Payment Security Market Size & Overview:

The Payment Security Market was valued at USD 25.9 Billion in 2023 and is expected to reach USD 91.3 Billion by 2032, growing at a CAGR of 15.07% from 2024-2032.

The growing volume of digital transactions over the past few years is fuelling the payment security market, which has witnessed rapid growth lately. Over the past few years, online payment transactions have multiplied — e-commerce solutions, mobile payment applications, and contactless payment systems handle millions of daily transactions. Digital payment transactions are estimated to be over 900 billion globally in 2023, proving that cashless is the way to go ever since it started to be prominent. At a more strategic level, organizations around the globe have reported investing heavily, more than 70% in advanced payment security technologies like encryption and even fraud detection systems to combat the risks of Cyber-attacks and data breaches.

To get more information on Payment Security Market - Request Free Sample Report

The increasing occurrence of cyber incidents only emphasizes the importance of a strong security posture. According to reports, financial fraud with digital payments has gone up by 25% on a year-over-year basis leading to businesses opting for securing their payment infrastructure.

Consumer behavior is changing at a rapid pace, with surveys indicating that over 80% of consumers prefer secure, non-cash, non-physical transactions compared to cash or card-based transactions. Similarly, an increasing number of people have also adopted mobile wallets, which have seen a 30% growth each year, propelled by convenience and the assumed safety of transacting in a contactless manner. More than 50% of businesses have implemented payment security protocols based on global standards like PCI DSS over the past five years.

Another major driver of growth is the rising prevalence of e-commerce and mobile payment platforms. Following the meteoric rise of e-commerce sales, which surpassed five trillion dollars worldwide in 2023, the demand for secure payment gateways has grown commensurately. Along with that, the utilization of real-time payment systems, which grew by 35% over the past year in different regions, demonstrates the increasing importance of the speed and safety of digital transactions. with the enormous surge in digital payment volumes, the rising risk of cyberattacks, and the need for consumers for a secure and continuous transaction experience, the payment security market is currently growing. All these trends emphasize the need for constant innovation and investment in payment security technologies to facilitate a growing digital economy.

Payment Security Market Dynamics

Drivers

-

Innovations in encryption, tokenization, and AI-powered fraud detection enhance payment security.

Cutting-edge technological advancements in encryption, tokenization, and AI-powered fraud detection are revolutionizing the space by providing innovative approaches to the protection of sensitive information in payment technologies. Transmitted payment information is kept safe with the help of an encryption process, so it is hardly possible for hackers to read or use it. As e-commerce and digital wallets continue to drive activity in online and mobile transactions, this technology is fundamental to safeguarding the data exchanged. The use of tokenization improves protection by using a unique identifier (token) to substitute sensitive payment information, such as card numbers so that the payment information has no value outside of a specific transaction. Because the tokens will not work if a system is compromised, this greatly reduces the risk of a data breach. This has led to tokenization becoming a key element in secure payment processing, particularly for industries with high transaction volumes.

AI-driven fraud detection provides an extra layer of protection by analyzing patterns behind transactions in real time. By using machine learning, these systems identify outliers and alert potential fraudulent activity before any transaction takes place, reducing financial damage, and increasing confidence in digital payment platforms. As time progresses, AI systems become more efficient by learning from the previous instances of fraud that were attempted. Combined, these technologies tackle the growing threats of both cyber threats and fraud in the payment security market. They ensure that they can deliver strong protection for a compliant business and confidence for a customer, driving the global acceleration of payments.

-

Increasing incidents of financial fraud and data breaches are compelling organizations to adopt advanced payment security solutions.

-

The surge in e-commerce, mobile payments, and contactless payment methods is driving the demand for secure payment systems.

Restraints

-

The expense of deploying advanced payment security technologies can be prohibitive for small and medium-sized enterprises (SMEs).

Adopting new technology for secure payment, like encryption, tokenization, and machine-learning-based fraud detection, can be expensive and difficult for small and medium-sized businesses to implement. This includes everything from the cost of the initial hardware and software to the ongoing cost of updating, maintaining, and training staff to use systems. The high-cost nature of such technologies can be financially burdensome for SMEs, as the resources dedicated to this technology need to be balanced against other areas of operation. It can be complicated to embed these systems into pre-existing payment ecosystems, usually requiring an experienced team to work on.

