Passive Radar Market Report Scope & Overview:

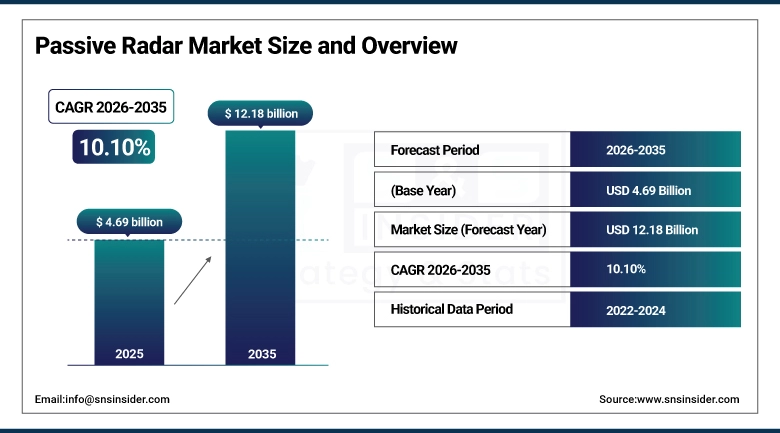

The Passive Radar Market size is valued at USD 4.69 Billion in 2025 and is projected to reach USD 12.18 Billion by 2035, growing at a CAGR of 10.10% during the forecast period 2026–2035.

The analysis report on the Passive Radar Market offers a detailed analysis of the dynamics, technology, and operational applications. The modernization of defense, increasing stealth detection requirements, and the growing need for integrating passive radar into civil aviation and homeland security are factors that are boosting the Passive Radar Market with high growth rates during 2026-2035.

The operational units for passive radar crossed thousands in 2025, owing to increasing defense requirements, border surveillance, and the need for cost-effective, non-emitting surveillance systems.

Market Size and Forecast:

-

Market Size in 2025: USD 4.69 Billion

-

Market Size by 2035: USD 12.18 Billion

-

CAGR: 10.10% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Passive Radar Market - Request Free Sample Report

Passive Radar Market Trends:

-

Modernization initiatives for defense systems have been emphasizing passive radar systems for stealth detection and border surveillance.

-

Civil aviation authorities have been using passive radar systems for better air traffic control.

-

Homeland security agencies have been utilizing passive radar systems for UAV detection and urban surveillance.

-

Multi-static and passive coherent location systems have been popularizing next-gen radar systems.

-

AI-based signal processing techniques have been changing the face of passive radar systems.

-

Space-based passive radar systems have been seen as a high-growth market for satellite-based surveillance.

-

Miniaturization techniques have been making passive radar systems more portable for various applications.

-

Sustainability and cost-effectiveness have been impacting procurement decisions for passive radar systems over traditional active radar systems.

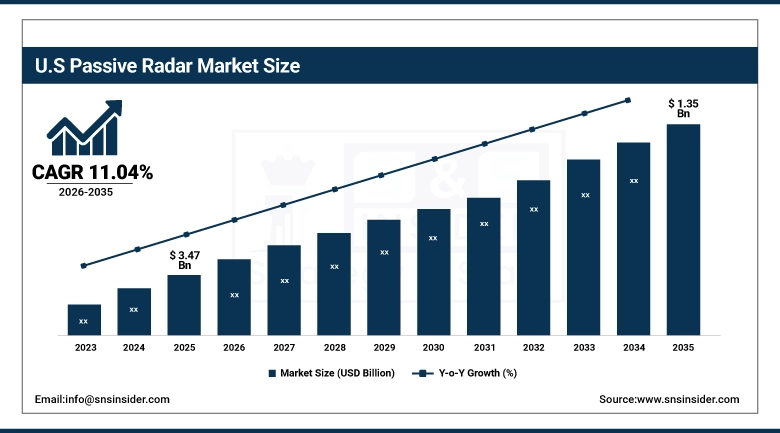

U.S. Passive Radar Market Insights:

U.S. Passive Radar Market is expected to grow at a CAGR of 11.04% and reach USD 3.47 Billion in 2035 from USD 1.35 Billion in 2025. The market is expected to grow due to increasing defense modernization programs, increasing need for stealth detection, high acceptance of advanced multi-static and passive coherent location technologies, and increasing focus on developing innovative AI-enabled, airborne, naval, and space-based radar systems.

