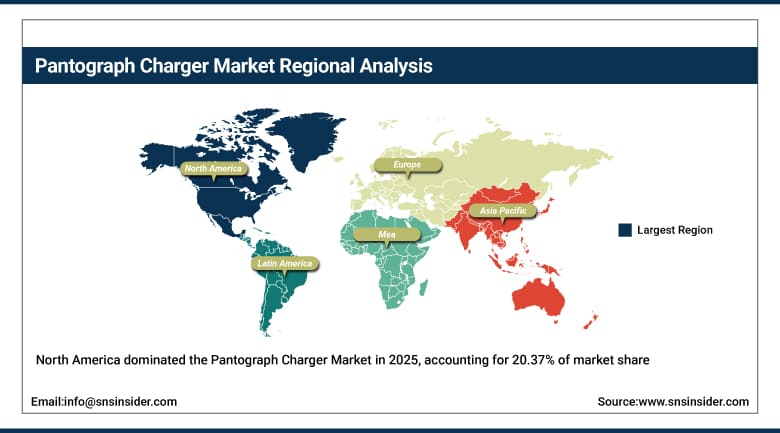

North America held a 20.37% share of the global Pantograph Charger Market in 2025 at USD 0.95 Billion, growing at a CAGR of 24.90% through 2035. The region's market is driven by urban transit authority electric bus fleet procurement programs supported by federal zero-emission bus grant funding, with the Federal Transit Administration's Low or No Emission Vehicle Program and the Infrastructure Investment and Jobs Act creating a sustained funding pipeline for zero-emission transit infrastructure that transit authorities in major U.S. cities are actively drawing on. The U.S. market is in an earlier stage of pantograph charger deployment relative to Europe and China, with most transit agencies having recently committed to fleet electrification timelines rather than having already completed large-scale transitions, meaning that the majority of North American pantograph charger procurement volume is ahead rather than behind in the forecast period.

Get Customized Report as Per Your Business Requirement - Enquiry Now

U.S. Pantograph Charger Market Insights

The United States dominated North America's pantograph charger market at 83.42%, USD 0.79 Billion in 2025. Los Angeles Metro, New York MTA, King County Metro in Seattle, and Chicago CTA are among the largest electric bus procurement programs underway in the U.S. that are generating associated pantograph charging infrastructure demand. U.S.-based charging infrastructure companies including ChargePoint are active in the commercial EV depot charging market and are developing pantograph charging product lines to address the growing demand from logistics and transit fleet operators that manual plug-in systems cannot serve efficiently at scale.

Europe Pantograph Charger Market Insights

Europe held 29.68% at USD 1.38 Billion in 2025, growing at a CAGR of 25.34% through 2035. Europe is the most advanced regional market for pantograph charger deployment in public transit applications, with established electric bus fleet operations in Geneva, Amsterdam, Hamburg, Stockholm, and dozens of other cities providing operational proof points that transit authorities in earlier-stage markets are drawing on to justify their own electrification investments. The EU Clean Vehicles Directive and national zero-emission transport policies in Germany, France, the Netherlands, and Scandinavia are the primary regulatory drivers of continued transit electrification procurement, while the EU's Alternative Fuels Infrastructure Regulation is creating a broader policy framework for electric vehicle charging infrastructure deployment that extends beyond transit into commercial and logistics fleet applications. Siemens, ABB, Heliox, and Ekoenergetyka-Polska are the most significant European pantograph charger manufacturers, with Heliox's Netherlands base and Ekoenergetyka-Polska's manufacturing presence giving the European supply chain a substantial domestic production capability.

Germany Pantograph Charger Market Insights

Germany was the leading national market for pantograph chargers in Europe in 2025, driven by the country's large urban transit bus network operated by Deutsche Bahn subsidiaries and municipal transport operators that are among the most active electric bus fleet procurers in Europe, combined with the presence of Siemens' e-bus charging infrastructure business and a sophisticated domestic industrial EV charging ecosystem that makes Germany both the largest European consumer and a significant producer of pantograph charging technology for transit and commercial vehicle applications.

Asia Pacific Pantograph Charger Market Insights

Asia Pacific is the largest and fastest-growing region at a CAGR of 27.55% through 2035, valued at USD 2.09 Billion in 2025 and projected to reach USD 23.81 Billion by 2035. China is by far the dominant national market within the region and globally, hosting the world's largest installed base of electric buses and the manufacturing infrastructure of CRRC, BYD, and Dalian Luobinsen that produces both the vehicles and the charging systems that power them. India's national electric bus program represents one of the largest single procurement opportunities in the global pantograph charger market for the forecast period, with the government's commitment to deploying a large fleet of electric buses across major cities creating a coordinated vehicle and infrastructure procurement program that international and domestic suppliers are actively competing to supply. Japan and South Korea are deploying pantograph charging infrastructure in rail transit and bus rapid transit applications where their mature public transit systems are being upgraded with electrified rolling stock that requires modern charging infrastructure.

China Pantograph Charger Market Insights

In the Asia Pacific region, the largest consumer of pantograph charger technology is seen in China, owing to its wide scale deployment of electric buses, government backing, advanced electric vehicle infrastructure and presence of leading manufacturers.