This economic barrier comes at a time when cybercriminals are making increasing efforts to take advantage of small and medium enterprises that have less robust security in place relative to larger corporations. While thinking that strong payment security is imperative, so many small and medium businesses have no other option but to rely on outdated or inferior systems, which exposes them to data breaches and fraudulent transactions. However, such vulnerabilities not only threaten their operations but also undermine customer trust which is a pivotal element of their growth and sustainability. Addressing this issue requires the payment security market to provide scalable, affordable solutions that are specifically designed for SMEs. Furthermore, programs such as financial aid or subsidies can close the affordability gap, making it possible for businesses of all sizes to protect sensitive payment data and facilitate a more secure digital economy.

-

Limited understanding of payment security solutions among smaller businesses hinders adoption.

-

A shortage of cybersecurity professionals affects the effective implementation and management of security systems.

Segment Analysis

By Solution

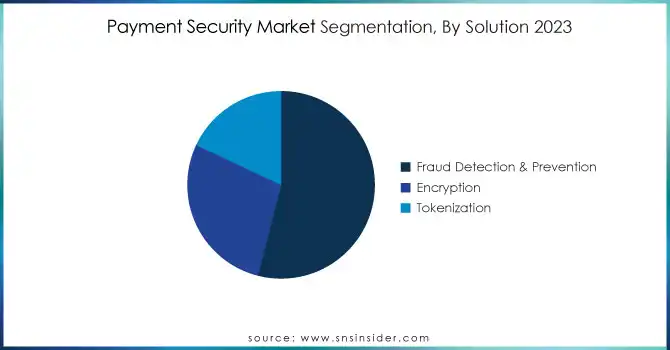

In 2023, The fraud detection & prevention segment dominated the market and represented a revenue share of more than 54%. Fraud can be considered to be the biggest threat to the payment system and data security. Fraud can take many forms such as card-not-present fraud, identity fraud, account takeover, and social engineering attacks. An essential part of payment security is fraud detection and prevention solutions since payment systems are now more advanced than ever, and moving towards the online world comes with the risk of fraud.

The tokenization segment is expected to see substantial growth during the forecast period. Tokenization of payment methods improves security and usability when transacting between different devices: secure point of sale, on-the-go payments, and traditional online shopping and in-app payment systems. Payment tokenization substitutes sensitive payment card information — the card number, expiration date, and other crucial data — with a special identifier called a token. The token is used for payment processing and can be stored securely on the smartphone, wearables, or computers to make an instant payment over a channel and platform.

By Enterprise Size

This large enterprise segment dominated the market and accounted for over 69% of the revenue in 2023. Payment security is another big part of a business, it is important to make sure everything is secure enough for customer data handling and deal with payment fraud. Big businesses usually have better funds to spend on the latest security tools and systems. Moreover, very enterprises also have a greater number of transactions and customers which raises the degree of fraud and cyber threat. Therefore, they tend to focus on investing in comprehensive security solutions to safeguard their business and customers.

The SME segment is expected to register the fastest CAGR during the forecast period. owing to the increasing trend of utilizing digital payment solutions including mobile payments, e-commerce platforms, and online payment gateways to make the payment process seamless and cover a wide customer segment across all businesses.

By Platform

In 2023, the POS-based/mobile-based segment dominated the market with a significant revenue share of more than 59%. Mobile-based payment systems, usually integrated with various point of sale systems are common in retail, hospitality, healthcare, transportation, and other industries. The systems allow merchants and consumers to make their payments quickly and securely through mobile devices, tablets, and POS terminals. Security threats. POS-based/mobile-based payment systems are vulnerable to plenty of security threats such as card skimming, data breaches, malware attacks, and social engineering scams. Consequently, the technology for payment security has advanced; solutions providers like those offering encryption, tokenization, fraud detection, or multi-factor authentication now offer various methods of protection over such systems and payment transactions.