Passive Radar Market Growth Drivers:

-

Increasing defense modernization programs and increasing demand for stealth detection are driving adoption of advanced passive radar technologies.

Increasing investments in defense procurement and escalating requirements for homeland security operations are some of the major factors propelling the market for Passive Radar Market. Defense departments, civil aviation authorities, and border security forces worldwide have been increasingly using highly advanced radar systems, including multi-static, airborne, naval, and space-based systems, to improve overall situational awareness and counter various new-age security threats.

More than 58% of defense and security departments in the U.S. have been utilizing highly advanced passive radar systems in 2025 to enhance stealth detection, border security operations, and UAV detection.

Passive Radar Market Restraints:

-

Higher R&D costs and integration complexities act as barriers for the wider adoption of passive radar systems.

Higher investment in signal processing, multi-static systems, and even AI-based systems act as barriers for various defense and civil departments. Interoperability issues with existing active systems, low adoption rates in the commercial sector, and high technical expertise required for operating passive systems act as restraints for the Passive Radar Market.

Delays in adopting passive systems for various departments in the civil aviation sector, where more than 42% of departments faced issues in adopting passive systems in 2025, act as restraints for market expansion.

Passive Radar Market Opportunities:

-

Expanding homeland security and border surveillance requirements are opening opportunities for passive radar adoption.

Increased demand for non-emitting, cost-effective surveillance technologies has opened opportunities in urban surveillance, anti-UAV operations, and coastal surveillance. Civil aviation authorities and space organizations are increasingly exploring opportunities in incorporating passive radar technologies into air traffic management and satellite surveillance operations. Advancements in AI-driven signal processing, digital twin technologies, and interoperability between domains are opening opportunities for more advanced applications, enhancing operational efficiency and effectiveness.

Over 46% of new defense and homeland security projects initiated in 2025 in the U.S. incorporated passive radar technologies, increasing surveillance capabilities and countering aerial threats.

Passive Radar Market Segmentation Analysis:

-

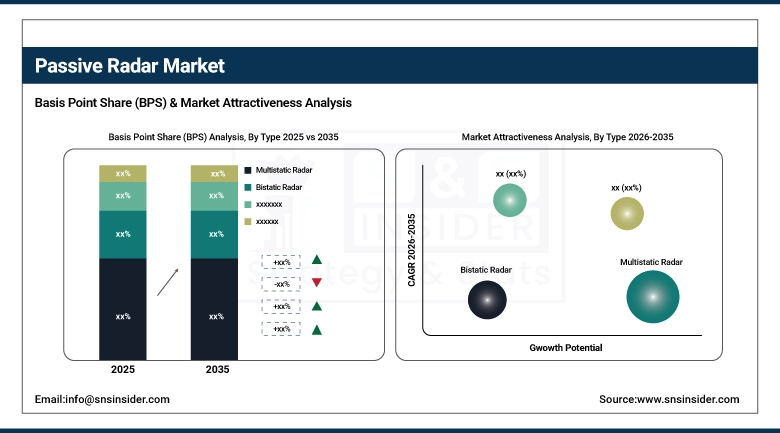

By Type, Multistatic Radar held the largest market share of 34.38% in 2025, while they are also expected to grow at the fastest CAGR of 12.81% during 2026–2035.

-

By Frequency Band, L-band dominated with 28.54% market share in 2025, whereas S-band are projected to record the fastest CAGR of 12.07% through 2026–2035.

-

By Platform, Ground-Based accounted for the highest market share of 39.82% in 2025, while Airborne are expected to grow at the fastest CAGR of 12.69% during the forecast period.