Latin America (LATAM) and Middle East & Africa (MEA) Pantograph Charger Market Insights

Latin America was valued at USD 0.15 Billion in 2025 and is growing at a CAGR of 24.88% through 2035, with Chile, Colombia, and Brazil representing the most active national markets for electric bus deployment driven by air quality improvement mandates in major cities and IDB and development bank financing that is making electric bus fleet investment accessible to transit authorities that would not have the budget to finance electrification unilaterally. Santiago, Chile has emerged as a regional reference market for electric bus fleet operations, with one of the largest electric bus fleets in Latin America providing a demonstration of operational viability that other regional cities are drawing on as they develop their own electrification programs. Middle East and Africa was valued at USD 0.09 Billion in 2025 and is growing at a CAGR of 25.69% through 2035, with Gulf state transit investments in metro and electric bus rapid transit systems in Dubai, Riyadh, and Abu Dhabi representing the primary demand sources in a region that is otherwise at an early stage of electric transit infrastructure deployment.

Competitive Landscape for Pantograph Charger Market:

ABB, headquartered in Zurich, Switzerland, is one of the global leaders in pantograph charging systems for electric buses and commercial vehicles, with its TOSA opportunity charging system and OppCharge-compatible depot charging portfolio deployed in transit operations across Europe, the United States, and Asia Pacific.

- In 2024, ABB expanded its pantograph charger product range to include a 600 kW high-power system specifically designed for electric articulated buses and heavy-duty commercial vehicles, addressing growing demand from transit authorities specifying high-capacity vehicles for high-frequency routes where mid-power charging systems had created operational bottlenecks by extending depot charging times beyond available overnight dwell periods.

Siemens, headquartered in Munich, Germany, operates a significant pantograph charging business through its eMobility division, supplying charging systems for electric buses, trams, and light rail vehicles to transit operators across Europe and Asia Pacific. Siemens' integration of pantograph charging hardware with its broader energy management, grid automation, and mobility infrastructure portfolio gives it a differentiated position in large transit authority procurement programs where total system integration from grid connection to vehicle charging optimization is a project requirement that standalone charging hardware suppliers cannot address.

- In 2024, Siemens completed the commissioning of a pantograph charging depot for a major German municipal transit operator, with the installation featuring 24 roof-mounted pantograph charging points at 300 kW each integrated with an energy management system that schedules charging loads to minimize peak demand charges and align high-power charging activity with periods of low grid carbon intensity, delivering both operational cost savings and carbon footprint reduction benefits that the transit authority used to demonstrate sustainability outcomes to its municipal funding stakeholders.

Pantograph Charger Market Key Players:

-

ABB

-

Siemens

-

Schunk Transit Systems

-

Heliox

-

Kempower

-

Wabtec

-

Medha

-

Dekon Power

-

ChargePoint

-

Dalian Luobinsen

-

Vector Informatik

-

SETEC Power

-

Valmont

-

Comeca

-

Hangzhou Aoneng

-

Ekoenergetyka-Polska

-

Furrer + Frey

-

Alstom

-

CRRC

-

Bombardier

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 4.66 Billion |

| Market Size by 2035 | USD 48.00 Billion |

| CAGR | CAGR of 26.29% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Charger Type (Single-Arm Pantograph Chargers, Dual-Arm Pantograph Chargers, Roof-Mounted Pantograph Chargers, and Side-Mounted Pantograph Chargers) • By Power Rating (< 150 kW (Low-Power), 150-350 kW (Mid-Power), 350-600 kW (High-Power), and > 600 kW (Ultra-High-Power)) • By Application (Public Transit Vehicles (Electric Buses/Trams), Rail Transit (Electric Trains/Light Rail), Commercial EV Fleets (Logistics & Delivery Vehicles), and Industrial & Depot Charging (Warehouses, Bus Depots)) • By End-User (Transit Authorities & Municipal Operators, Private Fleet Operators (Logistics & Delivery), Commercial EV Charging Infrastructure Providers, and Industrial & Enterprise Facility Owners) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | ABB, Siemens, Schunk Transit Systems, Heliox, Kempower, Wabtec, Medha, Dekon Power, ChargePoint, Dalian Luobinsen, Vector Informatik, SETEC Power, Valmont, Comeca, Hangzhou Aoneng, Ekoenergetyka‑Polska, Furrer + Frey, Alstom, CRRC, Bombardier. |

Frequently Asked Questions

Asia Pacific led the Pantograph Charger Market in 2025 with a 44.91% share.

Roof-Mounted Pantograph Chargers dominated the Pantograph Charger Market with a 32.18% share in 2025.

Key drivers include large-scale public transit bus fleet electrification mandates, commercial EV fleet depot charging demand, zero-emission transport policy commitments across major economies, and the operational efficiency advantages of automatic high-power pantograph charging over manual plug-in alternatives for fleet applications.

The Pantograph Charger Market size was USD 4.66 Billion in 2025 and is projected to reach USD 48.00 Billion by 2035.

The Pantograph Charger Market is expected to grow at a CAGR of 26.29% from 2026-2035.

Get in Touch