The web-based segment is expected to grow at a significant cagr over the forecast period. This growth in the segment is driven by the rising adoption of online payments and e-commerce. An online payment system allows consumers to do PHHS and other transactions to pay online with their desktop or mobile device without putting anything in the store or designated payment terminal. Such comfort has propelled online exchanges widely and web-based payment arrangements have turned into the core of the whole payment biological system.

Regional Landscape

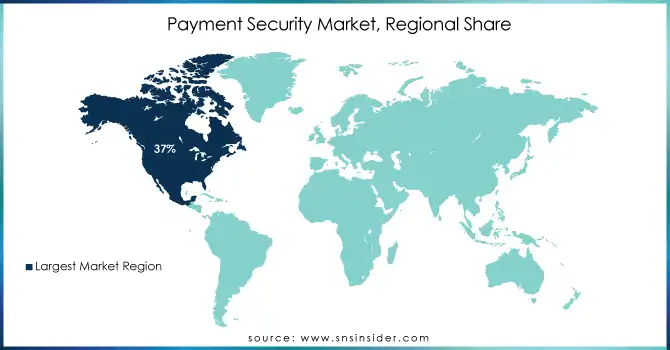

In 2023, North America dominated the payment security market and represented a revenue share of more than 37%. With the presence of global payment security providers, like Visa Inc., U.S. Bancorp, and Mastercard, North America is a prominent market for payment security. The North American regional market growth is also being accelerated witnessing the trend towards digital payment for payment at malls/restaurants and the availability of wider opportunities for the vendors and providers in the region.

Asia Pacific is expected to be the fastest-growing market during the forecast period. The growth of this region is primarily attributed to the rising regulatory requirements and compliance standards regarding payment security. The growth of the Asia Pacific market is maintained by the rise of strict regulations and guidelines for payment security such as in China, India, and Japan.

Get Customized Report as per Your Business Requirement - Enquiry Now

Key Players:

Prominent players in the market are Mastercard, Paypal Holdings, Inc., Visa Inc., American Express Company, Fiserv, Inc., Worldline S.A., Thales Group, NCR Corporation, Ingenico, Verifone, Inc., CyberSource Corporation, ACI Worldwide, Inc., Stripe, Inc. And others in the final report.

Recent development

March 2024: PayPal unveiled a new multi-factor authentication (MFA) system to enhance the security of its digital wallet services. The system combines traditional passwords with biometric authentication and one-time passcodes to ensure secure transactions.

|

Report Attributes |

Details |

|

Market Size in 2023 |

USD 25.9 Billion |

|

Market Size by 2032 |

USD 91.3 Billion |

|

CAGR |

CAGR of 15.07 % From 2024 to 2032 |

|

Base Year |

2023 |

|

Forecast Period |

2024-2032 |

|

Historical Data |

2020-2022 |

|

Report Scope & Coverage |

Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

|

Key Segments |

• By Platform (Web Based, POS Based/Mobile Based) |

|

Regional Analysis/Coverage |

North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

|

Company Profiles |

Mastercard, Paypal Holdings, Inc., American Express Company, Fiserv, Inc., Worldline S.A., Thales Group, NCR Corporation, Ingenico (a Worldline brand), Verifone, Inc., CyberSource Corporation (a Visa Solution), ACI Worldwide, Inc., Stripe, Inc. |

|

Key Drivers |

• Increasing incidents of financial fraud and data breaches are compelling organizations to adopt advanced payment security solutions. |

|

Market Opportunities |

• Limited understanding of payment security solutions among smaller businesses hinders adoption. |

Frequently Asked Questions

The Payment Security Market was valued at USD 25.9 Billion in 2023 and is expected to reach USD 91.3 Billion by 2032, growing at a CAGR of 15.07% from 2024-2032.

The CAGR of the Payment Security Market during the forecast period is 15.07% from 2024-2032.

Asia-Pacific is expected to register the fastest CAGR during the forecast period.

Increasing incidents of financial fraud and data breaches are compelling organizations to adopt advanced payment security solutions.

Limited understanding of payment security solutions among smaller businesses hinders adoption.

Get in Touch