-

By Application, Defense & Military dominated with a 59.67% share in 2025, while Homeland Security are anticipated to expand at the fastest CAGR of 13.62% through 2026–2035.

-

By Component, Receivers held the largest share of 29.67% in 2025, while Processors & Software are expected to grow at the fastest CAGR of 13.85% during the forecast period.

By Type, Multistatic Radar Dominates While Also Emerging as the Fastest‑Growing Segment:

Multistatic Radar Systems are at the dominating the market in 2025 due to the proven track record of these systems in stealth detection and awareness. Their ability to use multiple transmitters and receivers has made them the most popular and widely accepted technology in the field of surveillance.

Multistatic Radar Systems are the fastest-growing segment of the market due to the increasing demand for these systems and the use of UAVs and space-based systems with these systems. Their use is increasing rapidly in the field of surveillance and in the modernization of the defense sector, making it the top and the fastest-growing segment of the market.

By Frequency Band, L‑band Dominates While S‑band Emerges as the Fastest‑Growing Segment:

L-band Radar Systems were in dominating position, and this was due to the effectiveness of such radar systems in long-range surveillance, air traffic control, and defense activities. The ability of such radar systems to detect stealth aircraft has made them a favorite among military and aviation organizations.

S-band radar systems are growing the fastest, and this has been attributed to the growing need for improved maritime surveillance, weather monitoring, and UAV detection radar systems. The use of such radar systems has grown rapidly in 2025, especially in naval defense activities and homeland security, and therefore they are growing the fastest in the passive radar market.

By Platform, Ground‑Based Systems Dominate While Airborne Based Platforms Grow Rapidly:

Ground-Based Radar Systems Segment held the dominated share in the market due to the effectiveness of these systems in surveillance, air defense, and homeland security applications, which are deployed in military bases across the world. The number of operational deployments of these systems was in excess of several hundred units, indicating the high degree of acceptance among defense agencies.

Airborne Based Radar platforms are the fastest-growing segment in the market due to the rising need for stealth detection, UAV surveillance, and satellite surveillance, which has seen the adoption of these platforms in the market in large numbers in 2025.

By Application, Defense & Military Dominates While Homeland Security Emerges as the Fastest‑Growing Segment:

Defense and Military Applications was at the dominated position, given its importance in stealth detection, missile defense, and surveillance operations. Passive radar systems have been widely adopted in various forms within air defense systems, naval forces, and strategic locations, demonstrating a high level of trust in technology to boost national security.

Homeland security is an area where passive radar systems have been fastest growing, demonstrating its importance in providing security for urban infrastructure and supporting law enforcement operations. The increasing use of passive radar in counter‑UAV missions and border surveillance highlights its expanding role in safeguarding national security and enhancing situational awareness across critical regions.

By Component, Receivers Dominate While Processors & Software Emerge as the Fastest‑Growing Segment:

Receivers segment is dominating the market, given their importance in receiving signals from external transmitters, thus facilitating passive detection without radiation. Their reliability in defense and homeland security operations has made them the backbone of passive radar, with widespread use in ground-based and airborne configurations.

Processors & Software segment has been witnessing fastest growth, attributed to increasing needs for advanced signal processing, AI-driven detection, and real-time data integration. The segment gained traction with defense agencies and aviation authorities seeking better accuracy, automation, and integration, thus solidifying their position as the fastest-growing segment in passive radar.

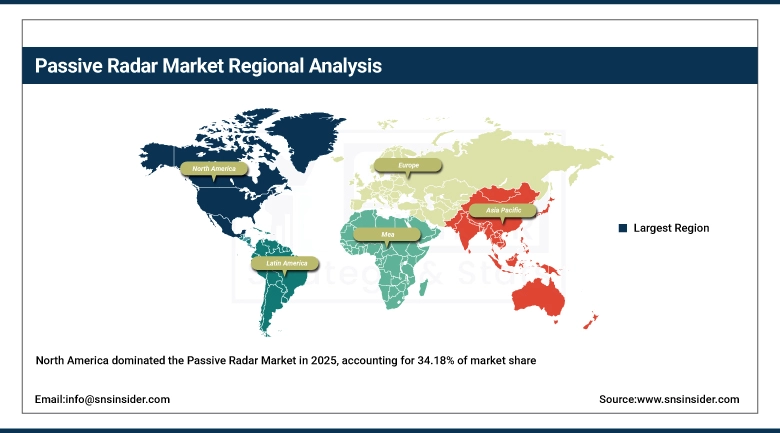

Passive Radar Market Regional Analysis:

North America Passive Radar Market Insights:

The North America Passive Radar Market is a highly developed market with a share of 34.18%, owing to the high modernization rate of defense systems and the presence of a highly developed surveillance system in the U.S. and Canada. The high rate of adoption of ground-based and airborne radar systems by defense organizations is a major driving factor for the North American passive radar market. The increasing need for stealth technology, border surveillance, and countering UAVs, coupled with the increasing investment rate in AI-based radar technologies, is also driving the North American passive radar market.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. Passive Radar Market Insights:

The U.S. Passive Radar Market is driven by significant defense procurement programs, advanced requirements for homeland security, and the use of radar technology for multi-domain operations. The increasing need for stealth technology, UAV surveillance, and border security is also driving the U.S. Passive Radar Market, making the U.S. the largest market for North America, followed by Canada, with significant opportunities for sustained growth through 2035.

Asia‑Pacific Passive Radar Market Insights:

The Asia Pacific passive radar market is witnessing fastest growth with a CAGR of 11.34%, driven by increasing defense spending, border surveillance, and development of indigenous radar technologies. Countries such as China, India, and Japan are adopting advanced multi-static and airborne radar technologies to enhance stealth detection capabilities and counter unmanned aerial vehicle threats. The rising trend of collaborations between defense organizations and technology developers, along with their integration into civil aviation, further emphasizes the growth prospects in this region.

China Passive Radar Market Insights:

The China Passive Radar Market is influenced by high government investment in defense modernization and indigenous technology development. The widespread adoption of passive radar technology in air defense, naval, and satellite surveillance capabilities underscores the country’s focus on improving stealth technology and multidomain warfare capabilities. The rapid evolution of AI technology for radar integration and UAV platforms cements China’s position as a leader in the Asia Pacific region.

Europe Passive Radar Market Insights:

The Europe Passive Radar Market has a positive outlook due to the existing defense infrastructure and ongoing modernization programs in NATO countries. The use of passive radar in ground-based and airborne platforms is high, and stealth detection using multi-static radar is gaining importance. Homeland security applications and joint R&D activities among European defense companies also boost the market growth rate.

Germany Passive Radar Market Insights:

The market for Passive Radar in Germany is driven by advanced military procurement strategies and investment in local radar technologies. Its use in air defense and civil aviation systems highlights Germany’s dominance in radar innovation in Europe. Continuous investment in AI-based signal processing and electronic warfare further highlights Germany’s importance in the European radar market.

Latin America Passive Radar Market Insights:

The Latin America Passive Radar Market is a new and growing market, driven by the increasing need for border surveillance, maritime surveillance, and homeland security. Countries such as Brazil and Mexico are gradually embracing the use of passive radar technology to improve defense capabilities. The lack of infrastructure and financial constraints are still major challenges, but the increasing ties with international defense suppliers are creating new opportunities for the market to grow.

Middle East & Africa Passive Radar Market Insights:

The Middle East and Africa Passive Radar Market is growing, and this growth can be attributed to increased military expenditure, geopolitical instability, and a growing need for advanced surveillance tools. The use of passive radar has been prominent in border security and UAV detection, especially in Gulf countries. Efforts to build local radar technologies and partner with international defense companies are further adding to the strategic importance of passive radar in the region.

Passive Radar Market Competitive Landscape:

Leonardo is an aerospace and defense company based in Italy and is considered to be one of the major players in the radar market, especially with its high-tech passive and active radars in the domain of air defense, naval surveillance, and border control. The company is well supported by its high investment in R&D and manufacturing capabilities, and Leonardo is moving ahead with the development of the latest technologies in the domain of radars, especially multi-static and space-based radars.

-

In May 2025, Leonardo advanced its Kronos radar family with enhanced passive detection modules, supporting air defense modernization programs in Italy and allied nations.

Thales Group is a major French defense and aerospace firm with a major presence in the radar industry, especially through its Ground Master and Sea Fire family of radars, which combine passive detection and multi-mission capabilities. The breadth of Thales' product range underscores its focus on versatility, cybersecurity, and interoperability, and its strong partnerships with NATO and other defense agencies across Europe. Thales is heavily committed to digital radars, AI-based signal processing, and sustainable production, guaranteeing its future success and viability, especially in defense and civil aviation applications.

-

In June 2025, Thales expanded its Ground Master radar applications to include homeland security and UAV detection, reinforcing its leadership in multi‑domain surveillance.

Raytheon Technologies (U.S.) is a leader in the defense and aerospace industries, holding the largest market share in the radar market, which includes the company's Passive Radar Solutions, designed for stealth, missile defense, and air traffic control. The company's product portfolio focuses on advanced sensor fusion, long-range detection, and its inclusion in the U.S. defense modernization strategies. The company's strong supply chain, extensive clinical-grade testing in defense conditions, and continuous investment in AI-enabled radar solutions drive the company's growth and success.

-

In July 2025, Raytheon advanced its SPY‑6 radar family with passive detection enhancements, strengthening U.S. Navy capabilities in maritime surveillance and missile defense.

Passive Radar Market Key Players:

Some of the Passive Radar Market Companies are:

-

Leonardo

-

Thales Group

-

Raytheon Technologies

-

Lockheed Martin

-

L3Harris Technologies

-

Hensoldt Holding

-

Saab AB

-

Indra Sistemas

-

Northrop Grumman

-

BAE Systems

-

SRC Inc.

-

OMNIPOL

-

Rohde & Schwarz

-

Ramet

-

Elbit Systems

-

Israel Aerospace Industries (IAI)

-

General Dynamics

-

Airbus Defence and Space

-

Collins Aerospace

-

Bharat Electronics Limited (BEL)

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 4.69 Billion |

| Market Size by 2035 | USD 12.18 Billion |

| CAGR | CAGR of 10.10% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Multistatic Radar, Bistatic Radar, Passive Coherent Location (PCL), Others), • By Frequency Band (L-band, S-band, C-band, X-band, Others) • By Platform (Ground-Based, Airborne, Naval, Space-Based, Others), • By Application (Defense & Military, Homeland Security, Civil Aviation, Disaster Monitoring & Commercial, Others) • By Component (Receivers, Antennas, Processors & Software, Transmitters (external signals), Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Leonardo, Thales Group, Raytheon Technologies, Lockheed Martin, L3Harris Technologies, Hensoldt Holding, Saab AB, Indra Sistemas, Northrop Grumman, BAE Systems, SRC Inc., OMNIPOL, Rohde & Schwarz, Ramet, Elbit Systems, Israel Aerospace Industries (IAI), General Dynamics, Airbus Defence and Space, Collins Aerospace, Bharat Electronics Limited (BEL). |

Frequently Asked Questions

High R&D costs, integration with existing defense infrastructure, and slower adoption in commercial sectors remain key challenges, alongside geopolitical uncertainties affecting defense budgets.

Homeland security and civil aviation are the fastest-growing segments, with CAGRs of 13.62%, fueled by demand for UAV detection and air traffic monitoring.

Defense and military applications dominate, accounting for 59.67% of market share, with passive radar widely used for stealth detection and border surveillance.

Asia-Pacific is the fastest-growing region with CAGR of 11.34%, driven by rising defense budgets in countries such as China and India, along with increasing adoption in civil aviation.

North America currently holds the largest share of 34.18% due to strong defense modernization programs and homeland security investments.

Get in Touch